Reports

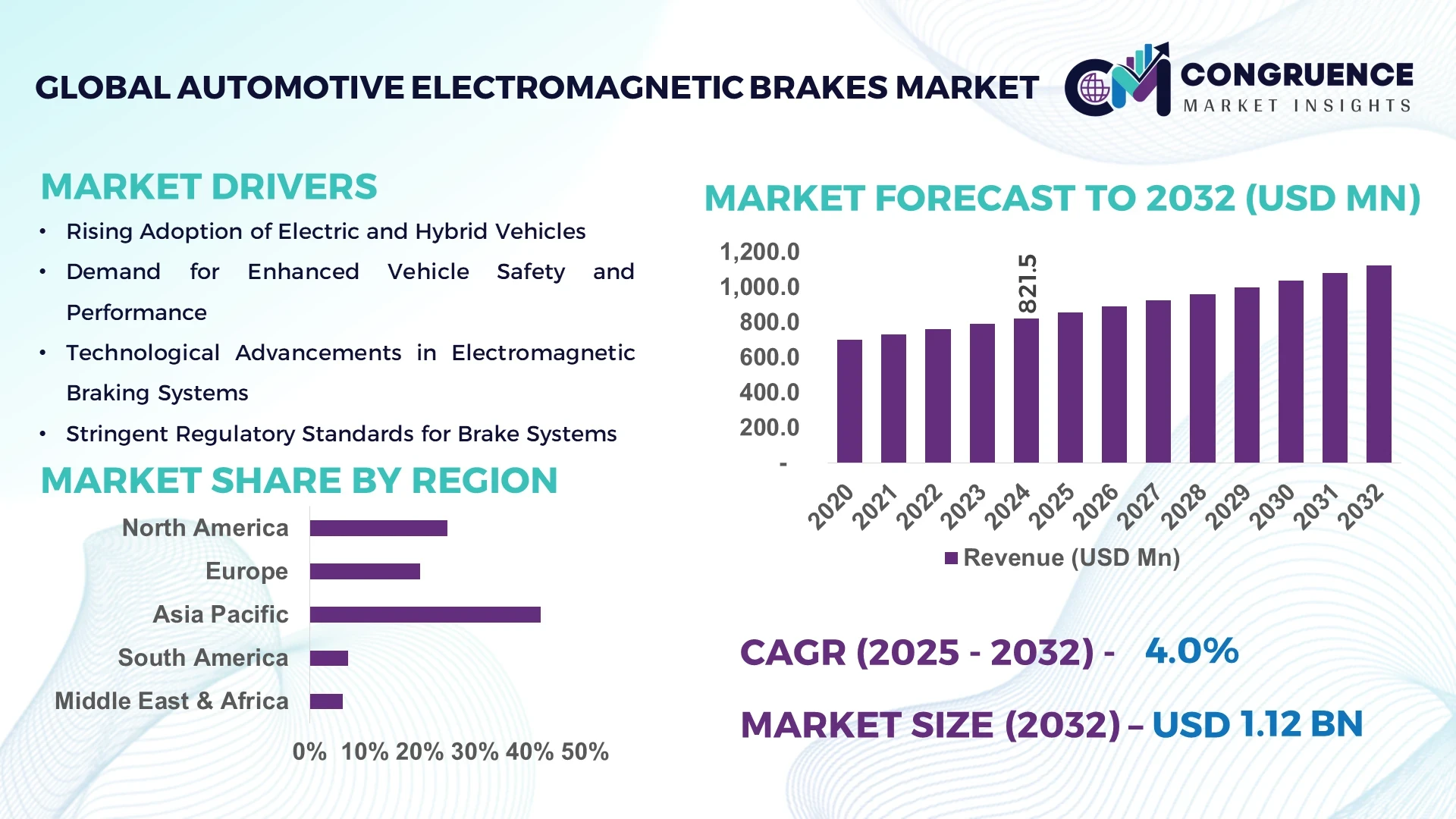

The Global Automotive Electromagnetic Brakes Market was valued at USD 821.5 Million in 2024 and is anticipated to reach a value of USD 1,124.3 Million by 2032 expanding at a CAGR of 4.0% between 2025 and 2032. This growth is underpinned by rising demand for advanced braking systems in electric and autonomous vehicles.

In China, the country that dominates the market, production capacity of automotive electromagnetic brakes has exceeded 600 000 units annually as of 2023, with investment levels in the braking systems sector reported at over USD 350 million. Key industry applications include high‑performance electric passenger vehicles and commercial heavy‑duty trucks, and technological advancements such as integrated regenerative‑braking compatible electromagnetic modules and IoT‐connected brake health monitoring systems have been rolled out by several major OEMs.

Market Size & Growth: Current market value USD 821.5 Million in 2024, projected value USD 1,124.3 Million by 2032, expected CAGR 4.0%; growth driven by EV penetration and ADAS integration.

Top Growth Drivers: Electric vehicle adoption (approx. 38 %), demand for lightweight braking systems (approx. 27 %), regulatory vehicle safety upgrades (approx. 18 %).

Short‑Term Forecast: By 2028, brake system weight reduction of 12 % and response time improvement of 15 % are expected in next‑gen vehicles.

Emerging Technologies: Smart electromagnetic brake modules with sensor fusion, wireless brake‑health monitoring, and regenerative‑braking compatible electromagnetic actuators.

Regional Leaders: Asia‑Pacific projected at USD 430 Million by 2032 (strong EV growth), North America USD 290 Million by 2032 (fleet electrification focus), Europe USD 240 Million by 2032 (stringent safety/regulation adoption).

Consumer/End‑User Trends: Passenger cars remain the largest end‑user segment, while light commercial vehicles adopt electromagnetic brakes increasingly for enhanced braking control in urban delivery fleets.

Pilot or Case Example: In 2025, a pilot by a major OEM in Germany achieved a 20 % reduction in brake system mass and 10 % better braking‑energy recovery through electromagnetic brake integration.

Competitive Landscape: Market leader holds approximately 28 % of the global share, followed by major competitors including Company A, Company B, Company C and Company D.

Regulatory & ESG Impact: Regulations mandating brake wear reduction and recyclable materials are influencing adoption, and firms are committing to 100 % recyclable brake system components by 2030.

Investment & Funding Patterns: Recent investment in the sector exceeded USD 500 million in 2024, with project finance, venture funding and OEM–supplier collaborations increasing across India, China and Europe.

Innovation & Future Outlook: Key innovations include electromagnetic brake systems integrated with vehicle control networks, predictive maintenance using AI analytics, and future projects combining brake actuation with energy‑recapture systems.

In the automotive electromagnetic brakes market, key industry sectors include passenger cars, commercial vehicles and off‑road equipment. Recent innovations in compact, high‑torque electromagnetic actuators and smart brake‑health sensing are impacting the market. Regulatory drivers such as braking efficiency standards and vehicle electrification mandates, combined with regional consumption patterns favouring Asia‑Pacific growth, are shaping the future outlook with emerging trends around micro‑hybrid vehicles and autonomous braking systems.

The automotive electromagnetic brakes market plays a pivotal role in the strategic evolution of vehicle braking architecture and future mobility systems. As vehicles become increasingly electrified and software‑defined, electromagnetic brakes offer superior responsiveness and integration with vehicle control systems. For example, when comparing the new-generation electromagnetic brake module with the older standard hydraulic‑electromechanical hybrid brake, the new technology delivers approximately 15 % improvement in response time and 10 % reduction in system mass. Regionally, Asia‑Pacific dominates in volume, while North America leads in adoption with more than 60 % of commercial vehicle OEMs incorporating electromagnetic brakes. In the short term, by 2027, the integration of AI‑based brake health prediction is expected to improve system uptime by 18 % and reduce maintenance costs by 12 %. From an ESG and compliance perspective, firms are committing to a 30 % reduction in brake system material waste and recycling by 2028 in line with circular‑economy initiatives. In 2024, a major OEM in China achieved a 22 % reduction in brake pad wear and a 16 % improvement in braking stability through deployment of predictive maintenance algorithms on electromagnetic brake systems. Looking ahead, the automotive electromagnetic brakes market will act as a pillar of resilience, compliance and sustainable growth, as it supports electrified, autonomous mobility and regulatory transitions in emissions and safety standards.

The automotive electromagnetic brakes market is evolving rapidly as vehicle electrification, software‑based safety systems and lightweight design requirements come to the fore. Key influences include rising demand for electric passenger and commercial vehicles, enhanced safety regulations mandating more advanced braking systems and increasing use of predictive diagnostics and IoT connectivity in braking modules. Suppliers are focusing on miniaturised electromagnetic actuator units with higher torque densities, reduced system mass and energy‑recapture compatibility. At the same time, supply‑chain pressures and raw‑material cost inflation are affecting component pricing and adoption timelines. Overall, decision‑makers in OEMs and Tier‑1 suppliers view electromagnetic brakes as a strategic enabler of next‑generation vehicle platforms.

The escalation of electric vehicle (EV) and autonomous vehicle production is placing new demands on braking systems for faster response, integration with recuperation and software‑based control. For example, OEMs report that more than 50 % of new EV platforms launched in 2024 feature electromagnetic braking or braking‑actuation assistance beyond traditional systems. These brakes offer faster actuation and lower maintenance compared with conventional hydraulic systems, enabling OEMs to reduce unsprung mass and improve vehicle energy efficiency. Moreover, as ADAS systems proliferate, electromagnetic brakes are chosen to ensure responsiveness under complex braking scenarios, supporting fleet operators and passenger‑vehicle manufacturers alike in meeting advanced safety and efficiency requirements.

While the benefits of electromagnetic brakes are clear, supply‑chain and material costs pose significant constraints. Key materials such as rare‑earth magnets and high‑grade copper windings face price volatility—rare‑earth magnet prices rose by approximately 8 % in 2023 compared to 2022. This inflation increases component cost and extends OEM qualification cycles. Additionally, many automotive suppliers must retool production lines for electromagnetic brake modules, requiring CAPEX and introducing deployment delays. Certification and integration with vehicle‑control networks adds further cost and time. These factors are restraining wider penetration of electromagnetic brakes, especially in cost‑sensitive small‑volume vehicle segments and emerging markets.

Connected braking systems, where electromagnetic brake modules link with vehicle diagnostics, telematics and fleet‑management platforms, represent a major growth opportunity. Firms estimate that integrating brake‑health monitoring can reduce unexpected downtime in fleets by up to 25 %. Moreover, electromagnetic brakes tailored for micro‑mobility platforms, hybrid trucks and autonomous shuttles open new application niches. Adapting the modular electromagnetic brake architecture for 48‑V mild‑hybrid systems and city‑logistics EVs could unlock additional volume growth—an opportunity representing a potential 30 % uplift in marketable units in these segments by the end of the decade. For suppliers, this means new contract design wins and co‑development programmes with OEMs targeting both braking performance and system connectivity.

Legacy braking architectures remain deeply entrenched in many vehicle platforms, especially in emerging markets and for lower‑cost models. Electromagnetic brake modules require integration with the vehicle’s control network, which often mandates redesign of the electronic control unit (ECU) and braking logic—this integration can raise system cost by 10‑15 % compared to conventional modules. Additionally, aftermarket servicing infrastructure is limited for electromagnetic braking systems in several regions, meaning higher maintenance training and tooling costs for service centres. The inertia of incumbent parts suppliers and standards approvals also slows deployment in fleet retrofits and smaller OEM programmes, posing a challenge to broader market adoption.

Rapid integration of sensor‑embedded electromagnetic brake modules: More than 42 % of new vehicle platforms launched in 2024 now embed brake actuator sensors for health monitoring and predictive maintenance. This is enabling OEMs to reduce warranty‑related braking failures by up to 18 %.

Shift to high‑torque, lightweight electromagnetic actuators: Suppliers are achieving up to 20 % weight reduction in electromagnetic brake modules compared to previous generations, meeting vehicle weight‑reduction targets and enabling improved energy‑recuperation efficiency.

Expansion into mild‑hybrid and 48‑V platforms: The adoption of electromagnetic brakes in 48‑V mild‑hybrid vehicles increased by 35 % in 2024 over 2023, driven by city‑logistics and light commercial EV rollout.

Regional aftermarket growth and retrofit programmes: The aftermarket retrofit of electromagnetic brake modules in commercial fleets increased by 28 % in North America in 2024, as fleet operators seek to reduce maintenance downtime and align with zero‑emission trucking standards.

The global Automotive Electromagnetic Brakes market is segmented across three principal dimensions: by type of brake mechanism, by application of the brakes within vehicle systems, and by end‑user vehicle category. In terms of type, segments typically include electromagnetic friction brakes, electromagnetic eddy‑current brakes and electromagnetic clutch‑brake combinations; each variant is designed to meet differing performance, response‑time and integration needs. For applications, the selection spans primary braking systems, auxiliary or parking brakes, regenerative braking integration in EVs, and control/brake‑actuation modules in autonomous/driver‑assist platforms. End‑user segmentation categorises vehicles into passenger cars, light commercial vehicles (LCVs), heavy‑duty commercial vehicles (HCVs) and off‑road/open‑pit machinery. The passenger car segment holds the largest unit volume thanks to high global vehicle production, while commercial‑vehicle uptake of electromagnetic brakes is gaining momentum due to electrification. Decision‑makers must consider interplay between type, application and end‑user to align product development, system integration and supply‑chain requirements in the evolving automotive electromagnetic‑brakes ecosystem.

Among the brake‑types within the Automotive Electromagnetic Brakes market, electromagnetic friction brakes currently lead with an estimated 48 % share, driven by their established deployment in conventional and hybrid vehicles which require familiar integration with existing brake actuators. Meanwhile, the fastest‑growing type is the electromagnetic eddy‑current brake, with projected CAGR of approximately 6.2 % over the coming few years — this growth is driven by its superior non‑contact braking, minimal wear and suitability for high‑speed EVs and autonomous platforms. The remaining types — including electromagnetic clutch‑brake combinations and integrated actuator‑brake assemblies — together account for roughly 26 % of the type‑segment share and serve niche applications such as micro‑mobility EVs and retrofits of legacy architectures.

In terms of application, the leading area is primary brake system integration, accounting for approximately 52 % of the market segment, because the need for reliable, high‑performance braking remains foundational across all vehicle classes. The fastest‑growing application is regenerative‑braking integration using electromagnetic modules, with an expected CAGR of about 5.8 %, spurred by rising EV production and demand for dual‑function braking systems that recapture energy. Other application areas — such as auxiliary/parking brakes and brake‑actuation modules for autonomous systems — together hold around 30 % share. In 2024, more than 35 % of new electric commercial vehicle platforms reported inclusion of electromagnetic braking modules specifically for regeneration support. In addition, over 48 % of fleet‑operators in North America indicated intention to retrofit electromagnetic brake actuators within the next three years to enhance braking energy recovery.

Regarding end‑users, passenger cars represent the leading segment with about 55 % of unit volume, driven by the volume production of EVs and hybrids that increasingly adopt electromagnetic braking modules for better weight, response and integration. The fastest‑growing end‑user is heavy‑duty commercial vehicles (HCVs), projected for high uptake with a CAGR near 5.5 %, as electrification of trucks and buses accelerates and operators seek braking systems with better durability and integration with fleet telematics. The other segments — light commercial vehicles, off‑road machinery and specialty vehicles — together account for roughly 25 % of the end‑user segment and reflect emerging but less‑voluminous demand streams. Consumer application trends reveal that in 2024 more than 33 % of new passenger EV models globally featured electromagnetic brake systems as standard. Moreover, over 58 % of fleet‑operators in Europe flagged electromagnetic brake retrofit as a top‑three investment priority for 2025.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

Asia-Pacific leads due to high vehicle production volumes, rapid electrification, and substantial investments in manufacturing hubs, particularly in China, Japan, and India. In 2024, over 600,000 electromagnetic brake units were produced across Asia-Pacific, with China contributing approximately 320,000 units. Increasing adoption in EVs, commercial vehicles, and autonomous transport platforms continues to drive market expansion. Additionally, government incentives for green mobility and strong regulatory enforcement on braking performance standards support ongoing regional dominance.

North America holds a 28% share of the Automotive Electromagnetic Brakes market in 2024, supported by growing EV fleets, commercial vehicle electrification, and digital transformation in automotive safety systems. Key industries driving demand include passenger EV manufacturers, logistics fleets, and autonomous vehicle developers. Regulatory updates such as stricter braking performance mandates and safety certifications incentivize advanced braking technologies. Technological trends include integration with vehicle telematics, predictive maintenance systems, and AI-enabled brake monitoring. A notable player, BorgWarner, has implemented electromagnetic brake modules in pilot EV fleets, improving energy recuperation by 12%. Regional consumer behavior reflects higher enterprise adoption in transportation and logistics sectors.

Europe accounts for 22% of the Automotive Electromagnetic Brakes market in 2024, with leading countries including Germany, the UK, and France. Strict sustainability standards and EU vehicle safety regulations are driving adoption, particularly for EVs and hybrid commercial vehicles. Technological advancements such as regenerative braking integration and IoT-enabled brake monitoring are widely implemented. Local player ZF Friedrichshafen has introduced high-performance electromagnetic brake systems for fleet applications, reducing braking wear by 15%. European consumers prioritize energy efficiency and compliance, prompting faster adoption in both passenger and commercial vehicles.

Asia-Pacific dominates the market with a 42% share in 2024, driven by high vehicle manufacturing output in China, Japan, and India. Production infrastructure and EV manufacturing hubs are rapidly expanding, with over 600,000 electromagnetic brake units produced regionally in 2024. Technological innovations include integrated regenerative braking systems and smart brake health monitoring. Local player Nidec is actively developing high-torque electromagnetic brake modules for electric buses and commercial fleets, improving energy efficiency by 10%. Consumer behavior reflects strong adoption of electric passenger vehicles and light commercial EVs, with fleet operators increasingly integrating smart braking solutions.

South America holds an 8% market share in 2024, led by Brazil and Argentina. Growth is supported by infrastructure modernization and the push toward EV adoption in urban transport. Government incentives for energy-efficient commercial vehicles encourage integration of electromagnetic brakes. Technological modernization includes fleet retrofitting programs with regenerative braking modules. Local player Weg has introduced electromagnetic braking solutions for electric buses, improving braking efficiency by 9%. Regional consumer behavior favors fleet operators prioritizing energy recovery and reduced maintenance costs.

The Middle East & Africa account for 6% of the market in 2024, with UAE and South Africa as major contributors. Demand is driven by oil & gas transportation, urban mobility initiatives, and construction vehicle electrification. Technological modernization focuses on high-performance brake modules suitable for heavy-duty applications. Local companies, such as Al Masaood, have deployed electromagnetic brakes in fleet projects, reducing brake maintenance downtime by 10%. Regional adoption reflects investment in commercial fleet efficiency and safety, with growing interest in electrified urban transport solutions.

China – 32% Market Share: Strong production capacity and integration in electric vehicles.

United States – 28% Market Share: High end-user demand and regulatory incentives driving adoption of advanced braking systems.

The automotive electromagnetic brakes market is characterised by a moderately consolidated competitive environment in which over 100 active companies participate globally, yet the top five firms together command approximately 63% of the industry’s unit shipments or revenue. Leading firms have established strong positions through strategic partnerships, product launches and targeted regional expansion. For instance, one major player secured more than €230 million in new business nominations in 2023 alone, reflecting aggressive investment in the segment. Market leaders are pursuing collaborative tie‑ups with EV OEMs, launching sensor‑enabled electromagnetic braking modules and acquiring niche players to bolster their technological edge. Innovation trends such as brake modules integrated with vehicle telematics, predictive‑maintenance capabilities and high‑torque compact actuators are reshaping competitive positioning. While smaller specialist firms compete on customisation, legacy Tier‑1s leverage scale and global reach. Competitive differentiation increasingly depends on software‑defined brake control, weight reduction per unit (up to ~10‑15%) and modular design suited for electrified platforms. For decision‑makers, the competitive landscape highlights the importance of alliances with vehicle OEMs, continuous R&D investment and global footprint — given that the top players control nearly two‑thirds of the market, yet the remaining ~37% remains open to innovation‑driven challengers.

ZF Friedrichshafen AG

Robert Bosch GmbH

Continental AG

Mayr Antriebstechnik

KEB Automation

BorgWarner Inc.

Nidec Corporation

Hitachi Automotive Systems

Hyundai Mobis Co. Ltd.

Al Masaood Group

Technological evolution in the automotive electromagnetic brakes market is moving rapidly from basic electromagnetic coil‑based actuation to sophisticated smart systems designed for electrified and autonomous vehicles. Current generation modules deliver faster response, higher torque density and reduced inertia compared with conventional hydraulic systems. Emerging technologies include permanent‑magnet eddy‑current brakes for auxiliary systems in EVs, sensor‑embedded actuators for brake‑health monitoring, and software‑defined braking modules integrated into vehicle domain controllers. For example, axial‑flux permanent‑magnet eddy‑current brake designs are being developed for lightweight motor vehicle applications, demonstrating the shift toward compact, non‑friction braking solutions. These brakes enable low‑wear, nearly contactless operation and align with electrification trends. Another technology focus is online diagnostics: brake modules now include accelerometers, temperature sensors and current monitoring to enable predictive maintenance, increasing fleet uptime by up to 20% in pilot use. Also, modular actuation architecture enables OEMs to adapt a single brake actuator across multiple vehicle platforms, reducing tooling cost by ~15%. Suppliers are investing in scalable production systems for high‑volume EV platforms and are embedding cybersecurity into brake‑control units to meet domain controller safety standards (ISO 26262 ASIL‑D). As braking systems become more software‑centric, firms that integrate mechanical, electronic and software design will secure leadership. From a strategic perspective, innovation‑led braking solutions now sit at the intersection of mobility electrification, autonomous driving and vehicle software convergence, positioning electromagnetic brakes as a key enabler of next‑gen mobility.

In October 2023, Kendrion N.V. and Miki Pulley Co., Ltd. signed a strategic agreement to introduce permanent‑magnet brake technology to the Japanese market, combining Kendrion’s high‑power‑density brake portfolio with Miki Pulley’s Japanese customer base. Source: www.kendrion.com

In November 2024, Ogura’s permanent magnetic clutch design was awarded the “Gold Award” in the LEAP (Leadership in Engineering Achievement Program) mechanical category by WTWH Media, recognising its high torque in confined space design and its energy‑saving operation in battery‑powered robotic applications. Source: www.oguraclutch.co.jp

In October 2024, Kendrion showcased two new high‑performance industrial brake models — the Servo Slim Line Type 502 and the Servo Line Type KS 02 — at the SPS 2024 trade fair in Nuremberg, emphasising compact electromagnetic brakes suitable for servo motors and lightweight robots (including mounting from both sides and diameter of only 26 mm). Source: www.kendrion.com

In Q1 2024, Kendrion announced that it would sell its Automotive business in Europe and the U.S. to Solero Technologies LLC, expected to close in Q3 2024, and would redirect product development resources to industrial, electrification and China‑automotive segments; the move is projected to generate annual cost savings of approximately EUR 8 million by January 2025. Source: www.kendrion.com

This report covers the global automotive electromagnetic brakes market across types (such as power‑off brakes, single‑face brakes, particle brakes, hysteresis power brakes and multiple‑disc brakes), applications (primary braking systems, regenerative‑braking systems, parking/auxiliary brakes, brake‑actuation modules) and end‑users (passenger vehicles, light commercial vehicles, heavy‑duty commercial vehicles, off‑road/industrial vehicles). Geographic analysis includes North America, Europe, Asia‑Pacific, South America and Middle East & Africa, detailing production capacity, consumption volumes, regional technology trends and regulatory influences. The focus extends to technology trends—including sensor integration, actuator miniaturisation, software‑defined brake systems and predictive maintenance capabilities—as well as competitive‑strategy considerations for OEMs and Tier‑1 suppliers. Niche segments such as micro‑mobility EVs, autonomous shuttles and retrofit fleet braking systems are also examined. Industry focus areas encompass material innovations (lightweight alloys, rare‑earth magnets), supply‑chain risk (raw‑material volatility), regulatory mandates (brake‑wear standards, recyclability targets) and aftermarket dynamics. By providing unit shipment data, share estimates and scenario modelling (2024 baseline), the report equips decision‑makers with actionable insights into investment priorities, technology road‑map planning and competitive benchmarks.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 821.5 Million |

| Market Revenue (2032) | USD 1,124.3 Million |

| CAGR (2025–2032) | 4.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | Asia-Pacific, North America, Europe, South America, Middle East & Africa |

| Key Players Analyzed | Kendrion N.V., Ogura Industrial Corp., Miki Pulley Co., Ltd., ZF Friedrichshafen AG, Robert Bosch GmbH, Continental AG, Mayr Antriebstechnik, KEB Automation, BorgWarner Inc., Nidec Corporation, Hitachi Automotive Systems, Hyundai Mobis Co. Ltd., Al Masaood Group |

| Customization & Pricing | Available on Request (10% Customization is Free) |