Reports

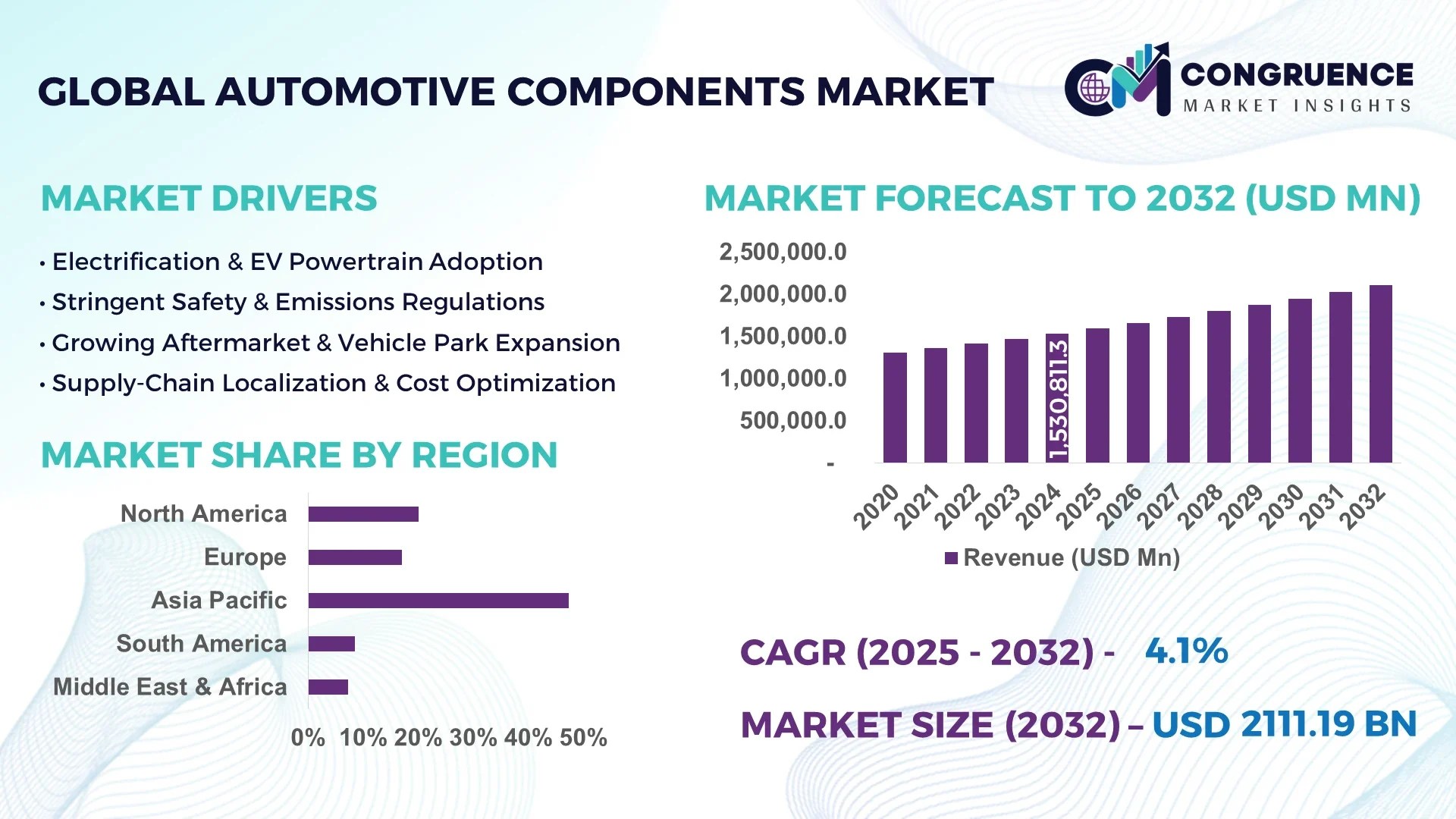

The Global Automotive Components Market was valued at USD 1,530,811.32 Million in 2024 and is anticipated to reach a value of USD 2,111,190.88 Million by 2032 expanding at a CAGR of 4.1% between 2025 and 2032.

In Japan, the country leading the automotive components marketplace, advanced production capacity continues to grow with significant investments in EV component manufacturing, high-precision drivetrain systems, and sensor modules for ADAS applications, aligning with the nation's commitment to low-emission and high-efficiency automotive technology development.

The Automotive Components Market covers a broad range of vehicle systems including powertrain, suspension, braking systems, lighting, electronics, and advanced driver-assistance systems, with each segment contributing dynamically to the overall ecosystem. The market has seen technological shifts with rising demand for lightweight materials, electrification of powertrain systems, and smart electronic control units aligning with sustainability goals and emission regulations. The integration of IoT and sensor-based diagnostics within automotive components enhances predictive maintenance, while environmental policies are accelerating adoption of green components across manufacturing facilities. Regional consumption patterns reveal Asia-Pacific maintaining high production and internal demand, whereas Europe and North America drive innovation in connected automotive components, digital cockpits, and autonomous-ready module systems. The market outlook highlights increasing investments in R&D for next-generation materials, enhanced durability, and high-efficiency designs, supporting the evolving electric and hybrid vehicle sectors within the Automotive Components Market.

Artificial intelligence is significantly transforming the Automotive Components Market by enabling manufacturers to achieve new benchmarks in operational efficiency and predictive performance across production lines. AI-powered quality inspection systems utilizing advanced computer vision algorithms identify microscopic defects in critical automotive components such as engine parts, braking systems, and electronic modules, reducing rework rates and minimizing material wastage. Additionally, AI-based predictive analytics are leveraged for equipment maintenance across automotive component manufacturing plants, reducing downtime and ensuring uninterrupted high-quality output.

In the Automotive Components Market, machine learning models are used to optimize supply chain management, aligning component availability with vehicle assembly schedules to reduce excess inventory and enhance response to demand fluctuations. AI-enabled robotics are improving precision in assembling complex electronic components and wiring harnesses, ensuring compliance with stringent quality norms across electric vehicle and ICE vehicle component manufacturing. AI is also streamlining product development cycles by using simulation-driven design optimization, allowing engineers to test component stress and thermal profiles digitally before physical prototyping, reducing development time while ensuring robust design output.

Furthermore, AI is helping manufacturers in the Automotive Components Market transition to sustainable production models by monitoring energy consumption in real time, analyzing emissions data, and automating adjustments across manufacturing processes to align with environmental compliance frameworks. AI-driven customer analytics are also helping component suppliers align product features with OEM requirements, enhancing competitiveness while improving design customization. This AI-driven evolution within the Automotive Components Market ensures higher performance, safety, and sustainability while maintaining competitive production costs across the evolving automotive landscape.

“In March 2025, an AI-powered adaptive production control system was implemented at a Japanese automotive component manufacturing facility, which reduced powertrain component production cycle times by 18% while improving dimensional accuracy by 12%, showcasing the transformative efficiency gains AI delivers within the Automotive Components Market.”

The Automotive Components Market is experiencing continuous evolution driven by advancements in electrification, autonomous technologies, and regulatory frameworks focusing on emission reduction and sustainability. Demand for lightweight components using high-strength steel and composites has risen to enhance fuel efficiency and reduce vehicle weight, while digitalization in manufacturing processes enables precision in producing complex assemblies. Key influences include the rising production of electric and hybrid vehicles, which is shifting demand toward advanced battery management systems, electric drivetrain components, and thermal management solutions. Additionally, consumer expectations for safety and connectivity features are pushing component manufacturers to innovate in ADAS modules, in-vehicle networking systems, and electronic control units, reshaping the global Automotive Components Market landscape.

The surge in electric vehicle production is a significant driver for the Automotive Components Market, creating high demand for specialized components including battery packs, power electronics, and lightweight structural parts. As global EV sales continue to expand, automotive component manufacturers are investing in advanced battery module housings, high-voltage wiring systems, and regenerative braking system components to meet OEM needs for electrified vehicle platforms. For instance, the production of electric drivetrains requires precision-engineered transmission and thermal management components to enhance energy efficiency and ensure safety standards are met. This shift toward electrification is fostering technological innovation across the Automotive Components Market while driving investments in automated and flexible manufacturing lines to support high-volume and customized component production.

Volatile raw material prices present a notable restraint within the Automotive Components Market, as fluctuations in the cost of aluminum, steel, rare earth elements, and specialized electronic materials directly impact manufacturing expenses and pricing strategies for suppliers. The automotive industry’s push toward lightweight and high-performance components requires the use of advanced materials whose prices are often influenced by global geopolitical factors and supply-demand imbalances. For example, disruptions in rare earth supply chains affect the availability of critical materials used in electronic and sensor-based components for ADAS and EV powertrains. These fluctuations lead to operational challenges for component manufacturers who must balance quality requirements with cost management while maintaining consistent delivery schedules to automotive OEMs in the highly competitive Automotive Components Market.

The rising integration of ADAS features across vehicle segments is presenting a significant opportunity for growth in the Automotive Components Market. As safety regulations tighten and consumer demand for advanced safety technologies increases, there is a strong market push for high-precision sensors, radar modules, camera-based monitoring systems, and electronic control units that enable automated driving functions and enhanced safety features. Manufacturers focusing on the development of robust, weather-resistant, and miniaturized ADAS components are well-positioned to capture emerging opportunities. For example, the integration of LiDAR systems and advanced image processing modules in braking and steering components is creating pathways for next-generation safety systems, driving investments in smart component manufacturing and stimulating innovation within the Automotive Components Market.

Navigating complex and evolving regulatory compliance requirements is a critical challenge within the Automotive Components Market. Different regions enforce varying standards for safety, emissions, and material usage in automotive components, requiring manufacturers to adapt product designs and processes accordingly. For example, the adoption of Euro 7 emission norms and stringent crash safety standards in Europe necessitates continuous redesigning and rigorous testing of components such as exhaust systems, braking modules, and electronic safety components. These compliance pressures increase certification costs and extend development timelines, impacting operational efficiency. Additionally, environmental regulations regarding recyclability and hazardous material restrictions in components add another layer of complexity, challenging global suppliers within the Automotive Components Market to balance regulatory adherence while ensuring cost-effectiveness and timely delivery to automotive OEMs.

• Expansion of EV-Specific Component Production: Electric vehicle growth is driving a measurable shift in the Automotive Components Market as manufacturers scale production of high-voltage battery management systems, electric drive modules, and regenerative braking systems. In 2025, multiple tier-1 suppliers in Asia-Pacific expanded EV component lines to address increased demand from local and European OEMs, emphasizing thermal management systems and lightweight battery enclosures. This trend supports high-efficiency EV adoption while boosting localized component manufacturing, reducing lead times, and enhancing production flexibility.

• Integration of Advanced Sensor Technologies: Automotive component manufacturers are adopting advanced sensor integration in braking, steering, and safety systems to support ADAS and semi-autonomous driving. The deployment of LiDAR and radar sensors in braking modules and steering actuators has increased, with notable installations across premium vehicle segments in Europe and North America. This trend is driving a rise in the production of weather-resistant, high-resolution sensors that enable enhanced real-time data collection for vehicle control systems, elevating component complexity and value.

• Lightweight Material Adoption in Components: There is a measurable rise in the use of high-strength, lightweight materials in powertrain and structural components to improve vehicle energy efficiency. Aluminum alloys, carbon fiber composites, and advanced polymers are increasingly used in engine components, suspension systems, and vehicle frames. In 2025, several manufacturers in Japan and Germany introduced new lightweight alloy component lines that support fuel economy targets while maintaining structural integrity, aligning with emission reduction frameworks in automotive manufacturing.

• Shift Toward Smart Manufacturing: Manufacturers in the Automotive Components Market are embracing smart manufacturing practices using automated quality control and AI-powered production optimization. In 2025, leading component suppliers adopted automated inspection systems using AI and machine vision to detect micro-level defects, reducing rework rates by over 15%. This transition is improving production efficiency while maintaining stringent quality standards, enabling scalable production of complex components for hybrid and electric vehicles across global manufacturing hubs.

The Automotive Components Market is segmented into types, applications, and end-user categories, providing a structured view of evolving demand drivers across the industry. By type, the market includes powertrain, chassis, braking systems, electronics, lighting systems, and interior components, with each segment contributing to technological advancements and vehicle efficiency improvements. In terms of applications, segments cover passenger cars, light commercial vehicles, heavy commercial vehicles, and electric vehicles, reflecting the diversity of demand across vehicle classes. End-user segmentation focuses on OEMs and the aftermarket, with OEMs driving demand for advanced safety and electrified components, while the aftermarket supports replacement and upgradation needs driven by aging vehicle fleets. The segmentation landscape enables stakeholders to align investment and production strategies to address evolving market needs effectively.

The powertrain components segment leads in the Automotive Components Market due to the continuous demand for high-performance engines, transmission systems, and drivetrain components that align with evolving emission norms and efficiency standards. Engine downsizing and the integration of turbocharging technologies are driving advancements in this segment, particularly in Asia-Pacific, where compact vehicle demand remains robust. The fastest-growing type is electronics, driven by the proliferation of ADAS, digital instrument clusters, and in-vehicle connectivity modules as OEMs prioritize safety and enhanced user experiences. Braking systems, lighting, and interior components maintain steady contributions to the market, with lighting systems seeing niche demand for LED and adaptive lighting modules in premium segments. Chassis and suspension components continue to evolve with lightweight material integration, supporting vehicle agility and fuel efficiency goals across OEM product lines in the Automotive Components Market.

Passenger cars dominate the Automotive Components Market application landscape, driven by consistent global demand for fuel-efficient, connected, and safe vehicles equipped with advanced components. The inclusion of sensor-integrated braking systems, lightweight powertrain modules, and advanced infotainment systems in passenger vehicles sustains this segment’s leadership. The fastest-growing application is electric vehicles, supported by rising environmental regulations and consumer interest in zero-emission mobility, leading to increased demand for battery packs, electric drivetrains, and high-voltage component systems. Light commercial vehicles and heavy commercial vehicles also contribute to market expansion, with a focus on durable powertrain components, efficient braking systems, and safety modules suited for high-load operations. This structured application analysis enables manufacturers to align component production strategies with the Automotive Components Market's evolving vehicle class demands.

OEMs are the leading end-user segment within the Automotive Components Market, driven by their continuous need for advanced, compliant, and reliable components for new vehicle models, including combustion, hybrid, and electric vehicles. OEMs require components that support vehicle safety, emissions reduction, and enhanced driving experiences, fueling consistent demand across global manufacturing hubs. The fastest-growing end-user segment is the aftermarket, propelled by the aging global vehicle fleet and increasing consumer preference for component upgrades and replacements. The aftermarket segment benefits from demand for high-quality replacement parts, performance-enhancing components, and electronics modules compatible with older vehicle systems. Other relevant end-users include fleet operators and specialty vehicle manufacturers, who contribute to the market by demanding customized, durable components aligned with specific operational requirements in the Automotive Components Market.

Asia-Pacific accounted for the largest market share at 47.3% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.7% between 2025 and 2032.

The Asia-Pacific Automotive Components Market remains a cornerstone for global manufacturing due to its extensive supplier networks, technological capability in advanced electronics, and the rising domestic demand in China, India, and Japan. North America’s strong growth trajectory is driven by increasing investments in electric and hybrid vehicle components, advanced ADAS modules, and robust regulatory frameworks supporting sustainable vehicle production. Europe continues to strengthen its position in high-precision and lightweight component manufacturing, aligning with its emissions and sustainability goals, while South America and the Middle East & Africa are witnessing steady demand increases for replacement and technologically upgraded components in the Automotive Components Market, driven by urbanization and industrial growth.

Driving Digitization and Electrification in Key Automotive Sectors

North America held a 24.8% share of the Automotive Components Market in 2024, with the United States leading demand for advanced electronic modules, lightweight structural parts, and ADAS components. Key industries including electric vehicle manufacturing, off-highway construction equipment, and defense vehicle production are primary drivers of component demand. Recent regulatory support for domestic EV battery production and advanced safety systems, under structured incentives, is accelerating the adoption of next-generation components. Technological advancements such as AI-enabled inspection, smart manufacturing lines, and digital twins for component validation are enhancing operational efficiency, supporting North America’s evolution into a high-tech hub within the Automotive Components Market.

Advanced Safety and Lightweight Trends Reshaping the Market Landscape

Europe captured a 19.3% share of the Automotive Components Market in 2024, with Germany, the UK, and France emerging as primary markets for high-quality automotive components across premium passenger and commercial vehicle segments. The region benefits from strict emission norms and Euro 7 compliance initiatives, pushing demand for lightweight aluminum and composite components in powertrain and chassis systems. Regulatory bodies continue to incentivize the adoption of green components and energy-efficient manufacturing. The adoption of emerging technologies including connected vehicle modules, advanced ADAS sensors, and digital manufacturing solutions is transforming the operational and production landscape, ensuring Europe's continued leadership in high-precision automotive component supply within the Automotive Components Market.

Strengthening Advanced Component Production and Local Consumption

Asia-Pacific maintained its position as the leading volume consumer in the Automotive Components Market, with China, India, and Japan driving high-volume demand across vehicle classes in 2024. Manufacturing trends in the region focus on scaling advanced EV component production, lightweight structure integration, and the adoption of smart manufacturing practices to address both domestic demand and global export needs. Japan continues to lead in precision drivetrain and ADAS module production, while India’s market is expanding with rising domestic vehicle assembly and tier-1 supplier base growth. Regional innovation hubs across China are focusing on integrated electronics and battery management systems, accelerating technological shifts within the Automotive Components Market across Asia-Pacific.

Infrastructure Development Supporting Component Market Growth

Brazil and Argentina are key countries within the South America Automotive Components Market, with Brazil accounting for the largest share due to its robust local vehicle manufacturing and aftermarket demand. Regional trends in 2024 highlight the increased need for durable powertrain and suspension components supporting agricultural and construction sectors as infrastructure projects expand. Government incentives under localized production policies and free-trade agreements with regional partners are facilitating the import of advanced manufacturing machinery for automotive components. Trends in the energy sector, including the push for biofuel-compatible vehicle systems, are influencing local component design priorities within the Automotive Components Market in South America.

Industrial Growth and Technological Upgradation Driving Demand

The Middle East & Africa Automotive Components Market is witnessing rising demand from sectors including oil & gas and construction, with UAE and South Africa emerging as key countries driving component purchases in 2024. The region’s market expansion is supported by increased vehicle assembly operations and a growing aftermarket for durable and reliable components suited for harsh operating conditions. Technological modernization trends include the gradual introduction of telematics modules, safety system components, and emission-compliant exhaust systems aligned with evolving local regulations. Trade partnerships within the Gulf and with African regional blocks are easing import and export flows, supporting market stability and growth in the Automotive Components Market across the Middle East & Africa.

China – 33.2% Market Share: High production capacity and robust domestic end-user demand support China’s dominance in the Automotive Components Market.

United States – 18.5% Market Share: Strong demand from electric vehicle and advanced safety system segments reinforces the United States’ leadership position within the Automotive Components Market.

The Automotive Components Market exhibits a highly competitive environment with over 300 active global and regional competitors operating across powertrain, electronics, chassis, and safety systems segments. Leading players are investing heavily in R&D to advance lightweight materials, precision electronics, and sensor-based safety modules, aligning with the increasing electrification and digitalization trends within the automotive sector. Strategic initiatives such as partnerships with EV manufacturers, technology licensing agreements, and the establishment of regional production hubs are common competitive moves, enhancing market reach and supply chain resilience. Mergers and acquisitions are shaping the landscape, particularly in advanced driver-assistance systems and electric drivetrain component segments, where integration of specialized technology providers strengthens the competitive positioning of larger players. Product innovation cycles have accelerated, with manufacturers launching smart components compatible with hybrid and electric vehicles, and digital cockpit modules to address connected vehicle demand. Additionally, competitive differentiation is evident in sustainability initiatives, including the adoption of energy-efficient production processes and the use of recyclable materials within automotive component manufacturing, further intensifying competition in the Automotive Components Market.

Robert Bosch GmbH

Denso Corporation

Magna International Inc.

ZF Friedrichshafen AG

Continental AG

Aisin Corporation

Valeo SA

BorgWarner Inc.

Hyundai Mobis Co., Ltd.

Aptiv PLC

Technological advancements are reshaping the Automotive Components Market with a focus on electrification, lightweight materials, and digital integration. Battery management systems are being optimized using advanced thermal interface materials to enhance thermal conductivity while reducing weight, crucial for next-generation EV powertrain components. High-strength aluminum alloys and carbon-fiber-reinforced plastics are increasingly adopted in chassis and structural components to improve crash performance while reducing mass, supporting fuel efficiency and sustainability targets.

Sensor technologies, including LiDAR, radar, and camera modules, are being integrated into braking and steering systems, advancing ADAS functionalities within the Automotive Components Market. These sensors are enabling real-time data capture, enhancing autonomous and semi-autonomous driving capabilities while meeting global safety regulations. Embedded electronics and microcontrollers are evolving to support connected vehicle architectures, with CAN FD and Ethernet-based networking enabling faster data transfer within vehicle subsystems.

In manufacturing, Industry 4.0 principles are driving smart factories for automotive components, incorporating AI-driven quality inspection systems, automated assembly lines, and digital twin technologies for product validation and predictive maintenance. The adoption of power electronics components with advanced silicon carbide (SiC) technology in inverters and converters is improving efficiency and thermal performance for electric drivetrains. These technology shifts collectively enhance the reliability, efficiency, and sustainability of components while supporting the evolving demand for electrified and connected mobility within the Automotive Components Market.

• In February 2023, Bosch announced the start of mass production of its silicon carbide power semiconductors at its Reutlingen plant, enhancing EV power electronics with higher efficiency and improved thermal management for inverter applications in electric drivetrains.

• In August 2023, ZF introduced its new generation 800V electric drive platform featuring a modular e-motor and power electronics system, enabling increased power density and faster charging capabilities for electric vehicle OEM partners across Europe and Asia.

• In March 2024, Continental launched its high-performance brake-by-wire system for volume production, reducing system weight by up to 5 kilograms while enhancing braking response times in electric and hybrid vehicles within the Automotive Components Market.

• In May 2024, Denso unveiled a next-generation LiDAR sensor with enhanced resolution and detection range designed for integration into ADAS and autonomous driving systems, improving vehicle safety and navigation precision across varying weather conditions.

The Automotive Components Market Report comprehensively covers key segments, including powertrain, chassis, suspension, braking systems, electronics, lighting, and advanced safety systems across internal combustion engine, hybrid, and electric vehicles. It analyzes the impact of lightweight material integration, such as aluminum alloys and composites, and the adoption of advanced sensor technologies, including LiDAR, radar, and camera modules, across vehicle components to address regulatory compliance and consumer safety requirements.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, examining region-specific production trends, technology adoption rates, and regulatory frameworks influencing the demand for automotive components. The report evaluates applications across passenger cars, light commercial vehicles, heavy commercial vehicles, and electric vehicles, identifying opportunities in the replacement and aftermarket sectors, particularly for electrification and connectivity upgrades.

The Automotive Components Market Report further outlines the emergence of Industry 4.0 practices, smart manufacturing, and AI-enabled quality control, emphasizing their influence on operational efficiency and component consistency. Additionally, it highlights niche segments, including EV battery management systems, power electronics, and ADAS-integrated braking systems, offering insight into future growth trajectories for stakeholders seeking to align investment and production strategies within the evolving Automotive Components Market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1530811.32 Million |

|

Market Revenue in 2032 |

USD 2111190.88 Million |

|

CAGR (2025 - 2032) |

4.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Robert Bosch GmbH, Denso Corporation, Magna International Inc., ZF Friedrichshafen AG, Continental AG, Aisin Corporation, Valeo SA, BorgWarner Inc., Hyundai Mobis Co., Ltd., Aptiv PLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |