Reports

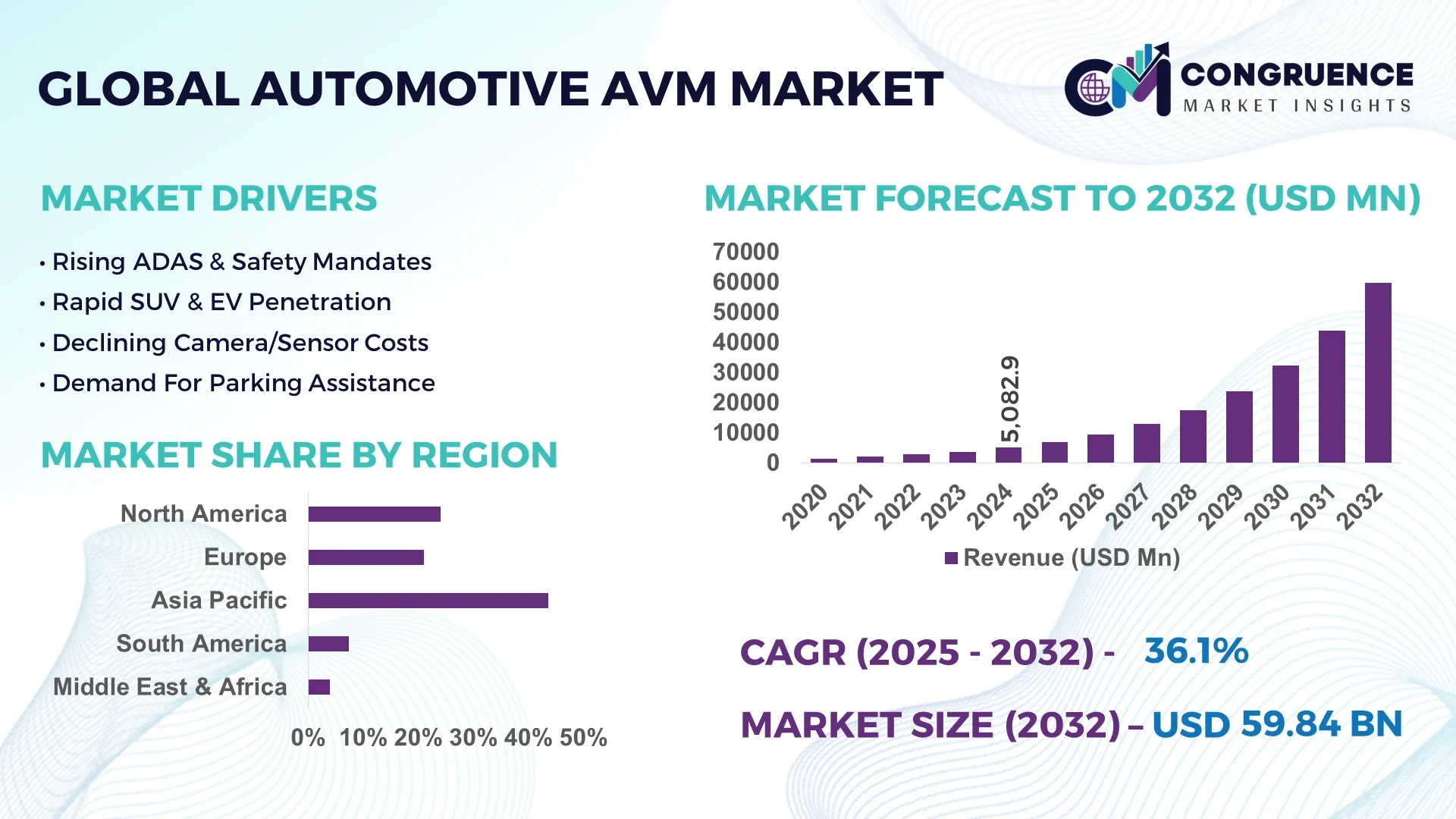

The Global Automotive AVM (Around View Monitoring) Market was valued at USD 5082.92 Million in 2024 and is anticipated to reach a value of USD 59838.24 Million by 2032 expanding at a CAGR of 36.1% between 2025 and 2032.

Japan continues to lead the global Automotive AVM (Around View Monitoring) market with extensive OEM integration in both passenger and commercial vehicles, supported by advanced R&D facilities, high-tech manufacturing infrastructure, and robust government funding in autonomous vehicle technologies.

The Automotive AVM (Around View Monitoring) Market is undergoing rapid evolution, driven by the increasing demand for enhanced driver assistance systems and safety-centric technologies across the automotive sector. The system’s deployment is growing in mid-range and entry-level vehicle segments, moving beyond luxury models. Key sectors including passenger vehicles, electric vehicles (EVs), and commercial fleets are integrating AVM technologies to support lane monitoring, blind spot detection, and parking automation. Noteworthy innovations such as high-definition surround-view cameras, AI-assisted object recognition, and integration with vehicle-to-everything (V2X) communication systems are reshaping the market landscape. Regulatory mandates emphasizing occupant and pedestrian safety, especially in North America and Europe, are pushing OEMs and Tier-1 suppliers toward mandatory AVM implementation. Additionally, rising urbanization, consumer demand for advanced safety, and premium driving experiences are fostering AVM adoption across Asia-Pacific and Latin America. The outlook remains strong with growing investments in AI, sensor fusion, and deep learning to improve real-time imaging and decision-making capabilities of AVM systems.

Artificial Intelligence (AI) is rapidly redefining the capabilities of the Automotive AVM (Around View Monitoring) Market, revolutionizing how modern vehicles perceive and respond to their surrounding environments. Through deep learning algorithms and real-time data analysis, AI enhances the accuracy and responsiveness of 360-degree vision systems, significantly improving driver assistance features and overall vehicle safety. AI-driven image stitching and semantic segmentation technologies enable AVM systems to deliver seamless bird’s-eye views with higher resolution, fewer blind spots, and dynamic object identification.

In the current landscape, AI is being deployed to support predictive analytics in AVM systems, which allows for real-time threat detection and automatic decision-making under complex driving conditions. This is particularly vital for autonomous and semi-autonomous vehicles where human intervention is minimal. AI-enhanced AVM systems can now differentiate between pedestrians, cyclists, and static obstacles, alerting drivers or initiating safety protocols based on situational awareness. Furthermore, AI contributes to adaptive calibration of sensors and cameras, ensuring reliable performance even in harsh weather or lighting conditions.

Vehicle manufacturers are also integrating AI to reduce processing latency, enabling near-instant image processing and faster driver feedback. The combination of AI and AVM technology is becoming a key selling point in competitive automotive markets, especially among electric and autonomous vehicle segments. As edge computing and GPU processing advance, the future of the Automotive AVM (Around View Monitoring) Market is set to deliver more intelligent, context-aware, and predictive safety solutions.

“In 2024, a leading global OEM deployed an AI-powered AVM system capable of real-time pedestrian prediction and trajectory estimation, reducing near-collision events in urban driving environments by 43% during pilot testing across 1,500 vehicles.”

The Automotive AVM (Around View Monitoring) market is shaped by the evolving landscape of intelligent mobility and increasing demand for advanced safety systems in vehicles. As consumer expectations shift toward enhanced driver assistance and accident prevention, AVM systems are gaining traction in both passenger and commercial vehicle segments. Integration of 360-degree camera systems with AI-driven analytics and real-time imaging technologies is driving innovation across product offerings. OEMs and Tier-1 suppliers are heavily investing in research and development to refine image processing, camera calibration, and sensor fusion, while regulatory frameworks such as UNECE regulations and Euro NCAP assessments are compelling automakers to include AVM in standard safety packages. The shift toward electric and autonomous vehicles is further accelerating adoption, especially in premium models where AVM systems support autonomous navigation, parking assist, and collision avoidance. Market dynamics also reflect increasing collaboration between automotive electronics manufacturers and software developers to offer scalable, customizable AVM solutions for different vehicle categories and regional markets.

The rapid proliferation of Advanced Driver Assistance Systems (ADAS) and autonomous driving solutions has significantly boosted demand within the Automotive AVM (Around View Monitoring) market. As manufacturers strive to enhance situational awareness and reduce human error in complex driving environments, AVM systems have emerged as a core component of comprehensive ADAS packages. The technology offers drivers a real-time 360-degree visual representation of the vehicle’s surroundings, enabling more accurate maneuvers and reduced risk of collision. For instance, AVM supports automated parking, lane departure warnings, and object detection—features critical to Level 2 and Level 3 autonomous vehicles. Leading OEMs are now integrating AVM as a standard offering in mid-range vehicles due to rising consumer awareness about safety features. The rise in urban vehicle density, tight parking spaces, and complex traffic scenarios has further necessitated AVM adoption, making it a vital technology in the automotive safety ecosystem.

Despite its safety advantages, the Automotive AVM (Around View Monitoring) market faces restraints due to the high cost of system integration and the complexity involved in calibrating multiple camera modules. AVM systems require a minimum of four high-resolution cameras, precise software alignment, and advanced processing units, all of which add substantial cost to vehicle production—especially in lower-cost and economy vehicles. Additionally, any misalignment in the camera system during vehicle servicing or minor accidents necessitates a recalibration process, which is both time-consuming and costly. These technical intricacies create a barrier to widespread AVM deployment in cost-sensitive markets. Manufacturers also face challenges in ensuring image stitching accuracy, sensor compatibility, and seamless functionality across various lighting and environmental conditions. The need for specialized technicians and expensive diagnostic equipment during maintenance further impacts long-term operational costs for fleet operators and individual users alike.

The ongoing expansion of electric vehicles (EVs) and connected fleet telematics offers a promising growth opportunity for the Automotive AVM (Around View Monitoring) market. As EV manufacturers prioritize lightweight, energy-efficient, and intelligent vehicle systems, AVM technology aligns seamlessly with these goals by providing safety-enhancing features without increasing significant energy consumption. Moreover, fleet operators are increasingly integrating AVM solutions to reduce insurance claims, minimize vehicle downtime, and enhance operational visibility through remote diagnostics. AVM systems, when connected to telematics platforms, allow real-time video streaming, incident recording, and proactive driver coaching. Governments across regions like Europe, China, and North America are also introducing mandates for improved driver safety in EV fleets, encouraging AVM deployment. The opportunity to integrate AVM with emerging technologies such as 5G connectivity, cloud-based analytics, and predictive maintenance platforms further strengthens its value proposition in the electric mobility and fleet management ecosystems.

One of the persistent challenges confronting the Automotive AVM (Around View Monitoring) market is the lack of standardized protocols and interoperability between hardware and software components from different suppliers. As vehicle platforms vary widely across OEMs and regions, ensuring consistent performance of AVM systems becomes technically demanding. Disparities in camera specifications, software algorithms, and system architectures often lead to compatibility issues, especially when integrating AVM into multi-brand or third-party infotainment systems. Furthermore, regional safety regulations and certification standards differ, requiring tailored solutions that increase development timelines and costs. The absence of unified AVM testing benchmarks and calibration guidelines hampers cross-platform deployment and limits after-market adaptability. These standardization challenges not only delay product rollout but also restrict the scalability of AVM systems in high-volume vehicle production. Overcoming this hurdle requires industry-wide collaboration on open protocols and shared validation frameworks to streamline AVM system integration across diverse automotive ecosystems.

• Integration of AVM Systems in Mid-Range Vehicles: Automotive AVM (Around View Monitoring) technology, once limited to premium vehicles, is increasingly being incorporated into mid-range models. OEMs are now standardizing AVM systems in sedans and compact SUVs to enhance safety features and increase vehicle appeal in competitive markets. In 2024, over 47% of new vehicle models launched in Asia included AVM systems as part of their advanced driver assistance packages, marking a significant shift in affordability and accessibility.

• Emergence of AI-Based Predictive Imaging: A major trend shaping the Automotive AVM (Around View Monitoring) market is the adoption of AI-driven predictive imaging. AI-enhanced AVM systems can now interpret driver intent and traffic behavior, offering dynamic viewpoint adjustments and real-time object classification. Over 1.2 million vehicles globally were equipped with AI-assisted AVM modules in 2024, improving detection accuracy in crowded or low-visibility environments by up to 60%.

• Multi-Sensor Fusion for Enhanced Accuracy: Automakers are shifting toward multi-sensor fusion by integrating AVM systems with radar, LiDAR, and ultrasonic sensors. This approach improves image precision and spatial awareness, enabling vehicles to handle complex scenarios such as tight urban navigation. In Europe, over 35% of newly registered autonomous vehicles featured AVM systems calibrated with sensor fusion algorithms as of late 2024.

• Surge in Cloud-Connected AVM Solutions: Cloud integration is rapidly becoming standard in AVM systems, allowing vehicles to store, share, and analyze environmental data in real time. Cloud-connected AVM systems now support fleet management and predictive maintenance applications. North America has seen a 40% increase in cloud-enabled AVM installations since 2023, especially among commercial fleets and delivery vehicles requiring remote diagnostics and live monitoring.

The Automotive AVM (Around View Monitoring) market is segmented based on type, application, and end-user, each contributing uniquely to the market’s development. By type, the market includes 2D and 3D AVM systems, as well as advanced hybrid configurations integrating additional sensors. In terms of application, AVM systems are increasingly used in parking assist, lane departure alerts, and object detection technologies. End-users range from private car owners to commercial vehicle operators and public sector transport authorities. Passenger vehicles dominate due to widespread consumer adoption of ADAS technologies, while commercial fleets are emerging as high-potential segments driven by safety and telematics integration. Each segment plays a distinct role in scaling AVM deployment across regions and use cases, reinforcing its relevance in the evolving mobility landscape.

The Automotive AVM (Around View Monitoring) market encompasses several product types including 2D AVM systems, 3D AVM systems, and hybrid variants that integrate LiDAR or radar-based enhancements. Among these, 3D AVM systems hold the leading position due to their superior depth perception and enhanced visual clarity, making them ideal for luxury and high-end vehicle models. Their ability to provide dynamic perspective switching and real-time environment mapping has made them the go-to solution for vehicles requiring advanced maneuvering support. Meanwhile, hybrid AVM systems that combine camera views with additional sensor data are the fastest-growing segment. These are increasingly adopted in semi-autonomous and electric vehicles, providing a multi-layered safety net. 2D AVM systems, though more affordable, are gradually becoming less favored in premium markets but still hold relevance in budget and mid-segment vehicles in developing regions. The growing push for ADAS integration across all vehicle classes continues to expand the scope of each AVM type.

Automotive AVM (Around View Monitoring) systems are primarily applied in parking assist, blind spot monitoring, lane change support, and object detection. Among these, parking assist is the leading application, driven by urbanization and reduced parking spaces, which demand precise maneuvering support. This segment has matured significantly with systems now offering automatic guidance and obstacle alerts in real time. Object detection is emerging as the fastest-growing application, fueled by advancements in AI and demand for automated threat identification. This application is crucial in low-speed environments and for pedestrian safety, especially in dense traffic areas. Lane change support and blind spot monitoring continue to be essential components in enhancing driver awareness on highways, contributing to accident reduction. AVM systems are increasingly integrated into a single user interface combining multiple functions, which improves driver usability and overall safety. The growing reliance on AVM across these functions signifies its expanding importance within the intelligent mobility ecosystem.

The Automotive AVM (Around View Monitoring) market is largely driven by private vehicle owners, commercial fleet operators, and public transportation agencies. Private passenger car users form the largest end-user group due to increased awareness of safety and convenience features, with a majority of new cars now offering AVM as part of their ADAS packages. Commercial fleets represent the fastest-growing end-user category, especially in logistics and ride-sharing services, where AVM systems are used for real-time monitoring, driver safety, and incident documentation. This segment is benefiting from growing investment in telematics and fleet management technologies. Public transportation systems, particularly in developed nations, are also beginning to adopt AVM systems to enhance passenger safety and assist in operator training. The diverse needs of each end-user segment are shaping product design and deployment strategies, encouraging OEMs to develop flexible, scalable AVM solutions suited for both private and commercial applications.

Asia-Pacific accounted for the largest market share at 43.6% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 39.2% between 2025 and 2032.

The Asia-Pacific region’s dominance in the Automotive AVM (Around View Monitoring) market stems from rapid advancements in vehicle manufacturing hubs like China, Japan, and South Korea. Rising demand for ADAS integration across electric vehicles, combined with strong supply chain capabilities and competitive electronics manufacturing, continues to bolster growth. In contrast, North America is witnessing rapid expansion due to accelerating adoption of semi-autonomous vehicles, heightened consumer safety awareness, and substantial investments from automotive OEMs and tech giants. Increasing regulatory mandates for advanced driver-assistance systems in the U.S. and Canada are further propelling AVM deployment. Across Europe, regulatory alignment and eco-innovation drive consistent AVM integration. South America and the Middle East & Africa show emerging potential, with fleet modernization and governmental push for smart mobility solutions. Regionally diverse dynamics, infrastructural readiness, and tech adaptability shape the competitive AVM landscape globally.

Expanding Vehicle Safety Mandates and Autonomous Mobility Investments

North America held a market share of 24.9% in 2024 within the Automotive AVM (Around View Monitoring) market, driven by increasing adoption in both the luxury and commercial fleet segments. The U.S. automotive industry is pushing AVM adoption through enhanced driver safety standards and the integration of intelligent parking solutions. Recent updates in FMVSS regulations have created a favorable environment for AVM systems as standard features. Automotive OEMs and Tier-1 suppliers are deploying high-definition AVM systems with real-time AI processing capabilities to meet growing consumer expectations. Rapid development in autonomous driving programs—particularly in states like California and Michigan—is creating demand for sensor-fused, cloud-connected AVM platforms. Government incentives supporting EV production further contribute to AVM integration in next-generation vehicle architectures.

Eco-Safe Mobility Policies and Next-Gen Automotive Innovation

Europe accounted for 20.3% of the global Automotive AVM (Around View Monitoring) market in 2024, with major contributions from Germany, the United Kingdom, and France. These nations lead in regulatory compliance and advanced vehicle technologies, where AVM systems support multiple safety and navigation applications. Germany’s emphasis on vehicle digitization and the UK’s aggressive electric vehicle rollout under zero-emission initiatives are driving demand. The European Commission’s Vision Zero strategy is compelling automakers to integrate AVM as a core safety measure in new models. Additionally, partnerships between vehicle manufacturers and AI tech startups across Scandinavia and Benelux are spurring integration of predictive imaging and sensor-based AVM systems into both urban and long-haul vehicle categories.

Mass Production Efficiency and Advanced Sensor Deployment Lead Growth

Asia-Pacific led the global Automotive AVM (Around View Monitoring) market in 2024 with a volume share of 43.6%, supported by strong demand in China, Japan, and South Korea. China’s large-scale automotive production and aggressive push toward connected electric vehicles provide a solid base for AVM integration. Japan continues to pioneer high-end AVM technologies through its globally renowned OEMs and component manufacturers, while South Korea emphasizes AVM as part of its smart mobility strategy. High investments in R&D and manufacturing automation, combined with state-backed initiatives in EV and autonomous vehicle development, are enabling cost-effective scalability of AVM systems. Innovation hubs in Tokyo and Seoul are further advancing camera, radar, and AI integration, accelerating next-generation AVM deployment.

Fleet Modernization and Smart Logistics Fuel Demand Surge

South America contributed 5.8% to the Automotive AVM (Around View Monitoring) market in 2024, with Brazil and Argentina emerging as the primary growth drivers. Demand is driven by fleet operators upgrading to safety-enhanced commercial vehicles, particularly in logistics and urban transport. Brazil’s growing electric bus market and tax incentives for smart mobility solutions are prompting OEMs to integrate AVM as standard. Argentina is witnessing gradual expansion due to increased automotive imports equipped with AVM technology. Investment in road infrastructure modernization and digital logistics platforms across the continent is encouraging broader AVM adoption, especially among regional logistics firms aiming to reduce operational risks and improve driver performance.

Urban Mobility Transformation and Safety Tech Investments Underway

The Middle East & Africa region accounted for 5.4% of the global Automotive AVM (Around View Monitoring) market in 2024. Countries such as the UAE and South Africa are leading growth through urban transport modernization and high-end vehicle demand. The UAE is heavily investing in smart city mobility infrastructure, including AI-enhanced road safety systems that rely on AVM technology. South Africa is gradually adopting AVM in commercial fleets as a safety compliance measure. The region is also witnessing a rise in public-private partnerships aimed at integrating AVM systems in smart transport initiatives. Local governments are endorsing digitization in automotive safety, with new import policies prioritizing AVM-equipped vehicles for public and private sector use.

China – 26.7% market share

High production capacity combined with expansive electric vehicle deployment and local demand for smart safety systems.

Japan – 17.2% market share

Strong AVM-focused R&D, advanced camera sensor technology, and high integration rates among domestic automotive OEMs.

The Automotive AVM (Around View Monitoring) market features a highly competitive landscape with over 25 prominent players actively shaping the global outlook. Leading OEMs and Tier-1 suppliers are heavily investing in AVM systems as demand for advanced driver assistance technologies accelerates. Major participants differentiate themselves through integrated ADAS solutions, seamless UI/UX, and compatibility with electric and autonomous vehicle platforms. Product innovations—such as real-time 3D surround views, AI-powered image stitching, and edge-processing capabilities—are now key competitive parameters. Companies are expanding strategic partnerships with software firms, chipset providers, and cloud service integrators to enhance performance and reduce latency. The competitive environment is further intensified by the entry of agile startups developing niche, modular AVM solutions tailored for commercial fleets and EV platforms. Mergers and acquisitions are also reshaping the ecosystem, with players acquiring firms specializing in imaging sensors, LiDAR fusion, or V2X communication. Regulatory shifts toward mandatory 360° safety systems in passenger and commercial vehicles have further catalyzed innovation cycles and accelerated the deployment of AVM technologies globally.

Continental AG

Magna International Inc.

Valeo SA

Denso Corporation

Hyundai Mobis Co., Ltd.

Gentex Corporation

Ficosa International S.A.

Panasonic Automotive Systems

ZF Friedrichshafen AG

Hitachi Astemo Ltd.

Aptiv PLC

Sony Corporation

The Automotive AVM (Around View Monitoring) market is undergoing a technological transformation driven by innovations in imaging, AI, and sensor fusion. Modern AVM systems utilize multiple ultra-wide-angle cameras—typically four or more—placed around the vehicle to generate a 360-degree bird’s-eye view in real time. These cameras are now increasingly equipped with full HD resolution and HDR capabilities, enhancing visibility under diverse lighting conditions such as low light, fog, or glare.

Emerging advancements include the integration of AI-powered image stitching algorithms that deliver seamless real-time visuals by correcting for lens distortion and camera misalignment. Deep learning models are being employed to detect objects, pedestrians, and lane markings more accurately, supporting higher-level ADAS functions. OEMs are also embedding AVM functionalities within centralized domain controllers that process data from various driver assistance sensors including radar and LiDAR, offering a more synchronized situational awareness system.

Another notable trend is the shift toward 3D AVM systems, which provide more dynamic and interactive displays, especially useful in parking and tight urban driving scenarios. Cloud connectivity is enabling remote firmware updates and diagnostic features, while edge processing ensures minimal latency in critical driving decisions. As automotive architectures transition toward zonal E/E platforms, AVM modules are becoming more modular, scalable, and interoperable with autonomous navigation frameworks.

• In February 2023, Denso Corporation launched an enhanced AVM system integrated with machine learning that improves object recognition and low-light performance, supporting better safety in nighttime and poor weather driving conditions.

• In July 2023, Magna International announced a partnership with a leading EV manufacturer to supply scalable AVM systems with embedded AI-based scene interpretation, aimed at enhancing urban mobility safety.

• In March 2024, Hyundai Mobis unveiled a next-generation AVM solution using solid-state LiDAR integration to provide multi-angle views combined with obstacle detection for autonomous driving applications.

• In May 2024, Valeo introduced its new “Safe Surround View” platform, which leverages 3D mapping and predictive analytics to support trailer maneuvering and smart parking assist for commercial vehicles.

The Automotive AVM (Around View Monitoring) Market Report provides a comprehensive analysis of the global landscape, examining technological, geographical, and application-level factors shaping the market. The report covers a wide range of vehicle categories including passenger cars, light commercial vehicles, and heavy-duty trucks, with detailed insights into both OEM-installed and aftermarket AVM systems. It segments the market by camera type (digital vs analog), system architecture (standalone vs integrated ADAS), display technology (2D vs 3D), and vehicle propulsion type (ICE, hybrid, and electric).

Geographically, the study spans North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, highlighting the varying regulatory environments and consumer adoption patterns influencing regional demand. Applications analyzed include parking assistance, low-speed maneuvering, lane change support, and autonomous navigation integration. The report also explores market penetration in electric and connected vehicle platforms, where AVM systems play a pivotal role in improving driver awareness and reducing collision risks.

Additionally, the study outlines the role of Tier-1 suppliers, software developers, and semiconductor companies in shaping the ecosystem through innovation in sensors, computing chips, and embedded software. The scope also includes coverage of emerging trends such as AVM in fleet management, 5G-enabled AVM data streaming, and AI-powered diagnostics for predictive maintenance in commercial vehicles.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5082.92 Million |

|

Market Revenue in 2032 |

USD 59838.24 Million |

|

CAGR (2025 - 2032) |

36.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Continental AG, Magna International Inc., Valeo SA, Denso Corporation, Hyundai Mobis Co., Ltd., Gentex Corporation, Ficosa International S.A., Panasonic Automotive Systems, ZF Friedrichshafen AG, Hitachi Astemo Ltd., Aptiv PLC, Sony Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |