Reports

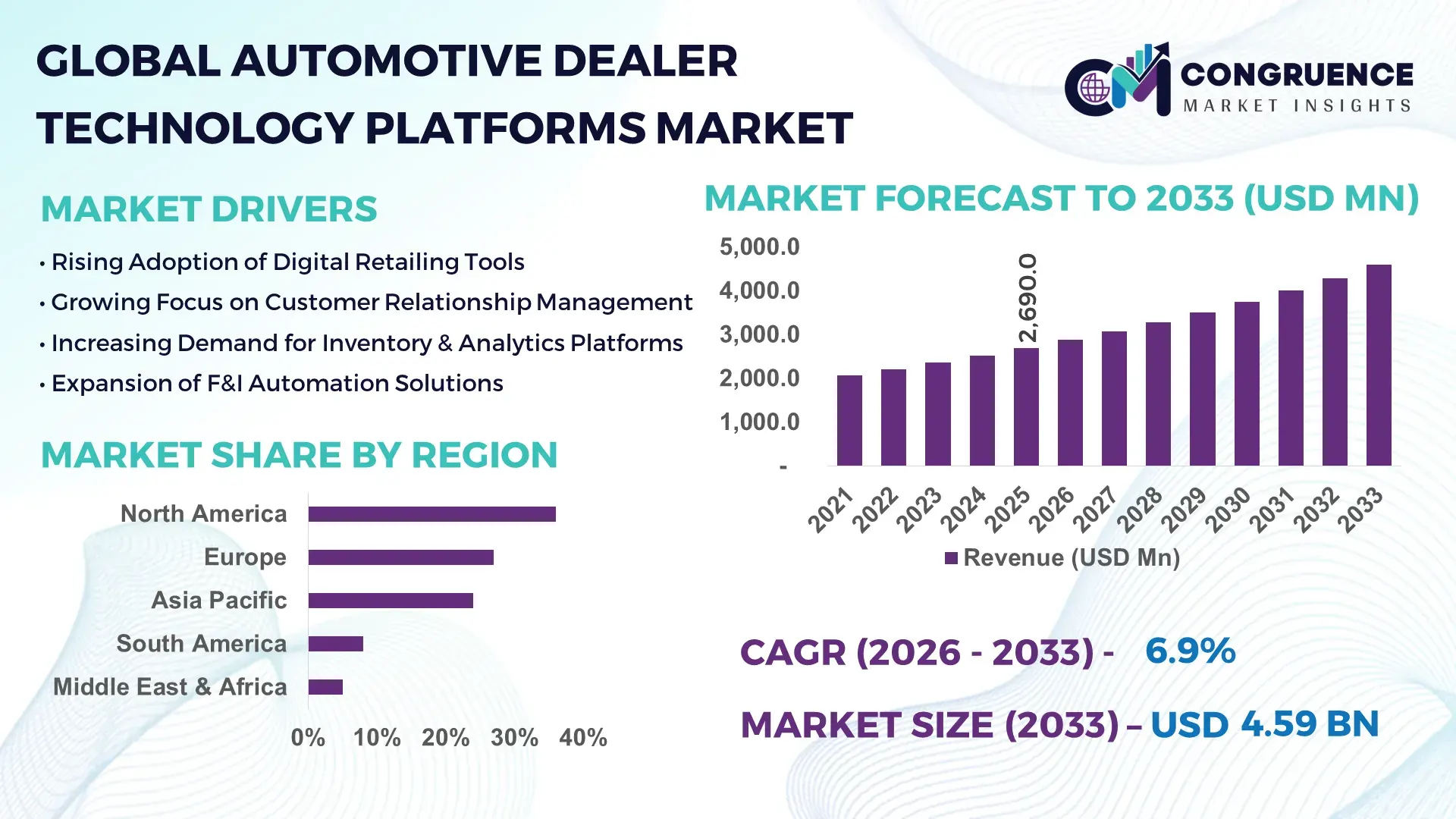

The Global Automotive Dealer Technology Platforms Market was valued at USD 2,690 Million in 2025 and is anticipated to reach a value of USD 4,587.5 Million by 2033 expanding at a CAGR of 6.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market growth is primarily driven by rapid digital transformation across automotive retail networks, increasing integration of AI-powered dealership management systems (DMS), and the shift toward omnichannel vehicle sales and aftersales service models.

The United States represents the dominant country in the Automotive Dealer Technology Platforms Market, supported by over 18,000 franchised dealerships and more than 40,000 independent dealers operating nationwide. Over 72% of U.S. dealerships utilize cloud-based Dealer Management Systems, while approximately 65% have integrated CRM and digital retailing modules into their sales workflows. Annual IT spending per large dealership group exceeds USD 250,000, with leading dealer groups investing heavily in AI-based inventory analytics, predictive maintenance tools, and online financing platforms. More than 60% of new vehicle buyers in the U.S. initiate purchases online, accelerating demand for end-to-end digital retailing platforms, automated F&I tools, and integrated compliance management systems.

Market Size & Growth: Valued at USD 2,690 Million in 2025 and projected to reach USD 4,587.5 Million by 2033, expanding at 6.9% CAGR, driven by digital retail adoption and AI-enabled dealership automation.

Top Growth Drivers: 72% cloud DMS adoption rate, 65% CRM integration across dealer groups, 60% online vehicle purchase initiation.

Short-Term Forecast: By 2028, AI-driven pricing and inventory tools are expected to improve dealership inventory turnover efficiency by 18% and reduce holding costs by 12%.

Emerging Technologies: AI-powered predictive analytics, blockchain-based vehicle history management, and API-driven omnichannel retail integration platforms.

Regional Leaders: North America projected to exceed USD 1,850 Million by 2033 with high SaaS penetration; Europe to surpass USD 1,200 Million driven by regulatory compliance systems; Asia-Pacific to cross USD 1,050 Million supported by digital showroom expansion.

Consumer/End-User Trends: Multi-location dealer groups representing over 55% of platform deployments, with 60% of buyers preferring hybrid online-offline purchase journeys.

Pilot or Case Example: In 2024, a U.S. dealer group implemented AI-driven lead scoring, increasing qualified lead conversion rates by 22% within 12 months.

Competitive Landscape: CDK Global holds approximately 28% share, followed by Reynolds and Reynolds, Cox Automotive, Dealertrack, and SAP Automotive Solutions.

Regulatory & ESG Impact: Digital documentation reduces paper use by up to 40%, while data privacy regulations require 100% encrypted customer data storage.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally in automotive retail software startups between 2022–2024, with strong venture backing for SaaS-based platforms.

Innovation & Future Outlook: Integration of AI copilots, EV sales modules, subscription-based mobility billing, and unified data lakes are shaping next-generation dealership ecosystems.

Franchise dealerships contribute nearly 62% of total platform deployments, followed by independent dealers at 28% and fleet operators at 10%. AI-enabled pricing engines and digital F&I tools have improved sales processing speed by 20%. Data protection laws and EV sales growth are accelerating demand for compliance-ready cloud systems, particularly in North America and Europe, while Asia-Pacific exhibits strong growth in mobile-first dealer applications and integrated financing platforms.

The Automotive Dealer Technology Platforms Market plays a strategic role in modernizing automotive retail by integrating sales, inventory, financing, service, and compliance into unified digital ecosystems. As dealership networks expand and customer journeys become increasingly digital, platform-based models enable real-time decision-making and operational visibility. AI-driven inventory optimization tools deliver 18% improvement in stock turnover compared to traditional spreadsheet-based management systems. Similarly, automated F&I software reduces contract processing time by 25% compared to legacy manual documentation workflows.

North America dominates in deployment volume due to its large dealership base, while Europe leads in adoption intensity, with nearly 68% of enterprise dealer groups implementing integrated CRM and compliance modules. Asia-Pacific is rapidly advancing in mobile-first dealership platforms, with over 55% of urban dealerships using app-based sales tracking tools.

By 2028, AI-powered predictive analytics is expected to reduce dealership operating expenses by 15% through improved lead targeting and service scheduling optimization. Firms are committing to ESG targets such as 30% reduction in paper-based documentation by 2030 through digital contracting platforms and e-signature systems.

In 2024, a leading U.S. dealer group achieved a 22% increase in lead conversion and a 14% improvement in service appointment utilization through AI-enabled CRM automation. Moving forward, the Automotive Dealer Technology Platforms Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable digital transformation across global automotive retail ecosystems.

The Automotive Dealer Technology Platforms Market is shaped by rapid digital transformation across automotive retail, increasing vehicle electrification, evolving compliance mandates, and consumer preference shifts toward online purchasing journeys. Over 60% of vehicle buyers globally conduct digital research prior to visiting dealerships, requiring integrated CRM, digital retailing, and analytics capabilities. Multi-location dealer groups now represent more than half of enterprise-level software deployments, accelerating demand for scalable SaaS-based platforms.

Technological convergence is also influencing dynamics, with AI-driven pricing tools improving margin optimization by nearly 15% and automated service scheduling enhancing workshop utilization rates by 12–18%. Regulatory frameworks including data protection and digital documentation mandates further compel dealerships to adopt encrypted, cloud-hosted platforms. The competitive environment is intensifying as vendors expand API ecosystems and integrate EV inventory management modules to support the rising share of electric vehicle sales across North America, Europe, and Asia-Pacific.

Over 60% of global car buyers initiate their purchasing journey online, and nearly 45% complete at least one transactional step digitally before visiting a showroom. This behavioral shift compels dealerships to integrate digital retail modules, AI-based lead scoring, and omnichannel communication tools. Dealerships implementing end-to-end digital sales platforms report 20% faster transaction cycles and 18% higher lead conversion efficiency. Furthermore, over 70% of large dealership groups have transitioned to cloud-based DMS platforms to ensure real-time data synchronization across locations. Increasing EV adoption—accounting for more than 18% of global new vehicle sales—also requires advanced inventory tracking and battery lifecycle management modules, further accelerating platform adoption.

Automotive dealer platforms handle sensitive financial, personal, and credit data, making them targets for cyberattacks. In recent years, automotive retail networks have experienced double-digit increases in ransomware attempts, with average recovery costs exceeding USD 1 million per incident for large dealer groups. Approximately 40% of dealerships report gaps in advanced cybersecurity readiness, limiting rapid cloud migration. Compliance with data protection laws such as GDPR and U.S. state-level privacy regulations increases operational complexity and IT expenditure. Smaller independent dealerships, representing nearly 30% of the market, often lack capital and expertise for robust cybersecurity upgrades, slowing uniform adoption of advanced digital platforms.

AI-powered analytics enables predictive pricing, demand forecasting, and service scheduling optimization. Dealerships deploying AI-driven inventory management tools report 15–20% improvements in stock rotation and up to 12% reduction in carrying costs. Predictive service reminders increase workshop utilization by nearly 17%. Additionally, subscription-based mobility services and EV charging management modules create new revenue management layers integrated into dealer platforms. Asia-Pacific markets, where over 55% of urban dealerships use mobile-first CRM systems, present expansion opportunities for SaaS vendors offering localized digital financing and regulatory-compliant solutions.

Many dealership groups operate legacy DMS platforms installed over a decade ago, with limited API compatibility. Integration with modern AI, CRM, and digital retail tools often requires system overhauls, leading to temporary productivity disruptions of 8–12%. Multi-brand dealer groups managing over 10 locations face data standardization challenges across inventory, pricing, and customer databases. Additionally, staff training costs can increase IT transition budgets by nearly 15%. Resistance to change and limited in-house IT expertise in mid-sized dealerships further complicate migration toward fully integrated, cloud-native Automotive Dealer Technology Platforms.

AI-Driven Inventory Optimization Improving Turnover by 18%: AI-based pricing and demand forecasting tools are reducing excess inventory days by nearly 15% while improving stock turnover efficiency by 18%. Over 70% of enterprise dealership groups have integrated machine-learning models to dynamically adjust vehicle pricing based on regional demand and competitor benchmarking.

Cloud-Native DMS Adoption Surpassing 72% in Developed Markets: More than 72% of dealerships in North America now use cloud-based Dealer Management Systems, reducing IT infrastructure costs by 20% and enabling real-time multi-location synchronization across networks with 10+ branches.

Digital F&I Platforms Reducing Processing Time by 25%: Automated finance and insurance modules have shortened contract approval cycles by 25%, while e-signature adoption has cut paperwork processing errors by 30%. Approximately 65% of dealerships now provide fully digital loan pre-approval workflows.

EV-Focused Platform Modules Supporting 18% of New Vehicle Sales: With electric vehicles accounting for over 18% of global new car sales, dealer platforms now integrate battery diagnostics, charging subscription management, and carbon tracking dashboards. Around 50% of large dealership groups have deployed EV-specific inventory and service management modules to meet evolving consumer demand.

The Automotive Dealer Technology Platforms Market is segmented by type, application, and end-user, reflecting the evolving digital infrastructure of global automotive retail. Platform adoption varies significantly depending on dealership size, operational complexity, and regional regulatory requirements. Cloud-native systems dominate new deployments, while hybrid architectures remain relevant among legacy-heavy dealer networks. Application segmentation highlights the shift from transactional Dealer Management Systems (DMS) to integrated digital retail ecosystems, including CRM, analytics, and F&I automation.

From an end-user perspective, franchise dealer groups and multi-location enterprises represent the most technology-intensive segment, deploying unified data platforms to standardize operations across geographically dispersed branches. Independent dealerships and fleet operators demonstrate selective adoption, often prioritizing CRM and service management modules. Increasing EV sales, online financing penetration, and compliance-driven digitization are reshaping demand patterns across all segmentation layers, with measurable improvements in lead conversion, inventory efficiency, and service throughput influencing platform investments.

The market by type includes Dealer Management Systems (DMS), Customer Relationship Management (CRM) Platforms, Digital Retailing & E-commerce Modules, Inventory & Analytics Platforms, and Finance & Insurance (F&I) Automation Systems. Dealer Management Systems currently account for approximately 38% of overall platform adoption, as they serve as the operational backbone integrating sales, service, accounting, and inventory workflows. Their leading position is reinforced by the fact that over 72% of enterprise dealerships operate centralized DMS environments across multiple locations.

CRM platforms represent nearly 24% of deployments, supporting lead tracking and marketing automation. Digital Retailing & E-commerce modules hold around 18%, but adoption in this segment is rising fastest, expected to surpass 28% by 2033, expanding at an estimated CAGR of 9.4% due to increasing online vehicle purchase journeys. Inventory & Analytics Platforms and F&I Automation Systems together contribute approximately 20%, offering niche but high-value optimization capabilities.

In 2024, a major U.S. automotive retail group reported deploying AI-enhanced DMS upgrades across 150+ dealerships, reducing manual reconciliation errors by 30% and improving reporting speed by 25%, as highlighted in an industry technology review publication.

Application segmentation includes Vehicle Sales Management, Aftersales & Service Management, Customer Engagement & Marketing Automation, Financing & Insurance Processing, and Compliance & Data Security Management. Vehicle Sales Management leads with approximately 34% share, supported by over 60% of buyers initiating vehicle searches online and nearly 45% completing at least one transactional step digitally. Integrated pricing engines and online configurators have improved sales cycle speed by 20% in digitally enabled dealerships.

Customer Engagement & Marketing Automation accounts for about 22%, while Aftersales & Service Management represents 21%, reflecting the increasing reliance on predictive maintenance scheduling and automated service reminders. Financing & Insurance Processing, currently at 15%, is the fastest-growing application segment, expanding at an estimated CAGR of 8.8%, driven by digital loan pre-approvals and e-contracting adoption. Compliance & Data Security applications collectively hold around 8%, ensuring encrypted storage and audit readiness.

In 2025, more than 40% of large dealership groups globally reported piloting AI-driven customer engagement tools to personalize marketing campaigns. Additionally, nearly 58% of millennial and Gen Z buyers prefer dealerships offering fully digital financing workflows.

In 2025, a U.S. transportation technology assessment highlighted that over 12,000 dealerships had integrated digital F&I platforms to streamline credit approvals, reducing average processing time by 25%.

End-user segmentation includes Franchise Dealerships, Independent Dealerships, Multi-Location Dealer Groups, Fleet Operators, and Automotive OEM-Affiliated Retail Networks. Franchise dealerships currently account for approximately 44% of platform deployments due to standardized operational requirements and compliance mandates across branded networks. Multi-location dealer groups follow with around 30%, leveraging centralized cloud systems to manage 10–50 outlets under unified dashboards.

Independent dealerships represent nearly 18% of adoption, often prioritizing CRM and service modules rather than full-suite integrations. Fleet operators and OEM-affiliated retail networks collectively hold about 8%, focusing on bulk inventory management and predictive maintenance platforms. Multi-location dealer groups are the fastest-growing end-user segment, expanding at an estimated CAGR of 8.6%, fueled by consolidation trends and demand for unified enterprise analytics.

In 2025, more than 55% of enterprise-level dealer groups globally reported upgrading to AI-enabled analytics modules for performance benchmarking. Additionally, approximately 62% of vehicle buyers indicated preference for dealerships offering hybrid online-offline purchase models.

In 2024, a recognized automotive industry benchmarking survey reported that digital platform adoption among mid-sized dealership groups increased by 21%, enabling over 500 dealer networks to standardize multi-branch inventory and customer data management systems.

North America accounted for the largest market share at 36% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.7% between 2026 and 2033.

North America’s leadership is supported by more than 18,000 franchised dealerships and over 72% cloud DMS penetration across enterprise dealer groups. Europe holds approximately 27% share, driven by strict data governance mandates affecting over 65% of dealership IT systems. Asia-Pacific represents nearly 24% of the global market, supported by more than 50,000 active dealership outlets across China, India, and Japan combined. South America accounts for around 8%, while the Middle East & Africa contributes close to 5%, reflecting gradual digital transition across emerging automotive retail networks. EV adoption rates exceeding 20% in parts of Europe and 18% in North America are increasing demand for battery lifecycle management modules within dealer platforms. Meanwhile, over 60% of urban dealerships in Asia-Pacific report adopting mobile-first CRM systems, indicating strong digital acceleration across high-growth economies.

North America holds approximately 36% of the global Automotive Dealer Technology Platforms Market share, supported by a highly organized dealership ecosystem and strong enterprise IT budgets. The region’s demand is primarily driven by franchised automotive dealerships, large dealer groups managing 10–50 outlets, and finance-intensive vehicle sales networks. Over 72% of dealerships operate cloud-based Dealer Management Systems, while nearly 65% provide fully digital financing and e-contracting options. Regulatory frameworks such as data privacy laws and digital documentation mandates require encrypted storage and audit-ready systems, accelerating SaaS adoption. AI-powered inventory analytics tools have improved stock turnover rates by 18% across large dealer networks. A leading regional player, CDK Global, has expanded AI-enabled service scheduling modules across thousands of dealerships, improving service lane utilization by 15%. Consumer behavior shows strong hybrid purchase preference, with over 60% of buyers completing at least one digital transaction step before showroom visits.

Europe represents approximately 27% of the Automotive Dealer Technology Platforms Market, with Germany, the UK, and France leading adoption. More than 68% of enterprise dealership groups in Western Europe operate integrated CRM and compliance modules. Regulatory oversight under GDPR and regional digital documentation standards has pushed over 70% of dealerships to upgrade encryption and consent-management systems. The rapid expansion of EV sales—exceeding 22% of new car registrations in several EU countries—has increased deployment of EV inventory tracking and battery diagnostics modules. Local technology providers such as Keyloop are expanding unified retail platforms integrating sales, service, and mobility subscription billing. European consumers demonstrate strong regulatory awareness, with nearly 58% preferring dealerships offering transparent digital pricing and compliant e-contracting solutions, reinforcing demand for secure and explainable AI-enabled dealer platforms.

Asia-Pacific accounts for nearly 24% of global market volume and ranks as the fastest-growing regional segment. China, India, and Japan represent the largest consuming countries, collectively operating more than 50,000 dealership outlets. Urban dealership clusters in China report over 65% mobile CRM usage, reflecting strong smartphone penetration and e-commerce integration. Infrastructure expansion and rapid vehicle production—particularly in China and India—are increasing demand for real-time inventory analytics and centralized DMS solutions. Regional innovation hubs are investing in AI-driven pricing engines capable of processing over 1 million data points daily for demand forecasting. A leading regional automotive technology provider has deployed cloud-native dealer suites across 5,000+ outlets, reducing manual reconciliation tasks by 28%. Consumer behavior is heavily digital, with more than 62% of buyers preferring app-based vehicle browsing and financing pre-approval workflows.

South America contributes approximately 8% of the global Automotive Dealer Technology Platforms Market, with Brazil and Argentina serving as primary markets. Brazil alone hosts over 7,000 franchised dealerships, many undergoing phased digital modernization. Around 48% of mid-sized dealerships in Brazil have transitioned to cloud-based CRM platforms to streamline lead management and marketing automation. Government trade policies encouraging automotive production localization are indirectly supporting dealership digitization initiatives. Infrastructure investments in urban mobility and connected vehicle ecosystems are also increasing platform integration needs. A regional dealership software provider recently expanded AI-based pricing modules across 1,200 dealership outlets, improving margin tracking accuracy by 14%. Consumer preferences in this region emphasize localized language interfaces and installment-based financing integration, with over 55% of buyers relying on dealership-arranged financing.

The Middle East & Africa region accounts for approximately 5% of global market share, with the UAE and South Africa as major growth contributors. Automotive retail modernization is being driven by diversified economic strategies and infrastructure development programs. In the UAE, over 50% of premium vehicle dealerships have implemented digital showroom platforms integrating virtual configurators and online booking systems. Oil-exporting economies are investing in smart retail ecosystems aligned with national digital transformation agendas. South Africa’s dealership networks are increasingly adopting CRM systems, with adoption rates approaching 45% among mid-sized outlets. A regional automotive retail group recently deployed centralized DMS solutions across 300+ branches, improving consolidated reporting speed by 20%. Consumer trends show strong demand for multilingual digital platforms and mobile-based booking tools, particularly among urban buyers.

United States – 31% Market Share: It is driven by over 18,000 franchised dealerships, high enterprise IT spending, and strong adoption of AI-enabled DMS and digital F&I systems.

Germany – 9% Market Share: It benefits from advanced automotive manufacturing ecosystems, strict digital compliance mandates, and high EV sales penetration supporting integrated dealer platform deployment.

The Automotive Dealer Technology Platforms Market is moderately consolidated, characterized by approximately 45–60 active global and regional competitors offering Dealer Management Systems (DMS), CRM platforms, digital retail modules, and F&I automation tools. The top five companies collectively account for nearly 62% of total market share, indicating strong concentration among established enterprise vendors while leaving room for specialized SaaS providers and regional software firms.

Leading vendors compete on platform integration depth, cybersecurity resilience, AI-enabled analytics, and multi-location scalability. Over 70% of large dealership groups (10+ outlets) prefer fully integrated suites rather than standalone modules, intensifying competition around unified ecosystems. Strategic initiatives between 2024 and 2025 included AI module launches, API-based open platform expansions, and dealership network partnerships exceeding 1,000+ rooftop integrations per agreement.

Mergers and acquisitions remain central to consolidation strategies, with several vendors acquiring niche CRM and digital F&I startups to strengthen omnichannel capabilities. Innovation trends include AI copilots for sales staff, predictive service scheduling tools improving workshop utilization by 15–20%, and blockchain-backed digital contracting systems enhancing document traceability. Cybersecurity investments have increased by nearly 25% among leading providers due to growing ransomware threats targeting dealership networks. Competitive differentiation increasingly depends on EV-specific modules, mobile-first architecture, and compliance-ready data encryption frameworks tailored to North American and European regulatory environments.

SAP Automotive

Oracle NetSuite

Tekion Corp – https://www.tekion.com

DealerSocket

Auto/Mate (Dealership Management Systems)

Keyloop

PBS Systems

Dominion DMS

Wipro Automotive Retail Solutions

AppOne

RouteOne

Autosoft DMS

e-Dealer

The Automotive Dealer Technology Platforms Market is undergoing rapid technological evolution driven by AI integration, cloud-native architecture, API interoperability, and data security advancements. More than 72% of enterprise dealerships now operate on cloud-based Dealer Management Systems, enabling real-time synchronization across 10–50 locations. Cloud migration has reduced infrastructure maintenance costs by approximately 20% while improving system uptime above 99.5%.

Artificial intelligence is central to next-generation platform capabilities. AI-driven pricing engines analyze over 1 million transactional data points daily to recommend optimal pricing, improving gross margin accuracy by 12–15%. Predictive service analytics platforms increase workshop scheduling efficiency by 17%, while AI-based lead scoring improves sales conversion rates by 20% or more in digitally mature dealerships.

Open API ecosystems are enabling seamless integration with third-party tools such as EV charging management software, insurance underwriting systems, and digital identity verification modules. Around 65% of dealer groups now demand open architecture platforms capable of integrating at least 15 external applications.

Cybersecurity technologies have also advanced significantly, with 100% encrypted cloud storage, multi-factor authentication adoption exceeding 68%, and AI-driven threat detection reducing incident response time by 30%. Additionally, blockchain-backed e-contracting solutions are being piloted to enhance document traceability and compliance reporting. EV-specific modules—including battery health tracking and charging subscription management—are now deployed in nearly 50% of large dealership groups, reflecting the increasing electrification of vehicle portfolios and the need for specialized digital workflows.

• In January 2026, CDK introduced a unified Customer Data Platform (CDP) embedded within its Dealership Xperience solution to consolidate fragmented customer info, deliver real‑time actionable insights, and enhance personalization and operational efficiency across sales, service, and marketing workflows. Source: www.cdkglobal.com

• In January 2025, Cox Automotive published the 20th annual Dealertrack Compliance Guide, providing updated regulatory strategies for dealers navigating heightened state and federal data privacy, consumer protection, and fair financing rules, aimed at improving transparency and trust across dealership operations. Source: www.coxautoinc.com

• In March 2025, Tekion announced the launch of AI Agents on its Automotive Retail Cloud platform designed to automate dealership workflows beyond insights, including service repair identification and coordination, enhancing customer interactions while reducing manual administrative effort. Source: www.businesswire.com

• In July 2024, Tekion secured $200 million in growth capital from Dragoneer Investment Group to accelerate product innovation, expand dealer and OEM adoption of its cloud‑native platform, and enhance implementation capabilities for global automotive retailers. Source: www.businesswire.com

The Automotive Dealer Technology Platforms Market Report provides comprehensive coverage of integrated digital solutions deployed across automotive retail ecosystems. The scope includes segmentation by product type such as Dealer Management Systems, CRM platforms, Digital Retailing modules, Inventory & Analytics tools, and Finance & Insurance automation systems. Application coverage spans vehicle sales management, aftersales service optimization, marketing automation, compliance management, and digital financing workflows.

Geographically, the report evaluates five primary regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—covering more than 70 countries with active automotive dealership networks. The analysis incorporates over 50,000 dealership outlets globally, assessing cloud adoption rates exceeding 72% in developed markets and mobile-first CRM penetration surpassing 60% in high-growth Asia-Pacific economies.

Technological scope includes AI-based pricing engines processing over 1 million daily data inputs, blockchain-enabled contract management systems, API-driven interoperability frameworks supporting 15+ third-party integrations, and cybersecurity systems with multi-factor authentication adoption nearing 70%. The report further examines EV-focused modules implemented in nearly half of large dealership groups, reflecting electrification trends.

Industry focus areas extend to franchised dealerships, independent retailers, fleet operators, and multi-location enterprise dealer groups managing 10–50 outlets. The report provides decision-makers with strategic insight into digital transformation benchmarks, compliance readiness metrics, enterprise integration trends, and innovation pathways shaping the Automotive Dealer Technology Platforms Market landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,690 Million |

| Market Revenue (2033) | USD 4,587.5 Million |

| CAGR (2026–2033) | 6.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | CDK Global; Reynolds and Reynolds; Cox Automotive (Dealertrack); SAP Automotive; Oracle NetSuite; Tekion Corp; DealerSocket; Auto/Mate; Keyloop; PBS Systems; Dominion DMS; Wipro Automotive Retail Solutions; AppOne; RouteOne; Autosoft DMS; e-Dealer |

| Customization & Pricing | Available on Request (10% Customization Free) |