Reports

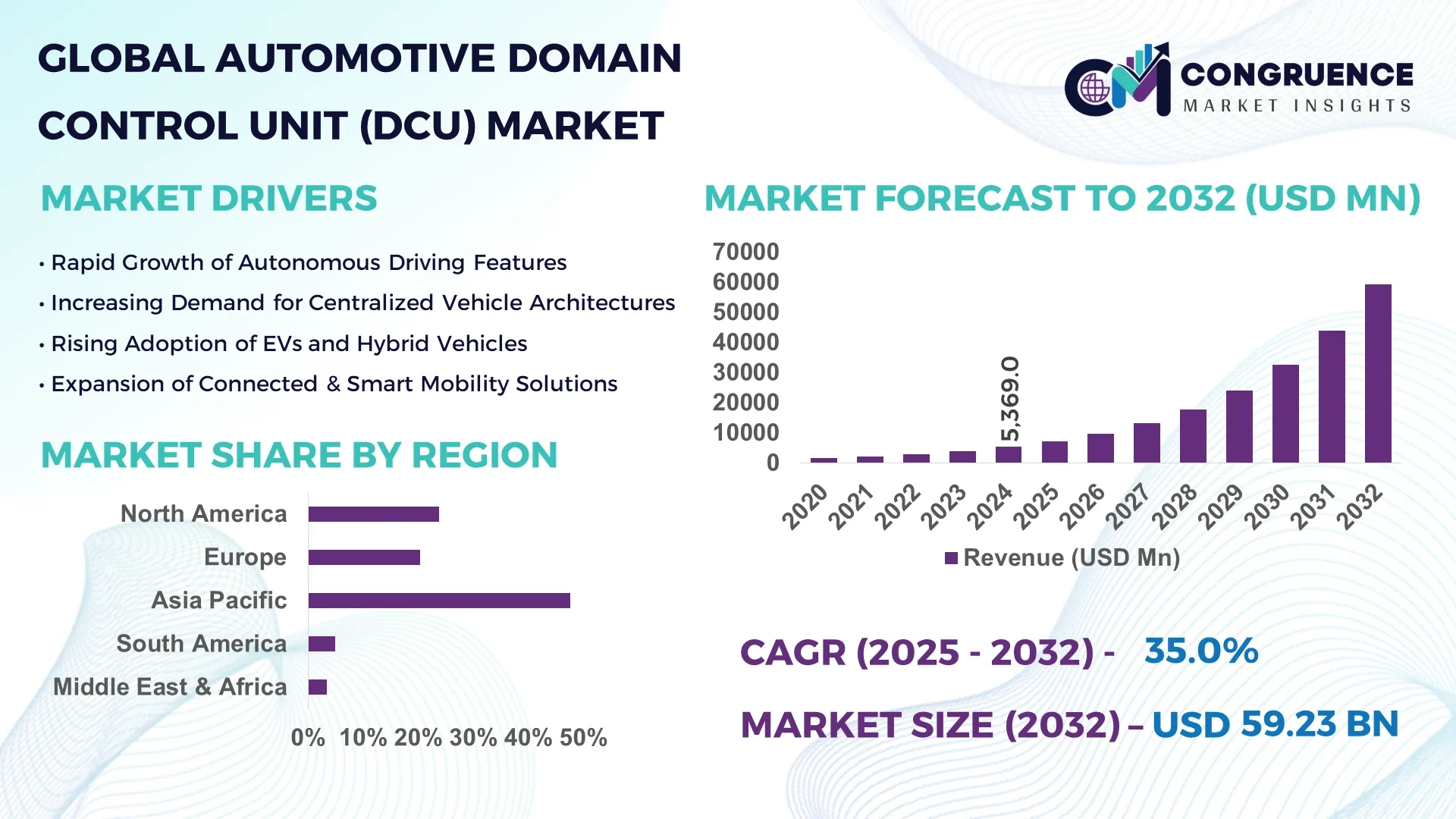

The Global Automotive Domain Control Unit (DCU) Market was valued at USD 5368.95 Million in 2024 and is anticipated to reach a value of USD 59232.42 Million by 2032 expanding at a CAGR of 35.0% between 2025 and 2032.

In China, leading production hubs maintain expansive manufacturing facilities dedicated to Domain Control Units, supporting high-volume output for major domestic automakers. Investments in DCU assembly lines focus on advanced cockpit systems, ADAS module integration, and EV-specific control units. Government-supported pilot programs validate DCU deployments in connected vehicle testbeds across urban zones. Local suppliers collaborate on safety‑critical use cases in passenger cars and commercial fleets, while cutting‑edge hardware/software integration continues in R&D centers.

The Automotive Domain Control Unit (DCU) Market encompasses major industry sectors including ADAS & autonomous driving, cockpit infotainment, body & comfort electronics, powertrain & chassis control systems, and connectivity domains. ADAS‑related DCUs account for over 40% of installed units globally, while cockpit and infotainment DCUs see rising adoption in premium vehicle segments. Recent innovations include centralised and zonal E/E architectures, sensor fusion platforms supporting multi‑modal input, over‑the‑air software update capability, edge‑compute integration for real‑time analytics, and high‑performance multicore processors with functional safety features. Regulatory drivers such as vehicle safety legislation, emissions control, and data security standards increasingly shape DCU design criteria. Economic factors like EV electrification and urban mobility deployments drive significant growth, especially in Asia‑Pacific and Europe. Emerging trends include AI‑enabled sensor fusion, software‑defined vehicle architecture, modular domain expansion, cybersecurity layering, and predictive diagnostics. The future outlook indicates sustained expansion as automakers shift to integrated intelligent architectures and scalable DCU platforms.

The Automotive Domain Control Unit (DCU) Market is undergoing a significant transformation driven by the integration of artificial intelligence. AI enables DCUs to process real‑time sensor data more efficiently, improving responsiveness in advanced driver assistance systems and autonomous driving functions. By using machine learning, DCUs can fuse inputs from radar, lidar, and camera systems, resulting in faster and more accurate decision-making during complex driving scenarios. This enhancement reduces system latency, improves safety margins, and ensures smoother vehicle control under dynamic conditions.

DCUs with AI capabilities support predictive diagnostics by continuously monitoring component health and usage patterns, helping to detect anomalies before failure occurs. This results in optimized maintenance cycles and reduced operational costs for vehicle owners and fleet operators. In cockpit environments, AI-driven personalization allows DCUs to adapt infotainment, climate, and seat configurations to user behavior and preferences, enhancing comfort and overall driving experience. Additionally, AI supports energy management systems by dynamically adjusting power distribution across components, contributing to improved electric vehicle range and efficiency.

Edge AI integration within DCUs eliminates the need for constant cloud communication, allowing for faster in-vehicle processing and increased data security. With AI models now updatable over-the-air, vehicle systems remain current and adaptive without requiring hardware changes. As the automotive industry advances toward connected and autonomous mobility, AI-powered DCUs are becoming foundational in delivering safe, intelligent, and adaptive vehicle control systems—solidifying their role as a critical component of the modern automotive ecosystem.

“In 2024, a major Tier‑1 supplier deployed AI‑based sensor‑fusion software within its domain control unit, achieving a 25 % increase in object detection accuracy and reducing processing latency from 120 ms to under 90 ms in real‑world ADAS trials.”

The Automotive Domain Control Unit (DCU) market is experiencing rapid technological evolution driven by shifts toward centralized electronic architecture, increased software content in vehicles, and integration of intelligent control modules. Demand for efficient vehicle electronic control and data processing is rising with the adoption of ADAS, infotainment systems, and electric powertrains. Automakers are transitioning from distributed ECU systems to domain-based architectures that streamline hardware usage and enhance software scalability. This evolution supports cost optimization and better system integration. Moreover, rising adoption of zonal architecture and software-defined vehicle platforms is reshaping how DCUs function within modular, upgradable systems. Market dynamics are also influenced by tightening safety and emissions regulations, increasing vehicle electrification, and escalating demand for in-vehicle connectivity. Regional developments, especially in Asia-Pacific and Europe, continue to shape the deployment rate of DCUs, while innovation in AI and edge computing accelerates the functionality of these units.

The growing adoption of ADAS is a major driver for the Automotive Domain Control Unit (DCU) market. Vehicles now rely on complex systems to interpret and respond to road conditions, requiring real-time data fusion and rapid decision-making. DCUs equipped with advanced microcontrollers and AI-based processing are essential for functionalities such as adaptive cruise control, automatic emergency braking, and lane-keeping assistance. In 2024, ADAS penetration in new vehicles exceeded 55% in developed markets, with high-end models featuring Level 2 and Level 3 automation. Domain controllers streamline signal processing from multiple sensors and reduce latency across vehicle subsystems. This shift toward centralized computing increases the efficiency and reliability of safety-critical functions. With regulatory mandates pushing for higher ADAS standardization in mass-market vehicles, OEMs are scaling DCU integration to meet compliance and consumer expectations.

One of the primary restraints in the Automotive Domain Control Unit (DCU) market is the complexity involved in integrating multiple domain-specific functions within a single hardware platform. As DCUs replace traditional ECUs, they must handle diverse tasks such as infotainment, body control, powertrain management, and ADAS—each requiring different levels of performance, safety certification, and real-time responsiveness. Harmonizing these domains under a unified software environment poses challenges related to data prioritization, cybersecurity, and thermal management. Automakers also face difficulties in sourcing compatible components and middleware that meet stringent functional safety standards like ISO 26262. In 2024, several OEMs reported delays in production timelines due to incompatibility between domain-specific applications during system testing phases. Additionally, the lack of standardized frameworks across suppliers complicates integration efforts, increasing time-to-market and system validation costs.

The shift toward software-defined vehicles (SDVs) presents significant growth opportunities for the Automotive Domain Control Unit (DCU) market. SDVs rely heavily on centralized computing to enable over-the-air updates, personalized user experiences, and dynamic feature activation. DCUs play a pivotal role in this transformation by serving as the primary control hub for zonal networks and integrated software stacks. As automakers look to extend the lifecycle of vehicle platforms through software innovations, the demand for flexible and upgradeable DCUs is increasing. By 2025, over 30% of new vehicle platforms are expected to support SDV capabilities, creating a fertile ground for domain controller deployment. DCUs with virtualization capabilities allow concurrent operation of multiple applications on a single chip, reducing hardware costs and improving software modularity. This trend is encouraging strategic collaborations between automakers and tech firms, accelerating the development of scalable DCU platforms that support continuous innovation and monetization models.

The Automotive Domain Control Unit (DCU) market faces significant challenges due to the increasing complexity of design, testing, and validation processes. With modern vehicles depending on centralized architectures, any malfunction in a DCU can have wide-ranging impacts across multiple subsystems. Ensuring fail-operational behavior, especially in safety-critical applications like braking or steering, demands exhaustive validation procedures that extend development timelines and increase engineering costs. Moreover, DCUs must comply with diverse regulatory requirements across regions, including automotive safety standards, electromagnetic compatibility, and cybersecurity guidelines. Automakers also grapple with the challenge of continuous software testing post-deployment, as over-the-air updates necessitate robust version control and rollback mechanisms. In 2024, many Tier-1 suppliers noted a sharp rise in resource allocation for hardware-in-the-loop (HIL) and software-in-the-loop (SIL) testing environments to simulate real-world driving conditions. The escalating burden of system verification and functional safety certification slows deployment cycles and increases total cost of ownership for manufacturers.

• Shift Toward Zonal Architectures in Modern Vehicle Platforms: Automakers are increasingly transitioning from traditional domain-based systems to zonal architectures, where DCUs manage data and functionality across specific vehicle zones. In 2024, over 25% of new electric vehicle platforms adopted zonal controller layouts to streamline wiring harness complexity and improve system scalability. This architecture not only reduces vehicle weight by up to 15 kg but also lowers electrical system costs while enhancing computing efficiency across functional domains.

• Integration of Edge AI in Domain Control Units: Edge computing capabilities within DCUs are now standard across many mid-to-premium segment vehicles. Edge AI allows in-vehicle data processing without dependency on external servers, enhancing real-time response for ADAS and infotainment systems. Recent designs demonstrate a 30% reduction in communication latency, improving critical decision-making and safety functionality. Automakers are prioritizing edge integration to support semi-autonomous features and real-time environmental awareness.

• Standardization of Over-the-Air (OTA) Update Capabilities: A growing number of DCUs now support OTA software and firmware updates, enabling continuous feature enhancements without physical intervention. In 2024, over 45% of newly deployed DCUs were OTA-enabled across major global markets. This trend supports lifecycle extension of vehicle electronics and offers automakers recurring revenue opportunities via feature unlocks and subscription models. It also minimizes service center visits and downtime, improving end-user satisfaction.

• Adoption of High-Performance SoCs in Centralized Controllers: DCUs are increasingly powered by high-performance system-on-chip (SoC) platforms that combine CPU, GPU, and AI accelerators for parallel processing. These SoCs support domain consolidation—combining infotainment, ADAS, and body control functions into a unified platform. Vehicles launched in 2024 equipped with such SoCs showed up to 2x improvement in frame rate processing for cockpit displays and enhanced multi-camera image stitching for surround view systems. This consolidation trend is driving efficiency, scalability, and advanced feature integration.

The Automotive Domain Control Unit (DCU) market is segmented into types, applications, and end-users, each playing a pivotal role in shaping market development and product deployment strategies. By type, centralized DCUs dominate due to their increasing use in software-defined vehicles, while zonal DCUs are emerging as a critical innovation for modular and scalable vehicle architectures. Application-wise, advanced driver assistance systems and infotainment segments contribute significantly to market volume, supported by the integration of AI and connectivity technologies. Among end-users, passenger vehicles lead in adoption due to demand for comfort and automation, but the commercial vehicle segment is rapidly expanding as fleet management systems and safety protocols become more sophisticated. These segments reflect evolving consumer expectations, regulatory influences, and OEM innovation cycles that continuously redefine the global Automotive Domain Control Unit (DCU) market.

Centralized domain control units currently lead the Automotive Domain Control Unit (DCU) market owing to their widespread deployment in modern, software-driven vehicle architectures. These DCUs serve as the core processing unit, integrating multiple vehicle functions such as powertrain, ADAS, and infotainment into a unified controller. Their rising adoption is driven by automakers’ efforts to streamline vehicle design, reduce ECU counts, and enhance feature scalability. In 2024, centralized DCUs were prominently featured in next-gen EVs across North America and Europe. The fastest-growing type is zonal DCUs, which support decentralized architecture by managing operations within specific vehicle zones. This type is gaining traction as it reduces wiring harness weight and cost, and improves modularity. Zonal DCUs are particularly favored in electric vehicles and high-end models due to their adaptability and processing efficiency. Other types include hybrid and function-specific DCUs, which remain relevant for legacy platforms and targeted applications. These units continue to support body control, lighting systems, and climate management, offering cost-effective solutions in budget segments or transitional vehicle platforms.

Advanced Driver Assistance Systems (ADAS) remain the dominant application in the Automotive Domain Control Unit (DCU) market. These systems demand high-speed data processing and multi-sensor fusion, both of which are effectively managed by modern DCUs. The increased regulatory push for mandatory safety features has led to widespread integration of domain controllers in this segment. Infotainment systems are the fastest-growing application due to the rising consumer demand for connected and immersive in-vehicle experiences. DCUs enable high-resolution display processing, voice recognition, and seamless smartphone integration. Vehicles launched in 2024 saw increased deployment of AI-driven cockpit DCUs, especially in mid and premium models. Additional applications include body electronics and powertrain control, where DCUs manage systems such as door locks, lighting, HVAC, engine control, and energy distribution. While these remain secondary in market share, their growing integration with zonal architectures and digital platforms sustains their relevance in both ICE and electric vehicle models.

Passenger vehicles are the leading end-user segment in the Automotive Domain Control Unit (DCU) market, driven by the growing consumer demand for comfort, safety, and connectivity. In 2024, more than 60% of passenger vehicle models globally were launched with at least two integrated DCUs managing cockpit and safety features. This reflects increased investments in digital cockpit platforms and regulatory pressure for ADAS deployment. The fastest-growing end-user is the commercial vehicle segment, where fleet operators are adopting DCUs to improve operational efficiency, driver safety, and predictive maintenance capabilities. Enhanced connectivity, real-time monitoring, and regulatory compliance are prompting heavy-duty OEMs to integrate scalable and updateable domain controllers. Other notable end-users include electric vehicle manufacturers and specialty vehicle producers. These segments demand high-performance computing and modular architecture, creating strong use cases for centralized and zonal DCUs. As digital transformation accelerates across vehicle categories, DCU adoption continues to expand in both volume and complexity.

China accounted for the largest market share at 41.6% in 2024 however, India is expected to register the fastest growth, expanding at a CAGR of 43.2% between 2025 and 2032.

China's leadership stems from its expansive automotive production base and robust integration of smart vehicle technologies. The country’s consistent push for electrification, coupled with local innovation in ADAS and zonal control systems, positions it as a central hub for DCU manufacturing. Meanwhile, India's automotive sector is undergoing digital acceleration, with substantial public and private investment in EV infrastructure, AI integration in vehicles, and domestic DCU assembly. Globally, the Automotive Domain Control Unit (DCU) market exhibits varied regional maturity, with Europe advancing software-defined vehicle platforms, North America emphasizing safety and autonomous capabilities, and Asia-Pacific leading in both volume and innovation. Emerging markets in South America and the Middle East & Africa are gradually increasing their adoption of DCUs, driven by infrastructure modernization and fleet digitalization. Regional policy frameworks, industry collaborations, and localization strategies are also shaping deployment patterns across automotive segments and platform architectures.

Evolving Demand for Safety-Compliant and Autonomous-Ready Vehicle Control Systems

In 2024, this region held a 23.8% share of the global Automotive Domain Control Unit (DCU) market, led by strong deployment across premium and mid-range vehicles. The presence of established automotive OEMs and Tier-1 suppliers continues to drive demand for centralized computing and AI-based safety systems. Industries such as commercial logistics, electric passenger vehicles, and autonomous mobility startups are contributing significantly to DCU utilization. Regulatory reforms around vehicle safety and data security have accelerated adoption of ADAS domain controllers, while federal funding supports testing of connected vehicle infrastructure. Technological innovations in edge computing, OTA updates, and deep learning algorithms are actively reshaping next-generation DCUs across platforms built for Level 2 and Level 3 autonomy.

Green Vehicle Transformation Accelerating Domain Control Innovation

With a 20.3% global share in 2024, the market continues to benefit from regulatory-driven innovation and high EV adoption. Germany, the UK, and France are leading countries, pushing the integration of DCUs in vehicles aligned with sustainability goals. The European Commission’s safety mandates and Euro NCAP standards have triggered significant demand for ADAS domain controllers. Additionally, CO₂ emissions regulations and digital twin R&D projects are boosting the requirement for centralized control units in electric and hybrid vehicles. DCUs in this region are increasingly embedded with features like fail-operational capabilities, thermal optimization for battery-powered platforms, and ISO-compliant safety systems.

High-Volume Production and Local Innovation Fueling Market Momentum

Asia-Pacific ranked highest in total volume shipments of Automotive Domain Control Units (DCUs) in 2024, with China, Japan, and India dominating consumption. China’s high-density EV production zones integrate zonal controllers and cockpit DCUs in almost every model released since late 2023. In India, government-supported digital mobility initiatives have enabled local manufacturing of safety-focused DCUs. Japan, known for automotive precision, focuses on high-efficiency powertrain DCUs and ADAS platforms integrated with robust cybersecurity protocols. Smart factories, autonomous testbeds, and 5G-enabled vehicle ecosystems across the region are accelerating regional DCU integration, particularly in EVs, commercial trucks, and future-ready passenger cars.

Gradual Integration of Control Units Across Electrifying Fleets

South America’s Automotive Domain Control Unit (DCU) market is gaining traction, with Brazil and Argentina leading the adoption. The region accounted for approximately 4.9% of global market volume in 2024. Brazil’s robust light-commercial vehicle sector and its push for digital fleet management are driving demand for modular and scalable DCUs. Argentina is seeing increased interest from local assemblers in cockpit and infotainment domain controllers for mid-range vehicles. Infrastructure upgrades and interest in hybrid/electric platforms are further contributing to market development. Trade partnerships and tax incentives on digital automotive imports have accelerated availability and integration of advanced DCU components.

Digitally-Driven Vehicle Systems Gaining Traction in Strategic Sectors

The Automotive Domain Control Unit (DCU) market in this region reached approximately 3.4% of global demand in 2024. UAE and South Africa are emerging as growth engines, where logistics, construction, and defense fleets are integrating domain controllers to optimize performance and reliability. Technological modernization, such as AI‑enabled diagnostics and fleet-wide OTA control, is expanding in smart city and industrial vehicle projects. Automotive OEMs in the region are collaborating with global suppliers to implement ADAS and infotainment DCUs across urban transport and utility vehicles. Trade liberalization and regional standardization policies are also facilitating the entry of advanced modular DCUs into the growing automotive aftermarket.

China – 41.6% Market Share

High production capacity, integration in electric vehicles, and rapid DCU innovation pipelines.

United States – 23.8% Market Share

Strong end-user demand in ADAS-equipped passenger and commercial vehicles, supported by safety-focused regulations.

The Automotive Domain Control Unit (DCU) market features a dynamic competitive environment with approximately two dozen prominent global players and numerous emerging technology firms. Established Tier‑1 suppliers and semiconductor specialists dominate primary market positioning, offering end‑to‑end domain architecture solutions across ADAS, cockpit, and powertrain domains. Leading companies are engaged in strategic partnerships with automakers and technology providers to co-develop high-performance domain controller platforms and modular SoC fabrics tailored for next‑generation vehicle platforms.

Recent product launches include integrated domain control modules combining AI accelerators, zonal networking support, and OTA firmware upgrade capabilities. Competitive differentiation hinges on silicon performance, safety certification compliance, software ecosystems, and scalability across vehicle segments. Several firms have entered joint ventures or collaborations focused on edge AI integration, cybersecurity features, and multi-modal sensor fusion. Innovation trends center on virtualization support, digital cockpit convergence, and high-speed Ethernet networking within zonal architectures.

Market positioning varies: established suppliers maintain broad OEM relationships and global delivery infrastructure, while niche players offer specialized solutions in cockpit computing or sensor-fusion DCUs. Emerging competitors from semiconductor startups are gaining traction with lightweight, energy-efficient platforms optimized for electric vehicles. Competitive intensity is further heightened by supplier consolidation, strategic mergers, and alliances aimed at cohesion across electric vehicle platforms, autonomous mobility projects, and global safety compliance demands. This competitive landscape underscores a rapidly evolving domain controller ecosystem where speed of innovation, platform flexibility, and strategic collaboration determine market leadership.

Bosch

Continental AG

Magna International

Denso

Aptiv

NXP Semiconductors

Infineon Technologies

Qualcomm

ZF Friedrichshafen

Valeo

The Automotive Domain Control Unit (DCU) market is undergoing a transformative shift driven by the rise of software-defined vehicles, high-performance computing, and zonal architectures. DCUs are increasingly central to vehicle electronics, consolidating control over multiple sub-systems including ADAS, infotainment, body control, and powertrain domains. Advanced System-on-Chip (SoC) platforms with embedded AI accelerators, functional safety compliance (ISO 26262), and real-time processing capabilities are redefining DCU architecture.

Modern DCUs integrate multiple sensors and actuators through high-bandwidth interfaces such as automotive Ethernet and CAN FD, enabling low-latency, deterministic communication across in-vehicle networks. Technologies like hardware virtualization and domain isolation are now standard in high-end DCUs to support concurrent applications and ensure fail-operational behavior. Flash-over-the-air (FOTA) and software-over-the-air (SOTA) update functionalities are also embedded, allowing OEMs to upgrade or patch software remotely, improving safety and user experience.

The transition from centralized to zonal architectures is prompting the development of scalable DCUs that consolidate multiple ECUs within each vehicle zone. These zonal controllers often rely on standardized software platforms such as AUTOSAR Adaptive and support real-time operating systems (RTOS) with deterministic execution. Thermal management innovations and power-efficient processing have become critical, particularly for EVs and autonomous platforms. Additionally, cybersecurity features such as secure boot, intrusion detection, and encrypted communication are integral to DCU designs, ensuring compliance with global regulations such as UNECE WP.29. Overall, DCUs are enabling the evolution of vehicles into software-centric, connected mobility platforms.

• In April 2024, Aptiv announced the launch of a new scalable ADAS domain controller capable of supporting Level 2+ and Level 3 autonomy, integrating high-performance computing and centralized sensor fusion across radar, LiDAR, and camera systems.

• In November 2023, Continental introduced its Smart Cockpit High-Performance Computer (HPC), a domain controller combining infotainment, cluster, and driver assistance processing into a single unit to reduce wiring complexity and enhance data synchronization.

• In February 2024, NXP Semiconductors unveiled its next-generation S32N family of processors designed specifically for zonal DCU platforms, offering real-time processing, multi-core architecture, and ISO 26262 ASIL-D functional safety compliance.

• In August 2023, Bosch announced a partnership with a leading Chinese OEM to develop a custom domain controller for EV platforms, integrating battery management, e-motor control, and telematics within a single modular unit.

The Automotive Domain Control Unit (DCU) Market Report encompasses a comprehensive analysis of domain controller adoption across major vehicle architectures, including ICE vehicles, hybrids, and battery electric vehicles (BEVs). The report evaluates the market across functional domains such as ADAS, powertrain, chassis, infotainment, and body electronics. It highlights technological transitions from traditional distributed ECU systems to centralized and zonal control architectures, reflecting the industry's evolution toward software-defined vehicles and connected mobility ecosystems.

The report offers granular segmentation by hardware types (microcontrollers, SoCs, memory modules), software platforms (AUTOSAR Classic, Adaptive AUTOSAR, RTOS), vehicle types (passenger cars, LCVs, HCVs), and integration levels (single-domain, multi-domain, zonal). It also investigates deployment trends in mid-range and premium vehicle segments, emphasizing how domain controllers are tailored for each segment's compute and functional safety needs.

Geographically, the report provides detailed insights into North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with focused coverage on regional OEM adoption rates, regulatory frameworks, and R&D activity. It explores industry-specific use cases such as over-the-air (OTA) update enablement, vehicle-to-everything (V2X) communication integration, and centralized cybersecurity management. Emerging segments including domain control for autonomous shuttles, last-mile delivery vehicles, and software-defined commercial fleets are also analyzed to provide a holistic market perspective.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5368.95 Million |

|

Market Revenue in 2032 |

USD 59232.42 Million |

|

CAGR (2025 - 2032) |

35% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bosch, Continental AG, Magna International, Denso, Aptiv, NXP Semiconductors, Infineon Technologies, Qualcomm, ZF Friedrichshafen, Valeo |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |