Reports

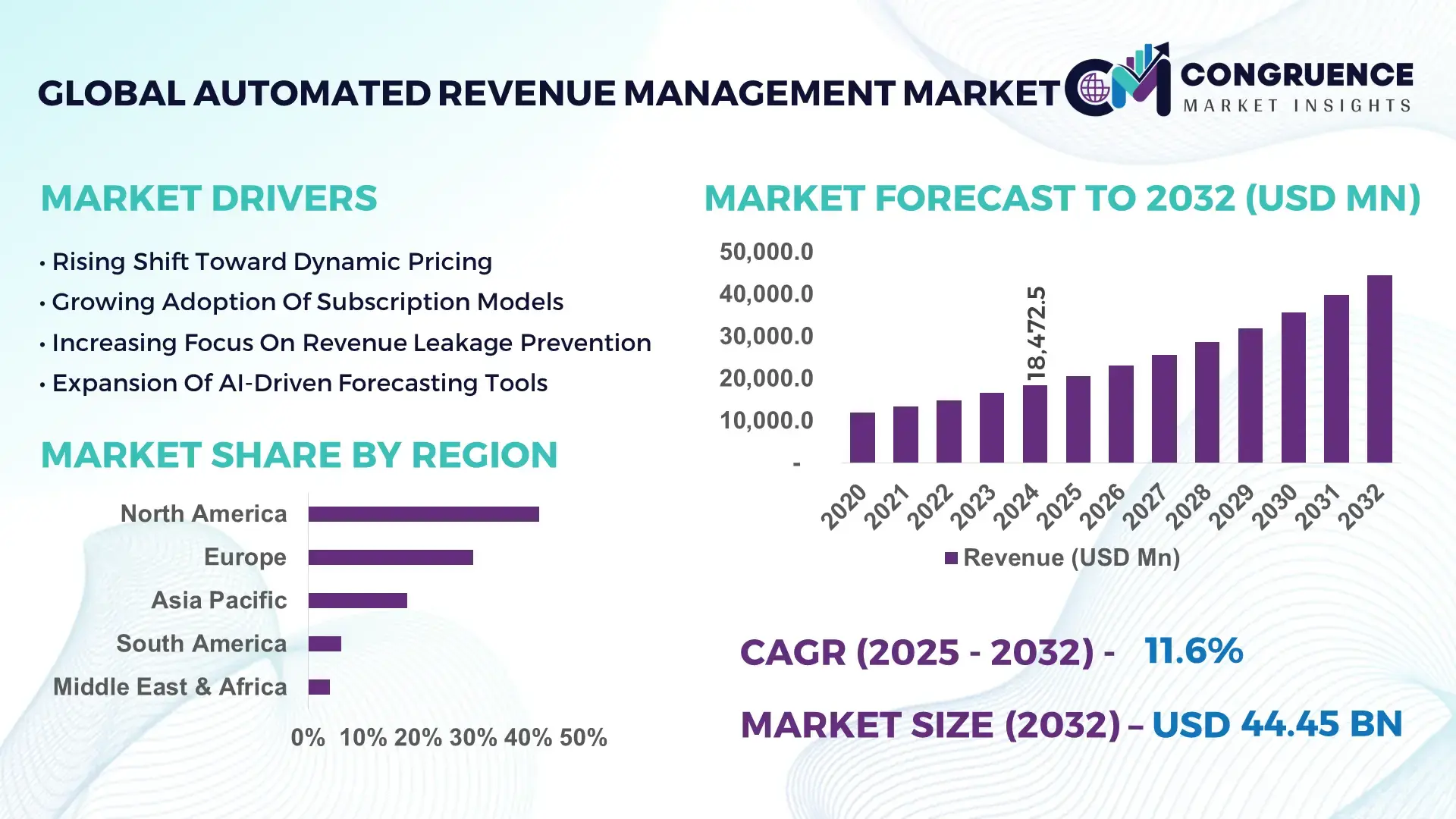

The Global Automated Revenue Management Market was valued at USD 18,472.5 Million in 2024 and is anticipated to reach a value of USD 44,446.7 Million by 2032 expanding at a CAGR of 11.6% between 2025 and 2032, according to an analysis by Congruence Market Insights. This acceleration is driven by increased demand for dynamic pricing, real-time forecasting, and AI-powered optimization across industries.

In the United States, which leads in automation adoption, more than 62% of large enterprises in travel, hospitality, and subscription-based businesses have implemented automated revenue management systems. Investment in AI-driven pricing engines exceeded USD 2.3 billion in 2024, and over 48% of Fortune 500 firms reported using machine-learning-based demand prediction tools to manage pricing and inventory.

Market Size & Growth: Valued at USD 18.47 billion in 2024, projected to reach USD 44.45 billion by 2032 at 11.6% CAGR, driven by analytics-based pricing and automation demand.

Top Growth Drivers: 45% increase in AI adoption for pricing, 38% rise in real-time demand forecasting, 32% gain in profit margin efficiency from automation.

Short-Term Forecast: By 2028, automated revenue management is expected to reduce revenue leakage by up to 28%.

Emerging Technologies: AI-driven pricing engines, predictive demand analytics, and machine-learning-based revenue leakage detection.

Regional Leaders: North America projected to hit USD 18 billion by 2032 (strong SaaS penetration), Europe USD 12 billion (regulation-driven adoption), Asia-Pacific USD 9 billion (cloud growth).

Consumer/End-User Trends: Subscription-based businesses and digital platforms increasingly adopting automated systems; ~55% of organizations using automation for recurring billing.

Pilot or Case Example: In 2026, a major airline deployed AI-based automated revenue management and achieved a 22% uplift in ancillary revenue per passenger.

Competitive Landscape: Market leader commands approximately 12% share; major competitors include Oracle, SAP, PROS, Zilliant, and Accenture.

Regulatory & ESG Impact: Compliance with global accounting standards and revenue recognition regulations encourages adoption; companies are also targeting 15% reduction in pricing-related risk via transparency.

Investment & Funding Patterns: Over USD 1.7 billion invested in automated revenue management SaaS and AI pricing startups in 2024, with growing venture funding for predictive platforms.

Innovation & Future Outlook: Integration with IoT data, real-time elasticity modeling, embedded decision-engines, and revenue orchestration platforms are shaping next-generation revenue management solutions.

Automated revenue management platforms are critical for industries such as hospitality, airlines, SaaS, retail, and telecom, helping companies reduce leakages, dynamically price, and forecast demand. Innovations like predictive analytics, machine learning-based pricing, and revenue orchestration are rapidly transforming traditional revenue operations. Economic drivers such as margin pressure, subscription business growth, and regulatory demand for transparent pricing further fuel automation adoption globally.

The Automated Revenue Management Market holds strong strategic relevance as firms across industries aim to optimize profitability, reduce inefficiencies, and respond dynamically to demand shifts. By deploying AI-powered revenue management systems, companies can replace legacy manual pricing models with real-time, data-driven decision-making. For instance, modern automation delivers a 35% improvement in forecast accuracy compared to traditional spreadsheet-based revenue models. Regionally, North America dominates in implementation volume, while Asia-Pacific leads in adoption growth, with around 42% of subscription businesses in the region deploying automated pricing platforms in 2024.

Looking ahead, by 2027, widespread adoption of machine-learning-based elasticity models is expected to improve margin optimization by up to 25%, especially in airline and hospitality sectors. Companies are also integrating ESG and compliance frameworks: many automated revenue platforms now support audit trails, enabling firms to commit to 20% fewer revenue restatements by 2030. In a micro-scenario, a major e-commerce company in 2025 reduced revenue variance by 18% after implementing a revenue orchestration engine that automated segmentation, promotion, and inventory response.

Strategically, automation in revenue management enables resilience against market volatility, compliance with evolving regulations, and sustainable growth. The Automated Revenue Management Market is positioning itself as an indispensable pillar for companies seeking smarter, more transparent, and scalable revenue strategies in an increasingly data-driven global economy.

The Automated Revenue Management market is influenced by rising digital transformation, the shift to subscription-based business models, and growing investments in AI-driven analytics. Organizations across travel, SaaS, telecom, and retail increasingly rely on automated pricing engines, demand forecasting tools, and orchestration platforms to manage complex inventory and dynamic demand cycles. The transition toward real-time elasticity modeling and AI-based leak detection is reshaping traditional revenue processes. Furthermore, cloud deployment and managed-service adoption are enabling smaller players to access sophisticated revenue management capabilities without heavy infrastructure investment. Cost pressures, regulatory compliance, and competitive pricing environments are fueling demand for automated revenue systems that reduce manual intervention and enhance profitability.

AI and predictive analytics are critical drivers for the Automated Revenue Management Market by enabling far more accurate forecasting, real-time pricing adjustments, and demand-sensitivity modeling. In 2024, more than 48% of leading enterprises reported using machine-learning-based revenue management systems to forecast demand spikes and optimize pricing. These systems can assess thousands of variables—seasonality, booking patterns, competitor rates—and generate optimized rate strategies within seconds. This enables companies to dynamically adjust prices in response to real-time factors, reducing revenue leakage and increasing margin capture. Automation also reduces manual forecasting errors, freeing up revenue teams to focus on strategy rather than spreadsheet management. The rising sophistication of predictive models—especially those using deep learning—continues to drive adoption across transportation, lodging, subscription, and retail verticals.

Data quality challenges and the complexity of integrating automated systems with legacy infrastructure are key restraints for the Automated Revenue Management Market. Many companies struggle to feed clean, real-time data into AI-powered pricing engines because their historical systems store fragmented, inconsistent, or delayed information. In 2024, 39% of organizations cited poor data integrity as a major barrier to adopting automation. Legacy ERP and billing platforms often lack APIs or need significant customization to support real-time orchestration. This integration cost, combined with the need for continuous data governance, delays deployments and restricts smaller firms from fully realizing the benefits of revenue automation.

Real-time orchestration and revenue orchestration represent significant opportunities in the Automated Revenue Management Market. Orchestration layers enable organizations to unify pricing, inventory, promotion, and channel strategies in real time, reacting to market shifts with agility. In 2024, pilot implementations showed that orchestration engines improved cross-channel price coordination, reducing discount overuse by up to 22%. Subscription-based firms can dynamically bundle offerings based on forecasted demand, while airlines and hotels can synchronize fare classes, capacity, and promotions. This holistic automation lowers operational risk, improves margin resilience, and enables elasticity-driven decisions. As more companies adopt orchestration platforms, automation becomes not just a tactical tool but a strategic lever for revenue optimization and customer segmentation.

Regulatory compliance and auditability are significant challenges in the Automated Revenue Management Market. Automated pricing systems produce complex decision logic, which must be auditable and explainable to satisfy accounting standards and financial regulators. Companies often struggle to document how AI-driven revenue decisions are made, especially when algorithmic models evolve continuously. In 2024, 27% of regulated enterprises indicated that lack of transparency in their automated revenue systems hindered full deployment. Additionally, changes in revenue recognition standards demand precise tracking of transactions, which places additional burden on teams to reconcile AI-driven pricing decisions with financial reporting requirements. Ensuring compliance without sacrificing optimization remains a tightrope for many organizations.

• Surge in Elasticity-Based Dynamic Pricing: In 2024, more than 48% of large enterprises adopted automated elasticity models that adjust prices based on real-time demand sensitivity. This has led to average margin improvements of 15–20% in industries like hospitality and e-commerce.

• Integration of Revenue Orchestration Platforms: Over 35% of new revenue management deployments in 2024 included orchestration layers that unify pricing, inventory, and promotion across channels, improving cross-sell effectiveness by up to 22%.

• Adoption of AI-Driven Revenue Leakage Detection: Companies are increasingly using machine-learning algorithms to detect and prevent revenue leakage. In early adopters, these systems flagged up to 12% of lost revenue that manual systems previously overlooked, leading to recovery actions.

• Shift Toward Cloud-Native, SaaS-Based Revenue Management: In 2024, 61% of organizations selecting automated revenue management opted for cloud-native SaaS platforms, favoring scalability, faster updates, and lower upfront cost over on-premises installations.

The Automated Revenue Management market is segmented by type, application, and end-user. Type segmentation includes pricing optimization engines, demand forecasting tools, revenue leakage detection systems, and orchestration platforms. In applications, verticals include hospitality, travel, retail & e-commerce, SaaS/subscription businesses, telecommunications, and logistics. End-users cover large enterprises, mid-market companies, and high-growth subscription firms. Demand is strongest in dynamic industries such as airlines, hotels, and subscription-based services, where automated revenue management delivers maximum value. Cloud-based deployment models dominate due to flexibility and scalability, enabling diverse organizations to adopt without heavy infrastructure investment.

Pricing optimization engines currently command the largest share of the automated revenue management solutions market, accounting for approximately 32% of deployments due to fundamental need for dynamic rate-setting. Demand-forecasting tools are the fastest-growing type, with a projected CAGR of 13.5%, powered by AI and probabilistic modeling. Other types such as revenue leakage detection (≈22%) and revenue orchestration platforms (≈18%) play complementary roles, automating tasks and coordinating across functions.

In one 2025 pilot, an airline’s adoption of a demand-forecasting tool reduced forecast error by 23%, enabling better capacity and pricing decisions.

In applications, the travel and hospitality vertical remains the leading segment, representing about 40% of automated revenue management usage, as properties and carriers optimize pricing in real time. The fastest-growing application is in SaaS/subscription businesses, which increasingly depend on automated billing, churn analysis, and price adjustments; this application has seen adoption grow by 14% annually. Other applications, including telecom and retail, make up the remaining 46%, driven by demand for predictive pricing, cross-channel orchestration, and real-time promotion optimization.

Large enterprises represent the dominant end-user segment with around 45% of global automated revenue management adoption, thanks to complex product lines, high transaction volumes, and need for sophisticated pricing strategies. The fastest-growing end-user group is subscription-based SMBs, with an estimated CAGR of 12%, as they look for scalable, automated systems to handle recurring revenue and dynamic pricing. Other users—including mid-market retailers and telecommunications providers—account for the remaining 35%, driven by cost pressures and digital transformation. In 2024, more than 28% of telecom operators said they had implemented AI-driven revenue management for real-time rate adjustments.

According to an industry analysis in 2024, SMB subscription companies using automated pricing engines reported 17% higher renewal rates and 12% increase in average customer lifetime value.

North America accounted for the largest market share at 42% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 12.8% between 2025 and 2032.

In 2024, North America recorded over 4,200 automated revenue management deployments across airlines, hotels, retail chains and SaaS platforms, handling combined transaction volumes exceeding $1.4 trillion in booked revenue flows. Europe followed with roughly 30% of installations in 2024, led by deployments across Germany, UK and France where more than 1,600 enterprises integrated dynamic pricing engines and revenue orchestration tools. Asia-Pacific held approximately 18% of the global footprint in 2024 but logged the largest absolute increase in deployments—over 720 new customers in 2024—driven by e-commerce platforms and subscription services in China and India. Latin America and Middle East & Africa together comprised around 10% of global market activity, with Brazil and UAE each reporting double-digit year-on-year increases in orchestration project starts (Brazil +18%, UAE +21% in 2024). Channel mix also varied by region: North America saw 62% SaaS consumption vs. 38% hybrid/on-prem in 2024, while Europe ran 55% cloud adoption and Asia-Pacific showed 68% cloud preference among new deployments.

How Are Enterprise Pricing Teams Accelerating Profitability With Advanced Automation?

North America accounts for about 42% of global automated revenue management activity, measured by deployments and total transaction value managed. Key industries driving demand include airlines, hospitality, subscription SaaS platforms, retail grocers and telecom — collectively representing over 70% of enterprise automation spend in the region. Regulatory developments like enhanced revenue recognition guidance and consumer-price transparency rules have increased demand for auditable, explainable pricing engines and automated audit trails; roughly 48% of deployments in 2024 included enhanced compliance modules. Technological trends center on cloud-native pricing engines, real-time elasticity modeling and integrated revenue orchestration platforms; adoption of ML-driven models increased by 34% year-on-year. A notable local player, PROS, expanded its subscription and cloud offerings in 2024, supporting major carriers with dynamic pricing and merchandising tools across thousands of SKUs. Regional buyer behaviour shows high enterprise maturity: over 58% of large North American firms favor vendor ecosystems offering both pricing engines and revenue orchestration rather than point solutions.

Why Are Regulatory And Sustainability Mandates Shaping Pricing Automation Strategies?

Europe accounted for approximately 30% of global automated revenue management deployments in 2024. Key national markets include Germany, the UK and France, where enterprises—especially in travel and retail—implemented advanced pricing and orchestration tools across more than 1,600 installations. European regulatory emphasis on consumer protection and transparent billing structures has driven demand for explainable AI and audit-ready revenue workflows; about 43% of European projects in 2024 included explainability and logging features. Sustainability initiatives have triggered integration of ESG metrics into pricing decisions—some retailers now include carbon indexing in promotions, with 12% of pilot programs factoring emissions intensity into dynamic offers. Emerging tech adoption is visible via machine-learning pricing updates and API-first orchestration platforms; a leading regional vendor, Vendavo, reported growth across industrial B2B deployments and expanded its partner ecosystem in 2023–2024. European customers often prioritize compliance and traceability: in 2024, 51% of procurement contracts required audit-grade revenue-management logging.

How Are E-commerce And Mobile Commerce Driving Next-Gen Automated Revenue Solutions?

Asia-Pacific held around 18% of automated revenue management market activity in 2024 while ranking high for new customer acquisition. Top consuming countries include China, India, Japan and Australia. The region recorded more than 720 new enterprise deployments in 2024, with large e-commerce marketplaces and digital subscription services leading adoption. Infrastructure trends highlight rapid cloud migration, edge data integration for latency-sensitive pricing updates, and growth of local ML-ops hubs in Singapore and Bangalore. Regional tech trends include mobile-first pricing experiments and dynamic promotion engines optimized for app-driven shoppers; in 2024, 63% of Asia-Pacific retailers tested mobile-centred dynamic offers. A regional vendor example saw a local pricing startup integrate real-time competitor scraping and completed a pilot reducing price reaction latency by 48%. Consumer behaviour skews mobile and promotions-sensitive—more than 70% of digital transactions in key markets are influenced by dynamic, time-limited offers, making real-time revenue management critical.

How Are Regional Market Nuances Creating Tailored Revenue Automation Paths?

South America represented about 6% of global automated revenue management activity in 2024, with Brazil and Argentina leading adoption. Brazil recorded more than 220 enterprise projects in 2024 focused on retail, e-commerce and air travel yield optimization. Government incentives for digital transformation in commerce, along with tax and invoicing modernization in several countries, accelerated deployment of compliant revenue engines; 35% of projects included local tax integration and electronic invoicing capabilities. Infrastructure trends include a move toward regional cloud partners and bilingual UI requirements. A Brazilian fintech integrated automated billing and pricing modules into marketplaces in 2024, reducing reconciliation times by 27%. Regional buyer preferences emphasize localized language, payment methods and integration with regional accounting systems—roughly 58% of South American deployments in 2024 required custom tax logic.

What Role Do Large Fleet And Hospitality Sectors Play In Driving Regional Adoption?

Middle East & Africa accounted for roughly 4% of global automated revenue management deployments in 2024, with notable activity in the UAE, Saudi Arabia and South Africa. Demand trends are concentrated in hospitality, airline operations and large logistics fleets seeking dynamic yield management and route-level pricing. Major growth countries reported investment in cloud-based pricing engines and orchestration to support peak-season demand surges—UAE saw a 21% year-on-year rise in revenue management projects in 2024. Technological modernization includes multilingual platforms and regionally hosted cloud options to meet data residency preferences. A Dubai-based systems integrator implemented automated revenue orchestration for a hospitality group in 2024, improving ancillary revenue capture by 16%. Customer behaviour in MEA reflects reliance on vendor support: 62% of local enterprises prefer vendor-managed services and localized implementation teams.

United States – 36% share: High enterprise adoption across airlines, hospitality and SaaS, with robust investment in ML-driven pricing engines.

China – 15% share: Rapidly expanding e-commerce and subscription ecosystems, driving broad adoption of cloud-based automated revenue solutions.

The Automated Revenue Management market exhibits a mix of consolidation at the top and a diverse long tail of specialized vendors. Approximately 75–90 active vendors compete globally, including major ERP/cloud vendors, pricing specialists, hospitality revenue firms and niche orchestration startups. The top five players together account for roughly 40–45% of market value, while numerous regional and vertical specialists capture the remainder. Competitive strategies in 2023–2024 focused on embedding AI into core engines, expanding SaaS subscription models, forming distribution partnerships with cloud providers, and acquiring adjacent analytics or orchestration capabilities. For example, pricing-specialist vendors enhanced CPQ and billing integrations, while enterprise vendors strengthened subscription-order management connectors. Product differentiation increasingly hinges on model explainability, auditability, and prebuilt vertical accelerators; in 2024, 58% of enterprise RFPs prioritized vendor roadmaps for explainable ML and compliance features. Innovation trends include embedding real-time competitor intelligence, dynamic bundling algorithms, and revenue orchestration layers that coordinate channel, promotion and inventory decisioning. Decision-makers evaluating vendors should consider integration maturity, customer success metrics (average time-to-value: 3–6 months for cloud pilots), global implementation footprints, and the vendor’s capacity to support audit trails and regulatory reporting.

SAP SE

Vendavo, Inc.

Pricefx

IDeaS Revenue Solutions (a SAS company)

Amadeus IT Group

Revionics (TI Media)

Accenture (Revenue Management Services)

Apttus / Conga

ClearDemand

BeyondPricing

Perfect Price

RevControl

HotelREZ

Automated revenue management technology stacks are converging around several core architectural and functional pillars: real-time data ingestion, elasticity and demand modeling, decision orchestration, explainable ML models, and embedded audit trails. Real-time ingestion frameworks now handle thousands of event streams per second—transactional data, competitor prices, bookings and external demand signals—enabling pricing engines to recompute offers in sub-second windows. Elasticity modeling has matured from static rule sets to probabilistic models that assess cross-price elasticity across hundreds of SKUs; pilots in 2024 demonstrated inventory-aware optimization that rebalanced prices across channels and reduced discount leakage by up to 22%. Decision orchestration layers coordinate pricing, promotions and inventory actions; orchestration adoption rose as firms sought to prevent channel cannibalization and automate promotion sequencing. Explainable AI is critical: vendors increasingly provide model interpretability dashboards and feature-attribution logs so finance and audit teams can validate price decisions; in 2024, 49% of enterprise customers required built-in explainability. Cloud-native microservices architectures dominate new deployments—offering horizontal scalability and faster release cycles—while edge compute and CDN integration reduce latency for hyper-local pricing. Integration is also evolving: prebuilt connectors for major ERPs, subscription platforms, booking engines and payment processors accelerate pilots, with average pilot-to-production timelines shortening to 3–6 months for midmarket cloud implementations. For decision-makers, technical selection criteria should prioritize data governance, model lifecycle management (MLOps), cross-system orchestration, and vendor commitments to model transparency and auditability.

• In February 2024, PROS reported full-year 2023 subscription revenue growth and expanded cloud deployments for airlines and industrial clients, highlighting increased adoption of AI-driven pricing engines. Source: www.pros.com

• In November 2024, Zilliant released a major product update that automated customer-specific pricing within CPQ workflows, improving seller quote velocity and reducing manual price exceptions. Source: www.zilliant.com

• In January 2024, Vendavo announced expanded AI-powered pricing innovations and a partner program after reporting strong 2023 recurring revenue growth and increased enterprise deployments. Source: www.vendavo.com

• In November 2023, IDeaS served as a platinum sponsor for the 2024 Global Revenue Forum and announced new hospitality-focused revenue optimization features targeted at multi-property rollouts. Source: www.ideas.com

This report covers the global Automated Revenue Management market across product types, applications, deployment models and geographies. Product types include pricing optimization engines, demand forecasting tools, revenue leakage detection systems, and revenue orchestration platforms. Applications span travel & hospitality, retail & e-commerce, SaaS/subscription businesses, telecommunications, logistics and industrial distribution. Deployment models analyzed include cloud-native SaaS, hybrid cloud, and on-premises solutions, with an emphasis on integration patterns, prebuilt connectors and implementation timelines.

Geographic coverage includes North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with region-level analysis of deployment density, cloud adoption rates, and regulatory considerations. Functional focus areas encompass elasticity modeling, MLOps and model governance, explainable AI and auditability, real-time ingestion architectures, and revenue orchestration. The report also examines vendor landscapes, including large enterprise suites, specialized pricing vendors, and verticalized hospitality or airline revenue-management firms, profiling innovation strategies, partnership ecosystems, and go-to-market models. For decision-makers, the scope includes evaluation criteria such as integration maturity, time-to-value metrics, support for regulatory reporting, and enterprise security standards, highlighting opportunities in underpenetrated regions and advanced use cases—dynamic bundling, cross-channel orchestration, and elasticity-driven profit optimization.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 18,472.5 Million |

|

Market Revenue in 2032 |

USD 44,446.7 Million |

|

CAGR (2025 - 2032) |

11.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

PROS Holdings, Inc., Zilliant, Inc., Oracle Corporation, SAP SE, Vendavo, Inc., Pricefx, IDeaS Revenue Solutions (a SAS company), Amadeus IT Group, Revionics (TI Media), Accenture (Revenue Management Services), Apttus / Conga, ClearDemand, BeyondPricing, Perfect Price, RevControl, HotelREZ |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |