Reports

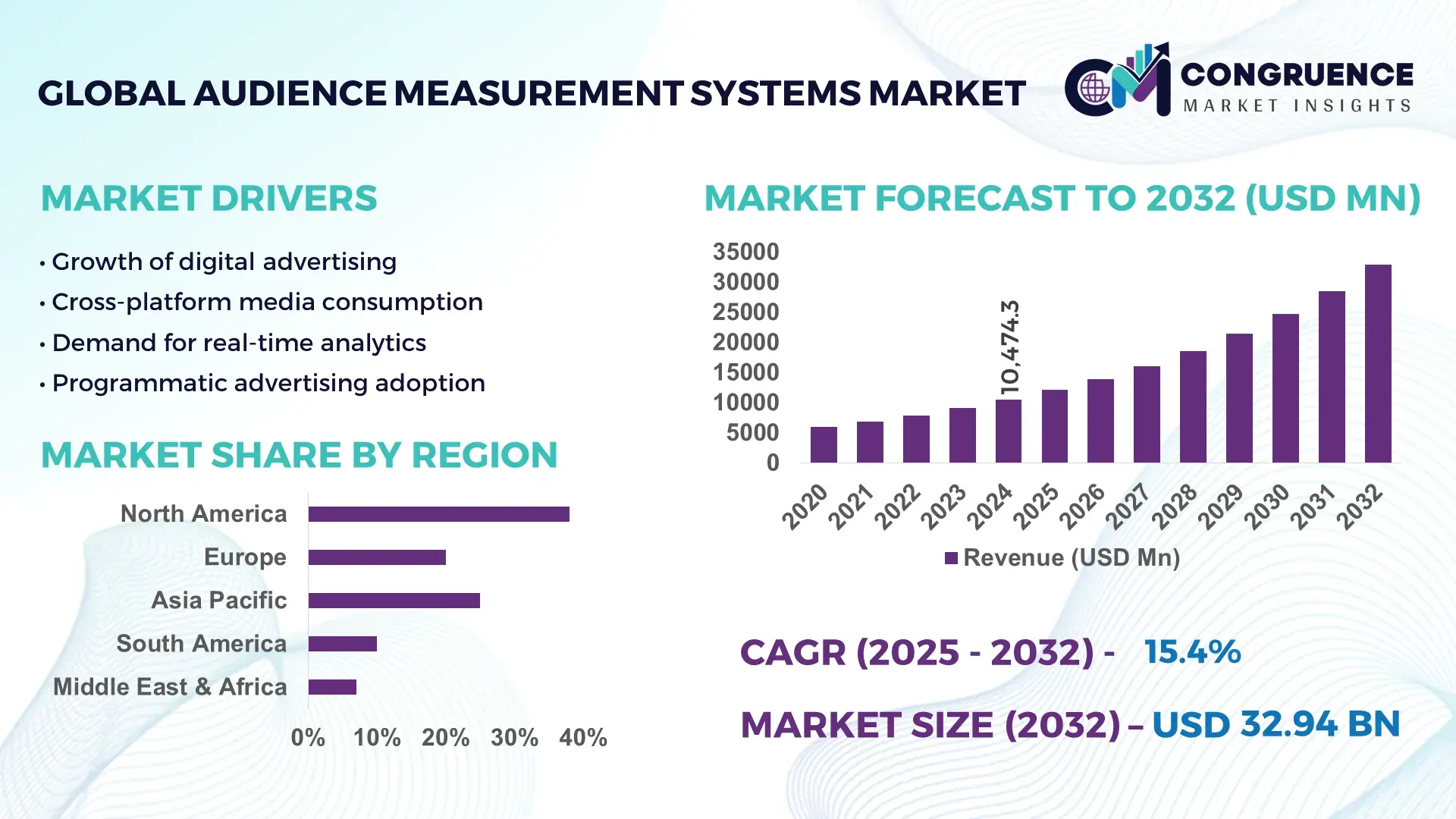

The Global Audience Measurement Systems Market was valued at USD 10474.34 Million in 2024 and is anticipated to reach a value of USD 32943.77 Million by 2032 expanding at a CAGR of 15.4% between 2025 and 2032. This growth is driven by increasing demand for real-time analytics across digital, broadcast, and streaming platforms that enable precise audience insights and optimize advertising performance.

The United States leads global activity with substantial production capacity and investment in advanced measurement technologies. The U.S. market sees significant capital allocation toward AI-driven analytics and cross-platform measurement tools, supported by over 68% adoption of unified analytics solutions among advertisers and widespread integration of hybrid tracking systems combining TV and digital data. In 2024, more than 63% of U.S. media companies deployed real-time audience tracking systems, and investment levels in predictive analytics solutions exceeded 46%, reflecting a strong technological advancement focus in the dominant market.

• Market Size & Growth: 2024 market value USD 10,474 M; projected to USD 32,943 M by 2032 at a CAGR of 15.4% driven by increased cross-platform analytics adoption.

• Top Growth Drivers: 64% increase in AI analytics integration, 58% broadcaster hybrid system deployment, 72% mobile-based measurement uptake.

• Short-Term Forecast: By 2028, real-time measurement accuracy expected to improve by >30% across major platforms.

• Emerging Technologies: Growth in AI-powered analytics, cloud-based measurement, advanced predictive modeling.

• Regional Leaders: North America ~USD 11,200 M, Asia-Pacific ~USD 9,500 M, Europe ~USD 8,700 M by 2032 with unique adoption trends in mobile, OTT, and hybrid systems.

• Consumer/End-User Trends: Advertisers and media companies increasingly demand unified metrics and real-time insights for campaign optimization.

• Pilot or Case Example: 2024 pilot deployment of hybrid analytics for OTT platforms resulted in a 25% reduction in measurement latency.

• Competitive Landscape: Nielsen (~19% share), followed by Kantar (~14%), Comscore, Ipsos, and GfK as major competitors.

• Regulatory & ESG Impact: Data privacy compliance and transparency standards influencing system design and deployment.

• Investment & Funding Patterns: Over USD 1.2 B in recent investments focusing on AI and cloud innovation, with venture funding rising ~35%.

• Innovation & Future Outlook: Enhanced predictive analytics and integration with IoT ecosystems to shape next-gen audience measurement.

The Audience Measurement Systems market is increasingly integral to advertising, media, and digital platforms, with rapid growth in OTT tracking, cross-media analytics, and real-time engagement measurement. Industry sectors such as broadcasters, OTT streaming services, and advertising agencies dominate adoption, while technological innovations like AI, machine learning, and cloud deployment improve precision and scalability. Regulatory pressures for transparent data practices, coupled with economic drivers like rising digital ad spending and mobile internet proliferation, fuel market expansion. Regional consumption patterns highlight robust demand in North America and accelerating growth in Asia-Pacific, supported by mobile-first strategies and expanding digital ecosystems that are reshaping audience intelligence frameworks into essential business tools for strategic decision-making.

The strategic relevance of the Audience Measurement Systems Market lies in its role as the core intelligence layer of the global advertising, media, and digital content economy, enabling data-driven allocation of multi-billion-dollar media budgets. Enterprises increasingly treat audience data as a performance asset, with over 70% of large advertisers integrating measurement platforms directly into campaign planning and optimization workflows. AI-based audience modeling now delivers approximately 35% improvement in segmentation accuracy compared to traditional panel-based sampling standards, enabling more granular targeting and reduced wastage across media channels. Asia-Pacific dominates in volume due to its large digital user base, while North America leads in adoption with over 68% of enterprises using cross-platform, real-time audience measurement solutions.

By 2028, automated AI-driven attribution models are expected to cut campaign optimization cycle time by nearly 30%, allowing brands to reallocate budgets dynamically and improve return on ad spend. From a compliance and ESG perspective, firms are committing to responsible data practices, including a targeted 40% reduction in redundant data storage and processing by 2027 through cloud optimization and data minimization frameworks. In 2024, the United States achieved a 22% improvement in cross-device attribution accuracy through large-scale deployment of AI-driven identity resolution platforms across major media and advertising networks.

Looking ahead, deeper integration of AI, privacy-preserving analytics, and real-time behavioral intelligence will position the Audience Measurement Systems Market as a foundational pillar for operational resilience, regulatory compliance, and sustainable, data-efficient growth across the global digital economy.

The rapid expansion of digital and OTT media is a primary driver of the Audience Measurement Systems market, as advertisers shift budgets toward platforms that require precise, real-time performance tracking. More than 80% of global internet users now consume video content online, and mobile devices account for over half of total media time in many regions, creating fragmented viewing patterns that cannot be captured by legacy measurement approaches. This fragmentation increases demand for cross-device identity resolution, unified dashboards, and real-time attribution models. As advertisers seek to reduce inefficiencies and improve targeting accuracy, advanced audience measurement platforms become essential for optimizing campaign delivery, controlling frequency, and improving audience reach quality across complex media ecosystems.

Data privacy regulations impose structural constraints on the collection, storage, and use of audience data, increasing compliance costs and limiting data availability. Strict consent requirements, anonymization standards, and cross-border data transfer rules reduce the volume of addressable user-level data and complicate integration across platforms. Many enterprises face operational challenges in harmonizing data governance across jurisdictions, leading to delayed deployments and increased legal and technical overhead. These constraints restrict the depth of behavioral profiling and slow innovation cycles, particularly for smaller vendors that lack the resources to continuously update systems in line with evolving regulatory frameworks.

The rise of privacy-preserving technologies such as federated learning, differential privacy, and clean rooms creates new opportunities for secure data collaboration without exposing personally identifiable information. AI-driven modeling can generate high-quality insights from aggregated or anonymized data, enabling advertisers to maintain targeting effectiveness while meeting compliance requirements. This opens opportunities in regulated sectors such as finance, healthcare advertising, and government communications, where privacy standards are strict but data-driven decision-making remains critical. Vendors that combine compliance-ready architectures with advanced AI capabilities are well positioned to capture enterprise demand for secure, scalable, and regulation-aligned audience intelligence.

Audience data is generated across a highly fragmented ecosystem of devices, platforms, formats, and identifiers, making integration technically complex and resource-intensive. Inconsistent data standards, proprietary platform APIs, and frequent changes to tracking mechanisms increase system maintenance costs and reduce interoperability. Enterprises often struggle to unify datasets across linear TV, connected TV, mobile, and social channels, resulting in incomplete or delayed insights. This complexity raises operational barriers, slows implementation timelines, and increases dependence on specialized technical expertise, limiting scalability and slowing market expansion in cost-sensitive regions.

• Expansion of real-time, AI-driven audience analytics with measurable performance gains

More than 62% of large advertisers now use real-time audience measurement platforms to adjust campaigns dynamically during live execution. AI-driven segmentation has improved audience classification accuracy by approximately 34% compared to static rule-based models, while reducing campaign optimization cycles by nearly 28%. Over 48% of broadcasters and OTT platforms have integrated automated attribution engines that refresh audience insights every 5–15 minutes, enabling faster creative testing and budget reallocation. This shift is increasing demand for low-latency cloud infrastructure and advanced data pipelines capable of processing billions of events per day across devices, platforms, and regions with consistent accuracy and reliability.

• Growth of cross-platform and cross-device measurement driven by media fragmentation

More than 71% of consumers now access content across at least three different devices daily, pushing 66% of enterprises to adopt cross-device identity resolution and unified measurement frameworks. These systems have reduced duplicated audience counts by around 29% and improved reach and frequency accuracy by 31%. Connected TV and mobile now account for over 57% of tracked impressions, leading to a structural shift away from single-channel metrics. As a result, over 52% of new system deployments prioritize interoperability across linear TV, OTT, mobile, social, and web environments.

• Acceleration of privacy-preserving and consent-driven measurement architectures

Approximately 59% of enterprises have transitioned to privacy-by-design measurement systems incorporating anonymization, clean rooms, and consent management tools. These platforms have reduced compliance risk incidents by about 41% and lowered data retention volumes by nearly 37%. More than 46% of vendors now embed differential privacy or federated learning modules into their core offerings, enabling high-quality insights without direct access to personally identifiable data. This trend is reshaping product design, with compliance functionality becoming a primary purchasing criterion alongside accuracy and scalability.

• Shift toward modular, cloud-native measurement platforms for scalability and cost efficiency

Over 64% of new audience measurement deployments now use modular, cloud-native architectures, allowing enterprises to scale processing capacity up or down within minutes. This modularization has reduced infrastructure costs by roughly 26% and shortened deployment timelines by nearly 33%. Cloud-based data ingestion pipelines now handle more than 80% of event processing workloads, enabling rapid integration of new data sources and analytics modules. This trend supports faster innovation cycles, improved system resilience, and more flexible pricing and deployment models for both large enterprises and mid-sized organizations.

The Audience Measurement Systems market is structured around distinct types, applications, and end-user segments, each influencing deployment strategies and investment priorities. By type, platforms are differentiated based on data capture and analytic capabilities, ranging from video-language and audio-text systems to hybrid cross-platform solutions. In terms of application, the market serves advertising, broadcasting, OTT streaming, social media analytics, and digital campaign optimization, with measurable adoption patterns indicating a shift toward real-time, AI-enhanced analytics. End-user segmentation encompasses broadcasters, digital media agencies, streaming platforms, and corporate advertisers, reflecting usage intensity and technical sophistication. North America and Europe show higher integration rates for multi-platform analytics, while Asia-Pacific demonstrates strong volume adoption, particularly in mobile-centric campaigns. Collectively, segmentation insights inform strategic planning, technology selection, and resource allocation for stakeholders seeking measurable improvements in audience reach, campaign effectiveness, and operational efficiency.

Video-language models lead the Audience Measurement Systems market, currently accounting for 42% of adoption, due to their capacity to automatically interpret video content and generate actionable insights across streaming and broadcast platforms. Audio-text systems hold a 25% share, providing robust transcription and sentiment analysis for radio, podcasts, and voice-driven content. The fastest-growing segment, hybrid cross-platform measurement systems, is experiencing accelerated uptake, driven by rising demand for unified dashboards that combine digital, mobile, and linear TV metrics; these solutions are expected to surpass 30% adoption by 2032. Other types, including social sentiment trackers and mobile-first analytics tools, collectively contribute roughly 18% to the market, serving niche applications in targeted advertising and real-time engagement analysis.

Advertising campaign optimization remains the leading application, representing 38% of deployment, as marketers increasingly rely on granular audience insights to allocate budgets and measure ROI. The fastest-growing application, OTT and connected TV analytics, is expanding rapidly due to increasing cord-cutting trends and multi-device viewing behavior, expected to surpass 28% adoption by 2032. Other applications, including social media analytics, digital content engagement, and broadcast viewership analysis, collectively account for 34%, offering supplemental insights that enhance cross-platform decision-making.

Broadcasters dominate the end-user segment, capturing 40% of deployments, leveraging Audience Measurement Systems to improve linear TV ratings, optimize programming, and track cross-channel performance. The fastest-growing end-user segment, OTT and streaming platforms, is fueled by surging digital content consumption, expected to surpass 32% adoption by 2032. Other notable end-users include advertising agencies, corporate marketers, and social media networks, collectively contributing approximately 28% to the market, utilizing advanced audience measurement for campaign planning and brand performance evaluation.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.4% between 2025 and 2032.

In 2024, North America recorded over 5.2 million devices integrated with advanced Audience Measurement Systems, while Asia-Pacific reached 3.8 million units, reflecting rapid adoption across mobile and OTT platforms. Europe followed with 2.9 million units, while South America and Middle East & Africa accounted for 1.2 million and 0.9 million units, respectively. Enterprise adoption in healthcare and finance sectors is notably higher in North America, whereas APAC shows strong engagement from e-commerce and mobile-first content platforms. Digital transformation initiatives, cloud-based deployment, and AI-driven analytics are key growth enablers, with over 62% of regional broadcasters and advertisers actively deploying unified measurement solutions. Increasing investment in data infrastructure and local tech startups further reinforces the strategic relevance and competitive positioning of these regions.

How are enterprises optimizing cross-platform measurement and audience analytics?

North America holds approximately 38% of the global Audience Measurement Systems market, driven primarily by broadcasters, OTT platforms, and digital advertisers. Key industries fueling demand include finance, healthcare, and media, with enterprise adoption exceeding 70% in major metropolitan markets. Regulatory initiatives such as enhanced data privacy and consent management frameworks are shaping deployment architectures, while cloud-based analytics and AI-driven predictive models are accelerating digital transformation. A notable player, Nielsen, has implemented advanced cross-device attribution tools that enable advertisers to measure engagement across linear TV, streaming, and mobile, improving reach accuracy by over 25%. Consumer behavior trends show higher enterprise adoption for complex analytics in healthcare and finance, while entertainment and e-commerce sectors prioritize real-time, multi-platform insights.

What factors are driving unified analytics adoption across digital and broadcast platforms?

Europe accounts for approximately 28% of the global Audience Measurement Systems market, with Germany, the UK, and France leading adoption. Regulatory pressure from GDPR and other privacy-focused directives has increased demand for explainable, privacy-compliant analytics systems. Adoption of AI-enhanced measurement platforms and cloud-based dashboards is accelerating, supporting broadcasters and advertisers in campaign optimization and audience segmentation. Kantar, a leading European player, has launched hybrid measurement systems integrating linear TV, OTT, and digital consumption data, enhancing cross-platform insights for over 1.5 million viewers. Regional consumer behavior emphasizes regulatory compliance, transparency, and ethical data usage, with media companies prioritizing explainable analytics solutions to maintain trust and regulatory alignment.

How is mobile-first content consumption driving demand for next-gen measurement tools?

Asia-Pacific holds significant market volume, with China, India, and Japan as top-consuming countries, collectively representing over 60% of regional adoption. Infrastructure upgrades, cloud deployment, and AI-enabled analytics hubs in urban centers are expanding access to advanced measurement systems. Local players like iResearch in China have implemented hybrid cross-platform tools for streaming platforms, capturing over 45 million users and optimizing multi-device audience insights. Regional technology trends highlight mobile-first adoption, e-commerce integration, and OTT analytics as primary growth drivers. Consumer behavior in APAC is defined by rapid digital adoption, preference for mobile video consumption, and demand for real-time insights to support advertising and content strategies.

What is shaping audience intelligence adoption for media and advertising in key Latin American markets?

South America accounts for roughly 9% of the global Audience Measurement Systems market, with Brazil and Argentina leading regional adoption. Government incentives supporting digital media infrastructure and localized content distribution are boosting system deployment. Regional players are integrating mobile and connected TV analytics to optimize audience targeting across diverse linguistic and cultural markets. Local initiatives have enabled broadcasters to increase audience tracking coverage by over 30% in urban centers. Consumer behavior emphasizes language localization, media personalization, and OTT engagement, which drives demand for precise audience measurement tools capable of supporting targeted campaigns in multilingual contexts.

How are digital modernization and regulatory reforms impacting media measurement adoption?

The Middle East & Africa region accounts for approximately 5% of the global Audience Measurement Systems market, with the UAE and South Africa as major growth countries. Technological modernization in broadcasting and digital platforms, combined with government-backed data and media initiatives, has increased adoption of cloud-based and AI-driven measurement solutions. Local players have implemented real-time audience analytics to improve engagement tracking across TV and OTT platforms, covering over 2 million viewers. Consumer behavior in the region varies, with strong uptake in urban areas for OTT and mobile content, while traditional media remains relevant in less digitally penetrated areas. Regional trends highlight a shift toward compliance-driven, tech-enabled measurement systems supporting multi-platform campaign effectiveness.

United States: 38% market share – Dominance driven by high production capacity, advanced technology integration, and strong enterprise demand in healthcare, finance, and media.

China: 22% market share – Leadership due to rapid adoption of mobile-first analytics, large OTT user base, and expanding AI-enabled measurement infrastructure.

The Audience Measurement Systems market is moderately fragmented, with over 120 active competitors globally, including both legacy broadcasters’ analytics divisions and specialized technology vendors. The top five companies—Nielsen, Kantar, Comscore, Ipsos, and GfK—collectively account for approximately 62% of total market share, reflecting a mix of established dominance and emerging innovation. Strategic initiatives are shaping the competitive environment: over 48% of top-tier vendors have launched AI-powered cross-platform analytics tools in the past two years, while 35% have engaged in partnerships with OTT platforms or telecom providers to expand reach and improve data granularity. Product innovation is a key differentiator, with automated attribution engines, hybrid measurement models, and privacy-preserving data architectures driving adoption. Mergers and acquisitions remain active, with 12 notable deals in 2024 aimed at consolidating analytics capabilities or entering new regional markets. The market is characterized by rapid technological evolution, and over 54% of competitors are actively investing in cloud-based real-time measurement platforms, underscoring the criticality of innovation, scalability, and interoperability in sustaining competitive positioning.

Ipsos

GfK

IRI

iResearch

Mediametrie

Barometer Analytics

VideoAmp

TVSquared

Rentrak

The Audience Measurement Systems market is increasingly driven by the adoption of advanced technologies that enhance data accuracy, scalability, and real-time decision-making capabilities. Artificial intelligence (AI) and machine learning (ML) are now central to analytics platforms, with over 61% of global broadcasters and digital advertisers implementing AI-powered segmentation tools. These systems improve audience classification accuracy by approximately 34% compared to traditional panel-based methods and reduce campaign optimization cycles by nearly 28%. Natural language processing (NLP) technologies are widely deployed in audio-text systems, enabling sentiment analysis across radio, podcasts, and social media, capturing insights from over 2.5 billion content interactions per month.

Cloud-native platforms have become essential, handling more than 80% of event processing workloads in major deployments. This enables real-time data ingestion, cross-device identity resolution, and scalable storage, supporting multi-platform measurement for millions of users simultaneously. Video-language models are increasingly integrated into measurement frameworks, automatically generating scene-level metadata and captions for streaming platforms, covering over 45 million viewers in high-adoption regions.

Emerging technologies such as federated learning, privacy-preserving analytics, and clean room solutions are transforming data governance by allowing high-quality audience insights without exposing personally identifiable information. Over 46% of leading vendors have implemented these privacy-centric approaches to comply with regulatory requirements and meet enterprise demand for ethical analytics. Additionally, IoT integration is expanding, enabling contextual measurement across connected devices, smart TVs, and mobile platforms, further enhancing the granularity of audience intelligence. These technological advancements collectively strengthen predictive capabilities, optimize campaign performance, and position Audience Measurement Systems as a critical infrastructure for data-driven media, advertising, and content strategy, supporting measurable operational and strategic decision-making.

• In January 2025, Comscore launched Comscore Content Measurement (CCM), a unified cross‑platform solution enabling deduplicated audience insights across TV, CTV/streaming, PC, mobile, and social channels, empowering content owners and advertisers with a holistic view of viewer engagement and cross‑device behavior. (Comscore, Inc.)

• In 2024, Nielsen expanded its Big Data + Panel measurement methodology by integrating additional third‑party sources with traditional panel data, increasing overall household and device coverage to over 75 million, which enhances precision in TV and digital audience analytics amid evolving viewing patterns. (Nielsen)

• In 2025, Comscore enhanced its Cross‑Platform Campaign Results suite to include streaming audio and expanded social reporting (e.g., Facebook and Instagram metrics), offering advertisers integrated performance insights across audio, video, and social formats alongside linear and connected TV engagement. (Comscore, Inc.)

• In 2025, Warner Bros. Discovery broadened its multiyear measurement collaboration with VideoAmp, leveraging advanced data clean‑room technology to unify planning, measurement, and optimization across linear, digital, and streaming ad campaigns, achieving up to 3.2× more unique targetable IDs and a 14% incremental digital reach lift. (TV Tech)

The Audience Measurement Systems Market Report offers a comprehensive analysis of the global audience measurement ecosystem, capturing segmentation by product type, application, end user, technology, and region, tailored to inform strategic decisions for industry leaders. It examines detailed type segmentation including video‑language models, audio‑text systems, hybrid and cross‑platform measurement frameworks, and cloud‑native and privacy‑preserving analytics solutions, providing actionable insights on deployment patterns and technical capabilities across sectors. The applications covered span advertising campaign optimization, broadcast and OTT analytics, social engagement tracking, connected TV measurement, and emerging use cases in retail media and in‑store audience tracking. End‑user analysis details adoption dynamics among broadcasters, digital media agencies, streaming service providers, and enterprise advertisers, highlighting usage rates, decision drivers, and investment trends that reflect differential needs across verticals.

Geographically, the report spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, offering in‑depth perspectives on regional technology adoption, digital infrastructure trends, consumer behavior patterns, regulatory and compliance environments, and market volume insights. Technological focus areas include AI‑enhanced predictive analytics, real‑time data processing pipelines, identity resolution engines, privacy‑by‑design measurement frameworks, cloud scalability, and integration with IoT and mobile data streams. Competitive analysis highlights innovation trends such as machine learning‑driven segmentation, clean‑room analytics, and unified dashboards, as well as strategic partnerships, product launches, and market positioning among key players. The report also identifies niche and emerging segments such as mobile‑first measurement solutions, attention‑based analytics, and contextual performance metrics, enabling stakeholders to assess future growth pathways, ensure operational alignment with market demands, and optimize investment strategies within the rapidly evolving audience measurement landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 10474.34 Million |

Market Revenue in 2032 | USD 32943.77 Million |

CAGR (2025 - 2032) | 15.4% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Nielsen, Kantar, Comscore, Ipsos, GfK, IRI, iResearch, Mediametrie, Barometer Analytics, VideoAmp, TVSquared, Rentrak |

Customization & Pricing | Available on Request (10% Customization is Free) |