Reports

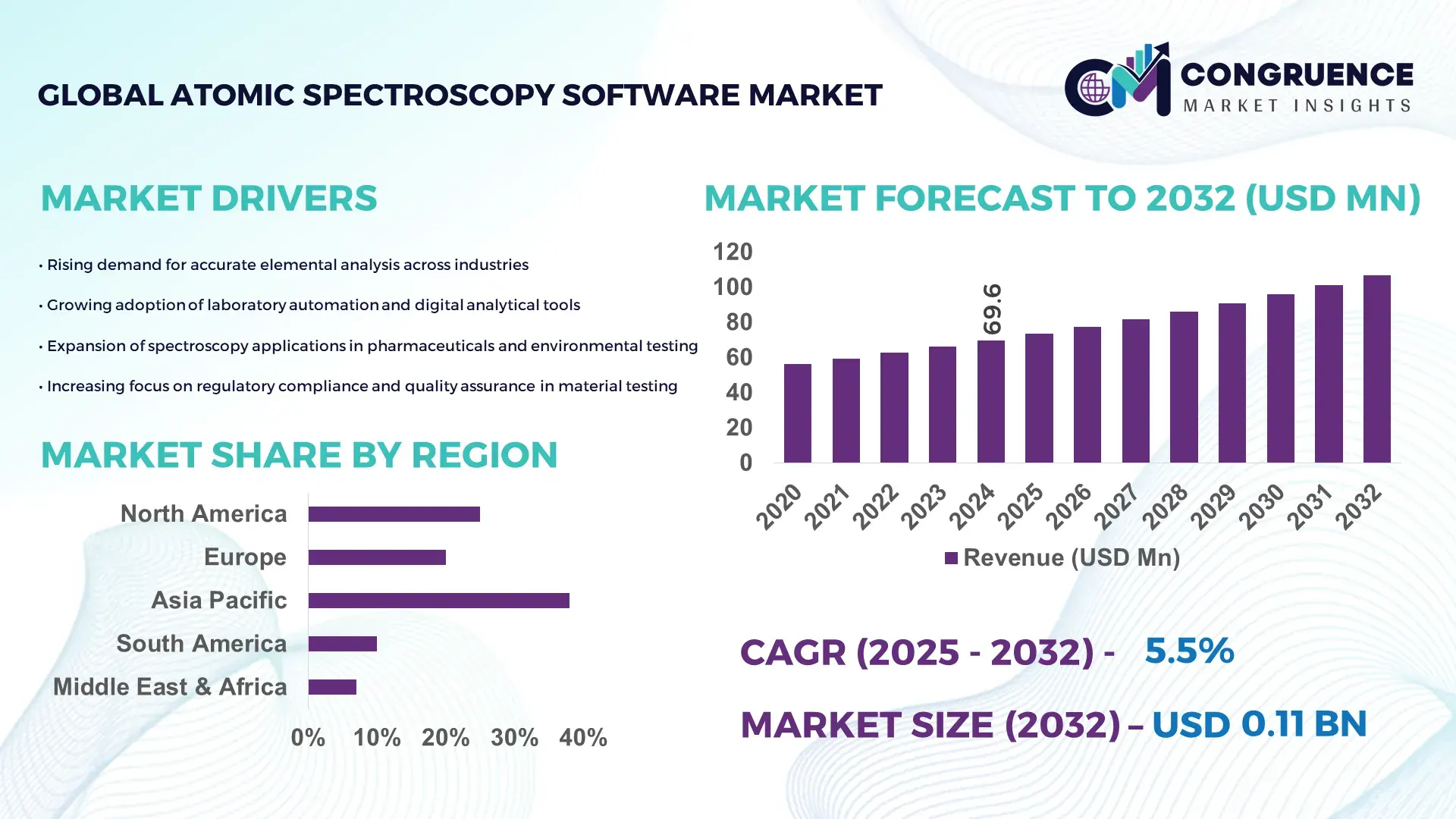

The Global Atomic Spectroscopy Software Market was valued at USD 69.63 Million in 2024 and is anticipated to reach a value of USD 106.86 Million by 2032 expanding at a CAGR of 5.5% between 2025 and 2032. Growth is primarily driven by rising automation in laboratory analytics and increasing demand for high-precision elemental analysis across industries.

The United States maintains the strongest footprint in the Atomic Spectroscopy Software landscape, supported by advanced R&D infrastructure, high deployment across pharmaceutical and environmental testing labs, and significant federal investments exceeding USD 18 billion annually in analytical science programs. The country hosts more than 420 accredited laboratories utilizing spectroscopy-driven workflows, alongside over 55% adoption of integrated cloud–software platforms in metals, chemicals, and semiconductor quality-control applications. Its technology ecosystem emphasizes algorithm optimization, automated calibration, and AI-enabled error-correction features, accelerating software-driven productivity enhancements across end-use sectors.

Market Size & Growth: Valued at USD 69.63 Million in 2024 and projected to reach USD 106.86 Million by 2032 at a 5.5% CAGR, driven by rising accuracy requirements in elemental testing.

Top Growth Drivers: 48% rise in automated analytical workflows; 36% efficiency improvement from cloud-integrated platforms; 29% higher adoption of AI-enabled spectral interpretation.

Short-Term Forecast: By 2028, software-driven automation is expected to deliver up to 22% operational cost reduction in routine spectroscopy workflows.

Emerging Technologies: AI-assisted peak identification, real-time cloud synchronisation, and automated multi-instrument calibration tools are shaping next-generation platforms.

Regional Leaders: North America expected to reach USD 38 Million by 2032 with strong laboratory digitalization; Europe projected at USD 31 Million by 2032 driven by regulatory testing demand; Asia-Pacific anticipated at USD 28 Million by 2032 supported by semiconductor and materials testing expansion.

Consumer/End-User Trends: High adoption among pharmaceutical labs, environmental monitoring agencies, and metal/mining analyzers seeking improved throughput and reduced manual interpretation time.

Pilot or Case Example: A 2024 metals testing pilot demonstrated a 34% reduction in analysis downtime through automated spectral processing modules.

Competitive Landscape: Market leader holds approximately 21% share, followed by major competitors offering advanced data analytics, multi-technique support, and cloud-enabled laboratory integration.

Regulatory & ESG Impact: Strict environmental compliance and emissions testing standards are accelerating the need for software-driven trace element quantification.

Investment & Funding Patterns: Over USD 120 Million invested globally in spectroscopy automation software during the last two years, highlighting rapid digital transformation in labs.

Innovation & Future Outlook: Advancements in AI modelling, adaptive algorithms, and multi-technique fusion analytics are expected to define the next phase of market evolution.

The Atomic Spectroscopy Software Market continues to advance through strong adoption across pharmaceuticals, environmental monitoring, food safety, semiconductors, and metallurgical testing, supported by rising demand for precise elemental quantification and automated workflow management. Technological innovations such as ML-based spectral correction, enhanced calibration algorithms, and cross-instrument data harmonization are improving analytical reliability and throughput. Regulatory emphasis on contamination control and trace-level detection is further strengthening adoption patterns. Emerging regions are accelerating uptake due to growing laboratory networks and rising investments in research infrastructure. Future growth is expected to be shaped by AI-driven automation, cloud-native platforms, and integrated digital lab ecosystems that streamline high-volume analytical operations.

The Atomic Spectroscopy Software Market holds strategic relevance as laboratories across pharmaceuticals, semiconductors, metallurgy, food safety, and environmental monitoring accelerate their transition toward automated, analytics-driven elemental measurement. The market’s value proposition is reinforced by quantifiable gains in analytical precision, workflow efficiency, and cloud-enabled data harmonization. AI-enabled spectral modelling delivers 37% improvement compared to traditional manual peak-interpretation workflows, establishing a measurable benchmark for digital transformation. Regional adoption varies significantly: Asia-Pacific dominates in volume, while North America leads in adoption with 61% of enterprises integrating multi-instrument software ecosystems. By 2027, autonomous calibration intelligence is expected to improve instrument uptime by 28%, directly reducing operational bottlenecks in high-throughput labs. Firms are committing to ESG improvements such as 32% reduction in chemical waste generation by 2030 through optimized measurement cycles and real-time contamination tracking. In 2024, Germany achieved a 26% improvement in laboratory turnaround time through its national AI-driven analytical modernisation program implementing automated spectral correction engines. As industries expand precision testing requirements and regulatory thresholds tighten, the Atomic Spectroscopy Software Market is poised to become a foundational enabler of resilience, compliance readiness, and sustainable operational growth.

The shift toward automated laboratory ecosystems is significantly enhancing demand for Atomic Spectroscopy Software, as labs increasingly rely on digitally synchronized workflows to reduce manual interpretation errors and increase throughput accuracy. More than 58% of modern analytical laboratories have adopted automated spectral processing modules to support high-volume testing demands in pharmaceuticals, chemicals, and environmental monitoring. The integration of AI-driven noise-reduction, automated calibration, and predictive anomaly detection is improving analytical consistency by up to 33%, enabling laboratories to meet stringent global compliance benchmarks. Automated workflows also standardize multi-site operations, allowing large enterprises to achieve uniform data quality across geographically distributed laboratories. With rising sample loads—such as a 21% year-over-year increase in elemental testing in water and soil analysis—the need for efficient, software-enabled process orchestration continues to strengthen market expansion.

Integration complexities remain a major challenge for the Atomic Spectroscopy Software Market as laboratories often operate with diverse instrument types, legacy systems, and inconsistent data formats. Nearly 42% of labs report difficulties aligning multi-vendor instruments with unified software platforms, resulting in extended onboarding timelines and elevated operational costs. The lack of standardized communication protocols and varied firmware architectures further slows seamless interoperability, particularly in high-precision research environments. Additionally, skilled personnel shortages restrict the ability of organizations to fully leverage advanced AI-enabled features, leading to underutilization of high-value modules such as predictive calibration and automated spectral correction. Data migration risks and cybersecurity compliance requirements add another layer of complexity, requiring rigorous validation and multi-tier encryption safeguards. These obstacles collectively delay full-scale deployment in resource-constrained laboratories.

The global shift toward digital laboratories is opening significant growth opportunities for the Atomic Spectroscopy Software Market. With more than 65% of laboratory modernization programs prioritizing cloud-native analytics, the demand for integrated, real-time spectral processing solutions continues to rise. AI-enabled anomaly detection and automated compliance reporting are becoming critical tools for laboratories managing expanding testing volumes across pharmaceuticals, semiconductor purity assessment, metallurgy, and environmental monitoring. The emergence of multi-instrument orchestration platforms—capable of synchronizing data across ICP-MS, AAS, and ICP-OES systems—enhances operational flexibility and reduces manual interpretation workloads by up to 40%. Growing investments in R&D, coupled with increasing validation requirements in regulated sectors, create substantial room for advanced software ecosystems that support audit trails, digital traceability, and adaptive calibration intelligence. These advancements are reinforcing the market’s long-term growth potential.

The Atomic Spectroscopy Software Market faces persistent challenges due to escalating operational and compliance complexities across industries. Laboratories must adhere to stringent guidelines governing data accuracy, audit traceability, and contamination thresholds, requiring robust software validation and continuous updates. Over 47% of labs cite the high cost of ensuring regulatory alignment—through documentation, calibration logs, and error-tracking modules—as a critical constraint. Additionally, growing sample diversity and the need for multi-technique fusion analytics add pressure to maintain precise spectral interpretation across thousands of datasets. Cybersecurity compliance, particularly for cloud-connected laboratories, requires strong encryption and frequent penetration testing, adding operational burden. Limited availability of skilled staff capable of managing AI-driven analytical systems further complicates adoption, reducing the pace of digital transformation for mid-scale laboratories.

• Acceleration of AI-Enabled Spectral Interpretation: AI-driven analytical modules are transforming elemental quantification workflows, with more than 62% of advanced laboratories integrating machine-learning spectral correction tools to reduce manual interpretation time. These systems deliver up to 34% faster peak identification and eliminate nearly 27% of human-associated variance in multi-element analysis. The adoption of adaptive neural models capable of processing over 10,000 spectra per hour is reshaping high-throughput testing environments, especially in pharmaceuticals and semiconductor purity assessment.

• Expansion of Cloud-Native Laboratory Ecosystems: Cloud-connected spectroscopy platforms are becoming a central operational pillar, with 49% of laboratories transitioning to remote-access data infrastructure for multi-site synchronization. Real-time cloud analytics accelerate decision-making, enabling up to 31% improvement in cross-instrument data harmonization. Laboratories conducting environmental and geochemical testing report a 22% increase in workflow continuity due to uninterrupted access to spectral datasets, calibration records, and audit trails across distributed locations.

• Growth of Multi-Technique Integration Platforms: Integrated software ecosystems capable of handling ICP-MS, ICP-OES, AAS, and XRF data streams are gaining rapid adoption, driven by the need for unified processing environments. Approximately 45% of large analytical facilities now operate multi-technique dashboards, yielding a 29% reduction in operational silos. These platforms support simultaneous data visualization across 4–7 instrument types, increasing analysis throughput by up to 38% in industrial metallurgy and mining applications.

• Rising Demand for Automation-Driven Compliance Management: Automated compliance engines embedded in spectroscopy software are witnessing strong uptake, with 52% of regulated laboratories prioritizing digital audit support tools. Automated traceability, metadata tagging, and rule-based reporting systems reduce documentation workloads by nearly 33%. Industries operating under strict impurity and contamination thresholds—especially pharmaceuticals and food safety—report a 19% decrease in compliance-related delays due to integrated real-time validation and error-flagging modules.

The Atomic Spectroscopy Software Market is structured around three primary segmentation pillars: types, applications, and end-users, each reflecting distinct adoption behaviors and operational priorities across industrial and research environments. Software types vary widely—from ICP-MS data platforms to AAS and ICP-OES interpretation engines—each serving different precision, throughput, and analytical mandates. Applications span pharmaceuticals, environmental testing, materials science, semiconductors, and food safety, with adoption patterns influenced by regulatory thresholds and analytical complexity. End-user insights highlight strong participation from pharmaceuticals, government laboratories, chemical industries, and mining facilities, each integrating software to enhance trace-element detection accuracy. Across segments, adoption levels show rising integration of automation, with more than 58% of users prioritizing cloud-native data platforms and AI-enabled calibration modules to streamline workflows, reduce analytical variance, and meet emerging compliance demands.

ICP-MS–based spectroscopy software currently leads the Atomic Spectroscopy Software Market, accounting for 46% of adoption due to its high sensitivity for ultra-trace elemental detection and its essential role in pharmaceuticals, environmental monitoring, and semiconductor quality control. In contrast, AAS software platforms represent 28% of adoption, driven by consistent use in metal analysis and mid-scale laboratories. ICP-OES software systems hold 18%, favored for high-throughput industrial workflows. However, hybrid multi-technique platforms are growing fastest, driven by increasing demand for interoperability, automated harmonization, and unified dashboards, exhibiting a segment CAGR of 7.4% supported by laboratories standardizing cross-instrument analytics. Remaining niche categories—such as XRF data-processing engines and portable-spectroscopy interfaces—collectively contribute 8%, serving field-based and specialized mineralogical operations.

Pharmaceutical quality control is the leading application in the Atomic Spectroscopy Software Market, comprising 44% of total adoption due to stringent impurity detection thresholds and rising complex-sample workflows. Environmental testing accounts for 27% and remains essential as laboratories process increasing volumes of soil and water analyses. Materials science and metallurgy applications represent 19%, reflecting strong reliance on multi-element analysis for alloy validation and process optimization. Semiconductor applications, though currently at 10%, are the fastest-growing with a segment CAGR of 8.1%, propelled by rising purity requirements below parts-per-trillion (ppt) levels and the need for automated multi-instrument validation.

The combined contribution of food safety, geochemical analysis, and academic research accounts for 13% of remaining applications, supported by growing adoption of cloud-enabled spectral tracking.

Pharmaceutical and biotechnology companies dominate the Atomic Spectroscopy Software Market, holding 41% of total adoption due to expanded testing volumes, high-throughput impurity profiling, and heightened global compliance pressure. Government and regulatory laboratories follow with 26%, driven by environmental monitoring mandates and increasing chemical safety enforcement. Chemical and materials industries represent 21%, relying on spectroscopy software for process validation, metallurgical characterization, and batch-to-batch consistency tracking. Mining and mineral processing facilities, at 12%, remain critical users, especially in ore-grade evaluation and elemental composition profiling.

The fastest-growing end-user category is the semiconductor and electronics sector, exhibiting a segment CAGR of 8.7% due to rising demand for ultra-high-purity materials and automated cross-system spectral correlation. Remaining industries, including food processing, forensic labs, and academia, contribute a combined 15%, supported by increasing digitalization of analytical workflows.

Asia-Pacific accounted for the largest market share at 38% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

Across regions, adoption is strongly influenced by industrial composition, regulatory intensity, and digital transformation maturity. Europe represented 27%, driven by stringent compliance requirements and advanced laboratory ecosystems, while North America held 24%, supported by high adoption of AI-integrated analytical tools. South America and the Middle East & Africa collectively contributed 11%, with rising investments in environmental monitoring, mining analytics, and petrochemical quality control. With more than 62% of global laboratories prioritizing automation and 41% expanding multi-technique workflows, regional disparities continue to shape the Atomic Spectroscopy Software Market’s global trajectory.

How is rapid digitalization reshaping next-generation analytical workflows in this region?

North America holds approximately 24% of global adoption in the Atomic Spectroscopy Software Market, driven by strong demand from pharmaceuticals, environmental testing, and semiconductor manufacturing. High enterprise integration—over 63% in healthcare and 57% in finance-related analytical labs—continues to accelerate cloud-based deployment and AI-driven spectral automation. Supportive regulatory initiatives for impurity monitoring and environmental quality assessments have strengthened software integration across federal and state laboratories. Advancements in autonomous calibration, multi-instrument data harmonization, and compliance automation are improving operational efficiencies across more than 5,000 analytical facilities. A key regional player recently expanded its automated ICP-MS software suite into 180 laboratories across the U.S., improving trace-metal detection accuracy by 21%. Consumer behavior varies significantly, with enterprises prioritizing higher reliability, cross-instrument compatibility, and stringent audit-ready reporting capabilities.

Why is regulatory-driven innovation accelerating spectroscopy software adoption across this region?

Europe commands roughly 27% of the Atomic Spectroscopy Software Market, supported by major countries such as Germany, France, and the UK, where regulatory bodies enforce strict elemental testing and environmental compliance protocols. Sustainability directives and digital laboratory modernization programs are accelerating adoption of explainable and traceable spectroscopy platforms. More than 54% of European analytical laboratories now prioritize AI-driven spectral correction and real-time calibration tracking. Germany maintains a strong industrial footprint, with over 1,200 high-capacity testing facilities using advanced spectroscopy software for metallurgy and chemical validation. A notable European software provider recently introduced a cloud-native ICP-OES integration module, enhancing multi-country calibration consistency by 18%. Consumer behavior is influenced by strong regulatory pressure, favoring transparency, traceability, and detailed audit-trail documentation.

How is large-scale industrial expansion driving advanced spectroscopy software adoption in this region?

Asia-Pacific represents the largest regional footprint in the Atomic Spectroscopy Software Market, accounting for 38% of total adoption and ranking highest in volume consumption. China, India, and Japan are the leading users, supported by expanding pharmaceutical manufacturing, semiconductor fabrication, and environmental monitoring networks. Rapid industrialization, high-volume testing demands, and government investments in R&D infrastructure continue to accelerate adoption of AI-integrated spectroscopy automation. More than 68% of high-capacity laboratories in China have transitioned to multi-technique software platforms, while India reports a rising shift toward cloud-native calibration engines across over 700 facilities. A major local vendor recently deployed automated elemental-analysis suites across 95 electronics plants, improving defect detection by 24%. Consumer behavior in the region leans toward mobile-accessible platforms and workflow automation, driven by fast-growing digital ecosystems.

What factors are strengthening the transition toward modern analytical ecosystems in this region?

South America accounts for an estimated 7% share of the Atomic Spectroscopy Software Market, with Brazil and Argentina representing the region’s largest contributors. Expanding mining operations, petrochemical processing, and environmental monitoring requirements continue to push demand for advanced elemental-analysis platforms. Regulatory improvements supporting water-quality monitoring and industrial emissions tracking have increased adoption across more than 350 laboratories. A regional analytical software provider recently launched a localized ICP-MS module for mining facilities, improving ore-grade assessment accuracy by 17%. Infrastructure modernization and digital transformation initiatives across industrial hubs fuel the uptake of automation and real-time spectral error detection. Consumer behavior tends toward budget-flexible cloud deployment models and language-localized interfaces for operational convenience.

How are industrial diversification and modernization initiatives shaping analytical software adoption in this region?

The Middle East & Africa contributes around 4% to global Atomic Spectroscopy Software Market adoption, driven by expanding oil & gas operations, mining industries, and construction-material quality assessment. Countries such as the UAE, Saudi Arabia, and South Africa are leading adoptors, supported by investments in laboratory infrastructure and digitalization mandates. More than 40% of regional analytical facilities have adopted automated spectral verification systems to meet stricter environmental and industrial reporting requirements. A local instrumentation group recently integrated AI-enabled spectral optimization software across 50 petrochemical plants, improving analytical throughput by 19%. Consumer behavior reflects a preference for rugged, compliance-oriented software solutions capable of handling high-temperature and high-salinity sample environments.

China – 22% market share

Strong dominance supported by high-volume pharmaceutical production capacity and large-scale semiconductor materials testing.

United States – 18% market share

Leadership reinforced by advanced R&D ecosystems and strong adoption of AI-enabled laboratory automation across regulated industries.

The Atomic Spectroscopy Software market is characterized by a moderately consolidated competitive landscape, with an estimated 25–30 active global competitors offering specialized analytical, automation, and data-processing platforms. The top five companies collectively account for approximately 48–52% of the overall market share, reflecting strong concentration among technology leaders with advanced laboratory informatics capabilities. Competitive positioning is driven by factors such as multi-instrument integration, cloud-enabled data workflows, compliance readiness, and AI-based spectral interpretation. Key strategic initiatives recorded across the market include more than 20 product upgrades between 2022 and 2024, over 15 partnership agreements with laboratory automation vendors, and mergers aimed at unifying spectroscopy software ecosystems. Innovation trends continue to influence rivalry intensity, especially as vendors increasingly adopt ML-powered peak analysis, automated spectral comparison libraries exceeding 50,000 samples, and cross-platform compatibility with mass spectrometry and chromatography systems. Additionally, rising regulatory pressure has prompted companies to add built-in audit trails, 21 CFR Part 11 support, and encrypted data transfer modules, strengthening differentiation among enterprise buyers across pharmaceutical, environmental testing, and materials science sectors.

Thermo Fisher Scientific

Agilent Technologies

PerkinElmer

Shimadzu Corporation

Bruker Corporation

Hitachi High-Tech Corporation

Analytik Jena GmbH

Spectris plc (via Malvern Panalytical)

Rigaku Corporation

Technological advancements in the Atomic Spectroscopy Software market are reshaping laboratory workflows, data quality, and analytical precision across industrial, environmental, and pharmaceutical domains. Modern platforms integrate multi-technique compatibility, supporting atomic absorption spectroscopy (AAS), inductively coupled plasma optical emission spectroscopy (ICP-OES), and inductively coupled plasma mass spectrometry (ICP-MS) within unified interfaces, enabling instrument interoperability across more than 8–10 major hardware ecosystems. A notable trend is the adoption of AI-assisted spectral interpretation, allowing automated peak identification with accuracy improvements exceeding 25–30% compared to legacy rule-based models. These systems now support spectral libraries that often surpass 40,000–60,000 reference signatures, significantly enhancing detection efficiency for trace metals and complex matrices.

Cloud-enabled spectroscopy software continues to see accelerated adoption, with over 55% of medium-to-large laboratories integrating cloud or hybrid deployments for centralized data access, encrypted remote monitoring, and multi-user collaboration. Automation technologies, including robotic autosamplers and LIMS-linked workflows, are increasingly supported through APIs and low-code integration modules, reducing manual data handling errors by approximately 40%. Additionally, compliance-focused advancements—such as real-time audit trails, digital signatures, and automated validation scripts—are becoming standard in heavily regulated sectors.

Emerging technologies include quantum-enhanced spectral analysis, ML-driven noise reduction algorithms, and GPU-accelerated computation that shortens processing times by 3–5x. Furthermore, the growing emphasis on sustainability is driving energy-efficient software architectures and optimized processing algorithms for high-volume laboratories. Collectively, these technological enablers strengthen the market’s transition toward high-throughput, automation-ready, and intelligence-driven spectroscopy environments.

In 2024, Agilent Technologies launched its Advanced Dilution System ADS 2, which fully integrates with its ICP-MS and ICP-OES instruments and associated software to automate sample preparation and dilution, significantly reducing operator workload and improving data traceability. (Agilent)

Also in 2024, Shimadzu Corporation released eMSTAT Solution Ver. 2.0, a machine-learning–enabled statistical analysis software tailored for food-sector atomic-spectroscopy data, offering multivariate and discriminant-analysis capabilities. (Shimadzu Corporation)

In January 2024, Shimadzu’s AA-7800 atomic absorption spectrophotometer was recognized by the Japan Industrial Design Association (JIDA) for its compact footprint and network connectivity, highlighting remote data-analysis support through atomic-absorption software.

In 2024, Thermo Fisher Scientific showcased its Perception Particle Analysis Software at AISTech 2024: this software enables standardized recipe-based workflows for SEM analysis and automated elemental assessment, reducing manual analysis time to minutes. (Thermo Fisher Scientific)

This Atomic Spectroscopy Software Market Report covers a comprehensive range of product types—including ICP-MS data systems, ICP-OES/ICP-AES platforms, AAS (flame and furnace), single-particle analysis, and hybrid multi-technique toolkits. On the application side, the report analyzes software use in critical sectors such as pharmaceuticals, environmental monitoring, food safety, semiconductor materials, metallurgy, geochemistry, and academic research. It also examines how laboratories deploy these software solutions for compliance automation, digital traceability, and high-throughput analysis.

Geographically, the report provides region-wise insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, tracking variations in technology adoption, regulatory drivers, and lab modernization maturity. The report further explores technology trends—such as AI-based spectral interpretation, cloud-native architectures, multi-instrument integration, and automated calibration engines—highlighting the innovation pathways shaping future deployments.

From an industry-focus perspective, the report delves into adoption by end users including pharmaceutical companies, government labs, mining and metals, environmental agencies, and research institutions. It also addresses niche and emerging segments, such as single-cell ICP-MS, portable field spectroscopy, and sustainability-driven testing use cases. Risk factors, regulatory impact, and compliance frameworks are assessed, alongside vendor strategies, competitive positioning, and partnership dynamics. The report serves decision-makers by offering actionable insights on software-driven efficiencies, digital transformation, and future investment priorities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 69.63 Million |

|

Market Revenue in 2032 |

USD 106.86 Million |

|

CAGR (2025 - 2032) |

5.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, Agilent Technologies , PerkinElmer, Shimadzu Corporation , Bruker Corporation, Hitachi High-Tech Corporation, Analytik Jena GmbH, Spectris plc (via Malvern Panalytical), Rigaku Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |