Automotive Connecting Rod Market Trends

• Rising Adoption of Lightweight Connecting Rods in Performance Vehicles: Lightweight connecting rods are becoming increasingly popular in high-performance and premium vehicles. Automakers are leveraging materials such as titanium and forged aluminum to reduce engine weight and enhance acceleration without compromising on durability. These rods help achieve higher RPMs and greater fuel efficiency. The motorsports industry, including Formula 1 and endurance racing, is significantly contributing to this trend. OEMs are now integrating such lightweight designs into performance variants of consumer vehicles to improve engine responsiveness and thermal efficiency.

• Increased Demand for Powder Metallurgy and Fracture-Split Connecting Rods: Powder metallurgy and fracture-split technology are revolutionizing mass production in the automotive sector. Powder forged connecting rods offer superior fatigue resistance and dimensional consistency, making them ideal for high-volume passenger vehicle production. Fracture-split rods are cost-effective and simplify the manufacturing process by eliminating the need for additional machining. In 2024, the majority of small-displacement engines manufactured in Asia utilized fracture-split rods due to their precise alignment and cost benefits, especially in 3-cylinder and 4-cylinder engine platforms.

• Integration of Smart Manufacturing and AI-Driven Quality Control: Automotive connecting rod manufacturers are increasingly integrating smart manufacturing technologies to enhance quality and traceability. AI-powered inspection systems are being deployed on production lines to detect micro-cracks, measure dimensional tolerances, and ensure consistent metallurgical properties. These systems reduce human error and scrap rates while optimizing process efficiency. Manufacturers in countries like Germany, Japan, and the United States are also utilizing IoT-enabled machines to gather real-time production data for predictive maintenance and inventory management.

• Global Shift Toward Hybrid Powertrains Sustaining Market Demand: While pure electric vehicles eliminate the need for connecting rods, hybrid powertrains continue to rely on internal combustion engines. The global surge in hybrid vehicle production is supporting the demand for high-durability connecting rods that can withstand frequent start-stop cycles and thermal fluctuations. Manufacturers are investing in thermally stable alloys and enhanced fatigue-resistant designs to address the needs of hybrid engines. This trend is particularly strong in North America and Asia, where hybrid adoption is rising as a transitional solution toward full electrification.

Segmentation Analysis

The Automotive Connecting Rod Market is segmented by type, application, and end-user, reflecting the diverse use of connecting rods in automotive engines across varying load requirements and performance standards. Types of connecting rods include steel, aluminum, titanium, and others, each catering to specific automotive demands such as cost-efficiency or performance optimization. In terms of applications, connecting rods are used in passenger cars, light commercial vehicles, and heavy commercial vehicles, depending on the engine size and operating conditions. From an end-user perspective, the market caters to OEMs and aftermarket suppliers, with OEMs representing the bulk of the demand due to their integral role in engine manufacturing. Increasing investments in lightweight materials and high-performance engines are influencing the preferences across all segments.

By Type

The Automotive Connecting Rod Market is classified into steel, aluminum, titanium, and others. Steel connecting rods hold the largest market share, with over 55% in 2024, primarily due to their strength, affordability, and compatibility with standard internal combustion engines. Steel remains the material of choice for most mass-produced vehicles, especially in emerging markets where cost efficiency is crucial. Aluminum connecting rods are witnessing the fastest growth due to their lightweight properties and application in sports and high-performance vehicles, with demand rising steadily in North America and Europe. Titanium rods, while offering the best strength-to-weight ratio, are limited to premium vehicles due to high production costs. The “others” category includes composite or alloy-based rods that are still in experimental or early-stage commercial use. As the automotive sector increasingly focuses on fuel economy and efficiency, lightweight aluminum rods are gaining traction for both OEMs and aftermarket performance upgrades.

By Application

Based on application, the Automotive Connecting Rod Market is segmented into passenger vehicles, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs). Passenger vehicles dominate the market, accounting for over 60% of global demand in 2024, due to the sheer volume of vehicles produced annually and the rising penetration of internal combustion and hybrid engines. LCVs, which include vans and pickup trucks, represent the second-largest segment and are expected to show notable growth driven by increasing urban logistics and e-commerce activity. The HCV segment is growing steadily, particularly in developing countries where robust engine parts are essential for freight transportation. Among these, passenger vehicles remain the leading segment, while LCVs are projected to be the fastest-growing, thanks to a rising demand for last-mile delivery services and infrastructure development. The high replacement frequency of connecting rods in commercial fleets further supports aftermarket growth in both LCV and HCV segments.

By End-User Insights

In terms of end-user, the Automotive Connecting Rod Market is segmented into OEMs (Original Equipment Manufacturers) and aftermarket. OEMs continue to lead the segment, accounting for nearly 70% of market share in 2024, as connecting rods are an essential component of newly manufactured internal combustion and hybrid engines. OEMs benefit from long-term contracts, scale efficiencies, and advanced R&D capabilities that support product innovation and compliance with evolving emission norms. However, the aftermarket segment is the fastest growing, driven by the aging vehicle fleet and increasing demand for high-performance and replacement components. In regions such as Asia-Pacific and Latin America, aftermarket players are witnessing rising sales, especially for two-wheelers and older cars that frequently require part replacements. The customization trend in vehicle tuning and performance upgrades is also bolstering the demand for aftermarket connecting rods, especially in motorsport and enthusiast communities.

Region-Wise Market Insights

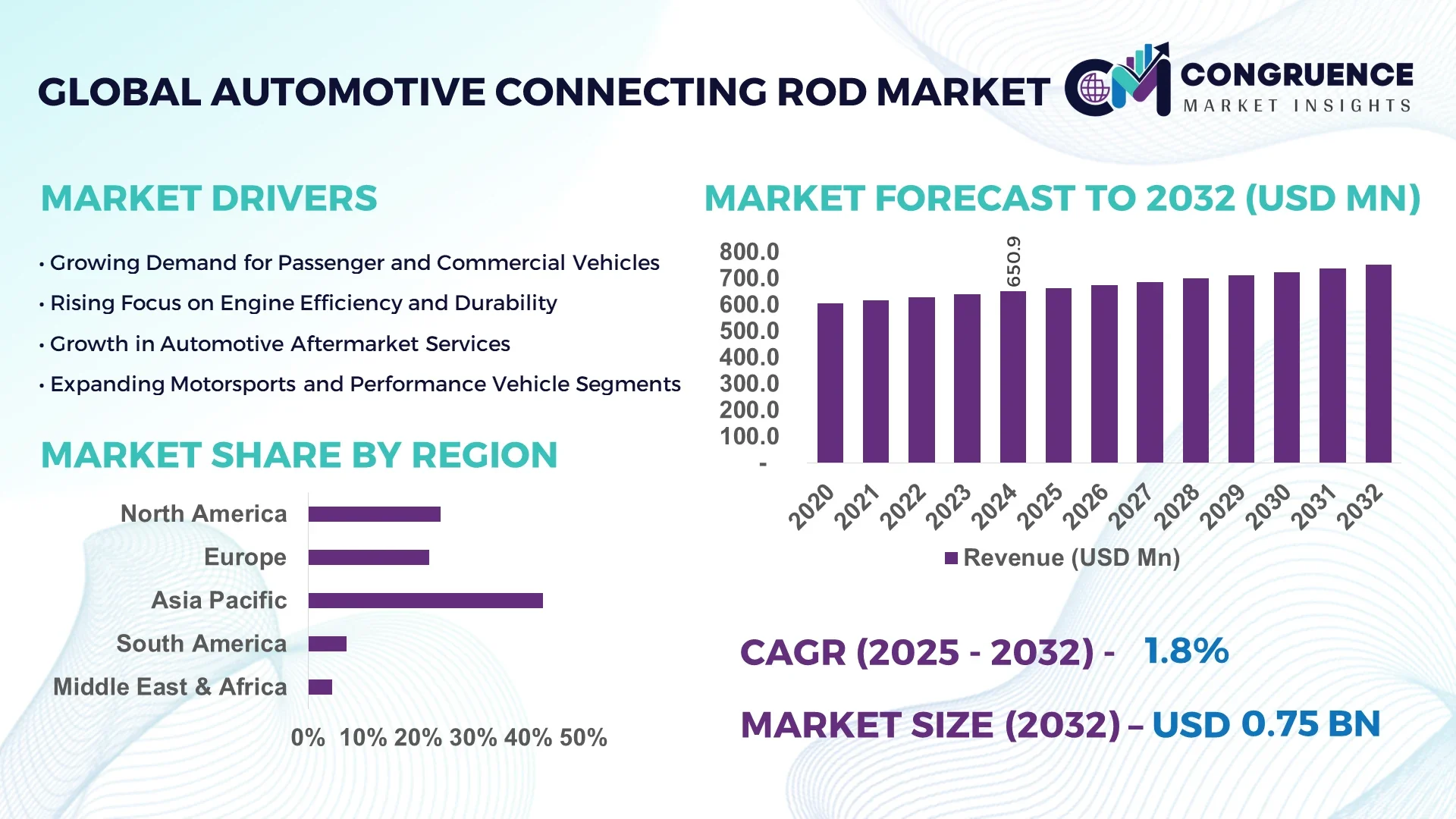

Asia-Pacific accounted for the largest market share at 42.6% in 2024; however, South America is expected to register the fastest growth, expanding at a CAGR of 5.7% between 2025 and 2032.

Asia-Pacific leads the global Automotive Connecting Rod Market due to the region's massive automotive manufacturing hubs in countries like China, India, and Japan. High vehicle production, expanding middle-class populations, and increasing domestic consumption continue to drive demand in this region. Europe and North America also hold substantial market shares due to a strong base of automotive OEMs and innovation in performance vehicle parts. South America, despite a smaller base, is poised for rapid growth due to rising automotive investments, improving economic conditions, and increasing vehicle ownership in countries like Brazil and Argentina. The region’s shift toward localized manufacturing and expansion in mid-sized car production is further accelerating connecting rod demand.

North America Automotive Connecting Rod Market Trends

Advanced Engine Technologies Drive Lightweight Connecting Rod Demand

The North American Automotive Connecting Rod Market remains strong, supported by a large number of internal combustion vehicle users and growing demand for performance-enhancing components. The U.S. dominates the regional market, accounting for over 75% of North America’s total share in 2024. The trend toward turbocharged and high-performance engines is increasing the adoption of aluminum and titanium connecting rods. Furthermore, the region’s well-developed aftermarket industry contributes significantly to connecting rod replacements and upgrades. Automotive sports and modification culture in the U.S. and Canada is fueling demand for durable and lightweight connecting rods, particularly among small car enthusiasts and motorsport users.

Europe Automotive Connecting Rod Market Trends

Sustainability and Lightweighting Influence Connecting Rod Innovation

Europe's Automotive Connecting Rod Market is driven by stringent emission regulations and a sharp focus on engine efficiency. Germany leads the region with over 34% market share in 2024, thanks to its robust auto manufacturing and premium car production. The increasing adoption of lightweight materials such as aluminum and titanium is notable across European OEMs, particularly in Germany, France, and Italy. Hybrid and plug-in hybrid vehicles are also pushing manufacturers to adopt high-strength yet light connecting rods for better thermal efficiency. Additionally, the strong presence of Tier-1 suppliers in countries like the UK and Poland is enhancing regional supply chains and export potential.

Asia-Pacific Automotive Connecting Rod Market Trends

Mass Vehicle Production and Growing Two-Wheeler Sector Boost Market

Asia-Pacific leads globally in automotive connecting rod consumption, propelled by high-volume vehicle manufacturing and a vast two-wheeler market. China alone holds over 41% of the regional share in 2024, followed by India and Japan. OEMs in this region rely heavily on steel rods due to their cost efficiency, especially in budget cars and motorcycles. However, the demand for aluminum rods is growing in Japanese and South Korean sports car segments. Additionally, rising disposable incomes and urbanization in Southeast Asia are increasing vehicle sales, further supporting market growth. Government initiatives in India and China promoting domestic automotive production also contribute to the upward trajectory.

South America Automotive Connecting Rod Market Trends

Automotive Industry Recovery and Local Manufacturing Fuel Market Expansion

The South American market for automotive connecting rods is witnessing a surge in growth, especially in Brazil and Argentina. Brazil held a market share of 62% in the region in 2024, benefiting from a revitalized automotive sector and increased domestic production. Recovery in passenger and light commercial vehicle sales is encouraging OEMs and component manufacturers to expand their presence in this market. There’s also a significant aftermarket demand for connecting rods due to aging fleets and high maintenance needs. Local component manufacturing initiatives and a growing network of domestic suppliers are further enhancing accessibility to connecting rods within the region.

Middle East & Africa Automotive Connecting Rod Market Trends

Rising Vehicle Imports and Fleet Maintenance Drive Connecting Rod MarketThe Middle East & Africa region is emerging as a growth zone for the automotive connecting rod market, led by increasing vehicle imports and expanding commercial vehicle fleets. South Africa and the UAE together held over 58% of the market share in MEA in 2024. South Africa benefits from local assembly lines, while the UAE relies heavily on luxury and performance imports that require specialized connecting rod components. Demand for aftermarket connecting rods is strong, particularly for commercial vehicles used in logistics, mining, and oil-related operations. Increased investments in road infrastructure and automotive service centers are also boosting component replacement rates in the region.

Top Two Countries with Highest Market Share

-

China (31.4%): China holds the largest market share due to its massive automotive manufacturing base and high vehicle production volume.

-

United States (18.2%): The United States benefits from a strong aftermarket industry and a significant presence of performance vehicle enthusiasts.

Market Competition Landscape

The Automotive Connecting Rod Market is highly competitive, with numerous key players vying for market share. Leading manufacturers are focusing on product innovation, strategic partnerships, and expanding their production capacities to cater to the increasing demand. Companies are leveraging advanced manufacturing technologies and utilizing high-quality materials to offer enhanced performance and durability of their connecting rods. With rising consumer preferences for fuel-efficient and high-performance vehicles, the competition is intensifying, especially in regions like North America, Europe, and Asia-Pacific. Several players are also investing in R&D to develop lightweight connecting rods and explore sustainable materials, ensuring a competitive edge. As a result, the market is witnessing frequent product launches, mergers, and collaborations among global leaders. These efforts are aimed at strengthening their market presence and providing cutting-edge solutions to meet the demands of the automotive sector.

Companies Profiled in the Automotive Connecting Rod Market Report

-

Mahle GmbH

-

Federal-Mogul Motorparts

-

Bosch Automotive Components

-

Aisin Seiki Co., Ltd.

-

NTN Corporation

-

Eagle Specialty Products

-

Scat Enterprises

-

K1 Technologies

-

Arrow Precision

-

Cummins Inc.

Technology Insights for the Automotive Connecting Rod Market

The automotive connecting rod industry is undergoing significant technological transformations to meet the evolving demands of modern engines. One notable advancement is the adoption of lightweight materials such as aluminum and titanium alloys. These materials offer a favorable strength-to-weight ratio, contributing to reduced engine weight and improved fuel efficiency. For instance, the use of aluminum connecting rods has led to a weight reduction of up to 20%, enhancing vehicle performance and meeting stringent emission standards.

Advanced manufacturing processes are also playing a crucial role in the evolution of connecting rods. Techniques like precision CNC machining and automated production lines enable the production of components with high dimensional accuracy and consistency. These methods not only improve the quality of the connecting rods but also increase production efficiency, allowing manufacturers to meet the growing demand in a timely manner.

Furthermore, the integration of 3D printing technology is revolutionizing the prototyping and manufacturing phases. This technology allows for the creation of complex geometries that were previously challenging to achieve with traditional methods. It also facilitates rapid prototyping, reducing the time required for product development and testing.

Additionally, the industry is witnessing innovations in design, such as the development of hollow connecting rods. These designs reduce the overall weight of the engine components without compromising strength, further contributing to fuel efficiency and performance. The continuous advancements in materials, manufacturing processes, and design are propelling the automotive connecting rod market toward more efficient and sustainable solutions.

Recent Developments in the Global Automotive Connecting Rod Market

-

In October 2023, Transcend Energy Group introduced the Thunder Rod, a two-piece connecting rod that shifts the actuator's pivot point to the joining rod. This design allows the piston to move up and down without sideways motion, reducing piston rock and enhancing engine performance. The company claims that the Thunder Rod could increase torque and dynamic compression by 25-30%. Transcend has patented the technology and is in the early stages of road testing.

-

In March 2024, Linamar Corporation announced the expansion of its high-performance automotive components manufacturing capabilities, including automotive connecting rods. This expansion aims to meet the growing demand for high-quality, durable components in electric and hybrid vehicle applications.

-

In April 2024, Mahle GmbH launched an upgraded connecting rod line using high-performance alloys tailored for hybrid vehicles. This development aligns with Mahle's goal to offer weight-optimized components, improving energy efficiency in both internal combustion engine and hybrid powertrains.

-

In October 2024, Bharat Forge Ltd acquired AAM India Manufacturing Corp., adding the commercial passenger vehicle axle and rod business in Pune to its portfolio. This acquisition enhances Bharat Forge's product and manufacturing strategy, particularly in the passenger vehicle, hybrid, and electric vehicle segments in India.

Scope of Automotive Connecting Rod Market Report

The scope of the Automotive Connecting Rod Market report is to provide an in-depth analysis of the market trends, technological advancements, and growth opportunities within the automotive sector, specifically focusing on connecting rods. This report covers various key aspects, including market dynamics, segmentation by type, application, and end-user insights, regional analysis, and competitive landscape. It explores the increasing demand for high-performance and lightweight connecting rods, driven by the ongoing advancements in automotive engine technologies, including electric and hybrid vehicles.

The report delves into the different types of connecting rods, such as forged, cast, and powdered metal, analyzing their specific benefits and market adoption. It further explores their application across various vehicle types, from passenger cars to heavy-duty trucks, emphasizing the increasing use of connecting rods in high-performance and electric vehicles. The study also provides insights into the major geographical markets, such as North America, Europe, and Asia-Pacific, highlighting their dominant roles in the automotive industry.

Key market players, technological trends, and innovations such as the use of aluminum and titanium alloys, 3D printing, and lightweight materials are also covered in the report. This comprehensive analysis helps businesses, manufacturers, and investors in the automotive industry make informed decisions by providing valuable data on current and future market conditions, growth opportunities, and challenges within the automotive connecting rod market.