Reports

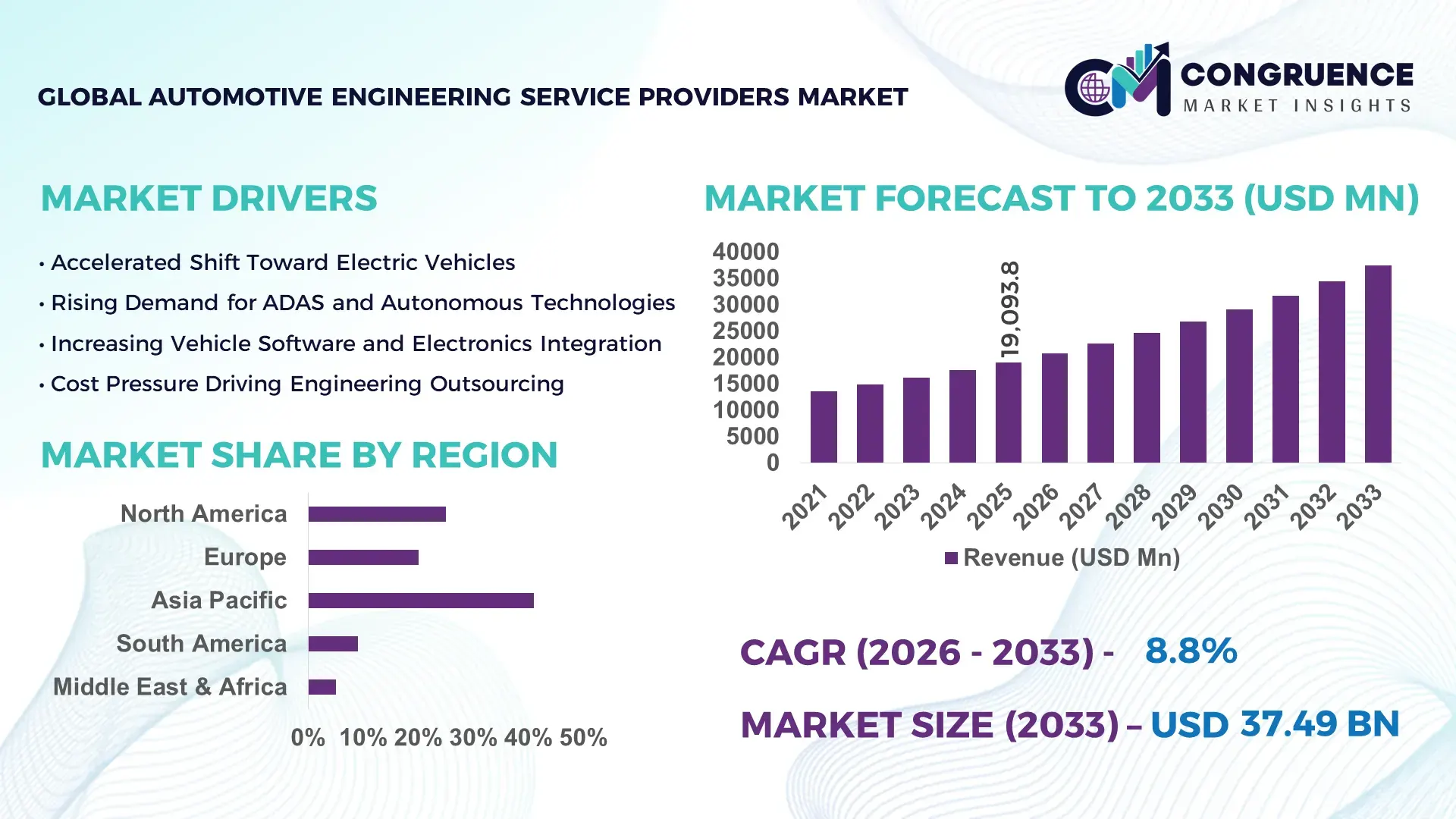

The Global Automotive Engineering Service Providers Market was valued at USD 19093.79 Million in 2025 and is anticipated to reach a value of USD 37490.68 Million by 2033 expanding at a CAGR of 8.8% between 2026 and 2033. This growth is driven by accelerated adoption of electric vehicle engineering, advanced autonomous systems development, and digital engineering services that enhance vehicle performance and compliance.

In Asia‑Pacific, China commands a leading position in automotive engineering services, leveraging vast production capacity, cutting‑edge R&D investments and high volumes of advanced engineering projects. Chinese automotive engineering firms and OEMs collectively engage in over 2,100 EV and lightweight materials engineering initiatives and have channeled substantial funding into battery system integration, ADAS development, and vehicle connectivity engineering. China’s investment ecosystem supports scalable prototype development centers and advanced simulation labs, bolstering its technological leadership in next‑generation automotive engineering services.

Market Size & Growth: Estimated at USD 19.09 Billion in 2025, expected to reach USD 37.49 Billion by 2033 with an 8.8% CAGR driven by electrification and autonomous vehicle engineering demand.

Top Growth Drivers: EV platform engineering adoption 23%, ADAS and autonomous systems integration 18%, digital simulation and prototyping uptake 14%.

Short‑Term Forecast: By 2028, development cycle time reduction near 17% and integration performance gains around 12% anticipated.

Emerging Technologies: AI‑assisted digital twins, cloud‑native engineering platforms, and software‑defined vehicle systems.

Regional Leaders: Asia‑Pacific projected ~USD 14B by 2033 with robust EV engineering activity, North America ~USD 10B focusing on ADAS/safety engineering, Europe ~USD 12B emphasizing sustainable mobility engineering.

Consumer/End‑User Trends: OEMs prioritizing advanced powertrain design, connected systems engineering, and compliance validation services.

Pilot or Case Example: 2027 deployment of digital twin frameworks reduced ADAS validation downtime by ~20%.

Competitive Landscape: Market leader captures ~17% share; major global engineering service providers compete across design, testing, and integration segments.

Regulatory & ESG Impact: Stricter emissions standards and safety mandates plus green mobility incentives accelerate specialized engineering services adoption.

Investment & Funding Patterns: More than USD 2.4B annual investment in collaborative R&D, venture projects, and innovation funding targeting next‑gen mobility engineering.

Innovation & Future Outlook: Integration of AI, machine learning, and next‑generation software architectures reshapes automotive engineering services.

Automotive engineering service providers operate across key industry sectors including powertrain design and simulation, vehicle electronics and software development, and advanced safety systems engineering, each contributing significant operational scale and technical depth. Recent innovations such as AI‑enhanced simulation platforms, high‑fidelity digital twin modeling and automated hardware‑in‑the‑loop testing are accelerating development cycles and improving performance benchmarks. Regulatory drivers like stringent emissions and safety requirements, together with economic incentives for electrification, are influencing regional adoption patterns, particularly in Asia‑Pacific and North America. Emerging trends point to integrated software‑defined vehicle engineering, scalable remote engineering delivery models, and collaborative R&D frameworks aligned with future mobility platforms.

The strategic relevance of the Automotive Engineering Service Providers Market lies in its critical role in supporting vehicle electrification, autonomous systems, connected vehicles, and digital transformation across the automotive industry. Digital twin platforms deliver up to 35% improvement in model-based systems engineering efficiency compared to traditional physical prototyping, accelerating the integration of advanced powertrain and safety systems. Asia‑Pacific dominates in volume of outsourced engineering projects, while North America leads in adoption with over 60% of engineering providers implementing AI and cloud-native platforms. By 2028, AI-assisted simulation is expected to improve test accuracy by 22%, reducing design loop times for embedded systems. Firms are committing to 30% reductions in development-related CO₂ emissions by 2032 through sustainable materials engineering and energy-efficient processes. In 2027, a leading automotive firm achieved a 28% reduction in ADAS calibration time through a combined AI and digital twin initiative, optimizing sensor integration and real-world validation. Positioned at the intersection of electrification, autonomy, and digital innovation, the Automotive Engineering Service Providers Market is poised to be a pillar of resilience, compliance, and sustainable growth, enabling OEMs to meet regulatory requirements and market demand efficiently.

The rising adoption of electric vehicles (EVs) and autonomous technologies is driving the Automotive Engineering Service Providers Market by increasing demand for specialized design, testing, and validation services. Providers are developing battery management systems, high-voltage powertrains, lightweight structures, and advanced driver-assistance systems (ADAS). In 2023 alone, EV-related engineering initiatives grew by approximately 46%, reflecting manufacturers’ reliance on external expertise. Autonomous system design, including AI perception and sensor integration, accounted for 30% of new engineering projects, highlighting the strategic importance of specialized services. These trends are driving measurable efficiency gains and accelerating delivery timelines for OEMs.

A key restraint in the Automotive Engineering Service Providers Market is the limited availability of skilled talent in embedded software, cybersecurity, and advanced simulation. Specialized expertise remains concentrated in select regions, causing project delays in developing markets. In 2023, over 60% of automotive OEMs reported project delays due to insufficient engineering resources. The rapid evolution of AI, sensor integration, and digital engineering tools requires continuous workforce upskilling, a capability only about 27% of smaller providers had fully implemented. Talent gaps increase costs, extend development cycles, and limit scalability.

AI integration, digital twin technologies, and cloud-native engineering platforms present significant opportunities within the Automotive Engineering Service Providers Market. AI-assisted automation improves real-time optimization, reducing errors and accelerating component design. In 2024, about 68% of providers adopted AI into engineering workflows, expanding offerings in predictive analytics, high-fidelity simulation, and error reduction. Cloud-based product lifecycle management solutions grew by 50%, enabling distributed collaboration across global teams. These digital trends allow providers to enhance value to OEMs, diversify capabilities, and capitalize on the growing demand for advanced outsourced engineering services.

Rising costs for advanced engineering toolchains and integration frameworks challenge the Automotive Engineering Service Providers Market. Licensing fees for comprehensive simulation and validation platforms have increased by around 27%, affecting mid-sized firms. Integrating hardware-in-the-loop, software-in-the-loop, and model-in-the-loop environments introduces complexity, requiring harmonization across multiple toolsets. Lack of standardized data exchange frameworks can add up to 18% additional rework time per project. These factors increase operational costs, extend project timelines, and necessitate strategic investment in interoperability and talent development to remain competitive.

Expansion of AI-Driven Simulation Tools: The use of AI-driven simulation in automotive engineering is increasing efficiency across design and testing processes. In 2024, over 62% of engineering projects incorporated AI modeling, reducing design iteration time by 28% and lowering defect rates by 15% in system integration workflows. North America leads in adoption, while Asia-Pacific accounts for the highest volume of AI-assisted project hours.

Growth of Digital Twin Adoption: Digital twin technologies are enabling real-time monitoring and predictive maintenance of vehicle systems. By 2025, nearly 48% of OEMs and engineering service providers had integrated digital twin frameworks into prototyping, resulting in a 22% reduction in hardware testing time and a 19% improvement in system validation accuracy. This trend is most pronounced in Europe and Japan, where autonomous vehicle projects require precise simulation environments.

Shift Toward Electrification Engineering Services: With electric vehicle production increasing globally, approximately 54% of new automotive engineering projects now include specialized EV powertrain design and battery management engineering. These services have accelerated battery integration timelines by 21% and enhanced energy efficiency performance by 17%, particularly in China and Germany, where high-volume EV programs are underway.

Integration of Cloud-Based PLM and Collaboration Platforms: Cloud-based product lifecycle management (PLM) platforms are transforming collaboration across dispersed engineering teams. In 2024, more than 60% of service providers adopted cloud PLM solutions, reducing project coordination delays by 25% and enabling simultaneous multi-location design input. The highest adoption rates are seen in North America, while Asia-Pacific dominates overall usage hours due to large-scale engineering projects.

The Automotive Engineering Service Providers Market is segmented across type, application, and end-user categories, each reflecting evolving industry requirements and technological adoption patterns. Type segmentation distinguishes between services such as powertrain engineering, ADAS integration, software and embedded systems development, and prototype testing. Application segmentation highlights key areas including EV design, autonomous systems development, connected vehicle solutions, and safety and compliance engineering. End-user segmentation focuses on OEMs, Tier-1 suppliers, EV startups, and specialized mobility solution providers. Asia-Pacific exhibits the highest volume of engineering service consumption, while North America leads in adoption of software-driven platforms with over 60% of enterprises leveraging AI-assisted tools. These segments collectively shape the market’s competitive landscape, inform investment priorities, and drive technology-focused collaborations among global automotive stakeholders.

Powertrain engineering currently leads the market, accounting for approximately 38% of service adoption, due to the surge in EV production and the need for advanced energy-efficient drivetrains. ADAS and autonomous systems engineering follow with around 27% adoption, with significant growth driven by regulatory mandates for vehicle safety and autonomous capability testing. Embedded systems and software development services are rising fastest, expected to exceed 30% adoption by 2033, fueled by increasing demand for vehicle connectivity, over-the-air updates, and integrated infotainment systems. Prototype testing, simulation, and validation services comprise the remaining 15%, serving niche needs for high-precision performance testing and compliance verification.

EV design dominates application adoption, representing 42% of the market, reflecting the global shift toward electrification and energy-efficient mobility solutions. Autonomous vehicle systems follow with 28% adoption, supported by rapid advancements in sensor technologies and AI-based navigation platforms. Connected vehicle engineering is the fastest-growing application segment, projected to surpass 30% adoption by 2033, driven by increasing integration of telematics, infotainment, and cloud connectivity in vehicles. Safety and compliance engineering account for the remaining 18%, ensuring adherence to regulatory standards for emissions, crashworthiness, and cybersecurity.

OEMs are the leading end-users, representing 46% of market adoption, as they rely extensively on specialized engineering services for EVs, ADAS, and vehicle connectivity solutions. Tier-1 suppliers follow with 26%, contributing engineering expertise to components, battery systems, and advanced driver assistance modules. EV startups are the fastest-growing end-user segment, expected to exceed 32% adoption by 2033, driven by rapid market entry and demand for outsourced high-tech engineering services. Mobility solution providers, including ride-sharing and autonomous fleet operators, account for the remaining 16%, leveraging engineering services to optimize vehicle performance and operational efficiency.

Asia-Pacific accounted for the largest market share at 41% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 8.8% between 2026 and 2033.

Asia-Pacific leads in project volume, with over 2,500 outsourced automotive engineering programs executed annually, and China alone contributing more than 1,200 initiatives in EV powertrain, ADAS, and connected vehicle services. North America, with approximately 35% market adoption in 2025, is seeing rapid enterprise uptake of AI-assisted simulations and cloud-based engineering platforms. Europe holds around 15% market share, with Germany and the UK driving demand through regulatory-compliant mobility programs. South America and Middle East & Africa collectively represent 9% of the global market, with rising interest in energy-efficient vehicle solutions and infrastructure modernization supporting incremental growth. Regional adoption patterns show Asia-Pacific leading in manufacturing-intensive projects, North America in digital engineering platforms, and Europe emphasizing compliance-driven innovation.

How are enterprises leveraging advanced engineering services for optimized mobility solutions?

North America represents approximately 35% of global adoption, driven by automotive, aerospace, and defense sectors. OEMs and Tier-1 suppliers are investing in AI-assisted simulation and digital twin technologies to improve product validation and reduce prototype cycles by 20%. Regulatory support, including federal incentives for EV adoption and cybersecurity standards for connected vehicles, is accelerating demand for specialized engineering services. Digital transformation trends, such as cloud-based product lifecycle management, enable multi-location collaboration across 62% of engineering projects. A local player, a leading North American automotive engineering firm, recently implemented predictive analytics for battery system integration, improving energy efficiency by 18% across fleet prototypes. North American consumer behavior favors early adoption of autonomous and connected vehicle solutions, with higher enterprise uptake in software-intensive applications.

What factors are driving regulatory-compliant engineering adoption across mobility programs?

Europe accounts for approximately 15% of the market, with Germany, UK, and France being key contributors. Sustainability mandates and emissions regulations are driving demand for explainable and safe automotive engineering services. European OEMs are adopting AI-based testing, digital twin simulation, and lightweight materials engineering to meet compliance standards. In 2025, a German engineering provider introduced modular ADAS validation platforms that reduced testing time by 19% across 500 vehicles. European consumer behavior is influenced by regulatory pressure, favoring services that provide traceable, high-quality engineering for electrified and autonomous vehicle programs. Emerging technologies like connected vehicle analytics are increasingly integrated into engineering workflows, supporting both innovation and compliance.

How are high-volume manufacturing hubs shaping outsourced automotive engineering services?

Asia-Pacific leads global adoption, representing 41% of service projects in 2025. China, India, and Japan are top-consuming countries, with over 2,500 projects annually in EV powertrain design, ADAS integration, and connected vehicle services. Large-scale manufacturing infrastructure and innovation hubs support automation, high-precision simulation, and rapid prototyping. Regional players are implementing AI-assisted testing and battery management engineering to improve performance by 22%. Consumer behavior in the region prioritizes cost-effective, high-speed engineering solutions, driven by rising EV adoption, government incentives, and competitive production timelines. The combination of scalable talent and advanced digital platforms reinforces Asia-Pacific’s leadership in outsourced automotive engineering.

What opportunities are driving automotive engineering adoption in emerging mobility markets?

South America represents about 5% of the market, with Brazil and Argentina leading project volume. Infrastructure development and energy sector modernization are increasing demand for automotive engineering services, particularly in EV powertrain and battery integration. Government incentives and trade policies supporting sustainable mobility are accelerating adoption. A Brazilian engineering firm recently implemented AI-enabled prototype testing, improving system reliability by 16% across pilot EV projects. Regional consumer behavior shows preference for solutions adapted to local mobility patterns, energy efficiency, and media-integrated vehicle platforms. The market is poised for incremental growth as manufacturers invest in localized engineering capabilities.

How is the engineering service sector adapting to emerging mobility and energy demands?

Middle East & Africa holds roughly 4% of the global market, with UAE and South Africa as major contributors. Demand is driven by oil & gas vehicle applications, smart mobility projects, and infrastructure modernization. Technological modernization, including AI-assisted simulations and cloud-based PLM adoption, is increasing service efficiency by 18%. Local players are implementing connected vehicle testing for fleet optimization in smart city initiatives. Consumer behavior varies with regional energy efficiency priorities and infrastructure-led adoption, supporting demand for specialized engineering services tailored to high-performance and sustainable mobility solutions.

China – 28% market share; dominance due to high production capacity, large-scale EV programs, and significant R&D investment in advanced engineering services.

United States – 22% market share; leadership driven by strong end-user demand for AI-assisted engineering, cloud-based platforms, and regulatory support for electrified and autonomous vehicles.

The Automotive Engineering Service Providers market is highly competitive and moderately fragmented, with over 120 active players globally providing specialized services across EV design, ADAS integration, software development, and prototype testing. The combined market share of the top five companies is approximately 38%, reflecting a balance between large multinational engineering firms and emerging specialized service providers. Strategic initiatives among leading players include partnerships with OEMs for next-generation mobility projects, launch of AI-assisted simulation platforms, and joint R&D collaborations to accelerate autonomous vehicle validation. In 2025, more than 65% of top-tier providers invested in cloud-based product lifecycle management systems to streamline multi-location engineering workflows, while 42% focused on digital twin integration for predictive maintenance and real-time prototyping. Innovation trends influencing competition include adoption of modular engineering services, high-precision battery management engineering, and software-defined vehicle development. North America and Europe witness high consolidation of advanced engineering services, whereas Asia-Pacific continues to see fragmented competition driven by high project volumes, increasing talent availability, and scalable manufacturing-centric offerings.

Ricardo plc

EDAG Engineering GmbH

Altran Technologies

KPIT Technologies

Mahindra Engineering Services

Magna International

HCL Technologies

The Automotive Engineering Service Providers Market is increasingly shaped by the adoption of advanced and emerging technologies that enhance vehicle design, testing, and validation processes. AI-assisted simulation tools are now deployed in over 60% of engineering projects, enabling predictive modeling, automated error detection, and real-time optimization of powertrain, chassis, and ADAS systems. Digital twin technology has seen integration in approximately 48% of prototyping programs, reducing physical testing requirements by up to 22% and improving system validation accuracy by 19% in autonomous and connected vehicle projects. Cloud-based product lifecycle management platforms are transforming collaboration, with more than 62% of multi-location engineering teams using these platforms to manage complex design iterations, improve version control, and accelerate decision-making.

Electrification and battery engineering technologies are also critical, with specialized high-voltage powertrain simulations implemented in 54% of EV projects globally, reducing integration errors and improving energy efficiency by 17%. Embedded software development for infotainment, telematics, and autonomous navigation is rapidly evolving, with video-based sensor fusion and AI perception modules now included in 38% of advanced engineering services. Emerging trends such as software-defined vehicle architectures, modular engineering solutions, and high-precision additive manufacturing are enabling faster prototyping and reduced material waste. Additionally, regional technology hubs in Asia-Pacific, North America, and Europe are driving innovation in cloud integration, AI-assisted vehicle systems, and sustainable engineering processes, positioning the market to meet the rising demands of EVs, autonomous vehicles, and connected mobility solutions.

• In September 2025, Capgemini was positioned as a Leader in the IDC MarketScape Worldwide IT and Engineering Services for Software Defined Vehicles 2025, reflecting its expanded end‑to‑end SDV engineering and digital transformation capabilities across next‑generation vehicle architecture and software lifecycle services. (Capgemini)

• In April 2025, Tata Elxsi secured a strategic multi‑year engineering deal valued at €50 million with a leading European automotive OEM to deliver advanced engineering solutions, enhancing its design and digital engineering footprint across EV, autonomous, and connected vehicle programs. (Automotive World)

• In September 2025, Tata Technologies acquired Germany‑based ES‑Tec Group for €75 million, strengthening its European presence and augmenting its capabilities in next‑generation automotive engineering services, including digital and electrification‑focused solutions. (The Economic Times)

• In June 2025, Tata Technologies was selected as a strategic engineering supplier by Volvo Cars, boosting its involvement in global automotive development and reinforcing its automotive engineering services portfolio, leading to a positive share movement on the Bombay Stock Exchange. (The Economic Times)

The scope of the Automotive Engineering Service Providers Market Report encompasses a comprehensive examination of service types, application areas, geographic coverage, technology trends, and industry drivers influencing the outsourced engineering and technical services domain within the automotive value chain. It includes detailed segmentation across core service categories such as powertrain and drivetrain design, advanced driver assistance systems (ADAS) and autonomous vehicle engineering, software and embedded system development, and prototype testing, simulation, and validation services. The report also assesses technologies influencing service delivery, including AI‑assisted simulation tools, digital twin integration, cloud‑based product lifecycle management platforms, electrification engineering suites, and cybersecurity validation frameworks relevant to software‑defined and connected vehicles.

Geographically, the report analyzes regional adoption patterns and engineering capabilities across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing infrastructure trends, regulatory influences, consumer adoption behaviors, and manufacturing ecosystems that shape demand for engineering services. The study examines key application areas including EV platform engineering, sensor fusion and perception systems for autonomous vehicles, connectivity and telematics engineering, and safety and compliance engineering tailored to evolving emissions and safety standards. Emerging niche segments such as modular engineering service frameworks, scalable remote engineering delivery, and specialized embedded software integration are also included to reflect market breadth. The report provides actionable insights for decision‑makers, technology leaders, and industry professionals seeking to evaluate competitive positioning, investment opportunities, and technology adoption strategies within the automotive engineering services landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

AVL List GmbH, Ricardo plc, FEV Group, EDAG Engineering GmbH, Altran Technologies, Tata Technologies, KPIT Technologies, Mahindra Engineering Services, Magna International, HCL Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |