Reports

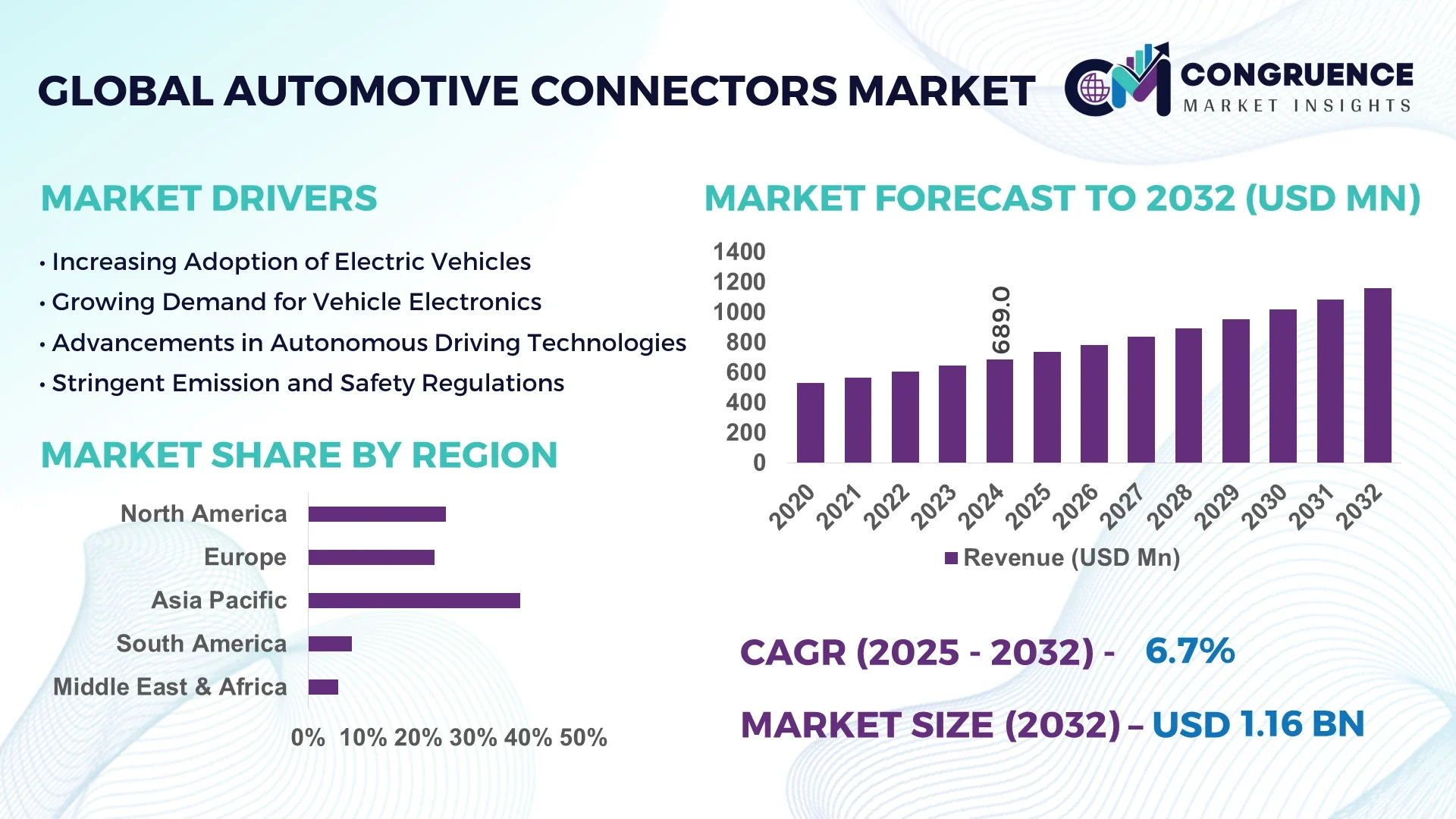

The Global Automotive Connectors Market was valued at USD 689.0 Million in 2024 and is anticipated to reach a value of USD 1,157.5 Million by 2032 expanding at a CAGR of 6.7% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Asia-Pacific dominates the automotive connectors market, driven largely by China’s expansive automotive manufacturing sector and rapid electric vehicle adoption. The region’s large-scale production facilities and increasing demand for advanced vehicle electronics make it the largest contributor globally, with manufacturers focusing heavily on integrating sophisticated connectors for EV powertrains and safety systems.

The automotive connectors market is evolving rapidly with the increasing complexity of vehicle electronics. Key applications include powertrain, safety and security systems, infotainment, and body electronics. The demand for connectors capable of withstanding harsh automotive environments, supporting high-speed data transmission, and ensuring reliability is rising. Additionally, the push toward lightweight materials and miniaturization of connectors aligns with industry efforts to improve fuel efficiency and vehicle performance. Innovations in connector designs now emphasize waterproofing, vibration resistance, and compatibility with electric vehicle battery systems, enhancing the market’s technological sophistication.

Artificial Intelligence (AI) is revolutionizing the automotive connectors market by enabling smarter design, testing, and manufacturing processes. AI-powered predictive analytics help manufacturers optimize connector designs to improve durability and performance under extreme conditions. Intelligent automation in production lines has significantly enhanced quality control, reducing defect rates by identifying potential failures early through machine learning algorithms. AI-driven simulation tools enable engineers to model complex connector behaviors, accelerating development cycles and reducing costs. Furthermore, AI enhances supply chain management by forecasting demand and optimizing inventory, ensuring timely availability of critical components.

In product innovation, AI is facilitating the development of adaptive connectors that can self-diagnose faults or signal maintenance needs. These smart connectors improve vehicle safety by ensuring uninterrupted electrical connectivity and enabling real-time monitoring. Integration with connected car systems allows AI to analyze connector performance data during operation, leading to better maintenance schedules and reduced downtime. The incorporation of AI in automotive connectors supports the broader industry trend toward connected, autonomous, and electric vehicles, where seamless data and power transmission is critical for system reliability and user safety.

“In 2024, a major advancement was made with the introduction of AI-enabled smart connectors that incorporate embedded sensors capable of real-time health monitoring and diagnostics within electric vehicles. These connectors provide continuous feedback on connection integrity, temperature, and voltage levels, significantly improving safety and maintenance efficiency.”

The growing consumer preference for vehicles equipped with advanced comfort and safety features is a significant driver of the automotive connectors market. Manufacturers are integrating connectors that support features such as adaptive lighting, advanced driver assistance systems (ADAS), and infotainment platforms. These connectors must maintain reliable electrical connections despite vibrations, temperature fluctuations, and exposure to harsh environments. As safety regulations become stricter globally, the demand for connectors that can support multiple safety-related functions in modern vehicles continues to grow rapidly.

The adoption of sophisticated connector technologies is often hindered by high production and material costs. Specialized connectors with enhanced durability, waterproofing, and data transmission capabilities require expensive materials and manufacturing processes. This can limit their use, especially in cost-sensitive vehicle segments or in developing markets where price competitiveness is crucial. Additionally, the complexity of integrating these connectors into existing vehicle architectures adds to development expenses, posing a challenge for manufacturers aiming to balance performance with cost efficiency.

The rapid growth of the electric vehicle (EV) sector presents substantial opportunities for the automotive connectors market. EVs require high-performance connectors for battery management systems, high-voltage power distribution, and charging infrastructure. The shift towards electrification is driving the demand for connectors that can handle high current loads and ensure safety under thermal and mechanical stress. Increasing government incentives and consumer adoption of EVs globally are accelerating the need for innovative connector solutions tailored specifically for electric mobility applications.

The increasing technological complexity of automotive connectors, driven by new functionalities and integration requirements, poses significant challenges. Achieving interoperability and standardization across various connector types and vehicle platforms remains difficult. Fragmentation in standards can lead to compatibility issues and increase costs for manufacturers who need to develop multiple connector variants. Additionally, the rapid pace of technological advancement demands continuous innovation, which requires substantial R&D investment and poses risks related to product obsolescence and supply chain management.

Miniaturization and Modular Designs: The market is shifting towards smaller, more compact connectors with higher pin density. This supports the increasing number of electronic control units (ECUs) in modern vehicles, especially electric and autonomous vehicles, without increasing space or weight. This trend helps improve vehicle architecture efficiency.

Integration of Fiber Optic Connectors: To meet demands for high-speed data transmission in connected and autonomous vehicles, fiber optic connectors are being increasingly adopted. These connectors facilitate faster and more reliable communication between complex vehicle sensor networks and infotainment systems, supporting enhanced vehicle connectivity.

Use of Sustainable and Recyclable Materials: Environmental concerns are prompting manufacturers to use eco-friendly plastics and metals in connector production. These materials aim to reduce the automotive industry’s carbon footprint while maintaining durability and performance, in line with stricter environmental regulations and greener manufacturing goals.

Automation and AI-Driven Manufacturing Processes: The rise of robotic assembly lines and AI-based quality inspections is boosting production efficiency and product consistency. Automation reduces human errors and enhances manufacturing precision, allowing OEMs to meet stringent quality standards and improve the reliability of automotive connectors.

The automotive connectors market is segmented by type, application, and end-user, each offering unique growth opportunities. By type, the market includes wire-to-wire, wire-to-board, and board-to-board connectors, each catering to different electrical connection needs within vehicles. Applications span powertrain systems, body electronics, infotainment, safety and security systems, and more, reflecting the diverse use cases of connectors in modern automobiles. End-user segments include passenger cars, commercial vehicles, and electric vehicles (EVs), with varying demands based on vehicle type and technology integration. This segmentation allows manufacturers to focus on specialized connectors that meet the precise requirements of each segment, driving innovation and adoption across the automotive industry.

The automotive connectors market by type includes wire-to-wire, wire-to-board, board-to-board, and others such as coaxial and power connectors. Among these, wire-to-wire connectors hold the largest market share due to their extensive use in power distribution and signal transmission across vehicle systems. They are favored for their flexibility and ease of installation in complex wiring harnesses. Wire-to-board connectors are the fastest-growing segment, driven by increasing integration of electronic control units (ECUs) and demand for compact, reliable connections on circuit boards in vehicles. Board-to-board connectors, used mainly for connecting printed circuit boards, continue to see steady growth with the rise of infotainment and telematics systems. The shift towards electric vehicles also boosts demand for high-current power connectors capable of handling battery and charging system requirements. Overall, the variety of connector types enables tailored solutions across evolving automotive architectures.

In terms of application, the automotive connectors market is divided into powertrain, safety and security, infotainment, body electronics, and others. The powertrain segment dominates the market due to the critical role connectors play in engine management, fuel injection, and transmission systems. High durability and resistance to extreme conditions are essential in this segment, supporting its leading position. The fastest-growing application segment is safety and security, fueled by the proliferation of advanced driver-assistance systems (ADAS), airbags, and electronic stability control systems. Increasing regulatory mandates for vehicle safety features are accelerating connector demand in this area. Infotainment systems, which include multimedia and navigation devices, also contribute significantly to market growth by requiring connectors that support high-speed data transmission and reliable connectivity. This application diversity reflects the expanding complexity of modern vehicles.

The end-user segmentation of the automotive connectors market includes passenger cars, commercial vehicles, and electric vehicles (EVs). Passenger cars dominate the market owing to their higher production volumes and the incorporation of advanced electronics across all vehicle segments, from economy to luxury models. Commercial vehicles, while smaller in volume, demand rugged connectors designed to withstand harsh operating conditions and heavier usage, supporting steady growth in this segment. The fastest-growing end-user segment is electric vehicles, propelled by rapid adoption worldwide and government incentives promoting green transportation. EVs require specialized connectors for battery packs, high-voltage powertrains, and charging stations, creating significant demand for innovative and high-performance connectors. This shift towards electrification is reshaping end-user dynamics and pushing the market towards more sustainable and technologically advanced connector solutions.

Asia-Pacific accounted for the largest market share at 38.5% in 2024; however, North America is expected to register the fastest growth, expanding significantly between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Asia-Pacific’s dominance is attributed to its vast automotive manufacturing base, especially in China, Japan, and South Korea, which drives high demand for automotive connectors across passenger vehicles and electric vehicles. Meanwhile, North America’s growth is fueled by increasing adoption of electric and autonomous vehicles, as well as strong investments in advanced automotive electronics. Europe and other regions also contribute substantially due to rising safety regulations and technological innovation in automotive connectivity solutions.

Technological Advancements Drive Market Innovation in North America

The North American automotive connectors market is characterized by rapid adoption of cutting-edge technologies such as smart connectors integrated with diagnostic sensors and AI-powered assembly lines. The U.S. leads the region with significant investments in electric vehicle production and autonomous vehicle development, boosting demand for high-performance connectors. Canada and Mexico also contribute, focusing on manufacturing efficiency and lightweight connector solutions. Growing regulatory emphasis on vehicle safety and emissions is accelerating the integration of connectors supporting advanced driver assistance systems (ADAS) and emission control systems, fostering steady market expansion.

Sustainability and Safety Regulations Propel Connector Innovations in Europe

Europe's automotive connectors market is driven by stringent environmental regulations and safety standards. Germany and France hold major shares, emphasizing eco-friendly materials and durable connector designs for electric and hybrid vehicles. The region is witnessing a growing demand for connectors capable of supporting complex infotainment and telematics systems in premium vehicles. Additionally, the expansion of electric vehicle infrastructure across countries like Norway and the Netherlands is encouraging manufacturers to develop connectors suited for high-voltage battery systems and charging networks. Collaborations between OEMs and technology providers are fostering innovations focused on reliability and modularity.

Rapid Electrification and Mass Production Fuel Market Growth in Asia-Pacific

Asia-Pacific remains the global leader in automotive connectors, led by China’s dominance in vehicle production and electric vehicle adoption. Japan and South Korea also play key roles with advanced electronics manufacturing. The region emphasizes high-volume production of connectors supporting electric powertrains, battery management systems, and infotainment electronics. Cost efficiency and scalability are crucial trends, with manufacturers investing in automated production and smart quality control systems. Expansion of EV charging infrastructure and government policies promoting green mobility further drive connector innovations and market growth across the region.

Emerging Manufacturing Hubs and Growing Vehicle Electrification in South America

South America’s automotive connectors market is growing steadily, led by Brazil and Argentina. The focus is on developing affordable yet reliable connectors for passenger and commercial vehicles, adapting to local manufacturing capabilities. Electrification trends are emerging, with increasing adoption of electric buses and light commercial EVs in urban centers, boosting demand for specialized connectors. Efforts to improve supply chain resilience and quality standards are influencing market dynamics. Additionally, import substitution strategies are encouraging local production of automotive connectors to reduce dependency on imports and enhance market stability.

Infrastructure Development and Electrification Initiatives Drive Market Growth

The Middle East & Africa automotive connectors market is evolving, led by countries such as the UAE and South Africa. Increasing investments in automotive manufacturing and EV infrastructure projects contribute to growing demand. The region is witnessing a gradual shift towards electric and hybrid vehicles, stimulating the need for connectors designed for high-voltage applications and harsh environmental conditions. Governments’ focus on sustainable transport and smart city initiatives is encouraging adoption of connected vehicle technologies. Challenges related to supply chain logistics and regulatory frameworks are being addressed to unlock further market potential.

Top Two Countries by Market Share in 2024

China: Holds the highest market share with an estimated value of USD 265 Million in 2024, driven by its vast automotive manufacturing industry and leadership in electric vehicle production.

United States: Holds the second-largest market share at approximately USD 180 Million in 2024, supported by rapid adoption of electric vehicles and advanced automotive electronics technologies.

The global automotive connectors market features a highly competitive landscape with numerous established players and emerging companies innovating rapidly. Key competitors focus on product diversification, technological advancements, and strategic partnerships to strengthen their market positions. Investments in research and development are driving the introduction of connectors with enhanced durability, miniaturization, and resistance to harsh environmental conditions. The market also sees consolidation trends, with mergers and acquisitions enabling companies to expand product portfolios and global reach. Companies emphasize customization to meet the specific needs of electric vehicles, autonomous systems, and connected car technologies. Regional manufacturing capabilities and supply chain optimization remain critical factors influencing competition, especially amid increasing demand for high-quality and cost-effective connectors worldwide.

TE Connectivity

Amphenol Corporation

Delphi Technologies

Yazaki Corporation

Molex LLC

JST Manufacturing Co., Ltd.

Sumitomo Electric Industries

Lear Corporation

Aptiv PLC

JAE Electronics, Inc.

Technological innovation is pivotal in the automotive connectors market, with manufacturers focusing on improving connector performance, miniaturization, and multifunctionality. Advanced materials such as high-temperature resistant polymers and corrosion-proof metals are increasingly used to ensure connectors withstand extreme automotive environments. The integration of fiber optic technology supports high-speed data transmission essential for connected and autonomous vehicles. Additionally, developments in wireless connector systems are emerging to reduce physical wiring complexity and weight. Manufacturing technologies like precision molding and automated assembly lines improve product consistency and reduce production costs. Furthermore, the rise of AI-assisted quality inspection ensures defect-free connectors, increasing reliability. These technological advancements enable the production of connectors that meet stringent safety and durability requirements while supporting evolving vehicle architectures, including electric powertrains and smart infotainment systems.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In December 2023, TE Connectivity launched a new series of lightweight, high-current connectors designed specifically for electric vehicle battery packs. These connectors offer enhanced thermal management and vibration resistance, improving overall battery system reliability.

In March 2024, Amphenol Corporation unveiled a next-generation board-to-board connector optimized for high-speed data transfer in autonomous vehicle systems, featuring improved shielding and miniaturized form factors.

In November 2023, Yazaki Corporation announced the expansion of its production facility in Mexico to increase output capacity for wire-to-wire connectors, addressing rising demand in the North American automotive manufacturing sector.

The automotive connectors market report provides a comprehensive analysis of market dynamics, technological advancements, and competitive landscapes globally. It covers key segments based on connector types, applications, and end-users, offering detailed insights into emerging trends and growth opportunities. The report assesses regional market variations, highlighting significant contributions from Asia-Pacific, North America, and Europe. It also examines the impact of electrification, autonomous driving, and connectivity on connector demand. By evaluating product innovations and manufacturing technologies, the report aids stakeholders in identifying strategic investment areas. Additionally, it outlines challenges such as supply chain constraints and raw material fluctuations affecting market growth. Overall, the report serves as a vital resource for manufacturers, suppliers, and investors aiming to capitalize on the evolving automotive connectors industry.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Automotive Connectors Market |

| Market Revenue (2024) | USD 689.0 Million |

| Market Revenue (2032) | USD 1,157.5 Million |

| CAGR (2025–2032) | 6.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional & Country Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | TE Connectivity, Amphenol Corporation, Delphi Technologies, Yazaki Corporation, Molex LLC, JST Manufacturing Co., Ltd., Sumitomo Electric Industries, Lear Corporation, Aptiv PLC, JAE Electronics, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |