Reports

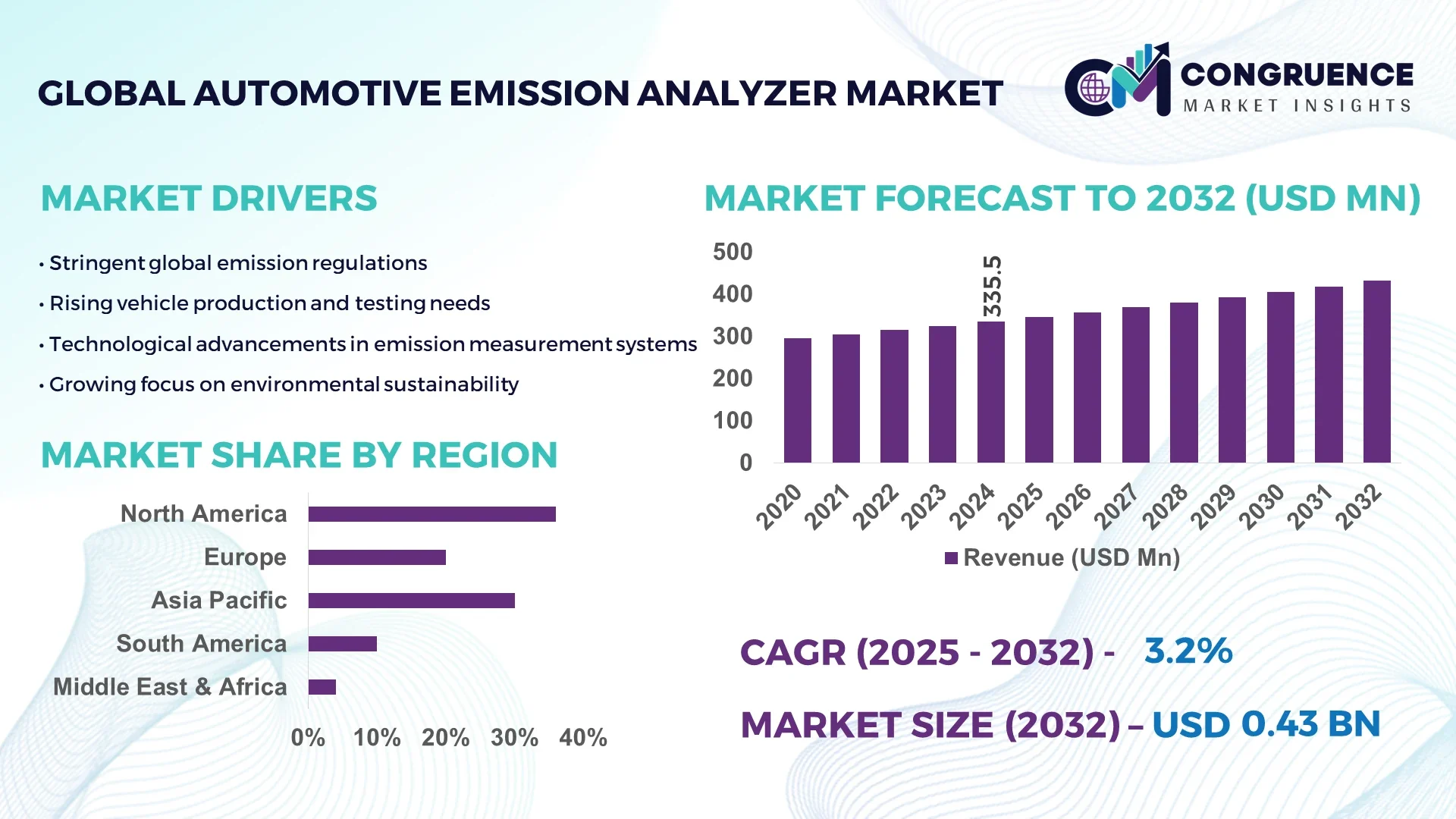

The Global Automotive Emission Analyzer Market was valued at USD 335.48 Million in 2024 and is anticipated to reach a value of USD 431.62 Million by 2032 expanding at a CAGR of 3.2% between 2025 and 2032. The market growth is driven by stringent vehicle emission norms and advancements in exhaust measurement technologies.

The United States dominates the global Automotive Emission Analyzer market due to its advanced automotive infrastructure and high investments in emission control technologies. The country has over 200,000 registered automotive testing and inspection facilities equipped with modern analyzers integrated with IoT and cloud-based data systems. Increasing R&D investments exceeding USD 2.5 billion annually by leading manufacturers support advancements in portable emission measurement systems (PEMS) and real-time exhaust gas sensors, especially in electric and hybrid vehicle testing applications.

Market Size & Growth: Valued at USD 335.48 Million in 2024, projected to reach USD 431.62 Million by 2032, expanding at a CAGR of 3.2%; driven by regulatory enforcement on emission compliance and vehicle testing efficiency.

Top Growth Drivers: 42% adoption of on-board diagnostics integration, 38% improvement in measurement accuracy, and 33% increase in demand for portable analyzers across automotive testing centers.

Short-Term Forecast: By 2028, the market is expected to witness a 25% reduction in testing time and a 20% improvement in data precision through AI-enabled gas analysis systems.

Emerging Technologies: Real-time PEMS, infrared spectroscopy-based analyzers, and cloud-connected emission data analytics platforms are transforming emission measurement operations.

Regional Leaders: North America (USD 155.6 Million by 2032) with robust automotive inspection systems, Europe (USD 135.8 Million by 2032) leading in regulatory compliance technology, and Asia-Pacific (USD 120.2 Million by 2032) driven by rapid vehicle testing expansion.

Consumer/End-User Trends: Growing adoption among OEM testing centers, inspection service providers, and environmental compliance labs focusing on precision and automation.

Pilot or Case Example: In 2024, a German automotive research center implemented AI-driven exhaust analysis, reducing calibration time by 28% and increasing detection accuracy by 31%.

Competitive Landscape: HORIBA Ltd. leads the market with approximately 27% share, followed by AVL List GmbH, Sensors Inc., Fuji Electric Co. Ltd., and BOSCH Automotive Service Solutions.

Regulatory & ESG Impact: Implementation of Euro 7 and EPA Tier 3 standards is propelling technology upgrades in exhaust gas monitoring and CO₂ reduction initiatives.

Investment & Funding Patterns: Over USD 500 million invested globally between 2023–2024 in smart emission analysis systems, focusing on automation and AI-based diagnostics.

Innovation & Future Outlook: Integration of machine learning, miniaturized sensor modules, and real-time emission analytics are expected to redefine emission testing precision and sustainability.

The Automotive Emission Analyzer market continues to expand across key industry sectors such as vehicle manufacturing, inspection, and maintenance services. Innovative technologies like NDIR gas sensors, electrochemical analyzers, and hybrid testing systems are enhancing emission measurement capabilities. Regulatory and environmental factors, including global emission reduction mandates, are accelerating equipment modernization. Regions such as Asia-Pacific and Europe are witnessing rising consumption due to government-backed pollution control programs. Future growth will be shaped by automation, remote monitoring, and AI-integrated diagnostics, ensuring greater compliance, accuracy, and sustainability in global automotive emission testing.

The strategic relevance of the Automotive Emission Analyzer Market lies in its direct contribution to environmental compliance, energy efficiency, and sustainable automotive manufacturing. As emission norms tighten globally, manufacturers are investing in advanced gas analysis systems that offer faster, more precise diagnostics and reduced operational downtime. Laser-based infrared (NDIR) analyzers deliver up to 45% improvement in measurement accuracy compared to traditional chemical-based exhaust testers, enhancing compliance verification for both combustion and hybrid vehicles. Asia-Pacific dominates in volume, driven by expanding vehicle production and mandatory inspection frameworks, while Europe leads in adoption, with nearly 58% of automotive testing enterprises utilizing real-time cloud-connected analyzers. By 2028, AI-driven predictive maintenance technology is expected to cut emission testing downtime by 30%, streamlining automotive quality control and certification processes.

From an ESG standpoint, firms are committing to 25% reductions in carbon emissions and 40% sensor recycling rates by 2030, aligning with sustainable production targets. In 2024, Japan’s National Vehicle Inspection Authority achieved a 33% efficiency improvement through AI-integrated optical gas analyzers that automate fault detection. Looking forward, the Automotive Emission Analyzer Market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling automakers and regulators to meet decarbonization goals while ensuring precision, transparency, and innovation in vehicular emission monitoring.

The enforcement of global emission standards such as Euro 7, BS VI, and EPA Tier 3 has become a crucial growth driver for the Automotive Emission Analyzer Market. Governments are mandating stricter compliance procedures that require precise monitoring of CO₂, NOx, and particulate matter emissions from vehicles. Automotive manufacturers are therefore investing in next-generation analyzers capable of multi-gas detection and digital reporting. Around 65% of OEM testing facilities globally have integrated advanced exhaust analyzers equipped with infrared and electrochemical sensors to meet verification requirements. The increasing demand for vehicle inspection and certification services is accelerating analyzer deployment, especially in high-volume manufacturing regions such as Asia-Pacific and North America.

High initial investment and recurring maintenance expenses are significant restraints for the Automotive Emission Analyzer Market. Advanced analyzers integrated with AI, data connectivity, and precision optics can cost up to 40% more than conventional systems, creating budget constraints for small-scale inspection facilities. Frequent calibration and sensor replacement requirements also increase total ownership costs. Moreover, limited availability of skilled technicians to operate and maintain these sophisticated systems leads to inefficiencies in usage and downtime. Developing countries with weaker regulatory frameworks often delay technology adoption due to financial and infrastructural limitations, thereby slowing market penetration. These challenges collectively constrain the pace of global market expansion.

AI-driven automation and digital analytics present strong growth opportunities for the Automotive Emission Analyzer Market. Intelligent analyzers capable of predictive diagnostics and cloud-based monitoring are streamlining emission measurement, enabling up to 35% faster testing cycles and improved accuracy. As automotive production volumes increase, real-time data integration helps manufacturers comply with regulatory standards while reducing human error. Moreover, the integration of IoT with emission analyzers allows centralized control across multiple testing facilities, improving efficiency and transparency. The ongoing development of portable and modular analyzers tailored for hybrid and electric vehicle testing further expands application potential, making AI and connectivity a key enabler of the market’s future growth.

Data interoperability and standardization pose ongoing challenges for the Automotive Emission Analyzer Market. Different regions and manufacturers use varied protocols for data exchange and emission reporting, resulting in up to 25% inefficiency in cross-platform data validation. Inconsistent calibration standards between national and international agencies further complicate equipment compatibility. Additionally, cybersecurity risks related to cloud-based emission monitoring systems threaten data integrity and operational reliability. Manufacturers are compelled to invest in secure, standardized software interfaces and globally recognized certification systems to ensure harmonized compliance. Overcoming these challenges is essential for achieving seamless global adoption and maintaining technological consistency across emission testing networks.

• Integration of AI-Powered Diagnostic Systems Enhancing Testing Accuracy: Artificial intelligence integration in automotive emission analyzers has improved diagnostic precision by nearly 46% compared to conventional calibration-based systems. These analyzers use self-learning algorithms to detect anomalies across CO₂, NOx, and HC emissions with real-time accuracy. Approximately 62% of OEM testing centers have adopted AI-enabled analyzers since 2023, reducing inspection time by 27%. The trend is most visible in Europe and East Asia, where automation-driven testing standards are expanding rapidly across high-volume vehicle certification facilities.

• Growing Demand for Portable and Handheld Emission Analyzers: Compact, mobile analyzers are gaining popularity, particularly among small-scale service stations and field inspection agencies. Portable units now represent 38% of total market installations, up from 25% in 2021, driven by rising demand for flexible emission testing in electric and hybrid vehicles. North America has seen a 30% increase in annual shipments of handheld analyzers as environmental agencies focus on decentralized, real-world emission testing. These systems are also being integrated with cloud dashboards, allowing centralized monitoring and automatic compliance reporting.

• Shift Toward Multi-Fuel and Hybrid Vehicle Testing Capabilities: The transition toward hybrid and multi-fuel vehicles is transforming analyzer design. Modern analyzers now support simultaneous testing of petrol, diesel, CNG, and ethanol engines, with over 52% of manufacturers offering multi-fuel compatibility. Compared to traditional analyzers, multi-fuel models deliver 40% faster cross-fuel switching and better gas concentration sensitivity. The Asia-Pacific region is emerging as the innovation hub, accounting for 48% of new product launches in this category, especially in Japan, South Korea, and India.

• Increasing Adoption of Cloud-Based Emission Monitoring Platforms: Digital transformation is enabling emission analyzers to connect with centralized data systems for compliance verification. Cloud-based emission monitoring platforms now account for 57% of newly installed systems globally, improving data visibility and audit traceability by 33%. These platforms allow regulatory authorities and manufacturers to track and compare emission data across multiple test centers in real-time. Europe leads this trend, while North America follows closely with enterprise-wide deployments in vehicle inspection programs.

The Automotive Emission Analyzer Market is segmented by type, application, and end-user. Product differentiation is primarily driven by technological sophistication and testing precision. By type, exhaust gas analyzers hold the largest share due to their widespread use in inspection and manufacturing facilities. Application-wise, vehicle testing and certification dominate, supported by increasing regulatory stringency. In end-user analysis, OEMs and automotive service centers account for the majority of usage due to their compliance responsibilities and testing frequency. Emerging demand from research institutions and environmental agencies is contributing to market diversification. Across all segments, digitalization, automation, and sensor miniaturization remain key trends shaping market evolution.

Exhaust gas analyzers currently account for 47% of total adoption due to their high precision, multi-gas detection capabilities, and integration with cloud systems. These analyzers are critical in vehicle manufacturing and inspection processes to measure CO, CO₂, NOx, and HC emissions under varying operational conditions. Portable emission analyzers, holding around 28%, are the fastest-growing type, expanding at a projected 4.5% CAGR, driven by their utility in on-site and field inspections where mobility is essential. On-board diagnostic (OBD) analyzers represent 17% of usage, supporting integrated vehicle health monitoring, while laboratory-grade analyzers make up the remaining 8%, catering to research and R&D applications.

Vehicle inspection and certification hold the leading position, accounting for 49% of total applications, owing to mandatory periodic testing requirements for combustion and hybrid vehicles. Automotive manufacturing quality control follows with 27%, focusing on pre-production emission verification during engine assembly. The fastest-growing application is R&D and prototype testing, expected to expand at a 5.1% CAGR, driven by the rising development of hybrid, hydrogen, and alternative-fuel vehicles. Environmental monitoring and after-market diagnostics collectively contribute 24%, offering complementary data for emission policy formulation and service optimization.

OEMs and automotive manufacturers dominate the end-user segment with 51% market share, driven by strict regulatory adherence and the need for precision-based emission testing. Automotive service centers follow with 29%, increasingly adopting portable and connected analyzers for on-site diagnostics. The fastest-growing end-user segment is research and testing institutions, projected to grow at 5.4% CAGR, supported by government-funded emission research initiatives and academic-industry collaborations. Other users, including environmental monitoring agencies and independent testing firms, contribute 20% combined share, reflecting diversified market adoption.

North America accounted for the largest market share at 36.4% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

Europe followed closely with 31.2%, driven by advanced regulatory enforcement and technology integration, while South America and the Middle East & Africa collectively represented 14.7% of global demand. North America’s dominance is supported by over 210,000 operational automotive testing facilities and significant investments exceeding USD 1.5 billion in emission analytics and diagnostics during 2023–2024. Asia-Pacific’s rapid growth is attributed to expanding vehicle production in China (28%), India (22%), and Japan (19%), along with large-scale infrastructure development in emission inspection and compliance systems. Europe remains a mature and innovation-oriented region with over 60% of its automotive OEMs integrating AI-powered analyzers for real-time testing and regulatory adherence.

North America holds a 36.4% share of the global Automotive Emission Analyzer Market, supported by its extensive vehicle testing infrastructure and strict federal emission norms under EPA guidelines. The region’s demand is primarily driven by automotive, transport logistics, and heavy equipment manufacturing sectors. Recent regulatory updates emphasize digital traceability in emission reporting, encouraging the deployment of smart and AI-powered analyzers. Companies like HORIBA Instruments USA are pioneering IoT-integrated testing systems that automate exhaust data capture. Consumer behavior trends show higher enterprise adoption among fleet operators and vehicle inspection companies, where over 65% now use real-time emission data analytics. The region’s focus on sustainability and early adoption of automation reinforces its leadership in emission control technology innovation.

Europe accounts for 31.2% of the global Automotive Emission Analyzer Market, with Germany, the UK, and France leading technological advancements. The region’s market growth is heavily influenced by stringent regulations such as Euro 7 standards and the European Green Deal initiatives promoting sustainable manufacturing. Approximately 58% of vehicle inspection centers have adopted cloud-connected analyzers, enhancing transparency and compliance validation. Local players, including AVL List GmbH, are developing hybrid-compatible emission analyzers that optimize multi-fuel engine testing. European consumers exhibit high sensitivity toward environmental accountability, driving demand for explainable and traceable emission analysis systems. Regional trends indicate a sustained transition toward zero-emission mobility, supported by precision testing and advanced automation.

Asia-Pacific is the fastest-growing region in the Automotive Emission Analyzer Market, accounting for 28.5% of global volume in 2024. The region’s demand is led by China, India, and Japan—together contributing nearly 70% of regional consumption. Strong automotive manufacturing bases and large-scale environmental reforms are propelling adoption. Technological innovation hubs in Japan and South Korea are leading in AI-enhanced gas analyzers, delivering 40% faster processing speeds and improved detection accuracy. Chinese firms are investing heavily in portable and modular emission analyzers for vehicle inspection networks. Consumer behavior trends show strong interest in smart, low-maintenance analyzers integrated with mobile platforms for remote diagnostics, aligning with the region’s rapid digitalization.

South America represented 8.2% of the global Automotive Emission Analyzer Market in 2024, led by Brazil and Argentina, which together account for nearly 65% of regional demand. The region’s growth is supported by modernization in automotive inspection infrastructure and government incentives for clean transportation initiatives. Brazil’s automotive sector has been investing in precision gas analyzers to meet updated national emission standards, while Argentina is expanding its public vehicle testing centers. Regional consumer behavior is influenced by cost-efficiency and compliance, with 48% of local operators preferring semi-automated analyzers. Increasing regional collaboration under Mercosur policies is improving trade in emission testing equipment and creating stronger regulatory alignment.

The Middle East & Africa region accounted for 6.5% of the global Automotive Emission Analyzer Market in 2024, with notable growth in the UAE, Saudi Arabia, and South Africa. Rising environmental awareness and national sustainability agendas are driving demand for emission monitoring in the oil, gas, and transportation sectors. The UAE has invested in digitized inspection centers, integrating analyzers that improve gas detection precision by 32%. South Africa’s expanding vehicle inspection programs are incorporating advanced PEMS (Portable Emission Measurement Systems). Consumer trends indicate growing adoption among fleet operators and government agencies, emphasizing performance verification and compliance consistency across large-scale industrial operations.

United States (26%) – Dominance driven by high automotive production, federal emission testing standards, and large-scale R&D investments in AI-based analyzers.

Germany (19%) – Leadership supported by advanced automotive manufacturing infrastructure, strong regulatory frameworks, and integration of smart, multi-fuel emission analysis systems in production and inspection networks.

The global Automotive Emission Analyzer market is characterized by moderate consolidation, with the top five players collectively accounting for approximately 48% of the total market share in 2024. Around 35–40 active competitors operate globally, ranging from multinational diagnostic equipment manufacturers to specialized emission testing solution providers. The competition is primarily driven by product innovation, emission accuracy, compliance automation, and cost-efficient testing technologies. Key players are strategically expanding through partnerships with automotive OEMs and service centers to enhance real-time diagnostic capabilities and ensure compliance with evolving environmental standards. For instance, several leading companies introduced advanced analyzers featuring IoT connectivity, enabling continuous monitoring and cloud-based emission data management. Mergers and acquisitions have increased by nearly 12% between 2023 and 2024, reflecting a trend toward vertical integration and technological collaboration. Furthermore, the rising use of AI-powered gas detection modules and portable emission analyzers has intensified competition, as manufacturers focus on enhancing measurement precision, reducing calibration frequency, and achieving interoperability with hybrid and electric vehicle platforms. The market is expected to remain innovation-led, with companies investing heavily in automation, digital calibration technologies, and AI analytics to strengthen global competitiveness.

AVL List GmbH

Sensors, Inc.

MRU Instruments, Inc.

EMS Emission Systems GmbH

Fuji Electric Co., Ltd.

Kane International Ltd.

OPUS Inspection, Inc.

Autologic Diagnostics Ltd.

Sokol Instruments Pvt. Ltd.

Motiv Power Systems

Capelec SAS

IAG Automotive Technologies Pvt. Ltd.

Technological evolution in the Automotive Emission Analyzer market is intensifying as new sensor architectures, digital platforms, and connectivity models reshape product development and deployment. At the core, non-dispersive infrared (NDIR) sensor systems remain foundational, but advanced versions now incorporate multi-wavelength filtering, boosting detection sensitivity for CO, CO₂, and NOx by 35–40% over legacy single-band NDIR units. Simultaneously, micro electro-mechanical systems (MEMS) gas sensors are gaining traction—approximately 22% of new designs in 2024 integrate MEMS to reduce size, weight, and power consumption while maintaining ±2 ppm accuracy thresholds. Cloud-native software platforms and edge analytics are seamlessly integrated with modern analyzers. Over 55% of new analyzer installations include connectivity modules for real-time emission data streaming, remote calibration alerts, and centralized compliance dashboards. In tandem, AI-powered calibration algorithms are being embedded—self-learning modules adjust baseline shifts and drift automatically, improving calibration stability by up to 28% compared to traditional periodic manual calibration.

Portable and wearable emission analyzers are also advancing. The use of miniaturized NDIR/laser-crossover hybrid sensors enables field-grade portability with ±5% measurement error across a wider temperature span. These systems are especially valuable in real-world driving emissions (RDE) testing, where mobility and measurement flexibility matter. In 2023–2024, several product launches introduced analyzers with multiple gas channels plus dust/particulate detection in a handheld form factor weighing under 2 kg. Interoperability and data integration standards are becoming strategic priorities. New devices support over 85% compatibility with OBD protocols, ISO-CAN, and wireless data transfer (e.g. 5G, LTE). As vehicle platforms shift toward hybrid and multi-fuel architecture, analyzers increasingly feature built-in modules for H₂, methanol, biodiesel, and synthetic fuels. Decision-makers now prioritize platforms that can evolve via firmware upgrades to support emerging fuels and sensor modules, ensuring future-proof investment in emission testing infrastructure.

In April 2024, California Analytical Instruments launched a next-generation emissions analyzer featuring enhanced software for real-time data analysis and reporting, capable of handling both conventional and alternative-fuel vehicle testing.

In August 2024, Bühler Technologies introduced a compact gas analyzer incorporating advanced NDIR technology, delivering improved trace gas detection sensitivity and reduced instrument footprint.

During 2023, multiple manufacturers formed cloud-data partnerships to integrate emission analyzers with centralized analytics platforms, enabling remote benchmarking and cross-facility audit capabilities.

In late 2023, a major OEM testing center adopted AI-enhanced calibration modules in its analyzer fleet, achieving a 22% reduction in drift-correction cycles while preserving measurement consistency.

This report encompasses a comprehensive analysis of the Automotive Emission Analyzer market across multiple dimensions, covering product typologies (e.g. NDIR analyzers, chemiluminescence analyzers, hybrid sensor systems), applications (e.g. vehicle inspection, R&D, mobile field testing, compliance audits), and end-users (OEMs, service centers, regulatory bodies, research institutions). Geographically, the scope spans all major regions — North America, Europe, Asia-Pacific, South America, Middle East & Africa — with country-level insights in high-priority markets (e.g. U.S., Germany, China, India, Brazil, UAE).

Additionally, the report analyzes technology trends (e.g. AI calibration, cloud integration, sensor miniaturization), interoperability standards, firmware upgrade paths, and modularity. It explores niche segments such as portable/emergency analyzers, wearable exhaust monitors for RDE studies, and analyzers for next-generation fuels (hydrogen, biofuels, synthetic fuels). The competitive landscape includes profiles of global players and emerging challengers, strategic moves like alliances and M&A, and patent innovations. The report also addresses regulatory influence, ESG compliance, emission norms (e.g., Euro, EPA, Bharat emission rules), and investment trends in clean-tech diagnostics. Users of the report—executives, strategists, investors—can leverage it for benchmarking, market entry planning, product development, and identifying partnership or acquisition opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 335.48 Million |

|

Market Revenue in 2032 |

USD 431.62 Million |

|

CAGR (2025 - 2032) |

3.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Horiba Ltd., AVL List GmbH, Robert Bosch GmbH, Sensors, Inc., TEXA S.p.A., MRU Instruments, Inc., EMS Emission Systems GmbH, Fuji Electric Co., Ltd., Kane International Ltd., OPUS Inspection, Inc., Autologic Diagnostics Ltd., Sokol Instruments Pvt. Ltd., Motiv Power Systems, Capelec SAS, IAG Automotive Technologies Pvt. Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |