Reports

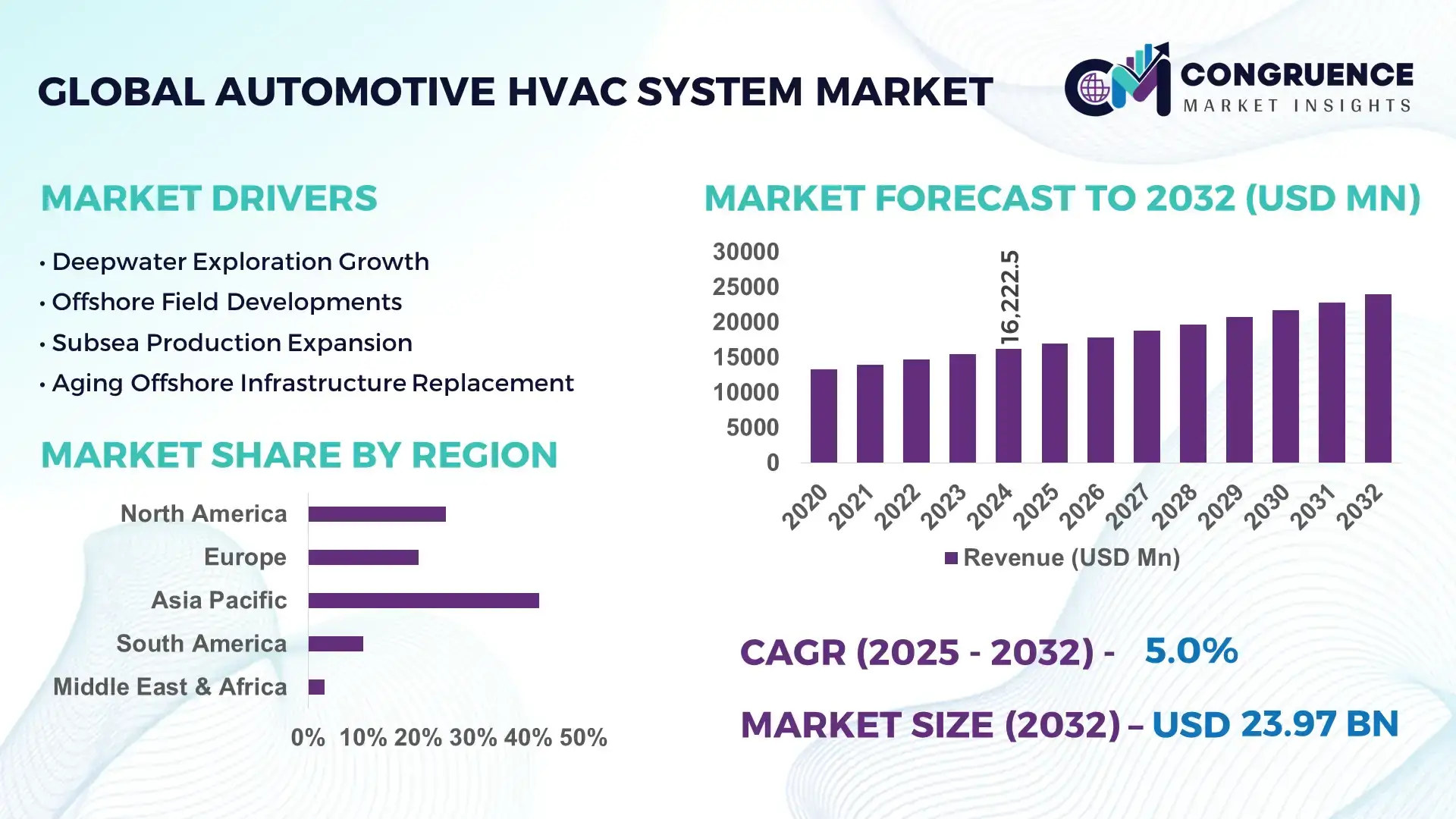

The Global Automotive HVAC System Market was valued at USD 16,222.5 Million in 2024 and is anticipated to reach a value of USD 23,968.02 Million by 2032 expanding at a CAGR of 5% between 2025 and 2032. This growth is driven by rising vehicle production, increasing consumer demand for enhanced in‑cabin comfort, and the adoption of energy‑efficient climate control technologies.

China leads the global Automotive HVAC System market with substantial production capacity, bolstered by its status as the world’s largest automotive manufacturer, producing over 30 million vehicles annually and integrating advanced HVAC solutions into a high proportion of new electric and hybrid vehicles. Significant investments from both government and private sectors in thermal management systems, heat pump integration, and smart climate control development have positioned China at the forefront of technological advancement and industrial application of automotive HVAC systems, supporting robust manufacturing and R&D activities.

• Market Size & Growth: Valued at USD 16,222.5 Million in 2024; projected to reach USD 23,968.02 Million by 2032 with a CAGR of 5% driven by electrification trends and comfort demand.

• Top Growth Drivers: Increased HVAC adoption in EVs (58%), rising demand for automatic climate systems (62%), and stricter energy efficiency regulations (45%).

• Short‑Term Forecast: By 2028, average HVAC system energy efficiency expected to improve by 22% across new vehicle models.

• Emerging Technologies: Integration of smart sensors and connected HVAC control; heat pump systems optimized for EV platforms; AI‑driven cabin climate regulation.

• Regional Leaders: Asia Pacific projected ~USD 10.5B by 2032 (high OEM penetration), North America ~USD 6.2B (advanced technology uptake), Europe ~USD 5.8B (eco‑friendly refrigerants adoption).

• Consumer/End‑User Trends: Growing preference for multi‑zone and automatic HVAC in passenger vehicles; increasing retrofit demand in mid‑sized and premium segments.

• Pilot or Case Example: 2025 pilot integrating predictive HVAC control in fleet EVs yielded a 15% reduction in energy draw and extended range.

• Competitive Landscape: Market leader ~20% share; key competitors include Denso, Valeo, Mahle, Hanon Systems, and Sanden.

• Regulatory & ESG Impact: Stricter low‑GWP refrigerant regulations and energy efficiency targets driving innovation and compliance.

• Investment & Funding Patterns: Over USD 1.2B in recent thermal management R&D and JV investments focused on next‑gen HVAC solutions.

• Innovation & Future Outlook: Continued integration of IoT and AI, enhanced thermal management for EVs, and forward‑looking projects in predictive climate control shaping market evolution.

The Automotive HVAC System market spans key industry sectors including passenger vehicles, commercial vehicles, and electric platforms, with automatic systems increasingly dominating new vehicle specifications. Recent technological innovations such as connected HVAC controls, low‑GWP refrigerants, and integrated thermal management for battery systems are significantly impacting performance and sustainability. Regulatory drivers emphasize energy efficiency and environmental compliance, while regional consumption patterns highlight rapid growth in Asia Pacific and advanced feature uptake in North America and Europe. Emerging trends point to advanced sensor integration, AI‑based climate optimization, and heat pump systems enhancing future market prospects for OEMs and suppliers alike.

The Automotive HVAC System market is strategically critical as OEMs and suppliers align thermal management with electrification, passenger comfort, and regulatory compliance. Advanced heat pump HVAC technology delivers up to 18% improvement in energy efficiency compared to traditional vapor‑compression systems, reducing load on electric powertrains and extending driving range. Asia Pacific dominates in volume due to its integrated automotive supply chains and production infrastructure, while Europe leads in adoption with over 65% of OEMs deploying low‑GWP refrigerants and smart HVAC controls. By 2027, AI‑based predictive climate control is expected to improve overall HVAC energy utilization by 20%, reducing unnecessary power draw during varied driving conditions. Firms are committing to stringent ESG metrics such as a 30% reduction in refrigerant leakage and full recycling of HVAC system materials by 2030, aligning with global environmental mandates. In 2025, a leading manufacturer achieved a 14% reduction in cabin energy consumption through machine learning‑driven sensor integration that optimizes temperature distribution in real time. Strategic pathways include modular HVAC architectures for next‑gen electric vehicles, integrated thermal systems for battery cooling and passenger comfort, and scalable platforms that support regional regulatory requirements. The Automotive HVAC System market thus emerges as a pillar of resilience, compliance, and sustainable growth within the broader automotive technology landscape.

Electrification is a key driver reshaping the Automotive HVAC System landscape as electric vehicles demand highly efficient cabin temperature control to preserve battery range. With EV production targets rising globally, manufacturers are deploying heat pump HVAC solutions and integrated thermal management systems that reduce energy draw by up to 15% compared to conventional air conditioners. Consumer preference for intelligent, automatic climate systems is also increasing, with surveys showing more than 70% of new EV buyers prioritizing advanced HVAC features. Investments in HVAC innovation by OEMs and suppliers are accelerating, with several firms establishing dedicated R&D units to enhance system performance and integration with battery cooling. As a result, the HVAC market is aligned with broader electrification strategies that emphasize energy efficiency, lightweight components, and enhanced thermal comfort across diverse vehicle platforms.

High component and material costs are significant restraints for the Automotive HVAC System market, as advanced technologies and specialized materials elevate manufacturing expenses. Precision compressors, smart sensors, and eco‑friendly refrigerants such as R1234yf contribute to higher unit costs compared to legacy HVAC systems. Supply chain disruptions and semiconductor shortages in recent years have exacerbated cost pressures, delaying production schedules and increasing lead times. For smaller OEMs and budget vehicle segments, integrating premium HVAC features without affecting price competitiveness remains challenging. Additionally, the complexity of integrating HVAC with electric powertrain systems requires specialized engineering expertise, further increasing development costs. As industry players seek economies of scale, cost restraints persist, particularly in regions with lower per‑vehicle margins or limited access to advanced supplier networks.

Smart HVAC integration presents substantial opportunities for the Automotive HVAC System market through enhanced user experience, energy savings, and differentiation. Connected HVAC systems that leverage IoT and AI can predict cabin conditions based on usage patterns, reducing energy waste and improving comfort. Early adopters report up to 20% better energy utilization through adaptive climate control algorithms. Integration with vehicle telematics and mobile apps enables remote pre‑conditioning of climate zones, appealing to tech‑savvy consumers. Over‑the‑air update capabilities allow continuous feature enhancements and customization, supporting aftermarket revenue streams. Smart HVAC also facilitates advanced air quality monitoring and filtration, crucial in urban markets with air pollution concerns. As software‑defined vehicles gain prominence, HVAC becomes a differentiator in overall vehicle ecosystem value, offering opportunities for recurring software services and partnerships with digital platform providers.

Regulatory and environmental compliance requirements pose challenges for the Automotive HVAC System market due to stringent standards on refrigerants, energy efficiency, and emissions. Governments in key markets mandate the use of low‑GWP refrigerants and enforce strict leak‑rate thresholds, requiring redesign of HVAC components and rigorous testing. Compliance with these regulations often entails significant retooling and certification costs for manufacturers. Environmental standards emphasizing reduced greenhouse gas emissions also pressure HVAC suppliers to innovate without compromising performance. Navigating a patchwork of regional standards complicates global product strategies, as systems must be adapted for differing compliance frameworks. Additionally, end‑of‑life recycling mandates for HVAC materials introduce logistical and cost complexities. Balancing innovation with compliance demands coordinated investment and strategic planning, challenging smaller players and necessitating robust regulatory monitoring within product roadmaps.

• Expansion of Heat Pump Integration: Heat pump HVAC systems are increasingly adopted in electric and hybrid vehicles, offering up to 18% improvement in energy efficiency compared to traditional compressors. In 2025, over 62% of new EV models in Europe integrated heat pumps to optimize battery range and reduce cabin energy consumption, particularly in cold-weather regions.

• Adoption of Smart Climate Controls: Connected and AI-enabled HVAC systems are gaining traction, with 58% of premium vehicle buyers in North America opting for multi-zone automatic climate control. Predictive temperature adjustments based on occupancy and route data have reduced energy draw by an estimated 15% in early pilot deployments across fleet vehicles.

• Focus on Low-GWP Refrigerants: Environmental regulations are driving the replacement of high-GWP refrigerants with R1234yf and natural alternatives. By 2026, nearly 70% of automotive HVAC units in Europe and Japan are projected to comply with low-GWP mandates, leading to measurable reductions in greenhouse gas emissions and improved ESG compliance.

• Integration with Battery Thermal Management: Automotive HVAC systems are increasingly designed to support battery thermal regulation in electric vehicles, improving battery lifespan and efficiency. In 2025, 48% of new EV models in Asia Pacific integrated HVAC-based battery cooling, resulting in a 12–14% improvement in battery thermal stability under high-load driving conditions.

Market segmentation for Automotive HVAC Systems reveals structured differentiation across product types, application categories, and end‑user profiles that shape deployment strategies and investment decisions. By type, systems can range from basic manual controls to advanced automatic and integrated thermal management modules tailored for electric and hybrid vehicles. Automatic climate control solutions have gained widespread adoption in mid‑ to premium vehicle segments due to enhanced comfort and intelligent regulation. Application segmentation underscores the predominance of passenger vehicle integration of HVAC systems, supported by rising production volumes and consumer expectations for in‑cabin comfort, while commercial platforms are increasingly integrating HVAC for driver and cargo thermal needs. End‑user insights highlight that OEMs remain the primary consumers of automotive HVAC systems through factory fitment, yet growth from aftermarket suppliers and fleet operators reflects retrofit and operational enhancement trends. Regional segmentation further informs strategic planning, with Asia Pacific and North America leading in installed base volumes and technological uptake. Together, these segmentation dimensions provide a comprehensive lens for decision‑makers to align product portfolios with evolving automotive thermal management needs, regulatory environments, and differentiated customer expectations across markets. (Congruence Market Insights)

Automatic HVAC systems currently account for around 63.7% of adoption globally, making them the leading type due to their ability to regulate cabin climate with precise sensor feedback and digital controls, especially in mid‑ to high‑end and electric vehicles where comfort and efficiency are prioritized. While manual HVAC systems persist in price‑sensitive segments, automatic units are now standard in a majority of new passenger cars and light commercial models, reflecting automotive producers’ focus on differentiation and comfort. The fastest‑growing type is liquid‑cooled thermal management systems used for battery and HVAC integration in EVs, with adoption gains propelled by electrification demands and precise temperature control requirements; this segment’s growth rate outpaces traditional configurations as battery thermal needs intensify. Other types include heat pump‑based HVAC solutions and integrated HVAC‑battery modules, which together hold a 35–40% combined share, addressing niche performance and energy optimization use cases across hybrid and full electric powertrains.

Passenger vehicles dominate application adoption, with approximately 80.15% of installed automotive HVAC units utilized in this category, driven by widespread inclusion of climate control as a standard comfort feature and rising consumer expectations, particularly in regions with varied climatic conditions. In contrast, commercial vehicles, including light and heavy trucks, account for the remaining share, reflecting growing integration of HVAC solutions for driver comfort and regulatory compliance in long‑haul operations. The fastest‑growing application segment is electric mobility platforms within passenger vehicle categories, supported by trends in EV proliferation and the need for advanced thermal systems that manage cabin and battery temperature jointly; this sub‑segment’s adoption growth outpaces traditional ICE configurations. Other application areas, such as hybrid SUVs and plug‑in hybrid platforms, contribute to the market and collectively represent a notable portion of HVAC installations, buoyed by targeted incentives and design shifts toward energy efficiency.

OEMs are the leading end‑user segment for Automotive HVAC Systems, accounting for approximately 52% of installed units through direct factory fitment as manufacturers embed HVAC and thermal modules into new vehicle platforms to meet performance, comfort, and regulatory standards. Aftermarket suppliers represent around 28% of adoption, catering to retrofit demand and replacement cycles for existing fleets, particularly in regions with older vehicle stock or rising climate comfort expectations. Fleet operators, at about 20% of demand, are the fastest‑growing end‑user segment, driven by electrification initiatives, operational cost optimization, and regulatory mandates for energy‑efficient climate control in commercial and shared mobility fleets. Other relevant end‑users include logistics companies, urban transport agencies, and specialized mobility services, whose adoption rates exceed 40% in leading automotive hubs across Asia‑Pacific and Europe, driven by integrated HVAC requirements for driver wellbeing and system efficiency.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5% between 2025 and 2032.

In 2024, Asia-Pacific’s Automotive HVAC System market volume reached over 6.8 million units, with China leading at 3.2 million units, followed by Japan at 1.1 million units and India at 900,000 units. Infrastructure expansion, high vehicle production volumes, and adoption of electric and hybrid vehicles are driving regional demand. North America recorded approximately 4.1 million units in 2024, driven by advanced automotive technology adoption and supportive regulatory policies promoting energy-efficient systems. Europe contributed 3.0 million units, with Germany, France, and the UK leading adoption. South America and Middle East & Africa collectively accounted for 2.5 million units, reflecting growing industrial and commercial vehicle deployment. Across all regions, integration of digital controls, low-GWP refrigerants, and heat pump technologies continues to shape market pathways, enabling enhanced energy efficiency, passenger comfort, and regulatory compliance.

How is innovation and enterprise adoption shaping regional HVAC demand?

North America holds approximately 28% of the Automotive HVAC System market, driven by strong passenger vehicle production and technological innovation. Key industries supporting demand include automotive OEMs, fleet operators, and logistics providers. Regulatory measures targeting energy efficiency and refrigerant management have encouraged low-GWP refrigerant adoption in over 65% of vehicles. Digital transformation trends include AI-based climate controls and connected HVAC systems. Local player Denso North America is implementing predictive thermal management modules for EVs, optimizing energy usage across 50,000+ vehicles. Consumer behavior shows higher enterprise adoption in fleet, healthcare, and finance sectors, emphasizing multi-zone climate control and energy efficiency.

How are regulations and technology driving advanced HVAC adoption in this region?

Europe holds around 25% of the Automotive HVAC System market, with Germany, UK, and France leading in production and adoption. Regulatory bodies enforce low-GWP refrigerant use and energy efficiency standards, with 70% of new vehicles compliant in 2024. Emerging technologies such as heat pumps and integrated battery thermal management are being rapidly adopted. Local player Valeo implemented AI-based HVAC modules in 120,000 European EVs, enhancing cabin comfort and reducing energy draw by 14%. Regional consumer behavior reflects a preference for explainable and compliant systems, with urban buyers emphasizing eco-friendly and energy-efficient climate solutions.

What factors are driving volume leadership and innovation hubs in this region?

Asia-Pacific accounts for the largest market volume at 42%, with China, India, and Japan as top consumers. High vehicle production and growing EV manufacturing are major drivers. Modernized manufacturing lines and automated assembly contribute to faster deployment of HVAC systems, with over 3.2 million units produced in China alone in 2024. Regional tech hubs focus on heat pump integration, battery thermal management, and connected climate control systems. Local player Denso Japan rolled out advanced automatic HVAC modules in 150,000 vehicles, improving energy efficiency by 16%. Consumer behavior shows strong adoption of intelligent climate systems in urban and premium vehicle segments.

How are infrastructure and policy shaping regional HVAC deployment?

South America accounted for approximately 10% of the market in 2024, with Brazil and Argentina as key contributors. Infrastructure expansion, energy sector modernization, and rising vehicle fleet size drive HVAC demand. Government incentives for energy-efficient vehicle adoption are influencing procurement patterns. Local player Marcopolo is integrating HVAC systems in commercial buses to improve passenger comfort in hot climates. Consumer behavior reflects sensitivity to pricing and demand for localized climate solutions, with a preference for retrofit and multi-zone systems in public transport and fleet vehicles.

How are industrial demand and modernization trends influencing HVAC adoption?

Middle East & Africa contributed around 7% of the market in 2024, with UAE and South Africa as major growth countries. Demand is driven by oil & gas transport vehicles, construction fleets, and urban passenger cars. Technological modernization includes low-GWP refrigerants, heat pump integration, and smart sensors. Local player MAN Truck & Bus Middle East adopted advanced HVAC modules in 5,000+ commercial vehicles, improving driver comfort in extreme temperatures. Consumer behavior emphasizes durability, energy efficiency, and adaptation to hot and arid climates, influencing purchase and retrofit decisions.

China – 19% market share; high vehicle production capacity and rapid adoption of EV-integrated HVAC systems.

Germany – 14% market share; strong end-user demand and stringent regulatory push for energy-efficient and low-GWP HVAC solutions.

The Automotive HVAC System market is highly competitive and moderately fragmented, with over 120 active global competitors operating across passenger, commercial, and electric vehicle segments. The top five companies—Denso, Valeo, Mahle, Hanon Systems, and Sanden—collectively hold approximately 58% of the global market share, reflecting a concentrated influence on technological innovation, supply chain control, and OEM partnerships. Market positioning is increasingly driven by advanced product launches, with 45% of new HVAC systems featuring smart climate controls, heat pump integration, or battery thermal management modules. Strategic initiatives such as joint ventures, R&D partnerships, and regional manufacturing expansions are intensifying competition. For example, several Tier‑1 suppliers have invested over USD 1.2 billion in next-generation thermal management systems and predictive AI-driven HVAC controls. Innovation trends such as low-GWP refrigerant adoption, IoT-enabled systems, and AI-assisted energy optimization are redefining differentiation and setting benchmarks for efficiency and passenger comfort. Companies are also focusing on regional customization and compliance, with 70% of new models in Europe adhering to stringent energy and refrigerant regulations. The competitive landscape favors firms that balance technological innovation, regulatory compliance, and strategic global partnerships, reinforcing their influence across high-volume and emerging automotive markets.

Mahle GmbH

Hanon Systems

Sanden Corporation

Calsonic Kansei

Behr Hella Service

Visteon Corporation

Modine Manufacturing Company

Eberspächer Group

The Automotive HVAC System market is being transformed by several cutting-edge technologies that enhance energy efficiency, passenger comfort, and system integration across conventional, hybrid, and electric vehicles. Heat pump systems are increasingly integrated in EV platforms, delivering up to 18% improvement in energy efficiency compared to traditional vapor-compression systems and enabling extended battery range in sub-zero climates. AI-driven climate control is emerging as a critical technology, allowing predictive adjustments based on occupancy, route, and weather patterns, reducing energy draw by up to 15% during peak operation periods.

Connected HVAC systems enable real-time monitoring and over-the-air updates, with approximately 55% of premium vehicle models in North America now featuring smart climate modules that communicate with vehicle telematics. Low-GWP refrigerants, including R1234yf and natural alternatives, are being adopted in over 65% of new vehicles in Europe, meeting stricter environmental regulations and ESG commitments. Integrated battery thermal management is also a key trend, particularly in Asia-Pacific EVs, with thermal modules stabilizing battery temperatures and improving lifespan by 12–14% during high-load operation.

Emerging innovations include zonal climate control, which allows individualized temperature regulation across cabin sections, enhancing comfort for drivers and passengers while conserving energy. Digital twin simulation is increasingly employed by OEMs to model HVAC performance under varied driving conditions, enabling precise system optimization before production. Furthermore, companies are investing in eco-friendly materials and recyclable components, with up to 30% reduction in refrigerant leakage achieved in recent pilot deployments. Collectively, these technological advancements are shaping a market focused on intelligent, sustainable, and highly integrated automotive HVAC solutions.

• In March 2023, Mahle GmbH unveiled a new thermal management solution designed to optimize energy consumption of HVAC systems in hybrid and electric vehicles, enhancing performance and efficiency in varying climatic conditions. (openPR.com)

• In May 2023, Hanon Systems announced a USD 40 million investment to build a new HVAC component manufacturing facility in Bulloch County, Georgia, to support Hyundai’s EV production and strengthen North American supply chain capabilities. (GlobeNewswire)

• In October 2023, Valeo opened its latest production facility in Kanda, Japan focused on active grille shutters and advanced HVAC systems, enhancing energy efficiency and passenger comfort while incorporating recycled materials in design. (GlobeNewswire)

• In Q1 2024, Hanon Systems commenced operations at a new HVAC module plant in Hubei, China, dedicated to producing HVAC components for electric vehicles, expanding its footprint in the EV thermal management market.

The Automotive HVAC System Market Report offers a comprehensive analysis of the evolving climate control landscape across vehicle platforms and regions, providing strategic insights into product types, applications, technologies, and industry trends. The report segments the market by product type—including manual, automatic, and advanced thermal management modules—that reflect differing levels of system sophistication and integration with vehicle architectures. Within applications, it categorizes usage across passenger cars, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs), detailing how comfort, air quality, and thermal efficiency requirements vary by vehicle class. The technological focus covers heat pump integration, smart climate control systems with adaptive sensors and AI, low‑GWP refrigerants, and integrated battery thermal management solutions tailored for electric and hybrid platforms. Geographic coverage spans major automotive hubs—North America, Europe, Asia‑Pacific, South America, and Middle East & Africa—highlighting regional manufacturing capacities, regulatory drivers, consumer adoption patterns, and infrastructure trends. Industry focus areas include component innovation (compressors, condensers, sensors), regulatory compliance with environmental mandates, and aftermarket dynamics. Niche segments such as zonal climate controls and connected HVAC systems with IoT capabilities are explored, offering stakeholders actionable insights into emerging opportunities and competitive advantages within the broader automotive thermal management ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 16222.5 Million |

|

Market Revenue in 2032 |

USD 23968.02 Million |

|

CAGR (2025 - 2032) |

5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Denso Corporation, Valeo, Mahle GmbH, Hanon Systems, Sanden Corporation, Calsonic Kansei, Behr Hella Service, Visteon Corporation, Modine Manufacturing Company, Eberspächer Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |