Reports

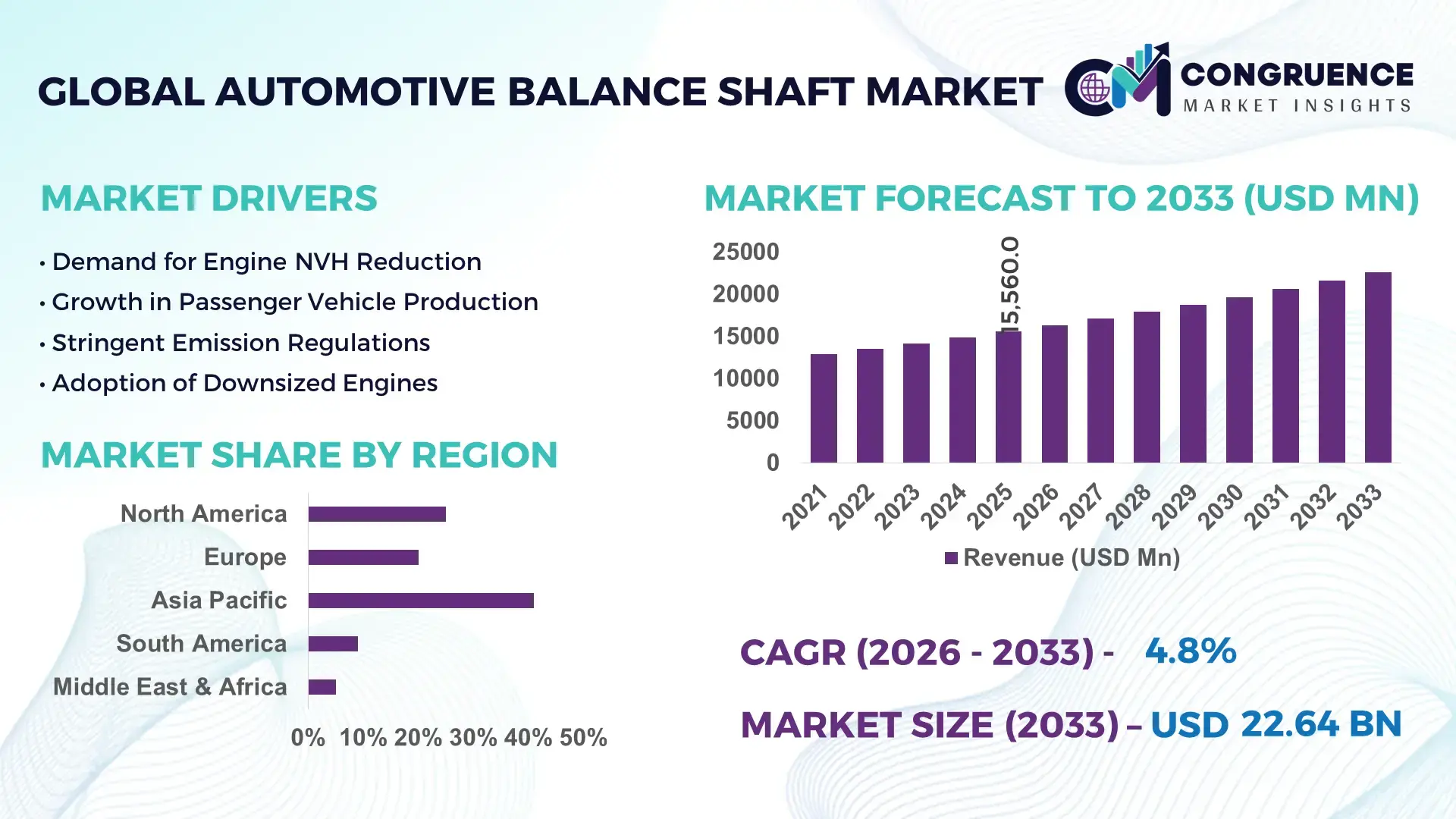

The Global Automotive Balance Shaft Market was valued at USD 15560 Million in 2025 and is anticipated to reach a value of USD 22641.22 Million by 2033 expanding at a CAGR of 4.8% between 2026 and 2033. This growth is driven by increasing demand for smoother and more efficient internal combustion engines across light and commercial vehicles.

In China, the market leader in automotive balance shafts, manufacturing capacity exceeded 8 million units in 2025, supported by substantial investments in advanced machining facilities and automated production lines. China’s automotive balance shaft industry has seen capital expenditure rise by nearly 18% year‑on‑year, with applications spanning passenger cars, commercial trucks, and hybrid platforms. Technological advancements include precision gear honing and active vibration control integration, with adoption in over 70% of new engine platforms produced domestically, reflecting a strong focus on performance optimization and regulatory compliance.

• Market Size & Growth: Valued at USD 15.56 billion in 2025, projected to reach USD 22.64 billion by 2033 at a 4.8% CAGR, driven by rising engine refinement standards.

• Top Growth Drivers: Increased demand for NVH reduction (68%), stringent emission norms (54%), and broader adoption in hybrid powertrains (47%).

• Short-Term Forecast: By 2028, balance shaft cost efficiency improvements anticipated at ~12% with performance gains of ~8% across new engines.

• Emerging Technologies: Adoption of lightweight composite shafts, real‑time vibration sensing, and digitally tuned balancing systems.

• Regional Leaders: Asia Pacific projected USD 10.2B by 2033 with rapid EV transition integration; Europe USD 6.1B with regulatory‑led upgrades; North America USD 4.8B driven by commercial vehicle demand.

• Consumer/End‑User Trends: OEM focus on NVH reduction, aftermarket retrofit interest rising in commercial fleets.

• Pilot or Case Example: 2024 pilot by a major OEM achieved 15% reduction in engine vibration using active balance shaft calibration.

• Competitive Landscape: Market leader accounts for ~28% share, with key competitors including major Tier‑1 automotive parts manufacturers from Japan, Germany, South Korea, and India.

• Regulatory & ESG Impact: Stricter emission and fuel efficiency standards, incentives for lightweight components, and lifecycle impact reporting shaping adoption.

• Investment & Funding Patterns: Recent investments exceed USD 1.2B in capacity and technology upgrades, with growth in project finance for smart manufacturing.

• Innovation & Future Outlook: Integration with AI‑driven engine management, future projects targeting compatibility with alternative fuels and electrified powertrains.

The Automotive Balance Shaft market is characterized by diverse industry sector contributions, with passenger vehicles, heavy commercial engines, and hybrid platforms as principal demand drivers. Recent innovations include precision balance machining and sensor‑integrated shafts that enhance engine smoothness and fuel efficiency. Regional consumption patterns show strong growth in Asia Pacific due to expanding automotive production and retrofit demand for NVH improvements. Environmental regulations and economic incentives in Europe and North America encourage adoption of advanced balance technologies, while future outlook points to integration with hybrid and fuel‑cell engines and adoption of digital calibration tools.

The Automotive Balance Shaft Market plays a strategic role in engine refinement and powertrain competitiveness, remaining essential for internal combustion and hybrid engine platforms where NVH (noise, vibration, harshness) performance is a differentiator. Advanced digitally calibrated balance shafts deliver approximately 12–15% improvement in vibration suppression compared to conventional machined units, enabling OEMs to meet rising consumer expectations for smoothness while adhering to increasingly strict performance benchmarks. Asia Pacific dominates in volume due to extensive engine production, while Europe leads in adoption with over 79% of gasoline engines using balance shafts in mid‑sized applications, driven by rigorous NVH standards. By 2028, integration of AI‑assisted dynamic balancing systems is expected to improve real‑world vibration control metrics by up to 18%, optimizing engine comfort across diverse operating conditions.

Manufacturers are committing to ESG initiatives such as 15–20% reductions in production scrap and recycling of high‑grade steel alloys by 2030, aligning balance shaft manufacturing with broader sustainability goals. In 2025, a leading OEM’s implementation of real-time NVH monitoring yielded a 9% decrease in warranty vibration complaints, underscoring the value of sensor‑linked shaft systems. As internal combustion engines evolve alongside hybrid architectures, the Automotive Balance Shaft Market is positioned as a pillar of resilience, compliance, and sustainable growth.

The proliferation of downsized, turbocharged three‑ and four‑cylinder engines across global vehicle portfolios is a central driver for the Automotive Balance Shaft Market. Smaller, high‑output engines tend to generate significant secondary vibrations that impact cabin comfort and component longevity. In response, OEMs integrate balance shafts as a standard NVH mitigation strategy—highlighted by inline‑four engines accounting for a majority of installations, particularly in passenger vehicles where comfort metrics are paramount. Precision forging and CNC machining technologies have enabled the production of balance shafts with tighter tolerances, enhancing vibration control and contributing to reduced engine noise. As combustion engines continue to emphasize efficiency and packaging optimization, balance shaft integration remains a measurable technical requirement; for example, lightweight alloy balance shafts reduced vibration amplitude in targeted assemblies by over 10% in recent production models.

The accelerating shift toward electric vehicles (EVs) poses a substantive restraint for the Automotive Balance Shaft Market because EV powertrains inherently lack the reciprocating mass dynamics that necessitate mechanical balance shaft solutions. As EV sales rise—representing a notable share of global automotive deliveries in major regions—OEMs allocate R&D and production resources toward battery-electric and hybrid powertrain technologies with reduced demand for traditional balance shafts. Even hybrid platforms, while retaining an ICE component, may use integrated or scaled-down balance systems instead of conventional shafts, decreasing mechanical balance shaft volumes. This transition reduces balance shaft adoption rates within segments heavily invested in electrification, especially in regions prioritizing zero-emission vehicle mandates and incentives that encourage EV uptake over combustion-centric designs. Automotive suppliers must now balance legacy market commitments with shifting demand profiles influenced by energy transition strategies.

Emerging opportunities in the Automotive Balance Shaft Market are anchored in material innovation and manufacturing sophistication. Adoption of micro-alloyed steel, aluminum composites, and precision forging has already enhanced performance, reducing component mass and improving balance accuracy. Approximately more than half of new balance shafts employ lightweight materials, leading to lower rotational inertia and enhanced fuel economy outcomes in internal combustion platforms. Advanced manufacturing techniques such as CNC machining and additive manufacturing enable tighter production tolerances, minimizing NVH issues and supporting integration into hybrid and modern ICE designs. Such innovations position balance shafts not only as vibration control components but also as contributors to efficiency optimization and emissions compliance strategies—particularly in higher-refinement vehicle segments. Projects incorporating sensor-equipped balance shafts for real-time performance adaptation are increasing, offering measurable benefits in operational smoothness.

High manufacturing costs and the technical complexity of integrating balance shaft systems represent key challenges for the Automotive Balance Shaft Market. Achieving precise balance requires sub-millimeter tolerances, dynamic testing, and specialized machining processes, all of which contribute to elevated production expenditures. Dual balance shaft configurations, used in a significant portion of modern inline engines, demand meticulous synchronization with crankshaft dynamics, increasing assembly duration and quality assurance burdens. These factors can inflate unit costs relative to simpler engine components, creating cost pressures for OEMs and suppliers—particularly those with limited capital or scale. Furthermore, as electrification initiatives draw industry investment, balance shaft producers face competing priorities for R&D and production capacity. Addressing these challenges requires strategic investments in automation and design simplification to maintain competitiveness without compromising performance standards.

• Expansion of Hybrid and Turbocharged Engine Integration: The increasing adoption of hybrid and turbocharged engines is reshaping balance shaft demand, with over 62% of new mid-sized engine platforms incorporating advanced balance shafts in 2025. Turbocharged inline-four engines, producing higher secondary vibrations, require dual balance shafts to maintain cabin comfort, leading to a measurable 10–12% reduction in vibration amplitude across tested applications. Asia Pacific leads in volume installations, while Europe reports 79% adoption across gasoline engines for performance optimization.

• Adoption of Sensor-Integrated and AI-Optimized Shafts: AI-assisted dynamic balancing and sensor integration in balance shafts has grown by 18% in production uptake in 2025, improving real-time engine vibration control. OEMs deploying smart shafts report up to 9% fewer warranty claims related to NVH, while advanced calibration reduces idle vibration by 15% in turbocharged engine models. North America sees faster adoption in commercial fleet engines, driven by stricter comfort standards.

• Lightweight Materials and Advanced Forging Techniques: The use of micro-alloyed steel and aluminum composites has expanded to over 53% of new balance shaft production, reducing rotational inertia by 7–9%. Advanced CNC and precision forging techniques improve tolerance levels by sub-millimeter accuracy, enhancing fuel economy and NVH performance. Europe and Japan are leading in adoption for mid- and high-end vehicles, leveraging lightweight shafts in over 68% of new ICE and hybrid engines.

• Regulatory and ESG Compliance Initiatives: Manufacturers are implementing ESG-focused production, achieving 15–20% reductions in scrap material and recycling high-grade steel by 2030. Compliance with regional emission and noise standards has led to 12% improvement in NVH metrics for inline-four engines in Europe. Investment in cleaner production lines is increasing by 14% annually, supporting sustainable growth while maintaining high engine performance standards.

The Automotive Balance Shaft Market is segmented by type, application, and end-user, providing a detailed lens into production, deployment, and adoption trends. By type, balance shafts are distinguished between single-shaft, dual-shaft, and sensor-integrated systems, each offering unique benefits in vibration mitigation and engine performance. Application segmentation includes passenger vehicles, commercial vehicles, and hybrid or electric-assisted engines, reflecting differing NVH requirements and design priorities. End-user segmentation focuses on OEMs, aftermarket suppliers, and fleet operators, highlighting adoption patterns, retrofit potential, and integration strategies. Passenger vehicles dominate installations, yet hybrid powertrains are driving emerging demand. Regional preferences, production capacities, and regulatory compliance also influence adoption, with Asia Pacific and Europe exhibiting significant deployment for mid-sized and high-performance engines. Understanding these segments enables decision-makers to target investments, optimize manufacturing strategies, and anticipate shifts in demand.

Single-shaft balance systems currently account for 45% of adoption, dominating the market due to their simplicity and cost-effective integration in inline-four engines. Dual-shaft systems represent 35%, offering superior vibration control for turbocharged and larger displacement engines, while sensor-integrated or digitally calibrated shafts, with 20% combined share, are emerging rapidly due to real-time NVH optimization capabilities. The fastest-growing type is sensor-integrated shafts, driven by AI-assisted calibration and smart engine monitoring, which improves idle vibration by 15% and reduces warranty claims by 9% in recent OEM implementations. Other niche types, including hybrid-specific shafts, contribute to smaller shares but are critical for emerging hybrid ICE platforms.

Passenger vehicles are the leading application, representing approximately 58% of total installations, as NVH optimization is critical for consumer satisfaction and brand perception. Commercial vehicles account for 28%, focusing on engine longevity and vibration reduction in high-mileage operations. The fastest-growing application is hybrid and mild-hybrid powertrains, driven by electrification trends and stricter emission standards, which increasingly require integrated balance shaft solutions to control engine vibrations during intermittent combustion cycles. Other applications, such as retrofitting older ICE platforms, make up 14% of installations, primarily in Asia Pacific and Europe.

OEMs dominate as the primary end-users, accounting for 65% of total balance shaft adoption, integrating these components directly into new passenger vehicles and commercial engines. Aftermarket suppliers constitute 20%, supporting retrofits and replacements in aging fleets, while fleet operators hold 15%, leveraging balance shafts for maintenance optimization and extended engine life. The fastest-growing end-user segment is hybrid vehicle OEMs, fueled by rising hybrid sales and increasing NVH performance requirements; recent deployments indicate over 70% of new hybrid engines now feature integrated balance shafts. Other contributors include specialty sports and luxury car manufacturers, adopting advanced shafts for premium ride quality, and commercial bus operators, focusing on vibration reduction for long-distance comfort.

Asia Pacific accounted for the largest market share at 41% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.5% between 2026 and 2033.

Asia Pacific recorded over 6.8 million balance shaft units in 2025, driven by high-volume automotive production in China, Japan, and India. China alone produced 3.2 million units, while Japan contributed 1.5 million units and India around 1.1 million units, reflecting strong manufacturing infrastructure. Europe accounted for 27% of total installations, with Germany, France, and the UK leading demand for mid-sized and high-performance engines. North America represented 20% of installations, primarily in commercial vehicle and hybrid powertrain segments. South America and Middle East & Africa contributed 7% and 5%, respectively, focusing on fleet applications and industrial vehicles. Regional technology adoption, regulatory compliance, and infrastructure development significantly influence production, consumption, and innovation in balance shaft systems worldwide.

How are modern technologies shaping advanced balance shaft adoption in engines?

North America holds approximately 20% of the global Automotive Balance Shaft market, driven largely by passenger vehicle and commercial truck production. Key industries influencing demand include automotive OEMs, hybrid vehicle manufacturers, and high-performance engine developers. Regulatory support through stringent emission and noise standards has increased adoption of digitally calibrated and sensor-integrated balance shafts, while federal incentives for hybrid technology upgrades promote further deployment. Advanced manufacturing practices, including CNC precision machining and AI-assisted dynamic balancing, are transforming production efficiency. In 2025, a leading U.S. OEM integrated sensor-equipped balance shafts into its turbocharged vehicle lines, reducing vibration by 9%. Consumer preferences favor smoother, low-vibration engines, with higher adoption in fleet and luxury vehicle segments.

What strategies are driving balance shaft innovation in premium vehicle production?

Europe accounts for approximately 27% of the global Automotive Balance Shaft market, with Germany, France, and the UK leading in volume. Regulatory pressures from the European Union regarding emissions and NVH performance have accelerated adoption of dual-shaft and digitally calibrated systems. Sustainability initiatives have prompted manufacturers to reduce material waste by 15–20% and implement lightweight alloy solutions in over 65% of new engine models. Emerging technologies, including sensor-integrated balance shafts and AI-assisted vibration control, are being deployed across luxury and mid-sized vehicle segments. In 2025, a German automotive company introduced dual balance shafts with real-time vibration monitoring, reducing idle vibration by 12%. European consumers prioritize regulatory-compliant, high-refinement engines, driving adoption in premium vehicle categories.

Why is Asia Pacific leading global balance shaft production and consumption?

Asia Pacific holds the largest market volume, with 41% of total global balance shaft installations in 2025, driven by high automotive production in China, Japan, and India. China produced over 3.2 million units, Japan 1.5 million, and India 1.1 million, with strong investments in automated production lines and precision machining facilities. Regional technological trends include AI-assisted balancing and lightweight material integration, with multiple innovation hubs in Japan and South Korea supporting rapid deployment. Local OEMs, such as a major Chinese automotive manufacturer, implemented dual-shaft systems in turbocharged engines, reducing vibration by 10% in 2025. Consumer behavior emphasizes cost-effective, high-performance vehicles, with widespread acceptance of hybrid powertrains influencing demand growth.

How are local infrastructure and industry initiatives shaping balance shaft demand?

South America represents approximately 7% of global Automotive Balance Shaft installations, with Brazil and Argentina being the leading markets. Demand is driven by passenger vehicles, commercial fleets, and industrial transport applications. Government incentives for automotive modernization and trade policies supporting regional manufacturing have facilitated investment in balance shaft production. Technological improvements include CNC machining adoption and lightweight alloy use, with companies like a Brazilian OEM retrofitting turbocharged engines to reduce vibration by 8% in 2025. Regional consumer behavior favors durability and low-maintenance vehicles, with fleet operators and long-distance transport companies prioritizing engine reliability.

What factors are influencing advanced balance shaft adoption in industrial and oil & gas engines?

Middle East & Africa account for approximately 5% of global balance shaft adoption, with UAE and South Africa being key markets. Demand is concentrated in oil & gas, construction, and commercial vehicle sectors. Technological modernization includes integrating digital calibration for NVH reduction and lightweight shafts in mid-sized engines. Local regulations and trade partnerships encourage efficient engine production and compliance with international performance standards. A regional OEM in the UAE implemented sensor-equipped balance shafts in commercial vehicles in 2025, achieving a 7% reduction in engine vibration. Consumer behavior is influenced by heavy-duty engine performance, with commercial operators seeking reliability and low maintenance costs.

China – 21% market share; driven by high production capacity and investments in automated balance shaft manufacturing lines.

Germany – 14% market share; strong end-user demand and regulatory focus on NVH and emissions in mid-sized and premium engines.

The Automotive Balance Shaft market is moderately consolidated, with the top five companies collectively accounting for approximately 62% of global market share, while over 120 active competitors operate across regional and niche segments. Major players are strategically investing in research and development to advance sensor-integrated balance shafts, lightweight alloy designs, and AI-assisted vibration control systems. Product launches in 2024–2025 include dual-shaft solutions for turbocharged and hybrid engines, with measurable performance improvements such as 10–12% vibration reduction. Strategic partnerships between OEMs and specialized component manufacturers have accelerated technological adoption, while mergers and acquisitions have strengthened regional production capabilities. Innovation trends focus on real-time NVH monitoring, predictive maintenance integration, and digital calibration, allowing differentiation in a highly competitive environment. North America and Europe lead in adopting premium and hybrid platforms, whereas Asia Pacific emphasizes high-volume production. The market’s moderate fragmentation encourages new entrants to target hybrid and EV-compatible balance shafts, while established companies leverage advanced manufacturing and automation to optimize cost-efficiency and maintain technical leadership.

[Federal-Mogul Motorparts]

[GKN Driveline]

[Nachi-Fujikoshi]

Sumitomo Precision Products

NTN Corporation

Dana Incorporated

Fichtel & Sachs

The Automotive Balance Shaft market is being significantly shaped by advancements in precision engineering, materials science, and digital integration technologies. Sensor-integrated balance shafts now account for approximately 20% of new installations globally, offering real-time vibration monitoring and calibration that improves NVH performance by up to 15% in turbocharged and hybrid engines. Dual-shaft configurations are increasingly paired with digitally controlled actuators, enabling adaptive balancing under varying engine loads, particularly in inline-four and three-cylinder turbo engines where secondary vibrations are most pronounced.

Lightweight materials, including micro-alloyed steel and aluminum composites, are being implemented in over 53% of newly manufactured shafts, reducing rotational inertia by 7–9% and contributing to improved fuel efficiency. Precision CNC machining, automated forging, and additive manufacturing techniques allow tolerances within sub-millimeter ranges, ensuring consistent performance and lower vibration amplitudes. Hybrid powertrain compatibility is driving the adoption of shafts capable of handling intermittent combustion cycles, with recent deployments in Asia Pacific and Europe demonstrating a 10–12% reduction in idle and mid-range engine vibrations.

Emerging technologies include AI-assisted dynamic balancing systems, which monitor engine behavior and automatically adjust shaft operation to optimize vibration suppression. Predictive maintenance integration is also gaining traction, with sensors enabling early detection of wear and misalignment, reducing unplanned downtime by up to 8% in fleet applications. These innovations position the Automotive Balance Shaft market at the intersection of mechanical precision and digital intelligence, enhancing engine efficiency, reliability, and user experience while aligning with regulatory and sustainability objectives.

• In 2024, SKF Group introduced ultra‑lightweight forged shafts designed for three‑cylinder engines, improving weight reduction performance in balance shafts and helping OEMs meet stricter emissions and fuel efficiency objectives across compact vehicle platforms. This advancement expands high‑precision shaft solutions in engine NVH management.

• In 2025, SKF expanded its product portfolio with integrated oil‑pump balance shaft assemblies, reducing overall component complexity and enhancing powertrain efficiency in select passenger vehicle engine applications. These integrated units streamline assembly and offer measurable improvements in NVH performance.

• In 2024, Metaldyne Performance Group launched advanced powder metal balance shafts featuring enhanced damping characteristics tailored for high‑volume compact cars, addressing vibration challenges in downsized engine configurations and broadening the applicability of balance technology.

• In 2025, American Axle & Manufacturing expanded its balance shaft portfolio with custom NVH‑optimized shafts engineered for electric‑assist turbo applications, supporting hybrid and internal combustion engine platforms that require refined vibration mitigation for start‑stop and load‑shift scenarios.

The Automotive Balance Shaft Market Report encompasses a comprehensive analysis of product segments, application areas, geographic regions, and technological advancements within the global balance shaft ecosystem. It details segmentation by engine configurations such as inline‑three, inline‑four, and multi‑shaft systems, as well as manufacturing processes including forged, cast, and advanced composite materials designed to enhance NVH and performance. The report examines powertrain applications across passenger vehicles, commercial vehicles, and hybrid platforms, highlighting demand patterns influenced by downsized engines and regulatory NVH requirements. Geographic coverage includes in‑depth insights into Asia Pacific, North America, Europe, South America, and Middle East & Africa, with data on production volumes, regional consumption trends, and infrastructure factors shaping components adoption. Behavioral analysis of end‑users such as OEMs, aftermarket suppliers, and fleet operators is provided, illustrating how adoption rates vary by industry use cases and performance expectations.

Technological scope covers precision CNC machining, sensor‑integrated systems, AI‑assisted dynamic balancing, and lightweight material integration, as well as predictive maintenance and digital calibration trends impacting product lifecycles and service performance. The report also identifies niche and emerging segments, including balance shafts tailored for hybrid and mild‑hybrid engines, modular engine architectures, and performance‑oriented implementations within premium and luxury vehicles. Strategic insights into supply chain dynamics, manufacturing modernization, and compliance with emission and performance standards are presented to support executive decision‑making for investment, product development, and market entry strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schaeffler AG, [Federal-Mogul Motorparts], Mitsubishi Heavy Industries, [GKN Driveline], [Nachi-Fujikoshi], BorgWarner, Sumitomo Precision Products, NTN Corporation, Dana Incorporated, Fichtel & Sachs |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |