Reports

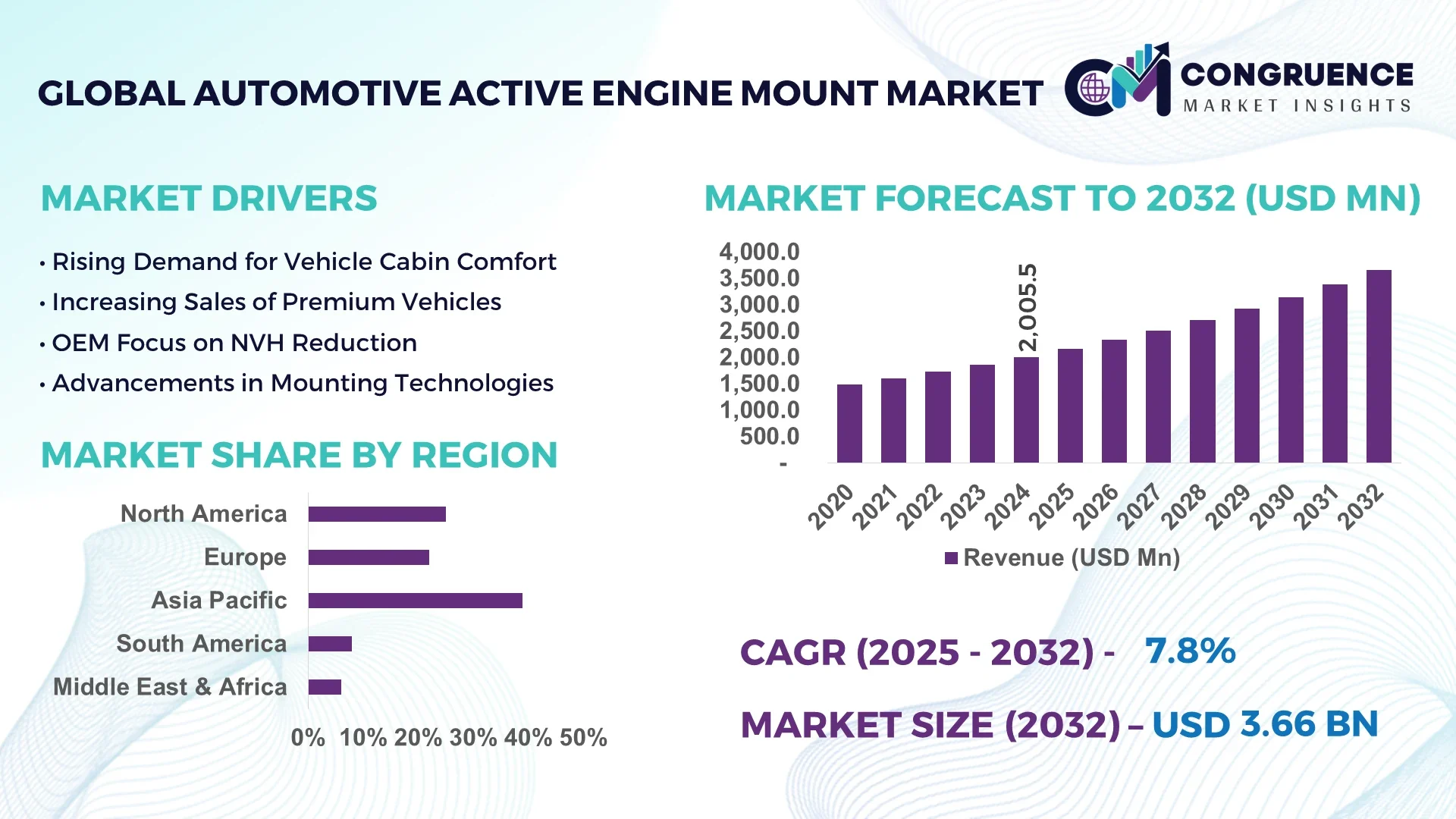

The Global Automotive Active Engine Mount Market was valued at USD 2,005.5 Million in 2024 and is anticipated to reach a value of USD 2,932.6 Million by 2032, expanding at a CAGR of 7.8% between 2025 and 2032.

The automotive active engine mount market is integral to reducing vibrations and noise within vehicle engines, improving overall ride comfort and operational efficiency. The market is predominantly led by North America, driven by robust automotive production and technological advancements. The United States, being one of the largest automotive manufacturers, plays a crucial role in the dominance of this market, with numerous automotive OEMs and suppliers operating within the region.

The growing demand for luxury, electric, and hybrid vehicles, combined with increasing consumer preferences for quieter and smoother driving experiences, is pushing the growth of the automotive active engine mount market. Manufacturers are focusing on developing innovative engine mounts equipped with advanced materials, such as elastomers and metals, to offer superior noise, vibration, and harshness (NVH) control. Additionally, technological advancements in sensor-based mounts that can actively adjust to engine vibrations are gaining popularity. The continuous trend toward enhancing vehicle comfort, along with stringent noise regulations and emission standards, supports the growing adoption of active engine mounts across the global automotive industry.

Artificial Intelligence (AI) is revolutionizing the automotive active engine mount market by optimizing engine mount performance, reducing wear and tear, and enhancing vibration control. AI algorithms are now being integrated with active engine mounts to monitor engine behavior in real time and adapt to varying vibration frequencies. AI-driven systems can predict and adjust the characteristics of the engine mounts to reduce noise and vibrations efficiently, leading to better driving comfort and improved engine performance. These AI-enhanced systems also enable more precise control over the engine's NVH (Noise, Vibration, Harshness) levels, which is a key demand from both consumers and manufacturers.

The application of AI in the automotive active engine mount market is not limited to just improving NVH performance. AI also helps in the design and production processes by leveraging machine learning and predictive maintenance. By using AI-driven simulations, manufacturers can optimize the material composition and structure of engine mounts, which leads to cost savings and extended product lifecycles. AI also plays a significant role in the automation of production lines, resulting in more consistent quality and reducing human error. With these advancements, the automotive active engine mount market is expected to see a more streamlined manufacturing process, ensuring higher performance and durability in active engine mounts.

“In 2024, a leading automotive supplier announced the integration of AI-based active engine mounts in their new electric vehicle models, improving NVH control by 40% compared to previous models. This development was recognized as a significant step in reducing engine vibrations and enhancing overall vehicle comfort.”

The automotive active engine mount market is experiencing a dynamic shift due to several factors that are shaping the industry’s growth trajectory. Innovations in engine mount technology, driven by advancements in materials science, smart sensor technology, and AI integration, are providing new opportunities. Rising consumer expectations for enhanced driving comfort and reduced noise, vibration, and harshness (NVH) levels are driving the demand for high-performance active engine mounts. Furthermore, the trend towards electric vehicles (EVs) and hybrid vehicles, which require specialized engine mounts to handle different engine vibrations, is fueling market growth. Additionally, stricter environmental regulations and noise control measures in the automotive sector are propelling the adoption of advanced active engine mounts, further strengthening the market's expansion.

The rising popularity of electric and hybrid vehicles is one of the primary drivers for the automotive active engine mount market. With electric vehicles (EVs) gaining significant market share, particularly in developed regions, the demand for advanced engine mount systems has surged. These vehicles have different vibration characteristics compared to traditional combustion engine vehicles, requiring specialized active engine mounts. Furthermore, the increasing environmental consciousness among consumers and government regulations mandating lower emissions are pushing automakers to invest in electric and hybrid vehicle production, further driving the demand for engine mount systems that offer better vibration and noise control.

The high manufacturing costs of active engine mounts pose a restraint to the growth of the market. Active engine mounts, which incorporate advanced materials and complex components such as sensors and actuators, tend to be more expensive than conventional passive engine mounts. The integration of smart technologies, while beneficial for NVH reduction, adds to the overall cost of production. Moreover, the necessity for highly skilled labor to design, test, and produce these components contributes to increased manufacturing expenses. These higher costs can be a significant barrier, particularly for automakers in price-sensitive regions, potentially limiting the widespread adoption of advanced engine mount systems.

The development of sensor-based active engine mounts presents significant growth opportunities for the market. These mounts, equipped with real-time vibration and noise sensors, can adapt their characteristics to actively cancel out engine vibrations, offering superior NVH control. The rise of AI and machine learning technologies also presents opportunities for optimizing the performance and design of these sensor-based systems. By incorporating real-time data, manufacturers can improve product longevity, reduce wear and tear, and enhance vehicle comfort. As demand for quieter, smoother driving experiences increases, sensor-based active engine mounts will become more mainstream, presenting significant opportunities for market players.

One of the primary challenges faced by the automotive active engine mount market is the complexity of integrating these advanced mounts into existing vehicle designs. Many vehicles, especially older models, were not designed to accommodate the sophisticated technology involved in active engine mounts. Retrofitting these vehicles with modern engine mounts can be a difficult and costly process. Additionally, ensuring that these mounts are compatible with various vehicle types, from traditional internal combustion engine (ICE) vehicles to electric and hybrid models, adds another layer of complexity. Overcoming these integration challenges requires significant research, development, and testing, which can slow down the adoption of active engine mount systems.

• Increase in Demand for Quieter and Smoother Driving Experiences: The demand for enhanced driving comfort is driving the adoption of automotive active engine mounts. Consumers are increasingly seeking vehicles with reduced noise, vibration, and harshness (NVH) levels, prompting automakers to invest in advanced engine mount technologies. Active engine mounts that dynamically adjust to engine vibrations are becoming a preferred choice in high-end and electric vehicles, especially in markets like North America and Europe. This trend is pushing the development of smarter, more efficient engine mounts with improved vibration control capabilities, leading to higher adoption across various vehicle segments.

• Integration of AI and Smart Technology in Engine Mounts: Another key trend in the automotive active engine mount market is the integration of artificial intelligence (AI) and smart sensor technology. These systems allow engine mounts to actively respond to real-time vibrations, enhancing comfort and reducing engine noise. AI-enabled mounts are becoming more common in electric and hybrid vehicles, which experience different vibration profiles compared to traditional vehicles. This trend is contributing to the development of more sophisticated and adaptive engine mount systems, enhancing their performance and increasing their appeal to automakers and consumers alike.

• Shift Towards Electric and Hybrid Vehicles: The increasing market share of electric and hybrid vehicles is shaping the automotive active engine mount market. Unlike traditional combustion engines, electric and hybrid powertrains produce unique vibration characteristics, which require specialized engine mounts to manage NVH. This trend is leading to the development of active engine mounts tailored specifically for electric vehicles (EVs) and hybrids, with higher demand for low-maintenance, lightweight, and efficient engine mounts in these vehicle categories.

• Focus on Sustainability and Regulatory Compliance: Governments worldwide are implementing stricter regulations regarding vehicle noise emissions and overall environmental impact. To comply with these regulations, automakers are investing in advanced engine mount technologies that can reduce noise pollution while maintaining optimal engine performance. This growing emphasis on sustainability and environmental responsibility is spurring the demand for more efficient, eco-friendly engine mounts in the automotive industry, particularly in markets like Europe, where regulatory frameworks for noise pollution are more stringent.

The automotive active engine mount market is segmented based on type, application, and end-user insights. By type, the market is categorized into passive mounts, active mounts, and semi-active mounts. Active mounts are gaining popularity due to their ability to adapt in real time, offering superior noise and vibration control. In terms of application, the market is divided into passenger cars, light commercial vehicles, and heavy commercial vehicles, with passenger cars being the largest segment. As for end-user insights, the market includes automotive OEMs and aftermarket services, with automotive OEMs contributing significantly to market growth due to the increasing demand for high-performance engine mounts in new vehicles.

The automotive active engine mount market is primarily categorized into three types: passive mounts, active mounts, and semi-active mounts. Active engine mounts are the leading segment due to their ability to adjust to engine vibrations in real time, offering superior noise, vibration, and harshness (NVH) control. This has become increasingly important in premium and electric vehicles, where NVH control is a top priority. Active mounts are particularly popular in electric vehicles (EVs), which experience unique vibration profiles compared to traditional combustion engines. Semi-active mounts are also gaining traction due to their ability to combine the benefits of passive and active mounts, providing a balanced performance at a lower cost. Passive mounts, while still widely used, are less favored in high-end models due to their inability to actively control vibrations.

The automotive active engine mount market is segmented into passenger cars, light commercial vehicles, and heavy commercial vehicles. Passenger cars dominate the market, driven by consumer demand for quieter, more comfortable rides, particularly in luxury and electric vehicles. The rise of electric vehicles, which require advanced NVH control, is further propelling this segment’s growth. Light commercial vehicles are the second-largest segment, driven by the need for improved comfort and performance in vehicles used for commercial transportation. Heavy commercial vehicles, while a smaller segment, are growing due to increasing demand for higher durability and comfort in long-haul trucks. The passenger car segment is not only the largest but also the fastest-growing due to the increasing popularity of electric and hybrid vehicles, which demand specialized engine mount solutions.

The automotive active engine mount market can be analyzed based on end-user insights, which include automotive original equipment manufacturers (OEMs) and aftermarket services. OEMs dominate the market, as they are the primary drivers of the demand for advanced engine mounts in newly produced vehicles. The growing preference for electric vehicles and the need for stringent noise control in premium cars contribute to OEMs’ significant share of the market. Aftermarket services, though a smaller segment, are witnessing growth due to increased demand for replacements and upgrades in older vehicles, particularly in markets with aging vehicle fleets. The OEM segment is expected to remain dominant in the foreseeable future, while the aftermarket segment is growing steadily due to increasing vehicle longevity and the need for maintenance and customization.

Asia-Pacific accounted for the largest market share at 39% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

The Asia-Pacific region holds a dominant share in the automotive active engine mount market, primarily due to the robust automotive manufacturing industry in countries like China, Japan, and South Korea. These countries are home to leading automotive manufacturers, which are heavily investing in advanced engine mount technologies to enhance vehicle performance and comfort. In addition, the growing adoption of electric vehicles (EVs) in the region is further driving demand for specialized engine mounts. The region's dominance is complemented by its expanding automotive production capacity and increasing consumer demand for high-performance vehicles, particularly in emerging economies like India and China.

Powering Comfort and Performance: North America's Push for Advanced Engine Mount Solutions

North America is a significant market for automotive active engine mounts, particularly driven by the increasing demand for electric vehicles (EVs) and the automotive industry's focus on reducing noise, vibration, and harshness (NVH) levels. The United States, being one of the largest automotive markets, leads in technological advancements and vehicle production. With major automakers focusing on high-performance and luxury vehicles, there is a growing need for advanced engine mounts. As consumer preferences shift towards quieter, more efficient driving experiences, manufacturers in North America are increasingly adopting active engine mount systems. The market is also driven by stringent regulations regarding vehicle noise emissions, encouraging automakers to invest in NVH-reducing technologies.

Sustainability Meets Innovation: Europe's Leading Role in Eco-Friendly Active Engine Mounts

Europe has emerged as a major market for automotive active engine mounts, with the region accounting for a substantial share in global automotive production. The increasing trend of environmental consciousness, coupled with a surge in demand for electric and hybrid vehicles, is driving the growth of advanced NVH technologies. Countries like Germany, France, and the UK are leading in automotive manufacturing, with a strong emphasis on reducing engine noise and vibration in their electric vehicle models. Regulatory frameworks in Europe are also pushing for innovations in noise reduction, leading to the adoption of active engine mounts in new vehicle models. The region is expected to witness steady growth, with increasing consumer demand for comfort and performance in both traditional and electric vehicles.

Driving Future Mobility: Asia-Pacific's Surge in Electric and Hybrid Vehicle Mounts

Asia-Pacific remains the dominant region in the automotive active engine mount market due to the sheer scale of automotive production in countries like China, Japan, and South Korea. The automotive industry in these countries is transitioning toward higher performance standards, particularly in the electric vehicle (EV) sector. As more consumers in the region opt for electric and hybrid vehicles, the demand for specialized engine mounts that can handle the unique vibrations of electric drivetrains is rising. Additionally, the expanding automotive manufacturing capacity in countries like China, which is one of the largest automotive markets globally, continues to drive the demand for advanced engine mount technologies. With significant investments in research and development, Asia-Pacific is poised to maintain its position as the largest and most influential market for automotive active engine mounts.

Emerging Markets, Evolving Needs: South America's Growing Demand for Advanced Engine Mounts

The South America automotive active engine mount market is witnessing gradual growth, particularly in Brazil and Argentina, where vehicle production is expanding. As the region's automotive industry focuses more on improving vehicle comfort and performance, the demand for engine mounts that reduce noise and vibration is increasing. The growth of the electric vehicle sector in South America, while in the early stages, is expected to drive further demand for active engine mounts. Moreover, the rise of global automotive manufacturers setting up production facilities in countries like Brazil is contributing to the expansion of the automotive active engine mount market. Despite its relatively smaller market size compared to other regions, South America is poised for steady growth in the coming years as demand for advanced vehicle technologies continues to rise.

Enhancing Vehicle Comfort: The Middle East & Africa’s Shift Towards Cutting-Edge Mount Technologies

The Middle East & Africa automotive active engine mount market is emerging as an important region, primarily driven by increased automotive manufacturing in countries like South Africa and the UAE. The region is seeing growth in both traditional vehicles and electric vehicles, with a rising emphasis on improving driving comfort and reducing NVH levels. The demand for luxury and high-performance vehicles in the Middle East, particularly in countries like Saudi Arabia and the UAE, is also contributing to the growth of advanced engine mount technologies. While the market size in the region is still small compared to others, the growth potential is significant, driven by investments in automotive manufacturing and the increasing adoption of electric vehicles.

China holds the largest market share at 23% due to its position as the world’s largest automotive manufacturer, driving demand for active engine mounts in both traditional and electric vehicles.

United States holds the second-largest share at 18%, driven by the strong presence of major automakers and the growing demand for high-performance and electric vehicles with advanced NVH solutions.

The automotive active engine mount market is characterized by the presence of a mix of global and regional players, each focusing on technological innovations and strategic partnerships to gain a competitive edge. The market is moderately consolidated with a few key companies holding significant market shares. Key players are investing heavily in research and development to cater to the growing demand for advanced engine mount solutions, especially those designed to reduce noise, vibration, and harshness (NVH) in vehicles. Leading companies are also capitalizing on the increasing adoption of electric vehicles (EVs) by offering specialized engine mounts for electric drivetrains. The competition is further intensified by the constant need for product innovation, with companies introducing active engine mounts equipped with advanced sensors and control systems to improve vehicle performance. Strategic acquisitions and collaborations are also key strategies used by these companies to expand their market presence and diversify their product portfolios. As the market evolves, the focus on sustainability and eco-friendly solutions is driving further competition among industry players.

Boge Rubber & Plastics Group

Continental AG

ZF Friedrichshafen AG

Trelleborg AB

Hutchinson S.A.

ElringKlinger AG

KYB Corporation

Mubea

Schaeffler Technologies AG & Co. KG

Magna International Inc.

Technological advancements in the automotive active engine mount market are primarily driven by the need for improved performance, comfort, and noise reduction. Active engine mounts, which incorporate sensors and electronic control units (ECUs), play a vital role in reducing vibrations and noise, thereby enhancing the driving experience. These systems continuously adjust the engine mount stiffness in real-time, depending on various factors like engine speed, load, and road conditions. The increasing use of electric vehicles (EVs) has further spurred the demand for active engine mounts, as these vehicles require specific NVH solutions to handle the unique characteristics of electric drivetrains. The integration of advanced materials such as lightweight composites is also helping reduce the overall weight of the engine mounts, contributing to improved fuel efficiency and vehicle performance. Additionally, developments in wireless technology and smart sensors have made it possible to design more efficient and cost-effective active engine mounts. These innovations are contributing to the overall growth and adoption of advanced engine mount systems across various vehicle segments. With growing emphasis on vehicle comfort, performance, and energy efficiency, the automotive active engine mount market is expected to continue benefiting from these technological advancements.

In June 2024, Hutchinson S.A. unveiled a magnetorheological (MR) fluid-based engine mount, enabling real-time stiffness adjustments with a reaction time of less than 1 millisecond. This innovation significantly enhances ride comfort in performance vehicles by providing instantaneous vibration control.

In May 2024, BOGE Rubber & Plastics Group introduced a lightweight, polymer-based active engine mount that is 30% lighter than traditional designs. This development aims to improve fuel efficiency in electric and hybrid vehicles by reducing overall vehicle weight.

In April 2024, ZF Friedrichshafen AG launched an electronic engine mount system integrating active noise cancellation technology. This system reduces in-cabin vibrations by up to 60%, enhancing passenger comfort in electric and hybrid vehicles.

In March 2024, Vibracoustic developed a hydraulically controlled adaptive engine mount, enhancing damping performance by 40%. This mount is specifically designed for hybrid vehicles, addressing the unique vibration profiles of electric powertrains.

The automotive active engine mount market report provides an in-depth analysis of the current and future trends shaping the industry. This report covers various types of active engine mounts, including those designed for conventional internal combustion engine (ICE) vehicles and those tailored for electric and hybrid vehicles. It explores advancements in materials, such as lightweight composites and advanced elastomers, which contribute to improved vehicle performance and NVH (noise, vibration, and harshness) reduction. The report also highlights the growing demand for engine mounts equipped with real-time adaptive features, utilizing sensors and electronic control systems to adjust stiffness based on driving conditions.

Key segments of the report include market dynamics, such as drivers, restraints, opportunities, and challenges affecting market growth. It also explores regional insights, covering North America, Europe, Asia-Pacific, and other significant markets, providing a clear understanding of geographical trends. Special emphasis is placed on emerging technologies such as magnetorheological fluids and hydraulic systems that offer better damping performance and noise reduction, particularly in electric vehicles.

Moreover, the report analyzes the impact of automotive electrification on the active engine mount market, identifying the shift in demand toward components suited for electric drivetrains. The scope of the report also includes detailed competitive analysis, highlighting key players in the market and their technological innovations. This comprehensive outlook aids stakeholders in making informed decisions in a rapidly evolving automotive landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2,005.5 Million |

|

Market Revenue in 2032 |

USD 2,932.6 Million |

|

CAGR (2025 - 2032) |

7.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Boge Rubber & Plastics Group, Continental AG, ZF Friedrichshafen AG, Trelleborg AB, Hutchinson S.A., ElringKlinger AG, KYB Corporation, Mubea, Schaeffler Technologies AG & Co. KG, Magna International Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |