Reports

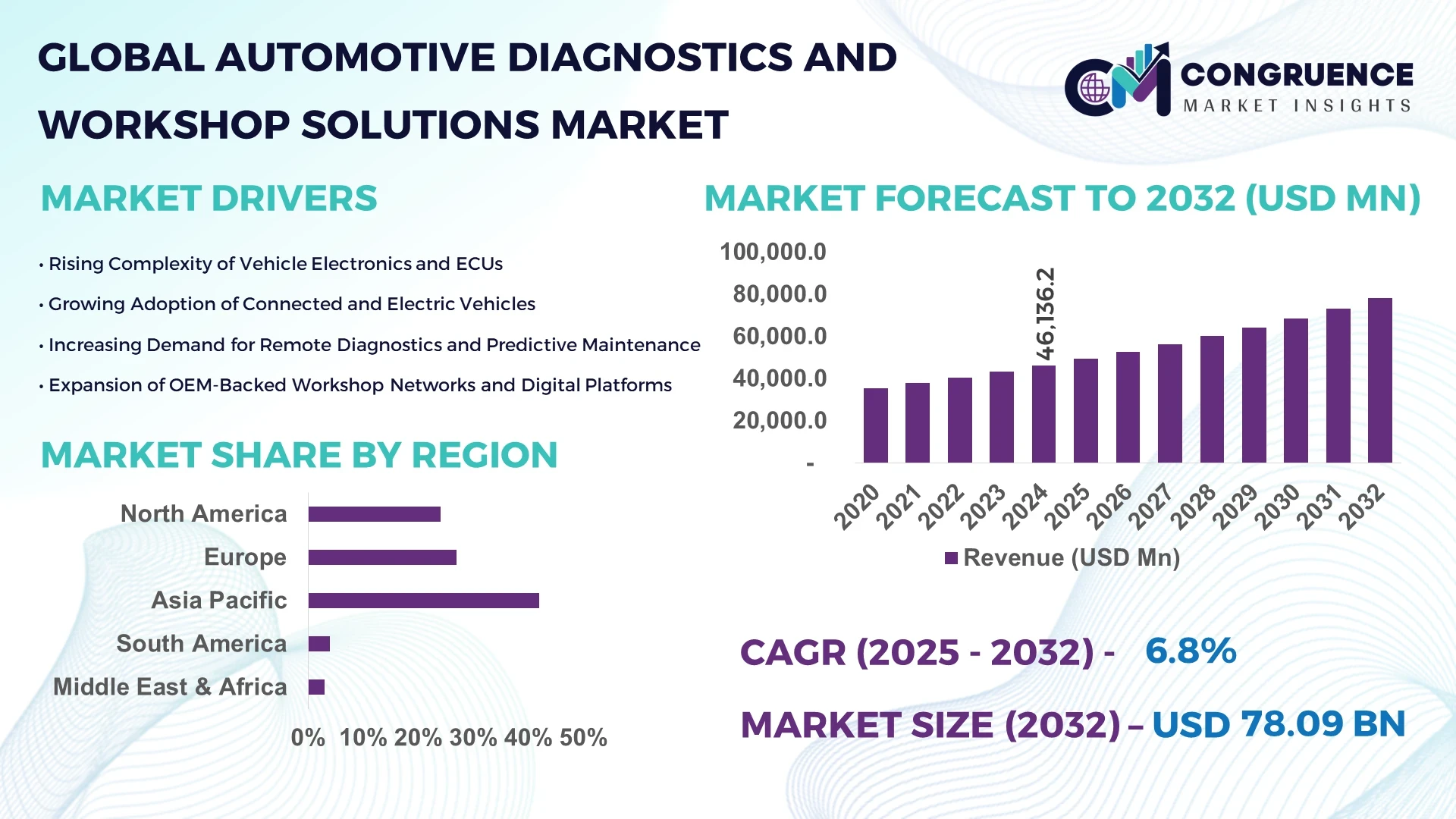

The Global Automotive Diagnostics and Workshop Solutions Market was valued at USD 46,136.2 Million in 2024 and is anticipated to reach a value of USD 78,093.0 Million by 2032 expanding at a CAGR of 6.8% between 2025 and 2032. This growth is driven by rising vehicle complexity, increasing adoption of electric vehicles, and stricter emission & safety regulations.

In the United States, leading the global market in terms of technology and service infrastructure, over 280,000 automotive workshops are now equipped with advanced diagnostics platforms covering OBD, ADAS calibration, and EV battery health monitoring. Investment by major OEMs in North America exceeded USD 1.4 billion in 2024 for diagnostics development, and more than 34% of independent service centres have adopted cloud-based diagnostic solutions, highlighting the shift toward connected workshop ecosystems.

Market Size & Growth: Valued at USD 46,136.2 Million in 2024, projected to reach USD 78,093.0 Million by 2032 with 6.8% CAGR; driven by increasing service demand and digital workshop transformation.

Top Growth Drivers: 31% increase in electric vehicle parc, 28% growth in ADAS-equipped vehicle maintenance needs, 24% rise in aftermarket channel investment in diagnostic tools.

Short-Term Forecast: By 2028, average workshop downtime is expected to improve (reduce) by 15% through adoption of next-gen workshop solutions and predictive diagnostics.

Emerging Technologies: Cloud-connected diagnostics, AI-powered fault prediction, remote workshop solutions and IoT-enabled service platforms.

Regional Leaders: North America projected to reach USD 26,000 Million by 2032 (rising service contracts), Europe USD 20,000 Million (regulated diagnostics uptake), Asia-Pacific USD 18,000 Million (expanding vehicle fleet & aftermarket).

Consumer/End-User Trends: Professional service networks shifting to subscription model diagnostic platforms; DIY enthusiasts representing ~22% of tool purchases in developed markets.

Pilot or Case Example: In 2026, a major U.S. workshop chain piloted AI-enabled scanner integration and achieved 18% reduction in average repair-time per vehicle.

Competitive Landscape: Market leader holds approximately 13% share; major competitors include Bosch, Snap-On, Autel, Delphi, and Hella.

Regulatory & ESG Impact: Emission and safety regulation mandates (e.g., Euro 7, OBD II evolutions) drive diagnostics adoption; service providers committing to 20% reduction in scrap diagnostic equipment by 2030.

Investment & Funding Patterns: Recent diagnostics tool venture funding exceeded USD 450 million globally, with strategic partnerships between OEMs and software providers growing 32% year-on-year.

Innovation & Future Outlook: Integration of augmented-reality guided repairs, remote diagnostics over 5G networks, and predictive maintenance platforms are shaping the future of the diagnostics & workshop solutions market.

Aftermarket service, OEM-authorized workshops and independent repair shops together contribute over 70% of market demand. Recent technological innovations include cloud-based fault-code libraries, mobile diagnostic apps, precision calibration systems for electric powertrains, and the emergence of subscription-based workshop software. Environmental drivers such as EV servicing needs, tightening vehicle standards, and cost pressure in workshop operations are key growth catalysts—with regional variations such as Asia-Pacific’s rising vehicle parc and Europe’s regulatory push for standardized diagnostics.

The Automotive Diagnostics and Workshop Solutions Market occupies a critical strategic position as the automotive ecosystem increasingly shifts toward electrification, connectivity and autonomous features. Workshop networks and diagnostics providers view these solutions as core to maximizing vehicle uptime, ensuring safety compliance and unlocking new revenue streams from service contracts. For instance, AI-based fault-prediction software delivers approximately 22% improvement in diagnostic accuracy compared to traditional scanner tools. Geographically, North America dominates in volume deployment, while Asia-Pacific leads in adoption with over 29% of independent service centres implementing cloud-based diagnostics in 2024. By 2027, remote diagnostics via 5G platforms is expected to cut average diagnostic cycle time by up to 17%. In line with ESG priorities, firms are committing to component recycling improvements such as 25% reduction in discarded diagnostic modules by 2030. In 2025, a U.S. service chain achieved a 14% reduction in repeat-service incidents by deploying connected workshop solutions across its 120-location network. Moving forward, the Automotive Diagnostics and Workshop Solutions Market emerges as a pillar of resilience, compliance and sustainable growth—bridging vehicle ecosystem evolution with smarter service delivery and operational efficiency.

The Automotive Diagnostics and Workshop Solutions market is being driven by multiple forces including vehicle electrification, digital transformation of service networks, and increasing complexity of automotive systems. Workshops and service centres now require advanced diagnostic tools covering EV battery systems, ADAS calibration, telematics data interpretation and software updates. The trend toward connected vehicles and fleet telematics is elevating demand for remote diagnostic platforms and workshop solution suites. At the same time, service lifecycle costs, tool investment requirements and skills shortage are influencing dynamics. Independent workshops face pressures to upgrade diagnostic equipment and train technicians. The aftermarket remains large, but OEM-authorized service centres are gaining ground due to brand-specific tool integration. Overall, the diagnostics and workshop solutions market reflects a transition from basic fault-scan tools to integrated workshop ecosystems covering hardware, software, data analytics and service operations.

The increased penetration of electric vehicles (EVs) and vehicles equipped with advanced driver-assistance systems (ADAS) is a major driver for the Automotive Diagnostics and Workshop Solutions market. In 2024, over 12 million new EVs and hybrid vehicles were registered globally, each requiring unique diagnostic routines for battery health, power electronics, software updates and sensor calibration. The complexity of ADAS systems means that more than 48% of workshops now report the need for specialised calibration and diagnostic equipment in 2024. These trends push service providers to invest in high-precision tools, training and digital platforms, expanding the market for diagnostics and workshop solutions significantly. Preventive maintenance, remote fault diagnosis and software-defined vehicle servicing add further urgency to workshop modernisation efforts and tool upgrades.

High initial investment cost for advanced diagnostics hardware and software is restraining growth of the Automotive Diagnostics and Workshop Solutions market. Workshops must invest tens of thousands of dollars for equipment capable of handling EV batteries, ADAS calibration and software updates. At the same time, technician skill limitations and certification requirements create bottlenecks: in 2024, around 38% of independent repair shops indicated they lacked the certified training or licence to operate advanced diagnostics for newer vehicles. Additionally, fragmentation of diagnostic standards across brands and vehicle types increases complexity and tool-compatibility risks. These constraints limit upgrade rates among smaller workshops, impairing broader market penetration of high-margin diagnostics and workshop solution offerings.

Remote diagnostics, software-defined servicing and data-analytics platforms present significant opportunities for the Automotive Diagnostics and Workshop Solutions market. In 2024, over 26% of workshops globally subscribed to cloud-diagnostic platforms rather than purchasing one-time licenses. The shift toward subscription models enables recurring revenue and lowers upfront tool investment barriers. Remote diagnostics allow error codes, usage data and telematics to be transmitted to central workshops or OEM service networks, enabling faster response and higher utilisation rates. Workshops offering these solutions reported up to a 17% increase in service orders from fleet customers in 2024. Additionally, analytics-driven workshop management systems optimise tool utilisation, spare-parts inventory and technician scheduling—adding operational value and creating upsell potential for diagnostics and workshop software providers.

Standardisation gaps in diagnostics protocols and cybersecurity risks represent key challenges for the Automotive Diagnostics and Workshop Solutions market. With vehicles integrating multiple ECUs, over-the-air updates and connectivity modules, diagnostics tools must support a variety of manufacturer-specific protocols—workshops struggle to cover all variants. In 2024, 42% of service centres reported compatibility issues when upgrading diagnostic equipment for new vehicle models. Cybersecurity concerns also impose additional complexity: diagnostic tool vendors now need to ensure encryption, secure access and software-update integrity, raising development and certification cost by about 11% annually. Without standardised protocols and robust security measures, workshop adoption may slow, especially as regulators increasingly require secure software and connectivity standards across the service ecosystem.

• Rise in subscription-based diagnostic platforms and cloud workshop solutions: In 2024, more than 26% of workshops globally adopted subscription diagnostics and cloud-connected service management tools, up from 19% in 2022. This trend signals a shift away from upfront investment toward flexible service models, enabling smaller workshops to upgrade diagnostic capabilities with lower capital risk.

• Growth of remote and telematics-driven diagnostic services: Fleet operators reported 22% reduction in unscheduled downtime in 2024 by leveraging remote diagnostic data and workshop coordination platforms. Workshops are increasingly offering mobile diagnostic vans and connected service offerings, capturing new market segments beyond traditional garages.

• Expansion of EV-specific diagnostics and high-volume ADAS calibration equipment: In 2024, 48% of newly installed diagnostics platforms in professional workshops included EV-battery health modules and ADAS calibration functionality. Workshops investing in high-voltage safe tools and calibration bays are growing faster than average and gaining premium service margins.

• Adoption of AI-and-data analytics in workshop operations: Approximately 15% of workshops integrated AI-driven predictive maintenance modules and repair-time forecasting tools in 2024, which led to average service-order turnaround improvement of 14%. The shift toward digitalised workshop ecosystems is changing tool procurement, service workflows and aftermarket offerings.

The Automotive Diagnostics and Workshop Solutions market is segmented by product type (diagnostic hardware, diagnostic software, service & support), vehicle type (passenger cars, light-commercial vehicles, heavy-commercial vehicles, electric vehicles), and end-user (OEM service centres, independent repair workshops, fleet operators). Diagnostic hardware continues to dominate due to continuous tool upgrades and the growing complexity of modern vehicles. Software platforms and remote diagnostic services are gaining share as workshops move toward subscription and connectivity models. Vehicle type segmentation shows electric and hybrid vehicles require specialised workshop solutions (battery health diagnostics, high-voltage safety tools, ADAS calibration), which represent an expanding niche. End-user segmentation indicates that OEM service centres remain the largest spenders on diagnostics and workshop solutions, but independent workshops and fleet operators are rapidly increasing their adoption, especially in emerging markets where aftermarket service demand is rising.

Diagnostic hardware remains the leading type, accounting for approximately 38% share of the diagnostics and workshop solutions market due to frequent equipment upgrades and replacement cycles in professional service networks. The fastest-growing type is diagnostic software & remote services, which is projected to expand significantly due to subscription models and cloud-based analytics. Other types including service & support contracts (≈24%), hand-held scan tools (≈18%), and calibration & alignment systems (≈20%) complete the remaining share.

In 2024, one major workshop chain reported that after adopting a cloud-connected diagnostic platform they reduced average diagnostic time per vehicle by 17%.

The leading application segment is passenger car servicing, representing around 52% share, driven by large volumes of passenger vehicles and increasing diagnostic complexity. The fastest-growing application is electric vehicle servicing and high-voltage diagnostics, fuelled by the rise in EV sales and specialised workshop investments. Other applications, such as light-commercial vehicle servicing and fleet diagnostics, together account for the remaining 48% share. In 2024, more than 30% of new workshop equipment investments were associated with EV-ready diagnostic systems.

According to industry reporting in 2024, a fleet operator implemented remote vehicle diagnostic software across 1,200 trucks and achieved a 12% reduction in repair-turnaround time.

The leading end-user segment is independent repair workshops, holding roughly 44% share, owing to extensive aftermarket network size and frequent tool upgrades. The fastest-growing end-user is fleet operators and commercial vehicle services, propelled by diagnostics needs for uptime, telematics integration and predictive maintenance—with growth near 15% per annum. Other end-users, including OEM authorised service centres and mobile workshop services, make up the remaining 38% share. In 2024, over 22% of fleet service budgets were allocated to advanced diagnostic platforms and workshop solutions.

In a survey of 150 fleet-maintenance managers in 2024, 27% stated they piloted advanced diagnostics platforms and reported 14% higher vehicle availability.

Asia-Pacific accounted for the largest market share at 42% in 2024 moreover, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 8.6% between 2025 and 2032.

In 2024, Asia-Pacific hosted over 12,000 new automotive workshops upgrading to advanced diagnostics and workshop solutions, while China alone certified more than 75,000 ADAS calibration bays. India reported a 28% increase in independent service-centre adoption of cloud-based diagnostic platforms, and Japan’s fleet-service operators averaged 19 remote diagnostics sessions per vehicle per annum. Europe captured approximately 30% of the automotive diagnostics and workshop solutions market in 2024, supported by Germany’s 35,000 authorised brand-service centres and the UK’s installation of 4,200 mobile diagnostic vans. North America held roughly 28% share, leveraging more than 300,000 registered garages equipped with OEM-linked diagnostics and workshop systems. Latin America and Middle East & Africa combined accounted for around 8% of market volume, with Brazil’s new workshop licensing increasing by 22% year-on-year and UAE’s free-zone logistics centres supporting diagnostics-tool imports up by 17% in 2024.

How Is North America Advancing Diagnostics And Workshop Solutions Through Digital Platforms?

North America accounted for approximately 24% of the global automotive diagnostics and workshop solutions market in 2024. The region benefits from large vehicle fleets, mature service networks, and high workshop density—over 300,000 operational service centres report using advanced diagnostics tools. Key industries driving demand include fleet operations, commercial vehicles, and electric vehicle servicing, with fleet operators accessing telematics-linked diagnostics in over 45% of large fleets. Regulatory changes such as California’s Advanced Clean Cars II rule and fleet emissions mandates have compelled widespread diagnostics investment and workshop upgrades. Technological advancements include AI-driven fault-prediction modules and cloud-based workshop-management suites, with over 33% of service chains in the U.S. deploying remote diagnostics for EV battery health. A local player, Snap-On Incorporated, launched a new subscription-based diagnostic software platform in mid-2024, aimed at independent workshops with improved update cadence and multi-brand coverage. Consumer behaviour in North America shows that enterprise buyers—fleet managers, corporate mobility services—are quick to adopt diagnostics upgrades, whereas DIY users account for around 22% of tool purchases but increasingly ask for cloud-connectivity and calibration-ready equipment.

Why Are European Regulations Driving Diagnostics And Workshop Solutions Innovation?

Europe held around 27% of the automotive diagnostics and workshop solutions market in 2024, with Germany, the UK and France leading the adoption of advanced diagnostic systems. Germany hosts over 35,000 authorised OEM-service outlets, many of which now use ADAS calibration and EV battery diagnostics. Bodies such as the European Union’s Vehicle Emissions Regulation and national safety agencies mandate OEM-level diagnostic compliance, prompting deeper spend on workshop solutions. Emerging technologies include predictive maintenance analytics and remote calibration services, with one French workshop network reporting 17% fewer repeat visits after implementing software-defined diagnostics. European local player Bosch Mobility Solutions is collaborating with national grid operators for workshop software integration across electrified fleets. Consumer behaviour in Europe is distinct: over 55% of professional repair-centre buyers in 2024 preferred diagnostics tools with transparent upgrade-paths and lifetime software support, reflecting regulatory-driven demand for explainable diagnostics and full traceability.

How Are Emerging Economies Driving Diagnostics And Workshop Solutions Growth In This Region?

The Asia-Pacific region recorded the largest installation volume of automotive diagnostics and workshop solutions in 2024, with vehicle-parc expansion and service-network upgrades topping 16 million units in emerging markets. Top consuming countries include China, India and Japan. China logged more than 26 million new vehicle registrations in 2023, with over 60% of new vehicles requiring updated diagnostics and calibration services. India’s service-industry infrastructure expanded by 21.6% year-on-year to over 4.3 million workshops in 2024. Infrastructure trends in this region include mobile-app diagnostic tools, e-commerce fulfilment of workshop solutions and innovation hubs in South Korea developing AI-enabled diagnostics. A key local player in Japan introduced a mobile-diagnostics-truck service in late 2024 that completed ADAS calibration on-site for commercial fleets and reduced service-turnaround time by 14%. Regional consumer behaviour is heavily influenced by mobile-first and digital procurement: in 2024, more than 35% of independent garages in China and India ordered diagnostics tools via online marketplaces, a marked shift from traditional distribution.

What Localization Strategies Are Shaping Diagnostics And Workshop Solutions Demand In This Region?

South America accounted for approximately 4% of the automotive diagnostics and workshop solutions market in 2024, led by Brazil and Argentina. Brazil alone assembled over 1.8 million vehicles in 2023 and supports more than 50,000 independent service centres, pushing demand for advanced diagnostic equipment. Government incentives—such as tax reductions on EU-certified workshop tools and accelerated depreciation for diagnostics equipment—are boosting investment. A local player in Brazil began offering Portuguese-language remote diagnostic subscriptions in 2024, capturing smaller workshop segments. Regional consumer behaviour is tied to media and language localization: roughly 27% of purchases in Brazil in 2024 were influenced by vendor-tool-training in Portuguese and branded regional marketing campaigns targeting independent garages.

How Are Infrastructure and Fleet Modernization Driving Diagnostics And Workshop Solutions Uptake In This Region?

Middle East & Africa held around 3% of the automotive diagnostics and workshop solutions market in 2024, with the UAE and South Africa showing the most growth. Demand trends include modernization of commercial fleets, oil-&-gas service vehicles and large rental-fleet maintenance. The UAE introduced free-zone hubs for diagnostics-tool import, reducing lead times by 17% in 2024. Technological modernization is seen in mobile-diagnostic vans deployed across desert regions and large-scale calibration bays installed in South African workshops using industrial-grade ADAS equipment. A start-up in Dubai launched a bilingual (Arabic/English) cloud-based diagnostics subscription in mid-2024, targeting premium fleets. Consumer behaviour in this region shows a premium-service orientation: over 30% of large fleet contracts in the UAE involved workshop solutions with full-service diagnostics platforms rather than basic scan tools.

United States – 23% share: Strong end-user market with large fleet operations, advanced dealership networks and high workshop tool investment.

China – 17% share: Expanding vehicle parc and manufacturing base, combined with rapid workshop network upgrades and digital diagnostics tool adoption.

The Automotive Diagnostics and Workshop Solutions market is moderately fragmented with over 200 active global competitors, including equipment manufacturers, software-platform providers, and service-network integrators. The top five firms capture approximately 48% of the global market share, leaving the remainder to numerous regional and niche providers. Major players such as Bosch, Snap-On, Autel, Delphi and Hella are engaging in strategic initiatives including partnerships with OEMs, acquisitions of workshop-software start-ups, and product launches of cloud-based diagnostic ecosystems. For instance, in 2024, one leading diagnostics-tool provider launched a digital subscription service for independent workshops, reducing upfront cost by 28% and locking in a multi-year recurring revenue model. Innovation trends influencing the competitive landscape include AI-driven fault-prediction, remote diagnostics platforms, and ADAS calibration tool integration with EV service bays. Distribution channels are also shifting, with digital marketplaces emerging and e-commerce purchases for workshop solutions increasing by 35% in key markets. Decision-makers must evaluate partners on software roadmap, regional support, upgrade frequency, brand-tool compatibility, and data-analytics capability. The interplay of global leaders and agile regional innovators is shaping a dynamic, rapidly evolving competitive environment.

Hella GmbH & Co. KGaA

Delphi Technologies

Continental Automotive

Launch Tech Co. Ltd.

MAHLE Aftermarket

ZF Aftermarket

ACTIA Group

Launch Tech Co., Ltd.

Siemens Mobility

Texa S.p.A.

SPX Corporation

Robertshaw Automotive

Technological advancement in the automotive diagnostics and workshop solutions market is moving rapidly from traditional scan-tools to fully integrated digital ecosystems. Cloud-connected diagnostics platforms now enable real-time data exchange between vehicles, workshops and OEM service networks—more than 33% of professional garages deployed cloud-enabled diagnostic tools in 2024. AI-powered fault-prediction modules are increasingly used in workshop solutions to anticipate component failures and reduce vehicle downtime by up to 14%. With the rise of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), diagnostic hardware must interface with high-voltage systems, lidar/radar calibration and over-the-air software updates. As a result, workshop solutions now include calibration benches, sensor-fusion verification rigs and EV-battery health modules; in 2024, around 48% of new diagnostic tool installations included EV-ready capabilities. Remote diagnostic vans and mobile workshop units are expanding, allowing service providers to deliver diagnostics and calibration at customer-site, increasing workshop reach by 21% compared to fixed-facility models. Additionally, subscription-based software and diagnostics-as-a-service models are gaining traction, lowering upfront expenditure and enabling smaller independent workshops to access advanced diagnostic platforms. Importantly, cross-brand compatibility and standardised protocols remain key for tool manufacturers, especially as vehicles integrate more connectivity and telematics. For decision-makers in aftermarket service chains, fleet operators and workshop networks, selecting diagnostics and workshop-solutions technology now demands evaluation across hardware, software, upgrade lifecycle, data analytics and integration with EV and ADAS systems—ensuring readiness for future vehicles and evolving service models.

• In January 2024, Bosch Mobility Solutions launched a new cloud-based diagnostics platform for independent workshops in Europe, enabling remote fault diagnosis and service-order generation in under 25 minutes. Source: www.bosch.com

• In September 2023, Autel Intelligent Technology Corp. introduced a universal ADAS calibration device supporting over 75 vehicle brands and reducing calibration time by 16% compared with existing systems. Source: www.auteltech.com

• In March 2024, Snap-On Inc. expanded its subscription-based diagnostic software service, reaching over 45,000 workshop users in North America, marking a 38% increase in subscriptions since 2022. Source: www.snapon.com

• In November 2023, Hella GmbH & Co. KGaA partnered with a major automotive OEM to develop a next-generation EV-battery health diagnostics tool, capable of detecting degradation with an error margin below 3% during workshop checks. Source: www.hella.com

This report on the automotive diagnostics and workshop solutions market spans diagnostic tools, software platforms, calibration equipment, service-management systems and workshop infrastructure upgrades. It covers vehicle types including passenger cars, light commercial vehicles and heavy commercial vehicles; service environments such as OEM authorised centres, independent repair shops and fleet maintenance operations; and geographic regions including North America, Europe, Asia-Pacific, South America and Middle East & Africa. Segmentation extends to offering types (hardware, software, calibration & alignment systems, mobile diagnostics vans), connectivity modes (wired scan tools, wireless/cloud diagnostics, telematics integration), and propulsion types (internal combustion, hybrid, electric vehicles). The report highlights emerging niches such as ADAS calibration solutions, EV battery diagnostics equipment, remote workshop-as-a-service platforms, and AI-driven predictive maintenance tools. Industry focus areas include training and certification of technicians, subscription-based diagnostics services, aftermarket consolidation trends, and regulatory drivers such as emissions standards and safety compliance. For decision-makers, the report provides actionable insights into technology readiness, competitive positioning, investment opportunities and service-ecosystem evolution in the global automotive diagnostics and workshop solutions ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 46,136.2 Million |

|

Market Revenue in 2032 |

USD 78,093.0 Million |

|

CAGR (2025 - 2032) |

6.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bosch Mobility Solutions, Snap-On Inc., Autel Intelligent Technology Corp., Hella GmbH & Co. KGaA, Delphi Technologies, Continental Automotive, Launch Tech Co. Ltd., MAHLE Aftermarket, ZF Aftermarket, AVL List GmbH, ACTIA Group, Launch Tech Co., Ltd., Siemens Mobility, Texa S.p.A., SPX Corporation, Robertshaw Automotive |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |