Reports

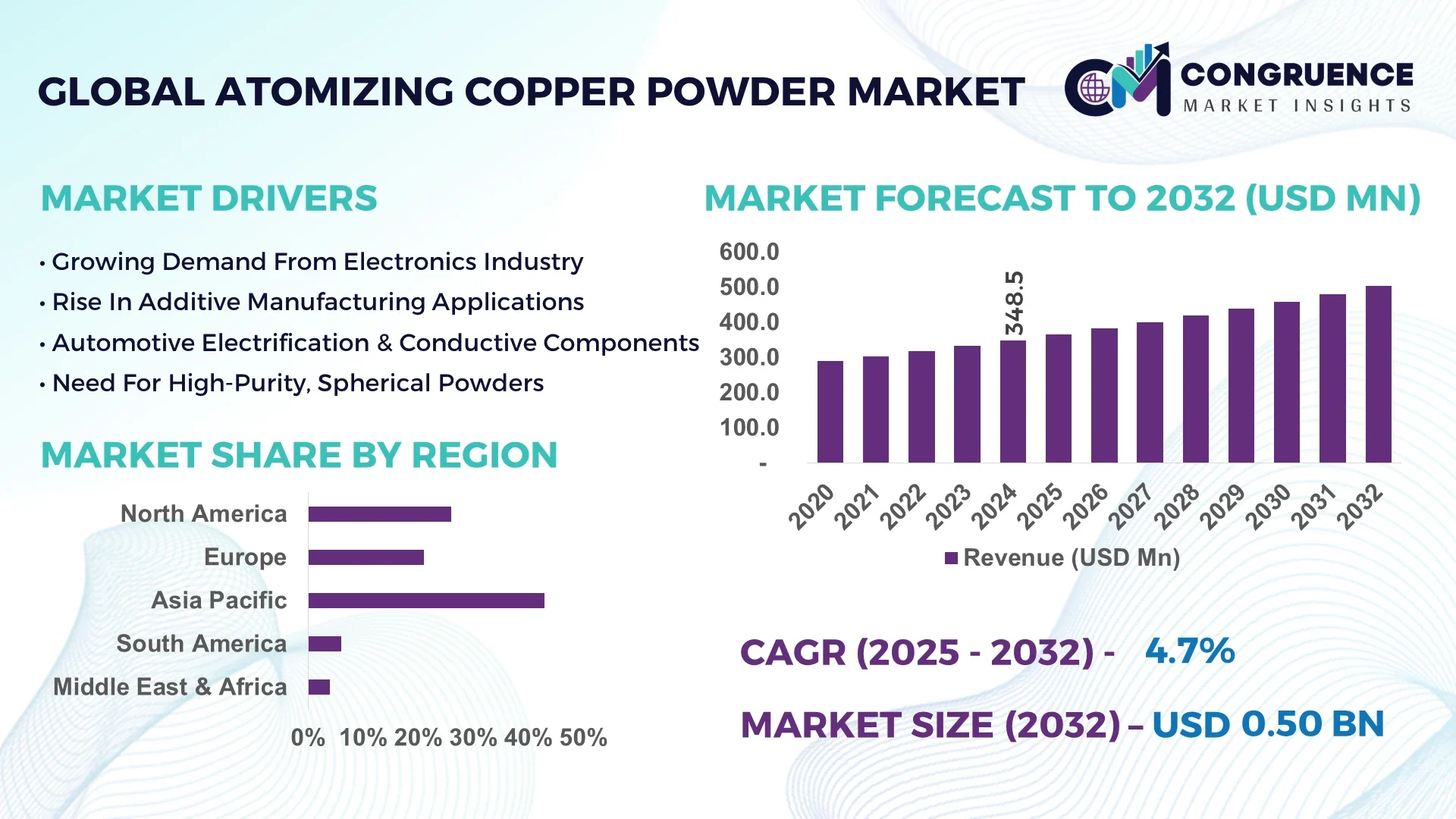

The Global Atomizing Copper Powder Market was valued at USD 348.54 Million in 2024 and is anticipated to reach a value of USD 503.3 Million by 2032 expanding at a CAGR of 4.7% between 2025 and 2032.

In China, manufacturing of atomizing copper powder has scaled with advanced production facilities incorporating high-pressure gas and water atomization lines. Substantial investments in R&D have enabled integrated pilot plants leveraging robotics for continuous powder refinement, supporting key sectors such as additive manufacturing, electrical components, and conductive alloys, while pioneering improvements in particle uniformity through real-time process monitoring.

Key industry sectors driving the Atomizing Copper Powder Market include metallurgy, where powders are used for alloy reinforcement and sintered components; electronics, for conductive inks, pastes, printed circuit substrates, and intricate electromagnetic parts; and chemical applications as catalysts and pigment formulations. Recent technological innovations such as ultrasonic atomization platforms with modular frequency control and closed-loop inert-gas handling have enhanced powder sphericity, flowability, and purity for additive manufacturing. Regulatory and economic drivers include rising demand for sustainable, high-precision materials, coupled with incentives for energy-efficient production processes. Environmental factors such as circular-economy reuse of scrap feedstock and tighter emissions controls are influencing manufacturing approaches. Regionally, Asia Pacific shows robust consumption growth, particularly in electronics hubs, while North America and Europe are advancing in aerospace and EV applications. Emerging trends involve miniaturized atomization systems adapted for R&D labs, integration of smart monitoring, and expanding use of copper powders in next-generation heat exchangers and electronic components—offering a dynamic outlook for strategic investment and innovation within the industry.

Artificial intelligence is revolutionizing the Atomizing Copper Powder Market through smart automation of atomization processes and advanced analytics. AI-driven optimization tools analyze real-time sensor data—such as melt temperature, gas pressure, and droplet formation—to fine-tune atomization parameters, resulting in consistent particle size distribution and improved batch repeatability. Machine-learning models predict equipment wear or clogging, enabling pre-emptive maintenance that reduces downtime and enhances yield. In additive manufacturing settings, AI algorithms optimize powder feedstock selection based on performance characteristics, accelerating the qualification of materials for demanding electronics or aerospace parts.

AI-empowered quality control systems inspect powder morphology using computer vision, detecting anomalies—like irregular sphericity or contamination—that traditional inspection may miss, ensuring higher reliability in downstream sintering or printing processes. Furthermore, AI integrates production scheduling with energy data, reducing power consumption during high-intensity steps like melting and atomization, thus improving operational sustainability. By leveraging predictive insights, manufacturers can adapt atomization recipes for new alloy formulations without extensive trial runs, shortening time-to-market for specialty powders. These AI applications significantly elevate operational performance, process optimization, and cost-effective scalability in the Atomizing Copper Powder Market while maintaining rigorous quality standards for industry professionals and decision-makers.

“In 2024, ultrasonic atomization workflows were enhanced with the ATO Suite platform, which integrates modular ultrasonic atomizers and auxiliary vacuum casting, sieving, and feedstock handling devices into a unified, remote-controlled production line—delivering precise particle-size control and enabling recycling of scrap copper to reusable powder via circular-economy processing.”

The Atomizing Copper Powder Market is shaped by technological advancements, evolving industrial applications, and shifting regional consumption trends. Demand growth is influenced by the expansion of additive manufacturing, precision electronics, and sustainable metallurgy. Manufacturers are increasingly adopting advanced atomization methods—such as high-pressure gas atomization and ultrasonic systems—to produce powders with superior purity, sphericity, and flow characteristics. Environmental regulations are pushing producers toward greener production techniques, including energy-efficient furnaces and recycling of copper scrap into atomized powder. Global trade patterns and supply chain modernization also play a crucial role, as major economies invest in high-performance copper powder applications for sectors like aerospace, electric vehicles, and renewable energy systems.

The accelerating shift toward electric mobility and renewable power systems is driving substantial growth in the Atomizing Copper Powder Market. Copper powders are essential in manufacturing high-conductivity components for EV motors, battery connectors, and charging infrastructure. In renewable energy, atomized copper is utilized in solar cell contacts, wind turbine electrical systems, and high-efficiency heat exchangers. With global EV sales surpassing 14 million units in 2024 and renewable installations reaching record highs, the demand for precision-engineered copper powders has increased significantly. These applications require powders with specific particle size distributions and enhanced conductivity, achievable through modern atomization technologies, thus propelling market expansion.

Volatility in copper prices presents a key restraint for the Atomizing Copper Powder Market, impacting production costs and profit margins. Global copper supply is sensitive to mining output fluctuations, geopolitical tensions, and trade restrictions, which can lead to unpredictable pricing. In addition, increased competition for high-grade copper from infrastructure and energy sectors puts additional pressure on supply availability for powder production. Manufacturers face challenges in securing stable feedstock at consistent quality, and price spikes can force end-users to explore alternative conductive materials. These supply chain uncertainties necessitate strategic sourcing and inventory management, but they still act as a limiting factor for market growth.

The growing integration of atomized copper powders in additive manufacturing presents a significant opportunity for market expansion. Copper’s exceptional thermal and electrical conductivity makes it ideal for 3D-printed components in aerospace, defense, medical devices, and high-performance electronics. Recent advancements in laser-based printing systems have improved the compatibility of copper powders, overcoming previous challenges with reflectivity and heat absorption. Governments and industries are investing in localized production hubs for 3D-printed copper parts, reducing lead times and enabling rapid prototyping. This shift toward customized, high-precision copper components is set to expand the customer base for powder producers and stimulate innovation in alloy development.

Producing atomized copper powder is energy-intensive, especially when using gas or ultrasonic atomization techniques that require high-temperature melting and pressurized systems. Energy costs represent a significant portion of operational expenditure, particularly in regions with fluctuating power tariffs. Additionally, decarbonization pressures and stricter environmental policies are compelling manufacturers to adopt cleaner, more efficient technologies—often involving substantial capital investments. Balancing cost control with the need to meet sustainability targets remains a complex challenge. Furthermore, maintaining consistent powder quality while reducing energy usage demands precision process control and technological upgrades, adding to the operational complexity in the Atomizing Copper Powder Market.

Rise in Modular and Prefabricated Construction: The expansion of modular and prefabricated construction is significantly impacting the Atomizing Copper Powder Market. Copper powders are increasingly used in high-conductivity joints, precision connectors, and conductive coatings for prefabricated modules. Automated fabrication lines integrate atomized copper components to streamline off-site assembly, reducing labor requirements and enhancing quality control. In Europe and North America, regulatory pushes for faster, more energy-efficient construction are fueling adoption, with large-scale housing and infrastructure projects specifying advanced copper-based components for performance and durability.

Integration of Ultrasonic Atomization for Premium Alloys: Ultrasonic atomization is gaining momentum as manufacturers target ultra-fine, spherical copper powders for specialized applications. This trend is particularly strong in aerospace and medical device production, where powder flowability and purity are critical. Adoption rates are rising in Japan and Germany, where manufacturers are upgrading facilities to incorporate modular ultrasonic lines capable of producing micro-sized particles with consistent morphology, enabling new high-precision applications in conductive microstructures and miniaturized electronics.

Advancements in Powder Recycling and Circular Economy Practices: Manufacturers are implementing closed-loop recycling systems to recover copper from scrap and production waste, converting it into reusable atomized powders. This shift not only reduces environmental impact but also stabilizes feedstock supply in volatile markets. Facilities in Asia-Pacific are leading innovations by integrating AI-powered sorting and refinement systems that ensure recycled powders meet stringent quality standards, broadening their use in automotive and industrial electronics manufacturing.

Adoption of AI-Driven Quality Assurance Systems: AI-based monitoring solutions are transforming quality assurance in the Atomizing Copper Powder Market. These systems analyze real-time data during atomization to detect deviations in particle size, sphericity, and surface composition, ensuring tighter tolerance levels. Implementation in high-volume plants across China and the U.S. has reduced defect rates and improved operational efficiency, directly supporting the production of powders suitable for demanding additive manufacturing and high-frequency electronics applications.

The Atomizing Copper Powder Market is segmented by type, application, and end-user, reflecting the diverse industrial roles copper powders fulfill. Product types range from high-purity spherical powders to dendritic and irregular morphologies, each suited for specific performance requirements. Applications span from conductive pastes and additive manufacturing to metallurgy and chemical catalysts, with notable growth in sectors demanding precision-engineered materials. End-user categories include electronics, automotive, aerospace, and industrial machinery, each influencing market demand through technological advancements and evolving product specifications. This segmentation highlights both established demand centers and emerging high-growth niches, enabling targeted strategies for manufacturers seeking to expand their competitive position.

High-purity spherical copper powder represents the leading product category, driven by its exceptional flowability and uniform packing density, which are critical for additive manufacturing and high-precision electronics. These powders are widely preferred in 3D printing due to their consistent particle morphology and superior thermal conductivity. The fastest-growing segment is fine dendritic copper powder, supported by rising demand in conductive ink and paste applications for flexible electronics and printed circuit boards. Irregular copper powders hold niche relevance in friction materials and brazing applications, where particle shape enhances mechanical bonding. Ultra-fine atomized powders are also gaining traction in thermal management solutions for advanced computing and power electronics, while composite copper-based powders find application in wear-resistant components. This diversity in types reflects the market’s adaptability to both traditional metallurgical uses and cutting-edge manufacturing technologies.

Electronics manufacturing leads the Atomizing Copper Powder Market, with demand fueled by the production of conductive inks, thermal interface materials, and advanced PCB substrates. Copper powder’s high conductivity and compatibility with precision printing make it indispensable in this sector. Additive manufacturing is the fastest-growing application, as aerospace, automotive, and industrial design companies adopt 3D-printed copper parts for customized, high-performance components. Metallurgy remains a stable application area, leveraging copper powder for sintered parts and alloy development in automotive and industrial machinery. In chemical processing, copper powder serves as a catalyst for specialized reactions, while its role in coatings and surface treatments supports industries requiring enhanced corrosion resistance. Each application segment reflects unique technical requirements, driving innovations in powder morphology and production processes to meet evolving performance standards.

The electronics sector is the leading end-user in the Atomizing Copper Powder Market, driven by the miniaturization of components, expansion of 5G infrastructure, and increasing production of high-density circuit boards. The fastest-growing end-user category is aerospace and defense, where lightweight, high-strength copper components are integral to advanced propulsion systems, avionics, and satellite technology. Automotive manufacturing maintains a strong position, with copper powders used in EV components, thermal management systems, and braking mechanisms. Industrial machinery producers also contribute to demand, utilizing copper powders in wear-resistant parts, heat exchangers, and precision tools. This end-user diversity reflects the material’s versatility, with growth trajectories shaped by sector-specific innovations, regulatory pressures, and global technological trends.

Asia-Pacific accounted for the largest market share at 43% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

The Asia-Pacific region benefits from high production capacity, well-established electronics manufacturing hubs, and expanding infrastructure investment, especially in China, Japan, and India. The region’s dominance is also supported by strong integration of atomized copper powders in automotive, industrial electronics, and renewable energy projects. North America’s growth momentum is being fueled by advancements in additive manufacturing, increasing EV production, and the adoption of energy-efficient copper-based components in industrial applications. Regulatory measures promoting sustainable manufacturing, coupled with advanced R&D facilities, position both regions as pivotal in shaping the global Atomizing Copper Powder Market landscape.

Technological innovation driving industrial copper powder applications

Holding approximately 26% of the global market volume, North America remains a hub for advanced manufacturing that heavily utilizes atomized copper powders. Key industries such as aerospace, defense, electric vehicles, and high-end electronics are major demand contributors. Government-backed initiatives to promote domestic manufacturing resilience and reduce reliance on imports have bolstered production. Regulatory measures focusing on reducing environmental impact are prompting investments in cleaner atomization processes. Digital transformation trends, including AI-driven quality monitoring and predictive maintenance in powder plants, are improving efficiency and reducing waste, enabling producers to meet stringent industry standards while maintaining competitive output levels.

Precision engineering and sustainable metallurgy boosting demand

With an estimated 21% market share, Europe’s atomizing copper powder demand is centered in Germany, the UK, and France, where high-tech manufacturing and precision engineering industries are prominent. The region benefits from EU sustainability policies and regulatory oversight by bodies promoting circular economy practices, pushing for recycled copper powder usage. Automotive electrification projects and industrial robotics are key demand drivers. Technological adoption, such as ultrasonic and inert-gas atomization, is improving powder purity and enabling more advanced applications in aerospace and renewable energy systems, further cementing the region’s role as a key innovator in specialized copper powder production.

Electronics dominance and manufacturing expansion fueling growth

Accounting for the largest market volume globally, this region is driven by strong consumption in China, Japan, and India. Demand is supported by massive electronics manufacturing ecosystems, large-scale infrastructure development, and growing electric vehicle production. The expansion of smart manufacturing hubs and integration of automation in powder atomization plants are improving product uniformity and production speed. Innovation hubs in Japan and South Korea are pioneering ultra-fine powder production for advanced semiconductors and miniaturized electronics. This combination of industrial scale, technological advancement, and diversified applications keeps the region at the forefront of the Atomizing Copper Powder Market.

Mining strength and industrial diversification supporting market expansion

Brazil and Argentina lead this region, collectively holding a moderate share of the global market. Strong copper mining operations provide abundant raw material supply, while growing adoption in industrial machinery and electrical component manufacturing boosts demand. Infrastructure modernization projects, particularly in transportation and renewable energy, are incorporating copper-based solutions. Government incentives for local manufacturing and reduced import tariffs on advanced production equipment are fostering investment in domestic atomization capabilities, enabling greater regional self-sufficiency and reduced reliance on imported copper powders.

Energy sector diversification and manufacturing modernization shaping demand

The regional market is gaining traction, led by countries such as the UAE and South Africa, where investments in oil & gas infrastructure, renewable energy projects, and construction are driving demand for high-conductivity copper components. Modernization of manufacturing facilities, including the adoption of automated atomization systems, is improving production efficiency. Trade partnerships within the Gulf Cooperation Council and African regional blocs are facilitating technology transfer and market access. Local regulations emphasizing sustainable material sourcing are influencing producers to integrate recycled copper into powder manufacturing, aligning with global environmental trends.

China – 34% market share – Dominates due to extensive electronics manufacturing capacity and large-scale copper powder production infrastructure.

United States – 18% market share – Leads in advanced additive manufacturing applications and strong aerospace and defense industry demand.

The Atomizing Copper Powder Market features a moderately consolidated competitive environment, with approximately 35–40 active global and regional players competing across various segments. Leading producers maintain strong market positioning through vertical integration, controlling both raw material sourcing and advanced atomization technologies. Competition is driven by innovation in powder morphology control, ultra-fine particle production, and environmentally sustainable manufacturing processes. Strategic initiatives such as joint ventures between technology providers and powder producers are becoming more common, enabling faster adoption of ultrasonic atomization, closed-loop recycling systems, and AI-based process monitoring. Several players are expanding capacity through new plant installations in high-demand regions like Asia-Pacific and North America, while others are targeting niche markets in aerospace-grade powders and high-purity electronics applications. Product differentiation based on sphericity, purity, and particle-size precision is a critical competitive lever, alongside supply chain reliability and the ability to meet stringent industry certifications. The market’s competitive intensity is further influenced by mergers and acquisitions aimed at consolidating expertise, reducing production costs, and expanding application portfolios.

GGP Metalpowder AG

Mitsui Mining & Smelting Co., Ltd.

Kymera International

Fukuda Metal Foil & Powder Co., Ltd.

Shanghai CNPC Powder Material Co., Ltd.

SCHLENK Metallic Pigments GmbH

Tongling Guochuan Electronic Material Co., Ltd.

Anhui Xujing Powder New-material Co., Ltd.

ALPA Powder Technology Co., Ltd.

GRIPM Advanced Materials Co., Ltd.

Technological advancements in the Atomizing Copper Powder Market are centered on improving powder uniformity, enhancing production efficiency, and reducing environmental impact. Gas atomization remains the most widely used process, utilizing high-pressure inert gases to produce spherical particles with excellent flow properties, particularly suited for additive manufacturing and high-performance electronics. Emerging ultrasonic atomization systems are gaining traction for their ability to generate ultra-fine powders under controlled conditions, achieving particle sizes below 10 microns with high purity—essential for microelectronic and advanced thermal management applications.

Closed-loop recycling technologies are being adopted to reclaim copper from production scrap, reducing waste and dependency on virgin materials. AI and machine learning integration in production facilities is enabling real-time monitoring of melt temperature, particle formation, and gas flow rates, resulting in defect reduction rates of up to 30%. Modular atomization units are also emerging, allowing producers to scale capacity flexibly and adapt to custom alloy production. Vacuum-assisted atomization is improving oxidation control, critical for maintaining electrical conductivity in powders for electronics. Furthermore, laser-assisted melting and hybrid atomization processes are being explored to produce specialty powders with tailored surface characteristics for niche applications such as wear-resistant coatings and catalytic systems. These advancements are reshaping production economics, quality assurance, and application capabilities across multiple industries.

In February 2024, Kymera International expanded its copper powder production facility in North Carolina by adding a high-capacity gas atomization line capable of producing over 1,200 tons annually, targeting aerospace-grade and high-purity electronics applications.

In October 2024, Shanghai CNPC Powder Material Co., Ltd. launched an AI-driven process monitoring system in its atomization plant, reducing powder defect rates by 25% and improving particle size consistency for additive manufacturing clients.

In May 2023, SCHLENK Metallic Pigments GmbH introduced an ultra-fine spherical copper powder series with an average particle size of 8 microns, designed for high-frequency electronic applications requiring low signal loss and improved thermal conductivity.

In December 2023, GGP Metalpowder AG installed a new vacuum-assisted atomization unit in its Swiss plant, enhancing oxidation control and enabling production of powders suitable for advanced conductive inks and microelectronics.

The Atomizing Copper Powder Market Report provides an in-depth examination of the industry’s structure, covering multiple market segments by type, application, end-user industry, and technology. Product segmentation includes high-purity spherical powders, dendritic powders, irregular powders, and ultra-fine grades, each serving distinct technical requirements across industries. Application coverage spans electronics manufacturing, additive manufacturing, metallurgy, catalysis, and coatings, with emphasis on their specific performance drivers and evolving technical specifications.

Geographically, the report analyzes major markets in Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, detailing regional demand trends, production capacities, and trade flows. The technology scope includes conventional gas and water atomization, ultrasonic and vacuum-assisted atomization, as well as hybrid and modular systems, highlighting their comparative advantages and innovation pathways. Special attention is given to digital transformation trends, including AI-driven process optimization, smart quality assurance systems, and closed-loop recycling technologies.

The report also assesses industry dynamics such as raw material availability, sustainability mandates, and regulatory frameworks influencing production and trade. It identifies emerging niches like microelectronics-grade ultra-fine powders and copper-based thermal interface materials for next-generation computing. This scope ensures a holistic view for stakeholders, enabling informed strategic planning, competitive benchmarking, and investment decisions in the global Atomizing Copper Powder Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 348.54 Million |

|

Market Revenue in 2032 |

USD 503.3 Million |

|

CAGR (2025 - 2032) |

4.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GGP Metalpowder AG, Mitsui Mining & Smelting Co., Ltd., Kymera International, Fukuda Metal Foil & Powder Co., Ltd., Shanghai CNPC Powder Material Co., Ltd., SCHLENK Metallic Pigments GmbH, Tongling Guochuan Electronic Material Co., Ltd., Anhui Xujing Powder New-material Co., Ltd., ALPA Powder Technology Co., Ltd., GRIPM Advanced Materials Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |