Global Automotive Engine Encapsulation Market Report Overview

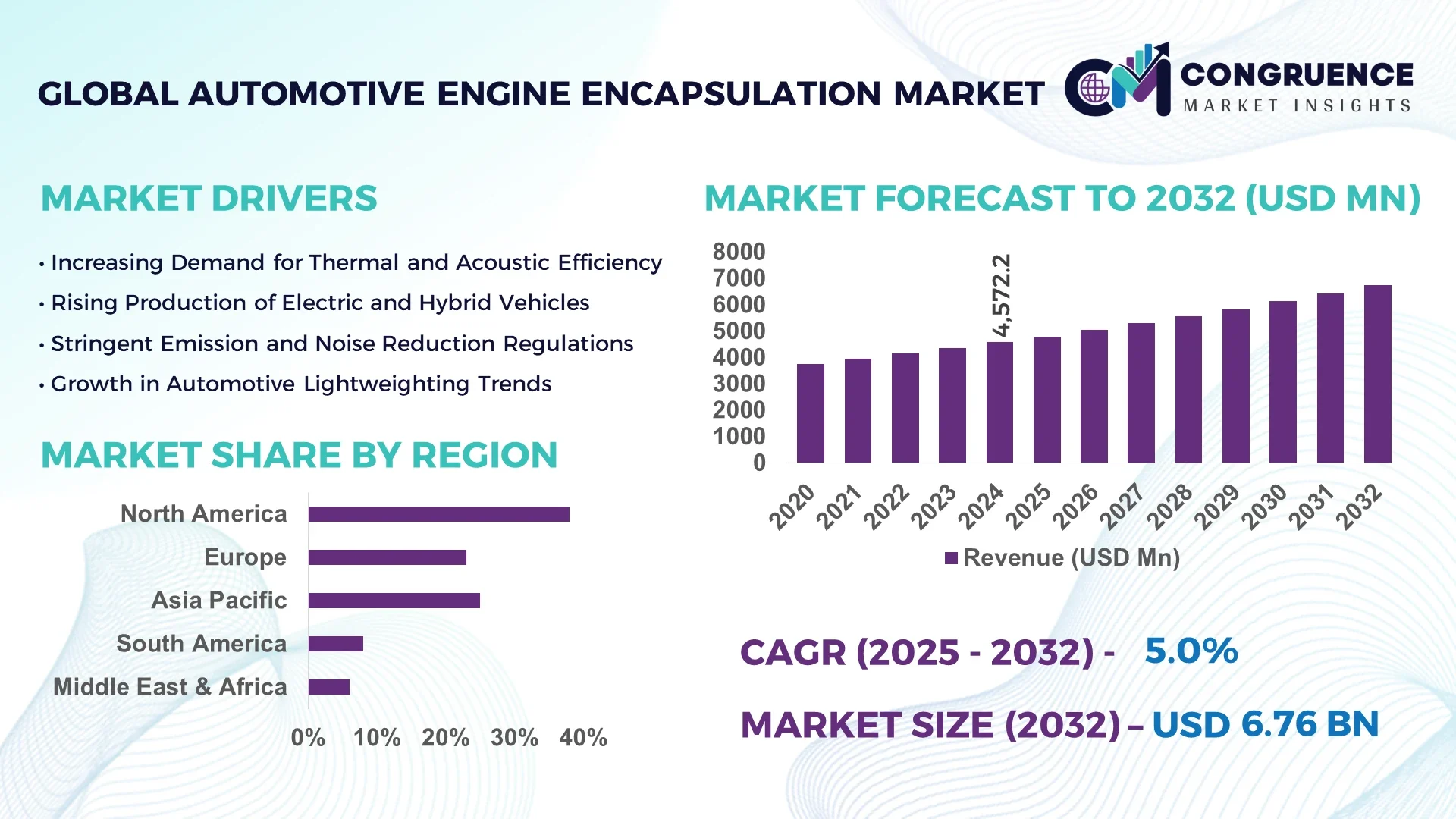

The Global Automotive Engine Encapsulation Market was valued at USD 4,572.24 million in 2024 and is anticipated to reach a value of USD 6,755.29 million by 2032, expanding at a CAGR of 5.0% between 2025 and 2032.

Germany's automotive engine encapsulation market is characterized by a robust automotive industry, home to leading automakers. The country is at the forefront of adopting innovative technologies to meet stringent emissions regulations. Engine encapsulation plays a key role in helping manufacturers comply with these regulations by improving thermal management, reducing fuel consumption, and minimizing CO₂ emissions.

The automotive engine encapsulation market is witnessing significant growth due to increasing demand for fuel-efficient and quieter vehicles. Engine encapsulation technology helps maintain optimal engine temperatures, reduces fuel consumption, and dampens engine noise, becoming standard in internal combustion engine vehicles and increasingly utilized in electric vehicles to mitigate noise around powertrains. Advances in lightweight materials such as polypropylene, polyurethane, and carbon fiber are further propelling market growth by providing encapsulation benefits without significantly increasing vehicle weight. In 2023, engine-mounted encapsulation systems dominated the market, acquiring a market of USD 3.8 billion. The passenger cars segment held the largest market share of 68.7% in 2023, benefiting significantly from engine encapsulation, which improves thermal management, reduces fuel consumption, and minimizes noise factors. Asia-Pacific dominated the market with a revenue share of 45.78% in 2023, owing to growing demand for innovations that improve vehicle performance, comfort, and efficiency.

How is AI Transforming Automotive Engine Encapsulation Market?

Artificial Intelligence (AI) is revolutionizing the automotive engine encapsulation market by enabling the development of advanced materials and designs that enhance thermal management and noise reduction. AI-driven simulations and modeling techniques allow engineers to predict and optimize the performance of encapsulation systems under various operating conditions, leading to more efficient and effective solutions. Machine learning algorithms analyze vast datasets to identify patterns and correlations, facilitating the creation of materials with improved heat resistance and sound absorption properties. These innovations contribute to the production of vehicles that are more fuel-efficient, environmentally friendly, and comfortable for passengers.

In addition, AI is streamlining the manufacturing processes of engine encapsulation components. By integrating AI into production lines, manufacturers can monitor and control quality in real-time, reducing defects and ensuring consistency. Predictive maintenance powered by AI minimizes downtime by anticipating equipment failures before they occur. This leads to increased productivity and cost savings, making the adoption of AI technologies a strategic advantage in the competitive automotive industry. Furthermore, AI is facilitating the customization of engine encapsulation solutions to meet specific vehicle requirements. By analyzing vehicle data, AI can recommend tailored encapsulation designs that optimize performance for different models and driving conditions. This level of personalization enhances the overall efficiency and effectiveness of engine encapsulation systems, aligning with the industry's move towards more specialized and high-performance vehicles.

“In October 2023, a new type of heat shield was developed for electric vehicle batteries with advanced fire resistance and improved thermal insulation, offering enhanced protection and performance for electric drivetrains.”

Automotive Engine Encapsulation Market Dynamics

DRIVER:

Growing Emphasis on Vehicle Noise Reduction and Fuel Efficiency

Increasing consumer demand for vehicles that offer quieter operation and better fuel economy is significantly boosting the automotive engine encapsulation market. Engine encapsulation systems act as a barrier that limits noise and vibration from reaching the passenger cabin, improving overall ride comfort. Additionally, by keeping engine heat contained for longer periods, these systems reduce engine warm-up times and improve thermal efficiency, resulting in lower fuel consumption. According to recent manufacturing trends, over 65% of premium vehicles manufactured in 2023 in Europe and North America incorporated advanced engine encapsulation systems. Luxury automakers are especially adopting these technologies as part of their broader NVH (noise, vibration, and harshness) optimization strategies, reinforcing their commitment to vehicle comfort and performance.

RESTRAINT:

High Costs of Advanced Encapsulation Materials and Production

Despite its benefits, the high cost of manufacturing and installing engine encapsulation systems poses a barrier to widespread market penetration, especially in budget vehicle segments. High-performance materials such as polyurethane, carbon fiber, and aerogel composites used in encapsulation add to production expenses. Additionally, the need for precision molding and specialized installation increases assembly time and cost. Many automotive OEMs in emerging economies still prioritize cost-effective manufacturing processes, making it difficult to adopt encapsulation solutions at scale. In 2023, small and mid-sized vehicle models in Southeast Asia showed less than 25% integration of engine encapsulation systems, highlighting cost-based hesitancy in price-sensitive markets.

OPPORTUNITY:

Integration of Encapsulation in Hybrid and Electric Vehicles

As global electrification accelerates, the demand for encapsulation in hybrid and electric vehicles presents a significant growth opportunity. While electric motors generate less noise than internal combustion engines, other sources such as battery cooling systems and electronic components introduce new acoustic challenges. Engine encapsulation technologies are being adapted to cover battery enclosures and electronic drive modules, improving thermal management and sound insulation in electric vehicles. In 2024, over 40% of new EV models introduced by global OEMs featured encapsulation components specifically designed for thermal optimization and cabin noise reduction. These solutions are particularly relevant in colder climates, where retaining battery warmth is critical for performance and longevity.

CHALLENGE:

Compatibility and Design Constraints in Compact Vehicle Segments

One of the major challenges in the automotive engine encapsulation market is designing solutions that fit within the spatial limitations of compact and subcompact vehicles. These vehicle types often have limited engine bay space, restricting the installation of bulky or layered encapsulation materials. Additionally, tight packaging requirements in these models make it difficult to maintain ventilation and serviceability when encapsulation is applied. As of 2023, fewer than 18% of compact cars sold globally were equipped with full engine encapsulation systems due to these structural limitations. Engineers must balance heat retention, noise reduction, and airflow management without compromising on engine accessibility or vehicle safety standards, making widespread application in smaller vehicles a complex task.

Automotive Engine Encapsulation Market Latest Trends

• Rise in Integration of Lightweight Composite Materials: Automotive manufacturers are increasingly adopting lightweight composite materials such as polyurethane foam, glass fiber-reinforced plastics, and carbon fiber composites in engine encapsulation to enhance vehicle efficiency and reduce emissions. These materials provide excellent thermal and acoustic insulation properties while reducing overall vehicle weight. In 2024, more than 55% of newly launched mid- and high-end vehicles featured encapsulation systems made from multi-layered composite panels, showcasing a clear trend toward lightweight design optimization.

• Growth in Adoption Across Electric and Hybrid Vehicle Platforms: With the surge in electric and hybrid vehicle production, encapsulation technologies are being redesigned to meet the unique cooling and noise insulation requirements of battery systems and electric drive units. By the first quarter of 2025, electric vehicles accounted for over 30% of engine encapsulation demand in Western Europe. Manufacturers are prioritizing encapsulation designs that ensure battery temperature consistency and suppress mechanical noise from auxiliary components.

• Increased Use of 3D Molding and Precision Design Techniques: Automotive suppliers are incorporating advanced 3D molding technologies to create encapsulation components that fit precisely within diverse engine architectures. These techniques allow for optimized airflow and minimal heat loss. As of 2024, more than 45% of encapsulation parts manufactured in Japan and Germany were produced using automated 3D design systems, resulting in better customization and performance alignment for OEMs.

• Emphasis on Sustainability and Recyclable Materials: Rising environmental awareness is pushing the market toward sustainable solutions. Manufacturers are now exploring biodegradable polymers and recyclable thermoplastics for use in encapsulation parts. In 2024, over 20% of encapsulation systems installed in European vehicles were produced using partially recycled thermoplastics, representing a shift toward circular economy principles. Automakers are investing in eco-friendly supply chains to meet both performance and environmental objectives.

Segmentation Analysis

The automotive engine encapsulation market is segmented based on type, application, and end-user, each playing a vital role in shaping the overall market landscape. Types include hood insulation, engine-mounted encapsulation, underbody encapsulation, and firewall encapsulation, each addressing specific thermal and acoustic control requirements. By application, the encapsulation is used across internal combustion engine vehicles, hybrid electric vehicles (HEVs), and battery electric vehicles (BEVs), with hybrid models gaining faster traction due to combined thermal and acoustic benefits. Key end-users include original equipment manufacturers (OEMs), aftermarket suppliers, and automotive assembly plants, with OEMs dominating the usage. These segments demonstrate diverse growth trajectories, influenced by evolving emission standards, vehicle electrification, and consumer demand for enhanced cabin comfort.

By Type

The market offers several encapsulation types, including engine-mounted encapsulation, hood insulation, underbody encapsulation, and firewall encapsulation. Among these, engine-mounted encapsulation holds the leading market share, accounting for more than 40% of total installations in 2024, as it provides direct insulation and efficient thermal containment for high-temperature zones. This type significantly reduces engine warm-up times and improves efficiency. Underbody encapsulation is emerging as the fastest-growing segment, with adoption accelerating in compact and electric vehicles to optimize airflow and improve aerodynamic efficiency. By 2025, underbody encapsulation is expected to experience double-digit growth, particularly in electric vehicle platforms. Hood insulation and firewall encapsulation continue to see steady demand due to their importance in cabin noise reduction and thermal management but trail behind in growth compared to the more integrated encapsulation formats.

By Application

Engine encapsulation finds application in internal combustion engine (ICE) vehicles, hybrid electric vehicles (HEVs), and battery electric vehicles (BEVs). ICE vehicles currently dominate the market, accounting for over 60% of global encapsulation demand due to their widespread presence and dependence on thermal efficiency for fuel economy. However, HEVs are the fastest-growing application segment, driven by the need for advanced insulation solutions that support dual powertrains. In 2024, HEVs accounted for nearly 25% of all new encapsulation installations in Asia-Pacific markets. BEVs are also gaining traction, especially in Europe and North America, where thermal regulation of batteries is critical. Manufacturers are increasingly adapting encapsulation systems to serve the cooling and noise control needs of electric platforms, leading to diversified design applications beyond traditional engine zones.

By End-User Insights

The primary end-users in the automotive engine encapsulation market are original equipment manufacturers (OEMs), aftermarket suppliers, and vehicle assembly units. OEMs dominate the segment with a market share exceeding 70% as they integrate encapsulation components during vehicle production to meet noise and emission standards. OEMs benefit from design alignment and better material integration. Aftermarket suppliers, though smaller in market share, are showing increased activity as consumers in regions like Latin America and Southeast Asia retrofit encapsulation systems for older vehicles. This segment grew by over 12% year-on-year in 2024. Vehicle assembly plants are also key contributors, especially those involved in multi-brand or contract manufacturing, where standard encapsulation modules are adapted across vehicle platforms. OEMs remain the strongest and most consistent user group, while aftermarket and contract-based installations are expanding steadily.

Region-Wise Market Insights

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.5% between 2025 and 2032.

North America’s market dominance is driven by the high adoption of advanced encapsulation technologies in both ICE and electric vehicles, supported by stringent emission and noise regulations. Meanwhile, Asia-Pacific’s rapid industrialization, rising vehicle production, and growing electric vehicle market are fueling the demand for innovative engine encapsulation solutions. Europe and South America hold substantial shares as well, with growing demand for lightweight and sustainable materials in encapsulation systems. The Middle East & Africa region is also expanding due to increasing automotive manufacturing investments.

North America Automotive Engine Encapsulation Market Trends

Driving Innovation with Advanced Noise and Thermal Solutions

North America is witnessing a strong trend toward integrating advanced lightweight composite materials in automotive engine encapsulation. In 2024, nearly 60% of new vehicles launched featured enhanced encapsulation designed for noise reduction and thermal management, particularly in the U.S. and Canada. The region is also focusing on expanding encapsulation solutions tailored for hybrid and electric vehicles, which accounted for over 35% of the encapsulation market in 2024. Additionally, increased investments in R&D for sustainable materials are influencing market dynamics. The aftermarket segment is also growing steadily, driven by vehicle maintenance and retrofitting demand in Mexico and the U.S.

Europe Automotive Engine Encapsulation Market Trends

Leading the Charge in Sustainable and Lightweight Encapsulation Technologies

Europe’s automotive engine encapsulation market is characterized by a strong focus on sustainability and regulatory compliance. In 2024, about 50% of encapsulation components used in Germany and France were manufactured using recyclable thermoplastics and biodegradable polymers. The region is also advancing in encapsulation designs specific to electric vehicles, which make up approximately 30% of the market share in countries like Norway and the Netherlands. The demand for modular encapsulation solutions that reduce assembly time is rising across the UK and Italy. Additionally, government incentives to reduce vehicle emissions are accelerating the uptake of enhanced thermal and acoustic encapsulation systems.

Asia-Pacific Automotive Engine Encapsulation Market Trends

Rapid Industrial Growth Fuels Demand for Engine Encapsulation

Asia-Pacific is the fastest-growing market for automotive engine encapsulation due to its expanding vehicle manufacturing hubs in China, India, and Japan. In 2024, encapsulation adoption in hybrid and electric vehicles accounted for over 28% of the market, led primarily by China’s push for new energy vehicles. The use of advanced 3D molding techniques is increasing rapidly, with over 40% of encapsulation parts produced using automated design processes in Japan. India is witnessing growth in aftermarket encapsulation due to rising demand for vehicle upgrades, accounting for 15% of the regional market. Southeast Asia is also emerging as a key market with increasing vehicle production capacity.

South America Automotive Engine Encapsulation Market Trends

Expanding Automotive Manufacturing Spurs Encapsulation Market

South America’s automotive engine encapsulation market is expanding steadily, driven by increasing vehicle production and modernization of manufacturing facilities in Brazil and Argentina. In 2024, Brazil accounted for nearly 55% of the regional encapsulation demand, focusing on engine-mounted and hood insulation types for thermal management in conventional vehicles. Argentina is experiencing growth in underbody encapsulation adoption, driven by a push to improve vehicle aerodynamics and fuel efficiency. The aftermarket segment is gaining momentum due to the extended use of vehicles in the region. Investment in sustainable materials remains moderate but is expected to rise gradually.

Middle East & Africa Automotive Engine Encapsulation Market Trends

Emerging Markets Accelerate Adoption of Engine Encapsulation

The Middle East & Africa region is witnessing gradual growth in automotive engine encapsulation, primarily fueled by expanding automotive manufacturing in the UAE and South Africa. In 2024, the UAE accounted for around 40% of the region’s encapsulation market, with a strong focus on encapsulation for SUVs and luxury vehicles, which require advanced noise and heat insulation. South Africa is seeing an increase in demand for firewall and underbody encapsulation due to vehicle safety regulations and durability requirements in harsh environments. Investments in sustainable and recyclable materials are limited but gaining attention among leading manufacturers.

Top Countries Holding Highest Market Share

-

China – 28.7% Market Share:China leads due to its massive automotive production scale and stringent environmental regulations, driving demand for advanced engine encapsulation solutions.

-

United States – 24% Market Share:The U.S. maintains a significant share, supported by robust automotive manufacturing and a strong emphasis on noise reduction and thermal management technologies.

Market Competition Landscape

The automotive engine encapsulation market is highly competitive, with several key players focusing on product innovation, strategic partnerships, and expanding manufacturing capacities to maintain and grow their market presence. Leading companies are investing heavily in research and development to introduce lightweight, sustainable, and high-performance encapsulation materials that meet stringent emission and noise regulations globally. The market is also witnessing mergers and acquisitions aimed at broadening product portfolios and geographic reach. Many players are enhancing their capabilities in advanced materials such as thermoplastics and composites to cater to the increasing demand from electric and hybrid vehicle segments. Furthermore, customization and modular design solutions are gaining traction as manufacturers seek to reduce vehicle assembly time and cost. The competitive landscape is shaped by strong regional players in Asia-Pacific, Europe, and North America, with ongoing investments in automated production technologies to improve quality and scalability.

Companies Profiled in the Automotive Engine Encapsulation Market Report

Technology Insights for the Automotive Engine Encapsulation Market

The automotive engine encapsulation market is experiencing significant technological advancements focused on enhancing thermal insulation, noise reduction, and vibration dampening for modern engines. Innovations in lightweight composite materials such as carbon fiber reinforced plastics and advanced thermoplastics are increasingly used to reduce overall vehicle weight while maintaining high durability and heat resistance. Integration of smart materials that can adapt to temperature changes is gaining traction, providing dynamic thermal management to improve engine efficiency and passenger comfort. Advanced manufacturing techniques, including injection molding and automated assembly lines, allow for precise encapsulation designs that fit complex engine architectures. Furthermore, eco-friendly materials derived from recycled polymers and bio-based composites are being adopted to meet growing environmental regulations. The incorporation of sound-absorbing foams and multi-layer barriers is improving noise reduction performance, critical for electric and hybrid vehicles where engine noise masking is essential. Digital twin technology is also being applied to simulate encapsulation performance, optimizing material use and design before production. This focus on material science, coupled with automation and digital tools, is driving the market toward more efficient, sustainable, and customizable engine encapsulation solutions.

Recent Developments in the Global Automotive Engine Encapsulation Market

-

In February 2024, Faurecia launched a new range of lightweight engine encapsulation solutions using bio-based thermoplastic composites, reducing material weight by up to 20% while maintaining high thermal resistance.

-

In September 2023, Benteler International AG unveiled an advanced encapsulation system designed for electric vehicle powertrains, incorporating multi-layer insulation to enhance thermal management and reduce noise.

-

In April 2023, Dana Incorporated expanded its production facility in North America to increase capacity for engine encapsulation parts, targeting improved supply chain efficiency and faster delivery times.

-

In November 2023, Toyoda Gosei Co., Ltd. introduced a next-generation engine cover with integrated sound absorption technology, boosting noise reduction by 15% compared to conventional encapsulation systems.

Scope of Automotive Engine Encapsulation Market Report

The scope of the Automotive Engine Encapsulation Market report encompasses comprehensive analysis of product types, applications, and end-user segments worldwide. It covers key encapsulation materials including thermoplastics, composites, and foams, with detailed insights into their performance in thermal insulation, noise reduction, and vibration control. The report evaluates encapsulation solutions for various engine types such as internal combustion engines, hybrid powertrains, and electric motors, reflecting the growing shift toward electrification. Applications studied range from passenger vehicles to commercial trucks, highlighting demand variations driven by vehicle class and usage. End-user segments include OEMs (Original Equipment Manufacturers) and aftermarket suppliers, with a focus on regional manufacturing hubs and emerging markets. The report also provides a detailed assessment of technological innovations, including the integration of lightweight materials and smart encapsulation systems that improve engine efficiency and reduce emissions. Furthermore, it explores regulatory impacts related to environmental standards and noise pollution controls, which shape product development and market expansion. Supply chain dynamics, competitive landscape, and recent developments are included to give stakeholders a holistic understanding of market opportunities and challenges. Overall, the report serves as a critical resource for manufacturers, suppliers, and investors aiming to capitalize on the evolving automotive engine encapsulation market landscape.

Automotive Engine Encapsulation Market Report Summary

| Report Attribute/Metric |

Report Details |

|

Market Revenue in 2024

|

USD 4572.24 Million

|

|

Market Revenue in 2032

|

USD 6755.29 Million

|

|

CAGR (2025 - 2032)

|

5%

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2032

|

|

Historic Period

|

2020 - 2024

|

|

Segments Covered

|

By Types

By Application

By End-User

-

Passenger Cars

-

Light Commercial Vehicles (LCVs)

-

Heavy Commercial Vehicles (HCVs)

-

Luxury Vehicles

-

Electric & Hybrid Vehicles

|

|

Key Report Deliverable

|

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape

|

|

Region Covered

|

North America, Europe, Asia-Pacific, South America, Middle East, Africa

|

|

Key Players Analyzed

|

Dana Incorporated, Faurecia SE, Adient plc, Magna International Inc., Lear Corporation, Benteler International AG, Toyoda Gosei Co., Ltd., Plastic Omnium SE, Hanon Systems, Tenneco Inc.

|

|

Customization & Pricing

|

Available on Request (10% Customization is Free)

|