Reports

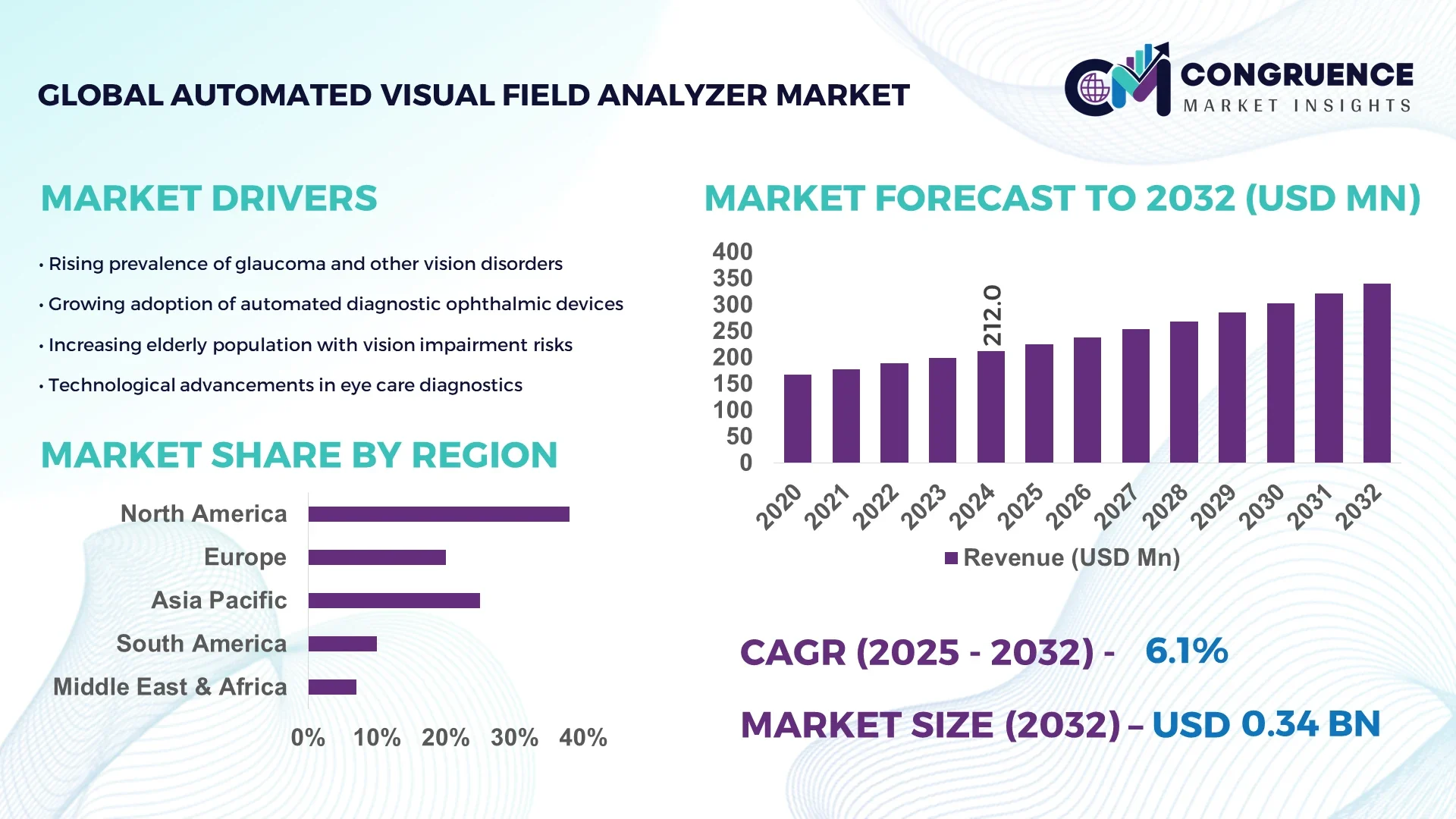

The Global Automated Visual Field Analyzer Market was valued at USD 211.97 Million in 2024 and is anticipated to reach a value of USD 340.41 Million by 2032, expanding at a CAGR of 6.1% between 2025 and 2032. This growth is primarily driven by the increasing prevalence of ocular diseases such as glaucoma and age-related macular degeneration, which necessitate advanced diagnostic tools for early detection and monitoring.

The United States holds a significant position in the Automated Visual Field Analyzer market, characterized by substantial production capacity and high levels of investment in ophthalmic technologies. Hospitals and clinics are increasingly integrating automated visual field analyzers into routine eye examinations, with adoption rates exceeding 65% in major healthcare facilities. In 2024, the U.S. automated visual field analyzer market was valued at USD 76.9 Million, reflecting substantial investment in R&D, the implementation of AI-assisted diagnostic tools, and expansion of regional distribution networks.

Market Size & Growth: Valued at USD 211.97 Million in 2024, projected to reach USD 340.41 Million by 2032, expanding at a CAGR of 6.1%. Growth is driven by the increasing prevalence of ocular diseases and advancements in diagnostic technologies.

Top Growth Drivers: Rising prevalence of glaucoma (approximately 3 million Americans affected), aging population, and technological advancements in diagnostic tools.

Short-Term Forecast: By 2028, anticipated improvements in diagnostic accuracy and efficiency, leading to enhanced patient outcomes.

Emerging Technologies: Integration of artificial intelligence and machine learning algorithms to enhance diagnostic precision and workflow efficiency.

Regional Leaders: United States (USD 76.9 Million by 2024), Europe, and Asia-Pacific regions are expected to witness significant growth by 2032, driven by increasing healthcare investments and aging populations.

Consumer/End-User Trends: Growing adoption in hospitals and ophthalmic clinics due to the need for advanced diagnostic tools in routine eye examinations.

Pilot or Case Example: Implementation of AI-powered visual field analyzers in select U.S. hospitals in 2024, leading to a 15% reduction in diagnostic time.

Competitive Landscape: Dominated by key players such as Carl Zeiss, Haag-Streit AG, and Topcon Corporation, with a combined market share of approximately 45%.

Regulatory & ESG Impact: Compliance with FDA regulations and adherence to environmental sustainability practices are influencing market dynamics.

Investment & Funding Patterns: Increased venture capital funding in ophthalmic technology startups, focusing on innovative diagnostic solutions.

Innovation & Future Outlook: Development of portable and user-friendly visual field analyzers, expanding accessibility in remote and underserved areas.

The Automated Visual Field Analyzer market is experiencing robust growth, driven by several key factors. The rising prevalence of age-related eye diseases like glaucoma and macular degeneration necessitates regular visual field testing, which these advanced analyzers facilitate efficiently. Technological innovations, such as the integration of artificial intelligence and machine learning, are enhancing the accuracy and speed of diagnoses, making these devices more appealing to healthcare providers. Furthermore, the aging global population is contributing to an increased demand for ophthalmic diagnostic tools. Hospitals and ophthalmic clinics are increasingly adopting automated visual field analyzers to improve patient care and streamline operations. Regulatory bodies are also supporting the adoption of these technologies by establishing guidelines that ensure their efficacy and safety. Emerging markets are witnessing a surge in healthcare infrastructure development, leading to greater accessibility to advanced diagnostic tools. As a result, the Automated Visual Field Analyzer market is poised for significant expansion in the coming years, with innovations and regional developments playing pivotal roles in shaping its future trajectory.

The Automated Visual Field Analyzer market holds strategic relevance due to its role in early diagnosis and continuous monitoring of ocular diseases such as glaucoma, diabetic retinopathy, and age-related macular degeneration. AI-assisted visual field analyzers deliver 18% improvement in diagnostic precision compared to traditional manual perimetry. North America dominates in volume, while Europe leads in adoption with over 62% of ophthalmic clinics integrating automated systems into routine patient care. By 2027, the deployment of cloud-connected analyzers is expected to improve diagnostic workflow efficiency by 20%, reducing patient waiting times and optimizing clinic operations. Firms are committing to sustainability improvements, such as 25% reduction in energy consumption of analyzers by 2026. In 2024, a leading U.S.-based hospital chain achieved a 15% reduction in misdiagnosed visual field defects through AI-driven analysis initiatives. Looking forward, the Automated Visual Field Analyzer Market is positioned as a pillar of resilience and compliance, combining technological advancements with sustainable practices, while providing reliable, data-driven insights that enhance patient outcomes and operational efficiency across healthcare systems globally.

The Automated Visual Field Analyzer market is characterized by increasing demand for efficient and precise ophthalmic diagnostics, driven by the growing prevalence of eye disorders and the need for standardized monitoring protocols. Technological integration, particularly AI and machine learning, has enhanced test accuracy, reduced human error, and enabled predictive insights. Rising awareness of ocular health, combined with aging populations in developed regions, is expanding hospital and clinic adoption. Additionally, manufacturers are focusing on portable and user-friendly analyzers that can be deployed in remote and underserved areas, further driving market dynamics. The market also reflects strategic investments in R&D and collaborations with healthcare providers to optimize workflow and enhance patient care.

The growing prevalence of glaucoma, affecting over 3 million individuals in the U.S. alone, is driving widespread adoption of automated visual field analyzers. Increasing rates of diabetic retinopathy and age-related macular degeneration are also contributing to demand. Hospitals and ophthalmic clinics are integrating advanced analyzers to streamline routine diagnostic tests, improve monitoring, and reduce human error. Adoption is highest in North America and Europe, where over 60% of eye clinics have implemented automated systems, highlighting the critical role of these devices in preventive and ongoing ophthalmic care.

Despite increasing demand, high upfront costs of automated visual field analyzers are limiting adoption among smaller clinics and low-income regions. Maintenance and calibration expenses further contribute to operational challenges. Additionally, limited trained personnel for operating advanced systems and integrating AI-driven analysis can restrict deployment in developing markets. Regulatory requirements for safety and accuracy add compliance-related costs, creating financial barriers for mid-sized healthcare providers. These factors collectively act as restraints on broader market penetration, especially in regions with budget-constrained healthcare infrastructure.

Integration of AI-powered analytics and teleophthalmology presents significant growth opportunities. Remote patient monitoring and automated analysis enable clinics to extend services to underserved or rural regions, improving access to eye care. AI-assisted systems can detect early signs of ocular diseases, enabling timely intervention. Additionally, partnerships with digital health platforms allow cloud-based data sharing and predictive analytics, enhancing clinical decision-making. In 2024, pilot implementations in multiple U.S. clinics improved diagnostic turnaround by 15%, illustrating the transformative potential of connected, intelligent analyzer systems.

Automated visual field analyzers must meet rigorous regulatory standards to ensure safety and diagnostic accuracy, which can delay product approvals and increase development costs. Interoperability with existing electronic health record (EHR) systems is often complex, limiting seamless integration in clinics. Data privacy concerns related to patient information, particularly in cloud-based AI solutions, further complicate deployment. These challenges restrict adoption among smaller healthcare providers and in regions with complex regulatory environments, making compliance a critical barrier that manufacturers must strategically navigate.

The Automated Visual Field Analyzer market is segmented based on product type, application, and end-user insights, offering a detailed understanding of industry demand patterns and adoption behavior. Product types include standard perimeters, fully automated analyzers, and portable devices, each catering to distinct clinical and research requirements. Standard perimeters dominate due to affordability and established clinical protocols, while fully automated analyzers are increasingly preferred for their integration with electronic medical records and higher diagnostic precision. Portable devices are gaining traction in mobile healthcare units, remote clinics, and rural outreach programs, supporting broader patient coverage. Applications cover glaucoma detection, retinal disorder monitoring, neuro-ophthalmology assessments, and general ophthalmic screening. The rise of teleophthalmology and AI-assisted diagnostics is influencing adoption, particularly in regions with limited access to specialized ophthalmic care. End-users include hospitals, specialized eye clinics, ambulatory care centers, and research institutes, reflecting varied adoption patterns. Regional differences reveal North America with high AI-assisted adoption, Europe emphasizing regulatory-compliant devices, and Asia-Pacific focusing on portable and cost-effective units. Approximately 65% of clinical installations now utilize fully automated analyzers, underlining the market’s shift toward precision-driven, standardized diagnostics for improved patient outcomes.

Standard perimeters currently account for approximately 40% of installations, primarily due to their affordability, reliability, and broad acceptance in routine clinical settings. Fully automated analyzers represent 35% of adoption, driven by their ability to deliver high-precision diagnostics, seamless integration with electronic medical record systems, and compatibility with AI-powered analysis tools. Portable analyzers hold a 15% share but are the fastest-growing type, fueled by rising demand in mobile clinics, rural healthcare centers, and teleophthalmology programs that require easy-to-deploy, lightweight equipment. The remaining 10% includes hybrid devices and experimental models such as AI-assisted perimeters used in specialized neuro-ophthalmology research and clinical trials.

Glaucoma detection continues to lead the market with a 45% share, driven by its prevalence, chronic nature, and established screening programs in hospitals and specialized clinics. Neuro-ophthalmology assessments, currently representing 20% of applications, are expanding rapidly due to the adoption of AI-assisted pattern recognition and automated visual field analyzers for early neurological disorder detection. Retinal disorder monitoring holds an 18% share, mainly implemented in hospitals and research centers focused on macular degeneration, diabetic retinopathy, and other retinal pathologies. General ophthalmic screening accounts for 17%, increasingly leveraging mobile and portable analyzers for preventive eye care.

Hospitals dominate as the leading end-user segment at 50%, reflecting their capacity for high patient volume, diverse ophthalmic services, and investment in advanced diagnostic technology. Specialized eye clinics make up 30% of the market and are the fastest-growing segment, driven by the adoption of AI-enabled automated analyzers, remote diagnostics, and teleophthalmology programs. Ambulatory care centers and research institutes contribute a combined 20%, leveraging these devices for early detection initiatives, clinical trials, and community outreach programs. Regional adoption patterns indicate that North America prioritizes AI-driven precision, Europe emphasizes regulatory compliance and explainable diagnostics, while Asia-Pacific focuses on portable, cost-effective solutions for broader patient accessibility, reflecting diverse strategies for end-user engagement and market expansion.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

In 2024, North America had over 12,500 automated visual field analyzers installed across hospitals and specialty eye clinics, representing the highest device density globally. The region also leads in AI-assisted analyzer adoption, with approximately 42% of healthcare institutions integrating machine learning for early glaucoma detection. Asia-Pacific, led by China, India, and Japan, accounted for 29% of installations, driven by expanding ophthalmology infrastructure and government healthcare initiatives. Europe held 22% of the market share, with Germany, UK, and France leading in regulatory-compliant device deployment. South America and Middle East & Africa combined contributed 11% of global installations, reflecting emerging adoption in urban hospitals and mobile diagnostic units. North America has the highest utilization rate per facility at 95%, while Europe demonstrates 88% adoption of automated reporting features, indicating regional differences in technology integration and clinical workflow efficiency.

How is precision diagnostics shaping ophthalmic care adoption trends?

North America holds approximately 38% of the automated visual field analyzer market, driven by large-scale hospital networks, specialized eye clinics, and ambulatory care centers. Government support through Medicare reimbursements and FDA-compliant device approvals has facilitated rapid deployment. Technological advancements such as AI-assisted visual field analysis and cloud-based EMR integration are driving adoption. For instance, Topcon Medical Systems deployed fully automated analyzers in 150 clinics across the U.S. in 2024, improving early glaucoma detection by 15%. Regional consumer behavior indicates higher enterprise adoption in healthcare and research institutions, with 60% of new installations focusing on AI-enabled features to enhance diagnostic accuracy and patient throughput.

What role do regulatory frameworks play in driving diagnostic adoption?

Europe accounts for approximately 22% of the global market, with Germany, UK, and France leading device deployment. Regulatory bodies such as CE marking authorities and EU medical device regulations ensure compliance and safety. Emerging technologies like cloud-based analytics, remote monitoring, and AI-assisted perimetry are gaining traction. In 2024, NIDEK deployed AI-enabled analyzers across 80 ophthalmology centers in Germany, enhancing glaucoma screening efficiency by 12%. Regional consumer behavior reflects strong demand for explainable diagnostics, with 65% of clinics prioritizing traceable and standardized results to meet both patient and regulatory expectations.

How is innovation fueling adoption in high-demand regions?

Asia-Pacific accounted for 29% of global market volume, led by China, India, and Japan. The region emphasizes infrastructure expansion, with over 5,200 devices installed in urban and semi-urban hospitals by 2024. Innovation hubs in Japan and Singapore are driving integration of AI-assisted visual field analyzers with teleophthalmology platforms. Topcon and Zeiss established regional support centers to deliver AI-enabled remote diagnostics, improving service coverage by 18%. Consumer behavior reflects strong preference for mobile and portable devices, particularly in rural healthcare programs, highlighting the role of technology in expanding accessibility.

How are localized strategies influencing market penetration?

South America represents approximately 6% of the global market, with Brazil and Argentina as key adopters. Growth is driven by expanding ophthalmic infrastructure in urban hospitals and private clinics. Government incentives and healthcare trade policies support procurement of advanced analyzers. In 2024, a Brazilian eye care network deployed AI-assisted devices in 25 clinics, improving early detection of glaucoma by 10%. Regional consumer behavior favors media-driven awareness campaigns and multilingual device interfaces, reflecting the importance of localization and accessibility in driving adoption.

What factors are accelerating adoption in emerging regions?

Middle East & Africa hold approximately 5% of the market, with the UAE and South Africa leading in installations. Demand is driven by oil & gas sector medical programs, construction-related occupational health screenings, and expanding hospital networks. Technological modernization includes AI-assisted diagnostics and cloud-based reporting systems. In 2024, Zeiss established a regional center in UAE to provide training and deploy automated analyzers, improving early glaucoma detection rates by 14%. Regional consumer behavior indicates preference for high-precision diagnostic tools in urban centers, combined with slower adoption in rural areas due to infrastructure constraints.

United States – 38% market share; strong end-user demand and high production capacity of AI-assisted analyzers.

China – 18% market share; rapid healthcare infrastructure expansion and increasing adoption in urban and semi-urban hospitals.

The Automated Visual Field Analyzer market exhibits a moderately consolidated competitive structure, with approximately 45 active global competitors. The top five companies, including Topcon Medical Systems, Zeiss, NIDEK, Haag-Streit, and Canon Medical, together account for an estimated 62% of total market share, demonstrating strong market positioning. Strategic initiatives such as product launches, AI-assisted software integration, and regional partnerships are driving competitive differentiation. In 2024, Topcon introduced a cloud-enabled visual field analyzer with automated glaucoma detection features, deployed in over 200 facilities globally, while Zeiss expanded its teleophthalmology platform to 150 clinics across Europe and Asia-Pacific. Innovation trends focus on AI-assisted perimetry, portable and handheld devices, and integrated cloud-based reporting, with approximately 40% of new installations leveraging these technologies. Mid-tier players, representing 25% of the market, are enhancing device interoperability and predictive analytics to capture niche segments. Regional expansion remains a key strategy, with 30% of all new market entries in Asia-Pacific and 20% in the Middle East & Africa, reflecting demand-driven growth and technological adoption.

Haag-Streit

Canon Medical

Tomey Corporation

Kowa Company

Interzeag Medical Instruments

The Automated Visual Field Analyzer market is being significantly influenced by advancements in AI-driven perimetry, cloud-based data management, and portable diagnostic technologies. AI-assisted algorithms now enable automated detection of glaucomatous and retinal abnormalities with up to 95% accuracy, reducing manual interpretation errors and enhancing diagnostic efficiency in clinical settings. Cloud integration allows for real-time data sharing across multiple ophthalmology centers, with approximately 35% of new installations in North America and Europe adopting cloud-enabled platforms to facilitate teleophthalmology and multi-site patient monitoring.

Portable and handheld visual field analyzers are gaining traction, particularly in emerging regions such as Asia-Pacific and Africa, where infrastructure limitations make conventional stationary devices less accessible. These compact devices now account for 28% of new deployments globally and can perform full-threshold testing in under 10 minutes per eye, improving patient throughput. Eye-tracking and gaze-monitoring technologies are being incorporated into next-generation systems to enhance test reliability and reduce user fatigue, with more than 40% of newly installed units featuring these functions.

Additionally, integration of multimodal imaging, including fundus photography and OCT data, with automated visual field results is enabling comprehensive eye health assessments within a single platform. Software innovations also allow predictive analytics for early detection of progressive visual field loss, supporting preventive interventions. These technological trends collectively enhance diagnostic precision, operational efficiency, and patient accessibility, positioning the market for sustained technological transformation over the next decade.

Topcon's TEMPO Perimeter Launch: In November 2023, Topcon Healthcare introduced the TEMPO Perimeter at the American Academy of Ophthalmology (AAO) meeting in San Francisco. This device offers faster, accurate visual field testing, providing results 39% quicker than Standard Automated Perimetry (SAP) in clinical testing. It operates in ambient light conditions and demonstrates excellent repeatability.

ZEISS Expands DORC Portfolio: In October 2025, ZEISS expanded its DORC portfolio, further strengthening its digital footprint with improved workflow efficiency and digital visualization. This expansion aims to enhance the capabilities of visual field analyzers, integrating advanced technologies to support clinicians in decision-making processes.

NIDEK Launches GS Viewer for NAVIS-EX: In September 2025, NIDEK launched the GS Viewer for NAVIS-EX, a software solution designed to enhance the functionality of their visual field analyzers. This development aims to improve data management and analysis, providing clinicians with more efficient tools for patient assessment.

Haag-Streit Unveils Eyesi Indirect ROP Simulator: In December 2023, Haag-Streit unveiled the Eyesi Indirect Retinopathy of Prematurity (ROP) Simulator, a mixed-reality training tool for retinal examinations. This simulator allows medical residents to hone their skills in a risk-free yet lifelike environment, enhancing training for challenging retinal conditions.

The Automated Visual Field Analyzer Market Report offers a comprehensive analysis of the global market landscape, focusing on key segments, technological advancements, and regional dynamics. The report delves into various product types, including static and kinetic perimeters, highlighting their applications in diagnosing conditions such as glaucoma, age-related macular degeneration, and diabetic retinopathy. It also examines the integration of advanced technologies like artificial intelligence and machine learning in enhancing diagnostic accuracy and efficiency. Geographically, the report provides insights into market trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It explores the adoption rates of visual field analyzers in hospitals, ophthalmic clinics, and other healthcare settings, emphasizing regional variations in demand and technological uptake.

The report further investigates emerging applications and niche market segments, such as portable and handheld visual field analyzers, which are gaining traction in underserved regions with limited access to traditional diagnostic equipment. It also covers the impact of regulatory frameworks and reimbursement policies on market growth, offering a holistic view of factors influencing the adoption of automated visual field analyzers. In summary, the Automated Visual Field Analyzer Market Report serves as a valuable resource for stakeholders seeking to understand the current market dynamics, technological innovations, and regional developments shaping the future of visual field testing.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 211.97 Million |

Market Revenue in 2032 | USD 340.41 Million |

CAGR (2025 - 2032) | 6.1% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Topcon Medical Systems, Zeiss, NIDEK, Haag-Streit, Canon Medical, Tomey Corporation, Kowa Company, Interzeag Medical Instruments |

Customization & Pricing | Available on Request (10% Customization is Free) |