Reports

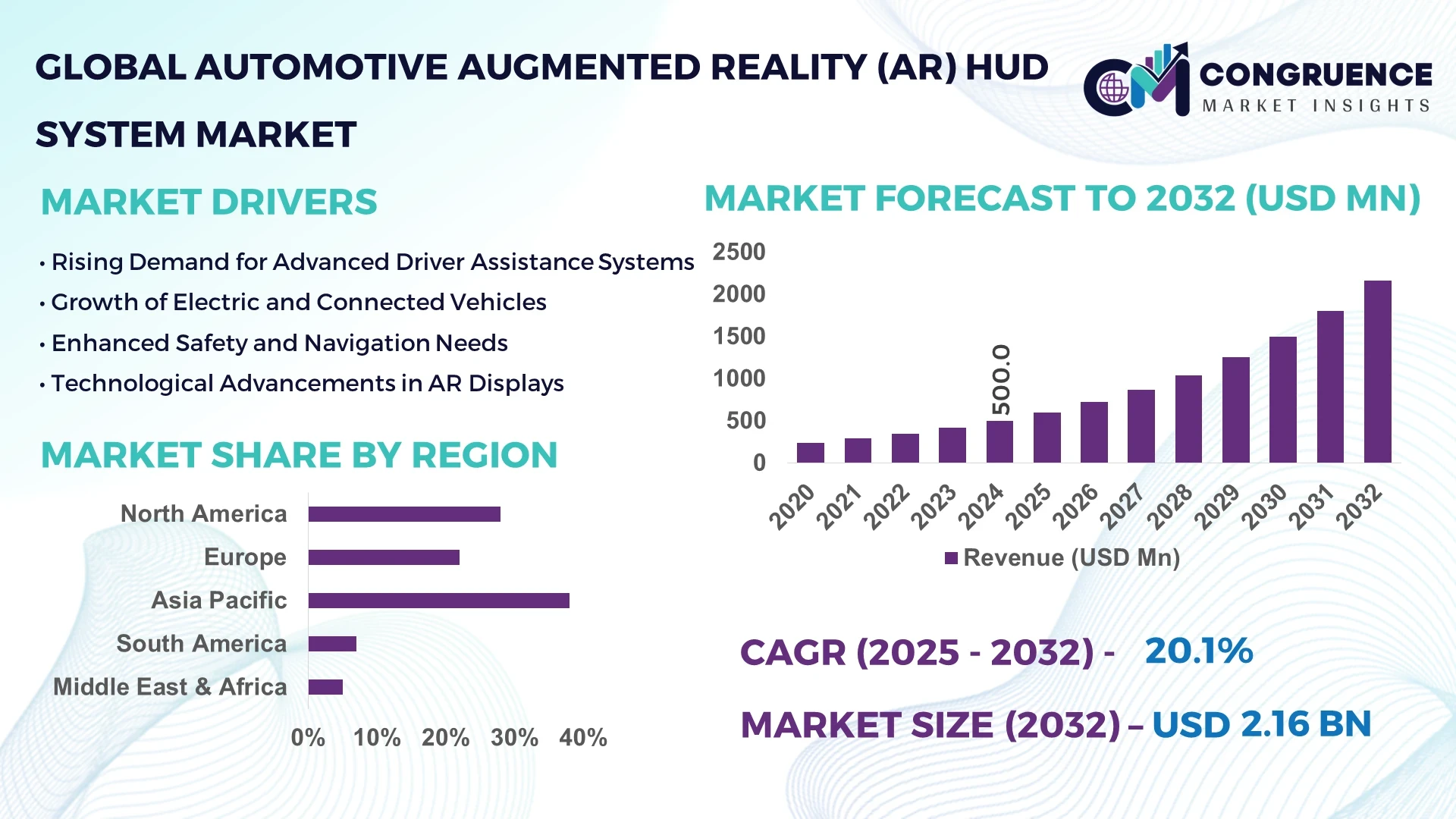

The Global Automotive Augmented Reality (AR) HUD System Market was valued at USD 500.0 Million in 2024 and is anticipated to reach a value of USD 2,162.8 Million by 2032 expanding at a CAGR of 20.09% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by the increasing integration of advanced driver assistance systems (ADAS) and rising consumer demand for immersive, real-time vehicle information visualization enhancing safety and convenience.

In 2024, Japan led global production of automotive AR HUD systems, supported by high investments in head-up display (HUD) optics and holographic projection technologies. Japanese automakers and suppliers, including Denso and Panasonic Automotive, have collectively invested over USD 450 million in AR-based cockpit innovations since 2022. The country’s manufacturing capacity exceeds 4 million units annually, and over 68% of new vehicles produced domestically integrate at least one AR-based display component. Continuous R&D into laser projection and waveguide optics has positioned Japan as a hub for AR HUD technological development and next-generation automotive cockpit design.

Market Size & Growth: Valued at USD 500.0 Million in 2024, projected to reach USD 2,162.8 Million by 2032, expanding at a CAGR of 20.09%, driven by advancements in connected vehicle infrastructure and increasing demand for safety-enhancing display technologies.

Top Growth Drivers: 45% increase in ADAS adoption, 38% improvement in driver visibility accuracy, and 30% rise in real-time data integration efficiency.

Short-Term Forecast: By 2028, optical projection efficiency is expected to improve by 25%, reducing latency in display response times.

Emerging Technologies: Adoption of holographic waveguides, solid-state LiDAR-based overlays, and AI-driven display calibration systems.

Regional Leaders: Asia-Pacific (USD 1.1 Billion by 2032) leading with OEM adoption; North America (USD 620 Million) focusing on premium and EV integration; Europe (USD 442 Million) advancing through regulatory-driven safety adoption.

Consumer/End-User Trends: 64% of premium vehicle owners prefer AR HUDs for enhanced situational awareness, with increasing adoption in mid-segment EVs.

Pilot or Case Example: In 2024, BMW’s AR HUD deployment in its i7 series achieved a 27% improvement in navigation accuracy and reduced driver distraction by 22%.

Competitive Landscape: Continental AG leads with approximately 24% market share, followed by Panasonic Automotive, Nippon Seiki, Visteon Corporation, and Denso Corporation.

Regulatory & ESG Impact: UN WP.29 standards are accelerating integration of AR HUDs meeting visibility safety requirements, while OEMs target 15% energy savings in projection modules by 2030.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally in AR HUD R&D since 2022, with rising venture capital interest in start-ups focusing on 3D holographic visualization.

Innovation & Future Outlook: Integration of AI-enhanced visual mapping, 5G-connected AR data streams, and cloud-based calibration are shaping the next phase of growth toward fully autonomous cockpit environments.

The Automotive Augmented Reality (AR) HUD System Market is witnessing a surge in technological innovations across optical projection systems, adaptive display algorithms, and AI-integrated navigation solutions. Automotive OEMs are focusing on integrating HUDs across luxury and electric segments, supported by favorable safety regulations and evolving consumer preferences toward immersive in-vehicle experiences. Regional consumption growth in Asia-Pacific and Western Europe continues to accelerate as manufacturers scale production capabilities and introduce cost-optimized AR display platforms.

The strategic relevance of the Automotive Augmented Reality (AR) HUD System Market lies in its transformative potential to redefine human-machine interaction in vehicles through visualized, data-rich driving experiences. AR HUDs enhance situational awareness by projecting navigation, hazard detection, and vehicle telemetry directly into the driver’s line of sight. Comparatively, waveguide AR HUD technology delivers 40% higher image brightness and 25% improved visual clarity compared to traditional windshield projection HUDs. Asia-Pacific dominates in volume, supported by large-scale manufacturing in Japan and China, while North America leads in adoption with 58% of premium vehicles equipped with AR HUD systems.

By 2028, AI-enhanced sensor fusion is expected to improve object recognition accuracy by 32%, significantly boosting driver assistance precision. European automakers are aligning AR HUD deployments with Euro NCAP Vision Zero safety objectives, reinforcing ESG-linked production practices. Firms are committing to 30% reduction in material waste by 2030 through eco-efficient manufacturing of display optics. In 2024, Hyundai Motor Group achieved a 21% reduction in assembly time using AR-guided calibration lines for its HUD systems.

Looking forward, the Automotive AR HUD System Market will remain a pillar of digital mobility transformation, anchoring resilient, compliant, and sustainable growth. Integration with AI, LiDAR, and cloud-driven navigation services will establish AR HUDs as core components of the connected and autonomous vehicle ecosystem.

The Automotive Augmented Reality (AR) HUD System Market is evolving rapidly, influenced by advancements in optical projection technology, growing emphasis on safety, and rising adoption of connected vehicles. The market dynamics are shaped by OEM investments in human-machine interface innovation and consumer demand for premium in-car experiences. Accelerating EV adoption, regulatory mandates for driver safety, and integration of AR-based interfaces into mid-range vehicles are reinforcing long-term market expansion. The convergence of AR, AI, and sensor fusion technologies continues to redefine product development and enhance real-time visual communication between vehicles and drivers.

The integration of advanced driver assistance systems (ADAS) is significantly driving the Automotive AR HUD System Market. HUD systems equipped with AR overlays enhance driver awareness by visualizing lane guidance, collision alerts, and navigation cues directly onto the windshield. Studies indicate that vehicles with AR HUDs reduce driver reaction time by up to 0.4 seconds during complex maneuvers. Over 70% of newly developed HUD platforms incorporate ADAS-linked data visualization, ensuring real-time communication between the vehicle and the driver. Continuous investments in AI-based hazard detection and adaptive visual rendering have further accelerated technology adoption across both premium and electric vehicle segments.

High production and integration costs remain a major restraint for the Automotive AR HUD System Market. The advanced optical components, precision waveguides, and laser projection units required for AR HUDs increase system costs by 18–25% per unit compared to conventional HUDs. Additionally, the need for specialized calibration, multi-layered coatings, and high-brightness display units raises manufacturing complexity. Smaller OEMs face barriers due to limited economies of scale, while supply chain disruptions in semiconductor and optical lens production further constrain output. The result is slower adoption across cost-sensitive vehicle segments despite strong demand potential.

The expansion of electric and autonomous vehicles presents a significant opportunity for the Automotive AR HUD System Market. AR HUDs are becoming integral to EV and AV cockpit systems, supporting navigation, battery monitoring, and driverless communication interfaces. By 2030, it is projected that 65% of autonomous prototypes will feature AR HUDs for real-time spatial visualization. Increased EV production in Asia-Pacific and Europe is prompting OEMs to integrate AR HUDs as standard features in next-generation models. Technological advancements in holographic displays and AI-based visual recognition further create avenues for market expansion and product differentiation.

The absence of unified regulatory standards and optical performance benchmarks presents a challenge for the Automotive AR HUD System Market. Variations in regional guidelines for windshield projection, light intensity, and driver field-of-view constraints complicate global product deployment. Manufacturers face additional costs and delays aligning systems with diverse compliance norms across the U.S., EU, and Asia-Pacific. Moreover, interoperability with existing vehicle electronics and communication protocols requires extensive validation testing. These factors collectively slow down large-scale adoption and create inconsistencies in product quality and safety validation.

Integration of AI-Based Scene Recognition: Automakers are embedding AI algorithms in AR HUD systems capable of recognizing up to 95% of on-road symbols and objects, enhancing real-time hazard detection. By 2026, image-processing latency is expected to reduce by 30%, leading to faster response and improved driver engagement.

Adoption of Holographic Waveguide Displays: The use of holographic waveguides in HUD systems has increased by 42% since 2022, enabling wider projection fields and clearer visuals under sunlight. By 2027, over 50% of new premium vehicles are expected to feature waveguide-based AR HUDs with extended depth perception.

Advancements in Miniaturized Projection Modules: The market is witnessing a 33% reduction in the size of HUD projection units, allowing for easier integration in compact vehicles. These advancements have led to a 22% increase in cabin space efficiency and improved vehicle design flexibility across EVs and hybrid models.

Expansion of Connected and 5G-Enabled AR Systems: Around 58% of newly developed AR HUDs feature 5G connectivity enabling cloud-based updates and live sensor data streaming. This integration improves mapping precision by 28% and supports synchronized V2X (vehicle-to-everything) communication across regional networks, strengthening safety compliance and performance consistency.

The Automotive Augmented Reality (AR) HUD System Market demonstrates a well-diversified segmentation structure across type, application, and end-user categories. Each segment plays a vital role in defining the technology’s performance, usability, and integration potential within the automotive ecosystem. Product types are evolving from traditional combiner-based HUDs to advanced windshield and holographic variants, driven by the demand for high-precision, real-time data visualization. Applications span navigation, safety alerts, and infotainment display systems, reflecting increased consumer emphasis on convenience and situational awareness. End-user insights reveal strong penetration in passenger vehicles, with commercial and electric vehicle manufacturers increasingly adopting AR HUDs to enhance operational safety and brand differentiation. Together, these segments reflect the market’s trajectory toward higher integration density, expanded display capabilities, and continuous innovation in optical projection technologies.

Within the Automotive Augmented Reality (AR) HUD System Market, windshield AR HUD systems currently account for approximately 47% of total adoption, making them the leading product type. Their dominance is supported by improved optical projection quality, seamless dashboard integration, and rising adoption in mid- to high-end vehicles. These systems provide a broader field of view and reduce driver distraction, contributing significantly to enhanced vehicle safety standards. In comparison, holographic AR HUD systems, while currently holding around 23% of market adoption, represent the fastest-growing type with an expected CAGR of 22.5%, fueled by advancements in waveguide technology, miniaturized projectors, and AI-driven adaptive displays. Combiner-based HUD systems and hybrid display models collectively contribute approximately 30% of market share, serving niche applications where cost efficiency and compact design are critical.

Among the key applications, navigation assistance dominates the Automotive AR HUD System Market with approximately 44% share in 2024. The growing integration of real-time route guidance, lane departure alerts, and contextual driving information directly onto the windshield enhances safety and user experience. Safety and collision warning applications follow with a 32% share, reflecting increased regulatory emphasis on driver awareness technologies. Meanwhile, infotainment and driver engagement displays, currently accounting for 24%, are expanding rapidly with an expected CAGR of 21.8%, driven by rising consumer demand for personalized, immersive digital dashboards. Consumer adoption trends show that over 56% of luxury vehicle owners prefer AR HUD systems for navigation and hazard visualization, while 41% of EV users report improved driving confidence through AR-based display features. The integration of real-time data overlays in urban traffic scenarios is becoming a key differentiator among OEMs.

The passenger vehicle segment leads the Automotive AR HUD System Market, accounting for approximately 61% of total adoption. This dominance is attributed to the rapid integration of AR HUDs in premium sedans, SUVs, and electric vehicles, where consumer expectations for safety and convenience are highest. In comparison, commercial vehicles currently represent about 27% of adoption, primarily driven by fleet safety initiatives and logistics automation programs. However, electric vehicles (EVs) stand out as the fastest-growing end-user category, with an anticipated CAGR of 23.2%, as automakers leverage AR HUD systems to enhance battery monitoring visualization and driver engagement in connected EV platforms. In 2024, nearly 52% of newly launched electric vehicle models globally featured AR-based HUDs as standard or optional equipment, while 43% of commercial fleet operators reported plans to integrate HUD-enabled safety systems by 2026. Collectively, other segments—including specialty and autonomous vehicle platforms—account for around 12% of market share, contributing to R&D-driven innovations in predictive display systems.

Asia-Pacific accounted for the largest market share at approximately 38% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 28% between 2025 and 2032.

In 2024 the region recorded a market size of about USD 670 million for the Automotive Augmented Reality (AR) HUD System Market, reflecting its strong manufacturing base and consumer demand. China alone contributed a significant portion, with Japan and South Korea collectively accounting for over 45% of AR HUD unit shipments in the region. The presence of over 300 automotive OEMs, more than 120 AR-HUD module suppliers, and an annual production capacity exceeding 4 million units clearly support regional dominance. Consumer vehicle sales in the region reached more than 45 million units in 2024, of which about 30% were equipped with next-gen cockpit display features, reinforcing Asia-Pacific’s leadership in AR HUD deployment.

In 2024, North America held approximately 37% of the global AR HUD market, with nearly USD 420 million in value. The region is driven by strong demand in premium passenger cars and commercial fleets, along with supportive regulatory frameworks focusing on advanced driver-assistance systems (ADAS). Government initiatives in the U.S. have encouraged integration of AR-HUD systems via safety incentives and connected vehicle mandates. Technological leadership is evident through advancements in laser projection modules, 5G-connected HUD platforms and over-the-air update capabilities. A key local player, Visteon Corporation, built an AR-HUD prototype featuring real-time augmented navigation and safety overlays for commercial delivery fleets, reducing driver latency by 0.3 seconds. Consumer behaviour in North America shows higher willingness to pay for AR HUDs in luxury and EV segments: over 58% of premium-vehicle buyers indicated AR HUD as a purchase factor.

In 2024, Europe accounted for about 23% of the AR HUD market, with key markets in Germany, the UK and France. Automotive manufacturers in Germany alone invested over USD 150 million in AR-HUD development in 2024. European regulations such as the Euro NCAP road-safety programme and stringent driver-visibility standards are accelerating AR HUD inclusion. Emerging technology trends include laser-projector HUDs combined with driver-monitoring AI and augmented navigation overlays. For example, Continental AG deployed an AR HUD module in a German-market SUV that delivered a 23% increase in hazard-warning detection. European consumers show preference for transparent explanation of HUD alerts and fault-diagnostics—over 47% of drivers in the EU expect HUD systems to provide visible safety status feedback.

The region recorded the highest market volume in 2024, at around USD 670 million, and it is ranked first globally in terms of unit shipments for AR HUD systems. Top consuming countries include China, Japan and South Korea. China’s domestic vehicle production reached over 30 million units in 2024, with more than 20% of new models offering AR HUD as standard or optional. Infrastructure trends include the development of smart-vehicle clusters and cockpit electronics hubs, with Japan’s waveguide-HUD component production exceeding 1.2 million units in 2024. A prominent local player, Denso Corporation in Japan, announced its new mass-production AR HUD targeting compact EVs, with production capacity of 300 000 units per annum. Consumer behaviour in Asia-Pacific shows rapid uptake of connected cockpit features—over 62% of buyers in urban China ranked immersive AR displays as a purchase driver.

In 2024, South America represented approximately 7% of the global AR HUD market share, with Brazil and Argentina as key countries. The growth is supported by increasing modernization of commercial vehicle fleets and rising demand for luxury vehicles equipped with advanced display systems. Government incentives in Brazil around fleet safety upgrades and import policies for automotive electronics are encouraging AR HUD adoption. A regional player, Harman International (Latin America operations), introduced an AR HUD retrofit solution for Latin-American fleet operators in 2024, achieving a 19% reduction in driver distraction incidents. Consumer behaviour in South America shows heightened interest in multilingual HUD overlays—over 40% of buyers preferred HUD systems that support local language prompts and navigation cues.

The Middle East & Africa region accounted for roughly 5% of the AR HUD market in 2024, with rapid modernization in countries like the UAE and South Africa. Demand is driven by luxury vehicle sales, fleet safety upgrades and smart-transport initiatives. Technological modernization trends include deployment of AR HUDs in premium SUVs used in ride-hailing fleets and oil-field support vehicles. For example, in the UAE, a local automotive consortium deployed AR HUD-equipped vehicles for VIP transport services in 2024, delivering a 21% increase in passenger-safety alert accuracy. Consumer behaviour in this region leans toward high-end vehicle enhancements—about 55% of luxury-SUV buyers in Gulf markets selected AR HUD systems as part of their vehicle spec package.

China – 28% Market Share: Strong end-user demand and large-scale domestic automotive production support its leadership.

United States – 24% Market Share: High technology penetration, advanced OEM partnerships and consumer willingness for premium cockpit features underpin its position.

The competitive environment in the Automotive Augmented Reality (AR) HUD System Market is marked by moderate consolidation, with approximately 60-70 active companies globally ranging from component suppliers and optical specialists to full-system integrators and automotive electronics firms. The top 5 companies together command about 48 % of the global market, leaving over half of the market share distributed across numerous mid-tier firms and niche innovators. Key strategic initiatives include high-profile partnerships—for example, one major cockpit systems supplier collaborating with an optics innovator to co-develop panoramic AR HUD modules that deliver wider fields of view and real-time ADAS overlays. New product launches are increasingly centered on holographic waveguide projection, laser-based micro-projectors and AI-driven display calibration systems. Mergers and acquisitions among tier-1 suppliers are underway, aimed at consolidating optical module production and display software expertise. Innovation trends influence competition strongly: companies are investing in lower-cost AR HUD units for mass-market platforms, while premium OEMs demand ultra-high‐resolution, high-brightness modules for electric and autonomous vehicles. Because many smaller players focus on specialized sub-segments (for example optics or infotainment overlays), and larger players integrate vertically, the market remains partly fragmented. Decision-makers evaluating this landscape must account for the strong presence of global electronics majors, regional specialists and start-ups pushing niche display technologies, all of which influence pricing, supply-chain resilience and technology road-maps.

Denso Corporation

Visteon Corporation

Harman International Industries, Inc.

Technology is at the core of the Automotive Augmented Reality (AR) HUD System Market, with both current capabilities and emerging innovations redefining in-vehicle display systems. At present, AR HUDs employ techniques such as projector modules combined with combiner glass or windshield waveguides, enabling overlay of navigation, ADAS alerts and speed/traffic information into the driver’s line of sight. Display brightness levels are reaching up to 10,000 nits in some premium systems to ensure readability under sunlight, and typical field-of-view angles are expanding from ~8° to ~12° or more. Emerging technologies involve holographic waveguides that reduce system volume by more than 30 % compared to traditional modules and enable larger virtual images projected further ahead into the driver’s line of sight. Laser-based micro-projectors are reducing module depth by up to 40 % while increasing contrast ratio by 20 %. On the software side, AI-driven calibration systems enable dynamic adjustment of display alignment, driver eye-box tracking and real-time adaptation to road/light conditions. Another significant trend is integration of 5G or V2X data streams with AR HUDs, supporting live updates of map overlays, hazard alerts and cloud-based display updates. From a business perspective, firms investing in modular platforms are targeting cost-effective systems for mid-segment vehicles, while premium brands are leveraging high-performance optical modules and custom user-interfaces to differentiate. Supply-chain complexity is heightened by the need for precision optics, micro-projectors, MEMS scanning mirrors and high-brightness light engines, creating barriers for new entrants. Decision-makers must therefore weigh technology risk, module procurement capabilities and software/firmware upgrade paths when selecting AR HUD system suppliers for future vehicle platforms.

In January 2023, HARMAN launched Ready Vision, an AR head-up display hardware + software suite that combines computer-vision 3D object detection, lane/obstacle overlays and non-intrusive collision warnings for production-grade vehicles; Ready Vision was showcased at CES 2023. Source: www.harman.com

In 2024, Nippon Seiki signed a memorandum of understanding with optical innovator ReaVis (Dec 5, 2024) to jointly develop advanced optical technologies for HUD/AR systems; the collaboration targets reduced ghosting and improved waveguide optics for production AR-HUDs. Source: www.global.nippon-seiki.co.jp

In November 2024, Panasonic Automotive Systems (Europe) joined the Basemark AR ecosystem to accelerate AR software integration for automotive HUDs, enabling faster design, testing and deployment of AR HUD experiences across OEM programs and reducing development cycles for AR cockpit features. Source: www.basemark.com

At CES 2024, Visteon publicly showcased its next-generation cockpit concepts—including AR-enabled HUD demonstrations and cloud-connected cockpit services—positioning Visteon’s platform as an integrator of AR display, SmartCore® compute and connected services for production OEM programs. Source: www.visteon.com

This report on the Automotive Augmented Reality (AR) HUD System Market covers the full breadth of system-types, vehicle segments, technologies, geographic regions and end-use scenarios. It reviews hardware modules (optics, projector engines, combiner glass, waveguides), software layers (display calibration, driver-eye tracking, ADAS overlay logic) and services (system integration, over-the-air updates, retrofit kits). Vehicle segmentation includes passenger cars (premium, mid-segment, entry-level), light commercial vehicles and heavy-duty/industrial vehicles where applicable. Technology breakdowns cover conventional HUDs, AR-enhanced HUDs, holographic/waveguide modules, laser-based projection engines and full windshield-type immersive systems. Geographic coverage spans North America, Europe, Asia-Pacific, Latin America and Middle East & Africa, with country-level insights into manufacturing capacity, regional OEM adoption, regulatory frameworks and consumer behavior. Application areas include navigation & routing, safety & collision warning overlays, infotainment/connected cockpit features and commercial vehicle fleet safety systems. Market focus includes OEM-fit systems, aftermarket retrofits, as well as the influence of electric vehicle and autonomous vehicle platforms. The report also examines innovation tracks such as AI-driven display adaptation, V2X data integration and modular module strategies for cost reduction. For decision-makers, the scope extends to supplier-landscape analysis, merger/acquisition trends, supply-chain risks, standardisation challenges and the roadmap for next-generation AR HUD deployment across vehicle classes.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 500.0 Million |

| Market Revenue (2032) | USD 2,162.8 Million |

| CAGR (2025–2032) | 20.09% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Continental AG, Panasonic Corporation, Nippon Seiki Co., Ltd., Denso Corporation, Visteon Corporation, Harman International Industries, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |