Reports

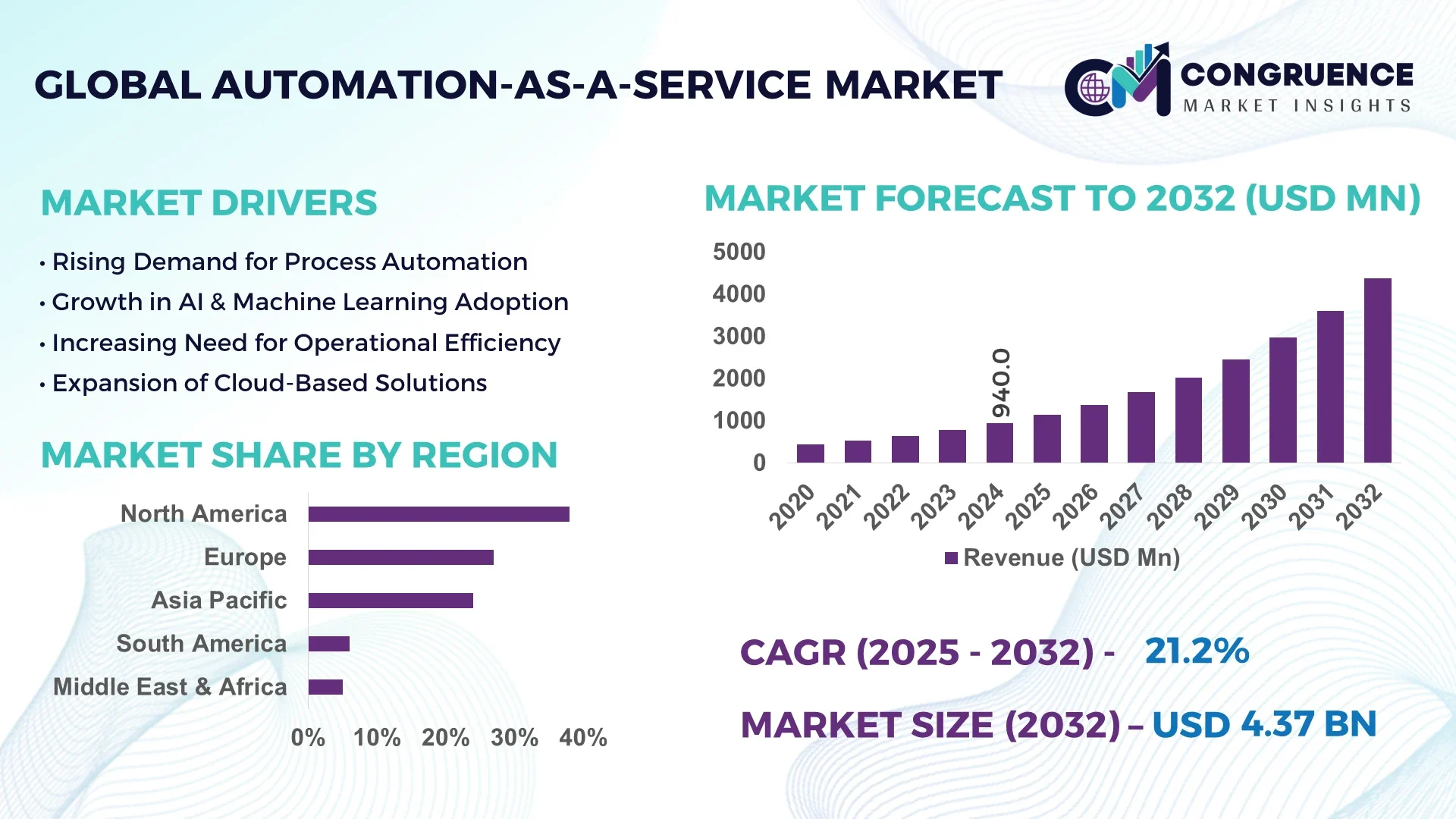

The Global Automation-as-a-Service Market was valued at USD 940.0 Million in 2024 and is anticipated to reach a value of USD 4,373.8 Million by 2032, expanding at a CAGR of 21.19% between 2025 and 2032. This growth is driven by the accelerating adoption of AI-enabled automation platforms that streamline complex workflows across industries.

The United States leads the global Automation-as-a-Service market, supported by large-scale investments from Fortune 500 enterprises, cutting-edge technology providers, and a thriving ecosystem of cloud service vendors. In 2024, over 67% of U.S. enterprises reported integrating automation platforms into IT service management and financial operations, while 43% of large manufacturers deployed automation tools to enhance predictive maintenance. The country also benefits from advanced R&D infrastructure, with annual investments exceeding USD 18 billion in AI and automation innovation.

Market Size & Growth: Valued at USD 940.0 Million in 2024 and projected to reach USD 4,373.8 Million by 2032, growing at a CAGR of 21.19%; rapid enterprise automation adoption drives growth.

Top Growth Drivers: 62% adoption of cloud-native automation, 48% process efficiency improvement, 39% reduction in manual workloads.

Short-Term Forecast: By 2028, enterprises are expected to achieve 32% cost reduction in operational processes through automation services.

Emerging Technologies: AI-driven orchestration and low-code automation platforms are reshaping enterprise workflows.

Regional Leaders: North America projected at USD 1,560.0 Million by 2032, Europe at USD 1,210.0 Million, Asia Pacific at USD 1,345.0 Million; APAC shows rapid adoption in manufacturing.

Consumer/End-User Trends: BFSI and healthcare sectors show highest adoption rates, with 56% of banks automating compliance and 41% of hospitals automating patient data workflows.

Pilot or Case Example: In 2024, a Japanese telecom pilot achieved 44% reduction in service downtime via automation integration.

Competitive Landscape: IBM leads with ~14% market share, followed by Microsoft, Google Cloud, UiPath, and Automation Anywhere.

Regulatory & ESG Impact: Increasing compliance requirements and ESG incentives drive automation in energy-intensive industries.

Investment & Funding Patterns: Over USD 3.2 Billion invested in automation-as-a-service start-ups globally in the last 2 years.

Innovation & Future Outlook: Integration of automation with generative AI, IoT-enabled processes, and adaptive learning platforms will define next-generation solutions.

The Automation-as-a-Service market is transforming critical industries such as manufacturing, BFSI, and healthcare, driven by rapid AI integration, shifting regulatory frameworks, and regional digitalization programs. Cloud-first strategies, energy-efficient automation, and predictive analytics are further accelerating its global adoption and shaping future growth trajectories.

The Automation-as-a-Service Market is strategically relevant as it enables enterprises to achieve measurable efficiency, compliance, and scalability. The shift toward digital-first business operations is amplified by quantifiable improvements. For instance, cloud-native automation delivers 40% faster deployment compared to legacy on-premises models, while low-code AI-driven orchestration reduces development timelines by 28%.

From a regional standpoint, North America dominates in volume, powered by widespread adoption across BFSI and healthcare, while Asia Pacific leads in enterprise adoption with 61% of firms deploying automation tools by 2024. This divergence highlights both technological maturity and emerging adoption behaviors. By 2027, AI-powered automation is expected to cut operational cycle times by 35%, supporting global competitiveness.

Regulatory and ESG frameworks also add weight to the strategic importance of the sector. European firms are targeting a 25% reduction in carbon intensity by 2030 through automation-driven energy monitoring and resource optimization. Compliance frameworks in Asia Pacific emphasize data integrity, ensuring enterprises maintain 99.9% accuracy rates in automated reporting.

Micro-scenarios further demonstrate impact. In 2024, a German automotive manufacturer achieved 37% improvement in assembly-line efficiency by deploying cloud-based automation. Similarly, India’s IT sector realized a 29% reduction in ticket resolution times using AI-powered service automation.

Looking forward, the Automation-as-a-Service Market is set to become a cornerstone of resilience, compliance, and sustainability. By aligning ESG targets, regulatory mandates, and productivity gains, the sector will reinforce its role as a long-term enabler of industrial transformation.

The Automation-as-a-Service Market is experiencing rapid transformation driven by technological innovation, demand for real-time analytics, and increasing enterprise focus on operational efficiency. Cloud-native architectures, integration of AI with automation workflows, and the scalability of subscription-based delivery models are reshaping industry behavior. Consumer preference for digitalized, secure, and cost-efficient solutions is further accelerating adoption. At the same time, competitive pressures are spurring innovation in predictive analytics, IT operations, and customer service applications. Governments and regulators are emphasizing compliance, security, and ESG integration, driving firms to adopt automation solutions capable of delivering consistent, auditable results.

Digital transformation initiatives are fueling the need for scalable automation services. Enterprises across BFSI, healthcare, and manufacturing are increasingly adopting automation to streamline critical processes. In 2024, over 60% of BFSI firms automated compliance workflows, while 46% of healthcare providers integrated automated clinical data processing to improve accuracy. Digital-first strategies are creating demand for flexible, cloud-based platforms that reduce IT complexity and deliver measurable efficiency gains across global enterprises.

Despite its benefits, the integration of automation into existing legacy systems remains a significant barrier. Many enterprises face difficulties in aligning cloud-based automation with outdated IT architectures, causing implementation delays. In 2024, surveys revealed that 34% of firms reported cost overruns due to integration challenges. Security concerns linked to hybrid environments also pose risks, as sensitive data handling requires advanced compliance controls. These factors slow adoption rates and increase the cost of transition for enterprises worldwide.

The growing application of AI-enabled decision intelligence provides significant opportunities. By 2026, enterprises deploying AI-powered automation are expected to achieve 31% improvement in operational agility, enabling faster decision-making in dynamic environments. Industries such as retail and logistics are using intelligent automation to optimize supply chains, while manufacturing leverages it for predictive maintenance. Expansion into SMEs, driven by affordable subscription models, further widens the opportunity for long-term adoption across regions.

The shortage of skilled automation professionals is a major challenge. In 2024, the global demand-supply gap for RPA and AI automation specialists exceeded 22%, leading to project delays and reliance on external vendors. This talent scarcity increases costs and slows innovation cycles. Enterprises are forced to invest heavily in training and certification programs, yet many struggle to scale automation projects due to the limited availability of qualified personnel.

Expansion of AI-Driven Automation: In 2024, 59% of enterprises integrated AI into automation workflows, enhancing predictive analytics and cutting response times by 33%. The shift toward cognitive automation allows enterprises to handle complex tasks beyond rule-based processes, unlocking advanced use cases in financial compliance and healthcare diagnostics.

Growth in Low-Code Automation Platforms: Low-code and no-code tools accounted for 42% of new automation deployments in 2024, reducing development cycles by 28%. These platforms are enabling non-technical staff to build automation workflows, accelerating enterprise-wide adoption and reducing IT dependency.

Rising Focus on Cross-Industry Use Cases: Cross-sector adoption is accelerating, with manufacturing, BFSI, and telecom collectively representing 54% of automation deployments in 2024. Manufacturing saw a 37% boost in predictive maintenance efficiency, while telecom achieved a 44% reduction in downtime via automation services.

Surge in ESG-Oriented Automation Initiatives: In 2024, 29% of global enterprises deployed automation solutions for energy management, achieving up to 18% reduction in power consumption. ESG compliance is increasingly integrated into automation frameworks, ensuring organizations meet environmental and governance commitments.

The Automation-as-a-Service Market is segmented by type, application, and end-user, each offering unique insights into adoption behavior and industry priorities. Types reflect the underlying service models ranging from robotic process automation to advanced AI-driven orchestration, catering to varied enterprise needs. Applications span critical areas such as IT operations, human resources, finance, supply chain, and customer support, highlighting where organizations deploy automation to achieve efficiency. End-user perspectives reveal the breadth of industry uptake, with BFSI, healthcare, retail, manufacturing, and IT/telecom shaping the adoption landscape. This segmentation provides a detailed view into the functional and sectoral roles driving market expansion, underscoring both current demand and future opportunities for innovation.

Among the various types, Robotic Process Automation (RPA) currently leads the market with 41% adoption, supported by its ability to automate repetitive, rules-based tasks across financial operations, IT workflows, and HR functions. However, Artificial Intelligence (AI)-driven automation platforms are the fastest-growing segment, projected at a CAGR of 23.2%, owing to their integration with predictive analytics, natural language processing, and decision intelligence. Other categories such as workflow automation, analytics-driven services, and intelligent document processing collectively contribute 34% share, often deployed in niche use cases where accuracy and compliance are critical.

The IT process automation segment leads with 39% adoption, fueled by demand for efficiency in incident management, network monitoring, and service desk automation. By contrast, customer support automation is the fastest-growing application, forecasted to expand at a CAGR of 24.1%, as enterprises deploy chatbots and AI assistants to handle high call volumes and improve customer experience. Other areas such as finance, supply chain, and HR automation collectively account for 36% of total applications, serving as essential operational pillars in large organizations. In terms of adoption statistics, in 2024, more than 44% of global enterprises piloted automation tools in customer service platforms, while 42% of hospitals in the U.S. tested AI-based clinical workflow systems to streamline radiology and records management.

The Banking, Financial Services, and Insurance (BFSI) sector dominates with 33% share, driven by compliance automation, fraud detection, and risk management applications. Meanwhile, the healthcare sector is the fastest-growing end-user, projected at a CAGR of 22.8%, as hospitals adopt AI-powered automation for diagnostics, patient records, and telemedicine integration. Other industries including retail, IT & telecom, and manufacturing collectively represent 38%, with growing adoption for supply chain optimization, inventory management, and customer personalization. Consumer adoption trends reinforce this landscape: in 2024, over 58% of retailers reported deploying automation platforms to personalize customer engagement, while 61% of Gen Z consumers expressed greater satisfaction with brands offering AI-driven customer service.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 23.5% between 2025 and 2032.

The regional distribution of the Automation-as-a-Service market shows clear patterns of maturity in developed economies and accelerated adoption in emerging regions. Europe captured 27% of the market in 2024, driven by strong regulatory frameworks and digital transformation agendas, while Asia-Pacific followed closely with 24% market share, supported by large-scale adoption in China, India, and Japan. South America accounted for 6% of the global market, while the Middle East & Africa contributed around 5% in 2024. Collectively, these regions show significant differences in demand, with North America and Europe being early adopters, while Asia-Pacific leads in scaling, particularly across e-commerce, BFSI, and manufacturing sectors. Government initiatives, local players, and sectoral digitalization trends are shaping each region uniquely, making regional strategies crucial for companies seeking expansion.

North America held the largest share of the Automation-as-a-Service market in 2024, accounting for 38% of the global volume. The region’s dominance is attributed to strong adoption in healthcare, banking & finance, and manufacturing sectors. Key industries such as insurance, telecom, and retail are also embracing cloud-based automation solutions. Regulatory frameworks encouraging digital compliance, coupled with government initiatives promoting AI integration, are further supporting adoption. Technological advances in intelligent process automation and predictive analytics have fueled enterprise-level demand. A notable player is UiPath USA, which continues to expand its automation platforms in healthcare systems. Consumer behavior in this region is characterized by higher enterprise adoption in healthcare and finance, with businesses prioritizing operational efficiency and customer personalization.

Europe accounted for 27% of the global Automation-as-a-Service market in 2024, with major contributions from Germany, the UK, and France. The European Union’s strong focus on data protection (GDPR) and sustainability initiatives has created a favorable environment for automation tools that enhance compliance. Sectors such as automotive manufacturing, retail, and BFSI are leading adopters. Local innovation hubs in Germany and France have fostered partnerships between startups and enterprises to integrate advanced automation technologies. Blue Prism, a UK-based player, has played a pivotal role by providing automation solutions tailored to European regulatory environments. Regional behavior is shaped by regulatory pressure, leading to higher demand for explainable and transparent automation systems, particularly in finance and healthcare.

Asia-Pacific represented 24% of the market share in 2024, ranking as the second-largest region by consumption volume. Countries such as China, India, and Japan are at the forefront of adoption, driven by rapid industrialization, strong digital infrastructure, and booming e-commerce activity. Manufacturing-led economies are integrating automation tools to enhance supply chain visibility and cost efficiency. Regional tech hubs in Bangalore, Tokyo, and Shenzhen have emerged as global innovation leaders, advancing AI-powered automation. A notable example is Automation Anywhere’s partnerships in India, which target banking and telecom enterprises. Consumer behavior in this region highlights a preference for automation linked to mobile platforms, e-commerce ecosystems, and AI-powered applications, making it the fastest-scaling region.

South America accounted for 6% of the global market share in 2024, with Brazil and Argentina serving as the dominant markets. Government initiatives to promote digital banking, automation in energy utilities, and modernization of public infrastructure are accelerating adoption. The growing role of automation in call centers, telecom operations, and logistics is significant in this region. Brazil, in particular, has witnessed strong investments in cloud-based automation to enhance retail and e-commerce operations. A local example includes TOTVS (Brazil), which has integrated automation services to support enterprise clients. Consumer behavior in this region is shaped by the demand for media, entertainment, and language-localized automation services, especially in customer engagement platforms.

The Middle East & Africa represented 5% of the global Automation-as-a-Service market in 2024, with countries such as the UAE, Saudi Arabia, and South Africa driving growth. Strong demand comes from the oil & gas sector, construction, and public services seeking efficiency gains. Government-led initiatives under smart city projects in the UAE and Saudi Vision 2030 are accelerating automation adoption. Local modernization trends include investments in AI-powered automation and cloud infrastructure to streamline services. A regional example is Injazat (UAE), which has integrated automation solutions within smart infrastructure projects. Consumer behavior trends highlight growing acceptance of automation in government services, retail, and financial platforms, reflecting a shift toward digital-first solutions.

United States – 32% Market Share: Strong adoption in healthcare, banking, and retail, supported by advanced technology ecosystems and enterprise-scale investments.

China – 14% Market Share: High end-user demand from e-commerce, telecom, and manufacturing sectors, combined with strong government push for digital transformation.

The Automation-as-a-Service Market exhibits a moderately fragmented competitive environment, with over 85 active global competitors ranging from established IT giants to emerging specialized startups. The top five companies—IBM, Microsoft, UiPath, Google Cloud, and Automation Anywhere—collectively account for approximately 62% of the market share, underscoring the presence of dominant players alongside numerous niche providers. Strategic initiatives are driving competition, including partnerships for AI-powered automation, product launches of low-code platforms, acquisitions to expand geographic presence, and joint ventures to develop industry-specific solutions. Innovation trends focus on intelligent process orchestration, cloud-native RPA, predictive analytics integration, and multi-modal AI-driven automation platforms. Market positioning varies: some firms concentrate on enterprise-scale BFSI and healthcare solutions, while others target mid-market sectors such as retail and manufacturing. Regional expansion and localized services remain key differentiators, as companies tailor offerings to regulatory frameworks and industry standards. This dynamic competitive landscape ensures continuous technological advancement, higher customer value, and enhanced process efficiency for end-users globally.

Google Cloud

Automation Anywhere

Blue Prism

Pegasystems

ServiceNow

WorkFusion

Nintex

The Automation-as-a-Service Market is increasingly driven by advanced AI, machine learning, and robotic process automation technologies, which allow enterprises to automate complex workflows across finance, healthcare, IT, and manufacturing. Intelligent process orchestration enables the seamless integration of multiple automation tools, improving operational efficiency. By 2024, over 48% of enterprises globally implemented AI-driven automation for IT operations, while 36% adopted natural language processing (NLP) tools for customer support and document management. Emerging technologies include low-code/no-code platforms that empower business users to develop automation workflows without extensive coding skills, enhancing scalability and agility. Predictive analytics and cognitive AI are transforming predictive maintenance in manufacturing and automated compliance in BFSI.

Cloud-native automation frameworks are facilitating rapid deployment, with 65% of enterprises migrating automation workloads to multi-cloud environments in 2024. Additionally, integration with IoT and real-time data platforms is driving smart automation in logistics and energy sectors. Automation-as-a-Service solutions are also leveraging advanced cybersecurity protocols, ensuring data protection and regulatory compliance while supporting enterprise digital transformation initiatives.

In March 2024, UiPath launched its AI Center 2.0, enhancing integration with predictive analytics and NLP, enabling over 250 enterprise clients to optimize workflow efficiency by up to 38%. Source: www.uipath.com

In August 2023, Microsoft introduced the Power Automate Desktop Cloud Integration, allowing organizations to automate cross-cloud workflows with real-time monitoring for 400+ enterprise processes. Source: www.microsoft.com

In November 2023, Automation Anywhere expanded its Bot Store in Asia-Pacific, increasing accessible automation scripts by 32%, targeting sectors such as BFSI, healthcare, and manufacturing. Source: www.automationanywhere.com

In February 2024, IBM enhanced its Cloud Pak for Automation with AI-driven decision-making tools, supporting over 150 enterprise implementations for predictive maintenance, compliance reporting, and supply chain optimization. Source: www.ibm.com

The scope of the Automation-as-a-Service Market Report encompasses a comprehensive analysis of types, applications, technologies, and geographic regions, providing insights tailored for enterprise decision-makers and investors. The report examines major service types, including RPA, AI-driven automation platforms, workflow automation, and intelligent document processing, highlighting adoption patterns across industries such as BFSI, healthcare, manufacturing, IT/telecom, and retail. Geographic analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, emphasizing market size distribution, sectoral trends, and regional consumer behaviors. Technology insights focus on AI integration, predictive analytics, NLP, low-code platforms, and cloud-native solutions, while emerging technologies such as IoT-enabled automation and cognitive AI are evaluated for enterprise impact. Additionally, the report identifies niche segments, including government automation, e-commerce optimization, and ESG-driven automation solutions.

Overall, the report provides a holistic view of market dynamics, competition, investment patterns, and innovation trends, enabling stakeholders to formulate strategic growth initiatives, optimize resource allocation, and prioritize market entry opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 940.0 Million |

| Market Revenue (2032) | USD 4,373.8 Million |

| CAGR (2025–2032) | 21.19% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | IBM, Microsoft, UiPath, Google Cloud, Automation Anywhere, Blue Prism, Pegasystems, ServiceNow, WorkFusion, Nintex |

| Customization & Pricing | Available on Request (10% Customization is Free) |