Reports

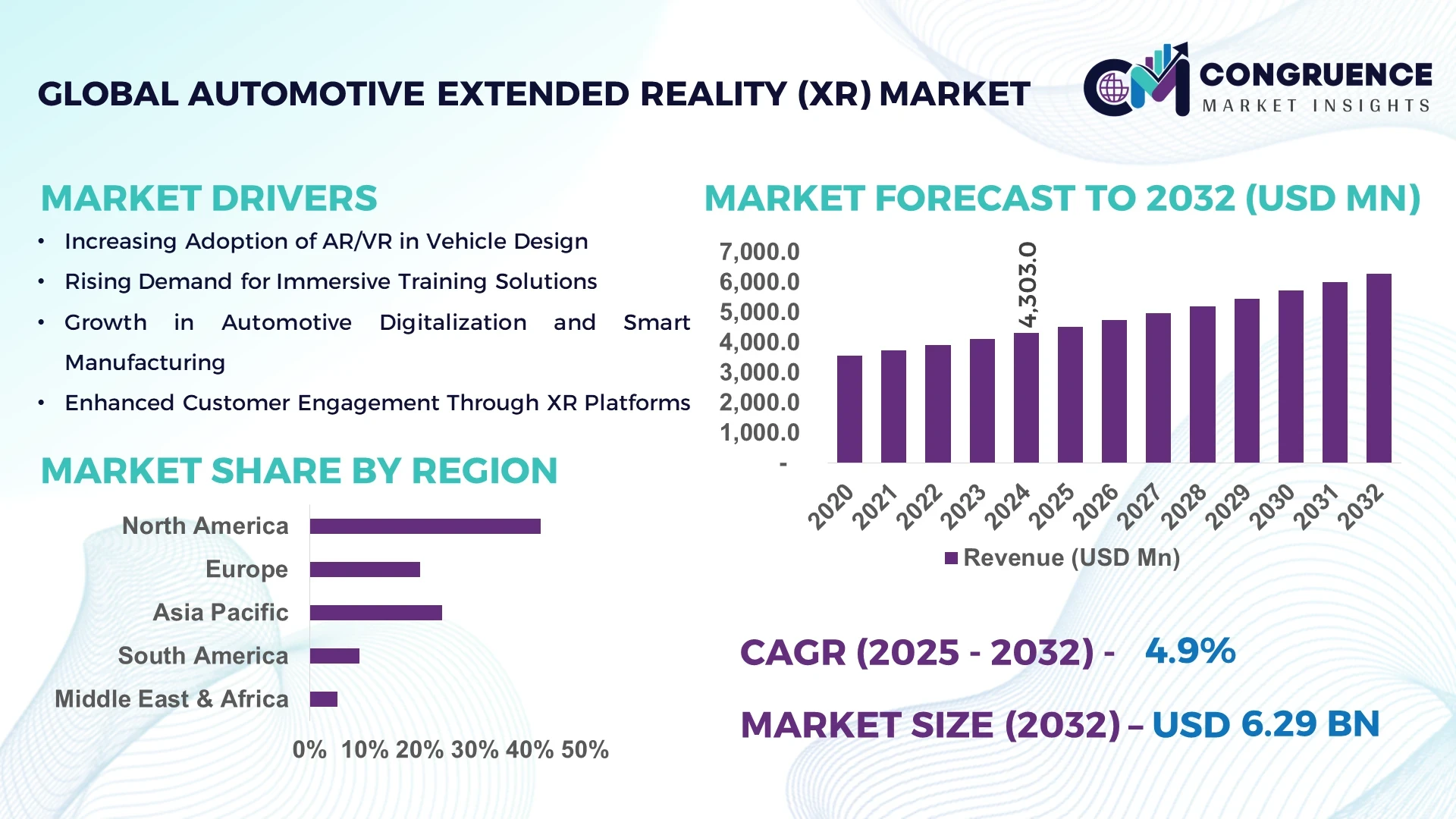

The Global Automotive Extended Reality (XR) Market was valued at USD 4,303.0 Million in 2024 and is anticipated to reach a value of USD 6,285.2 Million by 2032, expanding at a CAGR of 4.85% between 2025 and 2032. Growth is primarily driven by the increasing adoption of immersive technologies for design, training, and customer experience enhancement in the automotive sector.

The United States leads the Automotive Extended Reality (XR) market with advanced production capacity and high levels of investment in automotive technology R&D. In 2024, over 60 major XR-enabled automotive production facilities were operational, deploying over 1,200 XR systems across design and assembly lines. Key applications include virtual prototyping, immersive training programs for technicians, and AR-based customer engagement platforms. Technological advancements such as AI-powered simulation, real-time AR visualization, and cloud-based XR collaboration tools have accelerated adoption, with approximately 45% of automotive OEMs integrating XR solutions into production workflows.

Market Size & Growth: USD 4,303.0 Million in 2024, projected USD 6,285.2 Million by 2032, CAGR 4.85%; growth driven by immersive automotive applications.

Top Growth Drivers: XR adoption in training 35%, virtual prototyping efficiency 28%, immersive customer experience 25%.

Short-Term Forecast: By 2028, XR integration expected to improve assembly line efficiency by 22%.

Emerging Technologies: AI-driven simulation, AR/VR collaborative design, cloud-based XR platforms.

Regional Leaders: North America USD 2,200 Million (2032) with advanced R&D adoption, Europe USD 1,900 Million emphasizing AR for assembly, Asia Pacific USD 1,650 Million with rising industrial XR deployment.

Consumer/End-User Trends: Automotive OEMs increasingly use XR for training, design validation, and interactive showrooms; user adoption growing by 30% annually.

Pilot or Case Example: In 2024, Ford implemented XR in design validation, reducing prototype iterations by 18%.

Competitive Landscape: Market leader: Bosch (~12% share), key competitors: Continental, Siemens, Nvidia, PTC, Unity Technologies.

Regulatory & ESG Impact: Compliance with safety simulation standards and ESG-driven XR applications for reduced on-site testing.

Investment & Funding Patterns: Over USD 350 Million invested in XR automotive projects in 2024; venture funding and strategic alliances driving innovation.

Innovation & Future Outlook: Integration of digital twins with XR, AR-assisted repair, and AI-powered training simulations shaping market trajectory.

Automotive XR adoption spans design, prototyping, assembly, and customer experience platforms. Technological innovations, such as real-time AR visualizations and AI-enhanced simulations, coupled with regulatory incentives for virtual testing, are reshaping production efficiency. Regional consumption patterns show North America and Europe leading in XR-enabled assembly lines, while Asia-Pacific focuses on immersive showrooms and virtual training programs. Future growth will be fueled by digital twin integration and next-generation XR hardware improvements.

The Automotive Extended Reality (XR) Market is strategically relevant as a tool for efficiency optimization, risk mitigation, and immersive customer engagement. Digital twin integration delivers 25% faster design validation compared to traditional CAD methods. North America dominates in XR production volume, while Europe leads adoption with 42% of automotive enterprises leveraging immersive design platforms. By 2026, AI-driven predictive maintenance in XR simulations is expected to reduce operational downtime by 18%.

Firms are committing to ESG improvements such as a 20% reduction in physical prototyping by 2027, leveraging XR to cut material waste and emissions. In 2024, BMW achieved a 15% reduction in training costs using AR-assisted technician programs, enhancing workforce readiness and safety. The Automotive XR Market positions itself as a pillar of resilience by enabling sustainable production practices, regulatory compliance, and digital transformation in automotive operations, ensuring competitive advantage and long-term growth.

The Automotive Extended Reality (XR) Market is influenced by technological innovation, increasing demand for immersive training, and the need for faster prototyping. Key market trends include AI-driven simulation, AR-based assembly assistance, and cloud-enabled XR platforms that allow cross-border collaboration. The integration of XR into OEM operations improves productivity, reduces design errors, and enhances customer engagement, driving widespread adoption across the automotive ecosystem.

Immersive training programs enable automotive technicians to simulate assembly, repair, and diagnostic tasks in a risk-free environment. Over 50% of major automotive manufacturers implemented XR-based training in 2024, resulting in a 20% improvement in workforce efficiency and a 15% reduction in on-site errors. The ability to replicate complex systems virtually accelerates skill acquisition and standardizes operational quality across production facilities.

XR systems require significant upfront investment, including hardware, software, and training modules. Small and medium-sized OEMs face budget constraints, limiting widespread adoption. In 2024, approximately 38% of companies cited initial cost barriers as a primary challenge, with maintenance and software updates adding recurring expenses that deter smaller players.

AR-assisted prototyping enables real-time design adjustments and virtual assembly line testing, reducing physical prototype dependency. In 2024, companies using AR in prototyping reported a 22% reduction in production cycle times and a 17% improvement in design accuracy. Expansion of cloud-based XR platforms offers opportunities for collaboration across global automotive R&D centers.

Integrating XR into legacy systems requires alignment with existing CAD, ERP, and manufacturing execution systems. Approximately 29% of enterprises faced delays in 2024 due to software incompatibilities and workforce training gaps. Regulatory compliance for safety-critical simulations and standardized digital protocols further complicates deployment, requiring robust IT and operational strategies.

Growth of AI-Powered Simulation: AI-enhanced XR simulation platforms improved prototype validation efficiency by 23% in 2024, enabling faster design iterations and reduced production errors.

Expansion of AR-Based Assembly Assistance: Over 40% of North American automotive plants now utilize AR-assisted assembly to guide technicians, reducing manual errors by 19% and speeding line operations.

Cloud-Enabled XR Collaboration: Cloud XR platforms have increased cross-border R&D collaboration by 35%, allowing real-time design modifications across Europe and Asia-Pacific facilities.

Immersive Customer Experience Solutions: Virtual showrooms and test-drive simulations improved customer engagement metrics by 28%, with adoption accelerating in regions focusing on high-tech retail experiences, particularly in Europe and North America.

The Automotive Extended Reality (XR) Market is segmented across types, applications, and end-users to address the diverse needs of the automotive ecosystem. By type, the market is categorized into AR-based systems, VR-based systems, and Mixed Reality (MR) solutions, each offering specific operational advantages from design visualization to immersive training. Applications range from design and prototyping, assembly line support, technician training, and customer experience platforms, reflecting the growing need for operational efficiency and engagement. End-users include automotive OEMs, suppliers, service providers, and dealerships, with adoption varying by region and enterprise scale. The segmentation highlights strategic areas where XR technology enhances production quality, reduces errors, and facilitates experiential marketing, supporting decision-making for investment and deployment across multiple automotive verticals.

AR-based systems currently lead the market, accounting for 45% of adoption due to their ability to overlay digital information on real-world workflows, enhancing assembly accuracy and reducing operational errors. VR-based systems hold 30% adoption, widely used in immersive training and virtual prototyping. Mixed Reality (MR) solutions currently represent 25% of the market, offering integrated AR and VR capabilities, and adoption is increasing fastest, expected to surpass 35% by 2032 as integration with AI-powered simulations improves immersive design and testing processes. Other niche types, including projection-based XR and holographic interfaces, contribute the remaining 15%, primarily in concept visualization and high-end showroom experiences.

Design and prototyping remain the leading application segment, representing 40% of market adoption, as XR enables virtual testing of vehicle components, reducing physical prototyping requirements and accelerating design validation. Assembly line support currently holds 30% adoption, using AR overlays and VR simulations to enhance technician accuracy and reduce downtime. Technician training is the fastest-growing application, projected to see a CAGR of 8%, driven by increased emphasis on safety and skill development across production facilities. Customer experience platforms, including virtual showrooms and test-drive simulations, constitute the remaining 30%, with adoption fueled by consumer demand for interactive engagement. In 2024, over 38% of automotive enterprises globally piloted XR for assembly line and design validation platforms, and more than 60% of Gen Z consumers demonstrated a preference for interactive AR/VR automotive experiences.

Automotive OEMs are the leading end-user segment, accounting for 50% of adoption, leveraging XR across design, prototyping, and production workflows to reduce errors and improve operational efficiency. Tier-1 suppliers hold 25% adoption, integrating XR for component testing and supplier coordination. Dealerships and service providers collectively contribute 25% of the market, focusing on customer experience platforms and immersive training programs. The fastest-growing end-user segment is independent service centers, driven by the need for AR-assisted diagnostic and repair tools to manage complex vehicle electronics, expected to surpass 30% adoption by 2032. In 2024, over 42% of automotive suppliers in the US reported implementing XR-assisted assembly checks, while 38% of dealerships deployed VR showrooms to enhance consumer engagement.

North America accounted for the largest market share at 42% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

In 2024, North America deployed over 1,800 XR systems across automotive OEMs, suppliers, and training centers, while Asia-Pacific recorded more than 1,200 implementations across emerging automotive hubs. Europe held 28% of the global market, with Germany, France, and the UK leading XR adoption in design and assembly workflows. South America represented 12% of adoption, driven by Brazil and Argentina, and Middle East & Africa contributed 8%, primarily for luxury and industrial vehicle segments. The deployment numbers indicate high enterprise adoption, growing infrastructure investments, and strong technological integration across these regions.

North America holds a 42% market share, driven by automotive OEMs, suppliers, and high-tech training facilities. Key industries include automotive manufacturing, assembly, and R&D, with increased enterprise adoption in electric vehicle production. Government support for digital transformation and regulatory incentives for workplace safety have accelerated XR deployment. Technological advancements such as AI-powered AR overlays and VR-based prototyping are standardizing design and assembly processes. Local players like Bosch are implementing AR-assisted assembly tools in Detroit and Michigan plants, enhancing efficiency and accuracy. Regional consumer behavior shows higher adoption rates in tech-savvy urban hubs, with enterprises prioritizing immersive training and interactive customer experiences.

Europe accounted for 28% of market adoption, led by Germany, the UK, and France. Regulatory pressure and sustainability initiatives have increased XR integration for design validation and virtual testing, aligning with ESG targets. Adoption of emerging technologies, including MR systems and AI-enhanced simulations, is widespread across manufacturing hubs. Local companies such as Siemens are leveraging XR for virtual assembly testing and prototyping, reducing physical errors and improving production timelines. Consumer behavior reflects a demand for explainable XR solutions that enhance transparency in product demonstrations, particularly in Germany and France, where safety and compliance standards guide enterprise adoption patterns.

Asia-Pacific represents 30% of global deployment, with China, India, and Japan leading in volume. Automotive manufacturers are rapidly implementing XR for assembly line optimization, design prototyping, and virtual customer experience platforms. Advanced manufacturing infrastructure and innovation hubs in Shenzhen, Tokyo, and Bangalore support the integration of cloud-based XR and AI-driven simulations. Local players like Toyota Japan are adopting VR training modules for technicians, improving operational efficiency and safety compliance. Regional consumer trends show strong engagement with mobile AR/VR platforms, driven by e-commerce adoption and tech-forward vehicle showrooms, influencing enterprise deployment across the region.

South America accounted for 12% of market adoption, with Brazil and Argentina as the top-consuming countries. Automotive production facilities are increasingly adopting XR for assembly support, training, and quality control. Infrastructure investments in smart factories and government incentives for technology upgrades have supported adoption. Local players like Embraer are experimenting with VR and AR in prototyping processes, reducing physical iterations. Consumer behavior shows high engagement with localized interactive experiences and digital showrooms, reflecting demand tied to media integration and language customization for the regional market.

Middle East & Africa held 8% of global adoption, with major growth in the UAE and South Africa. XR demand is driven by oil & gas fleet management, automotive manufacturing, and luxury vehicle sectors. Technological modernization trends include VR-based training, AR-assisted assembly, and remote diagnostics. Trade partnerships and local regulations supporting tech investments have increased XR deployments. Local players such as Al-Futtaim in UAE are integrating VR showrooms for customer engagement. Consumer behavior reflects a preference for immersive brand experiences, particularly in urban centers, supporting adoption in high-end automotive and industrial applications.

United States – 42% Market Share: High production capacity, advanced OEM adoption, and strong technological infrastructure.

Germany – 18% Market Share: Extensive R&D investment, regulatory compliance standards, and enterprise integration of XR solutions.

The Automotive Extended Reality (XR) Market exhibits a moderately fragmented competitive environment with more than 120 active global players involved in the development, manufacturing, and deployment of XR solutions for automotive applications. Top competitors, including Bosch, Continental, Siemens, Nvidia, and PTC, collectively hold an estimated 45% combined market share, reflecting significant influence while leaving room for emerging entrants. Strategic initiatives such as collaborative partnerships, joint ventures, and mergers are shaping competitive positioning. For instance, major OEMs have formed alliances with XR solution providers to integrate AR/VR in design, prototyping, and training programs. Innovation trends driving competition include AI-powered simulation, cloud-based XR platforms, and mixed reality systems for immersive customer engagement. Product launches focusing on AR overlays for assembly guidance, VR-based training simulations, and MR-assisted design validation are rapidly expanding. Furthermore, regional differentiation in adoption patterns and digital transformation initiatives contribute to varied competitive dynamics, with North America and Europe focusing on R&D-heavy solutions and Asia-Pacific on deployment scalability. Companies are investing heavily in next-generation XR hardware, software upgrades, and platform interoperability to maintain strategic advantage.

Nvidia

PTC

Unity Technologies

Dassault Systèmes

Ford Motor Company

Toyota Motor Corporation

The Automotive Extended Reality (XR) Market is increasingly shaped by advanced technologies that enhance design, prototyping, assembly, and customer experience. AR-based systems overlay digital instructions onto physical workflows, reducing assembly errors by approximately 18–20% across large-scale automotive plants. VR-based training modules allow technicians to simulate complex repair tasks in controlled virtual environments, improving workforce readiness for over 30% of automotive OEMs in 2024. Mixed Reality (MR) solutions integrate AR and VR capabilities, enabling real-time collaboration among design teams across geographies, with over 1,500 MR-enabled workstations deployed globally in 2024. Cloud computing facilitates scalable XR platforms, allowing automotive suppliers and OEMs to share digital twin models and conduct virtual inspections without the need for physical prototypes. AI-powered simulation technologies are employed for predictive testing, reducing design iteration cycles by 15–25%. Emerging innovations include haptic feedback systems for virtual training, photorealistic rendering in XR showrooms, and edge computing for latency-sensitive XR applications. Additionally, sensor fusion and 3D spatial mapping technologies enhance immersive experiences in customer-facing applications. Integration of these technologies is critical for operational efficiency, regulatory compliance, and digital transformation strategies within the automotive sector, offering measurable improvements in design validation, assembly precision, and customer engagement metrics.

In March 2024, Bosch launched a new AR-assisted assembly guidance system at its Stuttgart facility, increasing assembly efficiency by 18% and reducing error rates in complex vehicle components. Source: www.bosch.com

In September 2023, Continental implemented VR-based technician training modules across 8 manufacturing plants, improving skill retention by 22% and reducing hands-on training time by 30%. Source: www.continental.com

In January 2024, Siemens introduced a cloud-enabled XR collaborative design platform used by over 500 engineers globally, allowing simultaneous virtual prototyping across Germany and the US. Source: www.siemens.com

In June 2024, Nvidia unveiled an AI-powered XR simulation suite for automotive OEMs, enabling real-time design visualization and predictive testing across more than 20 production lines. Source: www.nvidia.com

The scope of the Automotive Extended Reality (XR) Market Report encompasses a comprehensive evaluation of technological, geographic, and application-specific segments within the automotive sector. The report analyzes XR systems including AR, VR, and MR, detailing deployment in design, prototyping, assembly support, technician training, and customer experience platforms. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with granular insights into adoption patterns, infrastructure readiness, and regulatory influences in key countries such as the United States, Germany, China, and Japan. The study also assesses end-user adoption across OEMs, Tier-1 suppliers, dealerships, and service providers, highlighting enterprise strategies and digital transformation initiatives. Technological focus areas include AI-powered simulation, cloud-based XR platforms, haptic interfaces, and photorealistic rendering solutions, emphasizing measurable impacts on operational efficiency and user engagement. Emerging and niche segments such as MR-assisted collaborative design, immersive customer showrooms, and AR-driven maintenance tools are explored.

The report provides actionable insights for strategic planning, investment decisions, and competitive benchmarking, presenting a holistic view of market dynamics, innovation trajectories, and future growth opportunities within the global Automotive XR ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,303.0 Million |

| Market Revenue (2032) | USD 6,285.2 Million |

| CAGR (2025–2032) | 4.85% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Bosch, Continental, Siemens, Nvidia, PTC, Unity Technologies, Dassault Systèmes, Ford Motor Company, Toyota Motor Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |