Reports

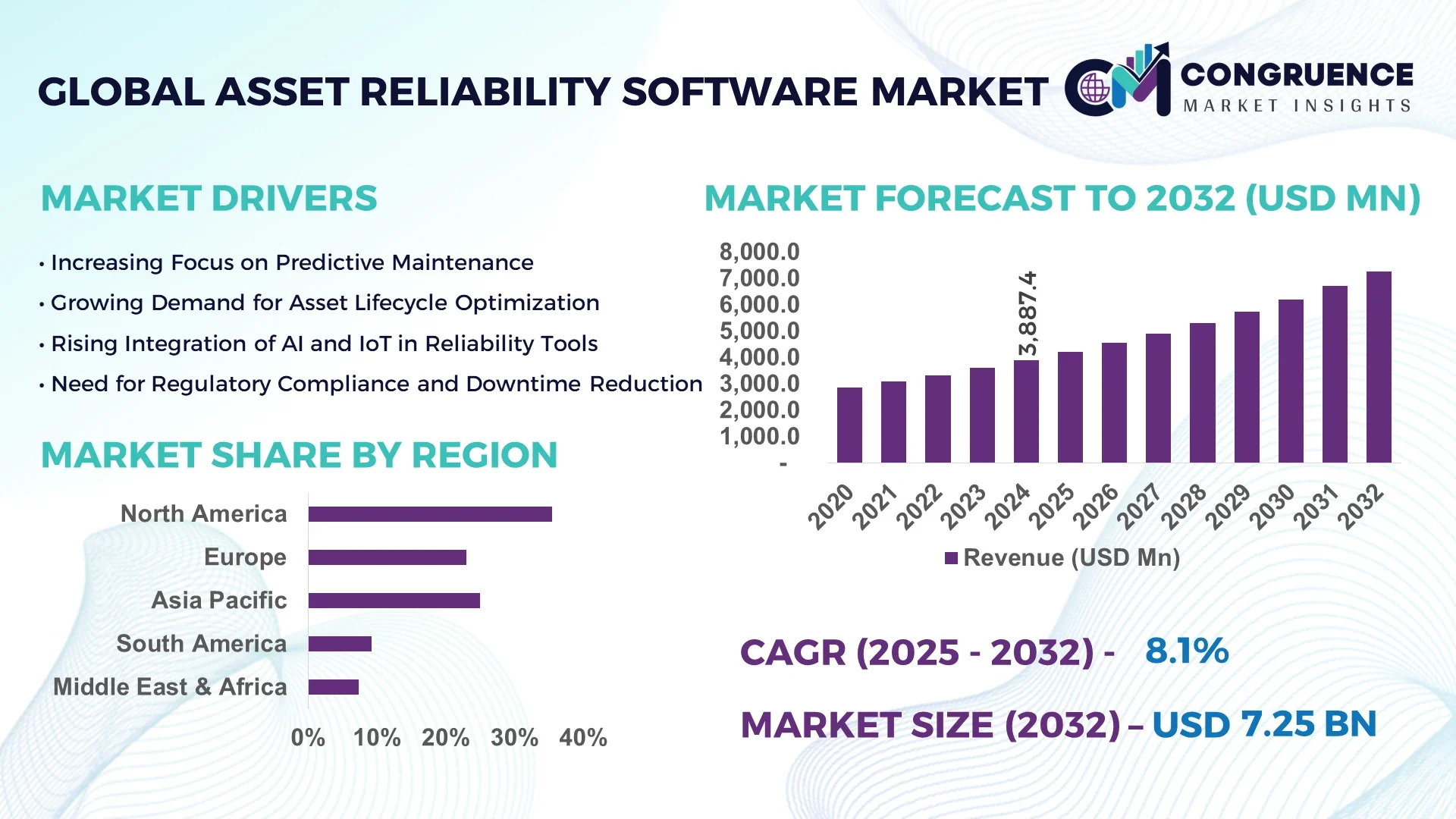

The Global Asset Reliability Software Market was valued at USD 3887.38 Million in 2024 and is anticipated to reach a value of USD 7248.74 Million by 2032 expanding at a CAGR of 8.1% between 2025 and 2032.

In the United States, extensive investments in predictive maintenance technologies, increasing industrial automation adoption, and advancements in data analytics tools have positioned the country as a leader in the Asset Reliability Software market. U.S.-based manufacturing and energy sectors are increasingly deploying asset-centric platforms to optimize uptime and reduce operational disruptions.

The Asset Reliability Software market plays a pivotal role in enhancing operational stability across core sectors such as oil & gas, utilities, manufacturing, mining, and transportation. Leading industries are integrating advanced asset performance management tools to enable real-time monitoring, failure prediction, and optimized maintenance schedules. This has led to a noticeable reduction in unplanned downtimes and increased asset utilization. Regulatory compliance, especially in highly governed industries like energy and pharmaceuticals, is further driving the demand for software platforms that offer audit trails and safety management features. Additionally, innovations in cloud-based deployment models and mobile accessibility are making these systems scalable and cost-efficient. Regional consumption is accelerating in Asia-Pacific and Latin America, owing to infrastructural expansions and the modernization of industrial frameworks. Future trends point toward the integration of digital twins and edge computing into asset reliability frameworks for heightened precision and responsiveness.

Artificial Intelligence (AI) is significantly transforming the Asset Reliability Software Market by enhancing decision-making, automating diagnostics, and enabling predictive capabilities that improve overall asset performance. AI-driven analytics engines are being embedded into software platforms to deliver real-time insights that predict equipment failure well before it occurs. This reduces maintenance costs, prolongs asset life, and minimizes unplanned outages. In sectors like utilities, aviation, and petrochemicals, where equipment uptime is critical, AI’s ability to detect anomalies and correlate diverse datasets is reshaping operational strategies.

One of the most notable applications of AI in the Asset Reliability Software Market is predictive maintenance powered by machine learning algorithms. These systems continuously ingest historical and real-time data to assess wear and tear, temperature variations, pressure anomalies, and more—triggering maintenance activities only when truly needed. This optimizes labor utilization and reduces inventory overheads. AI-enhanced platforms are also enabling prescriptive maintenance, guiding technicians not only on when but also how to resolve issues efficiently.

Additionally, AI is driving the evolution of automated root cause analysis (RCA) tools, which drastically cut investigation time and enhance accuracy. Visual AI applications, including image recognition and thermal monitoring via drones and IoT sensors, are also gaining ground in large-scale industrial environments. As a result, AI is no longer just a value-add—it has become a foundational component of next-generation asset management strategies. Companies adopting these technologies report measurable improvements in uptime, cost savings, and employee productivity.

“In January 2024, IBM’s Maximo Application Suite integrated a new AI-powered failure mode analysis engine that reduced diagnostics time for mechanical assets by 34% across several manufacturing pilot projects, significantly improving operational continuity and workforce efficiency.”

Predictive maintenance is emerging as a powerful growth driver in the Asset Reliability Software market as industries aim to shift from reactive to proactive maintenance strategies. With increasing operational complexity, unplanned equipment failures lead to significant losses, particularly in sectors like oil & gas, automotive, and energy. Predictive analytics integrated into asset reliability platforms allows companies to forecast equipment failures using historical performance data, sensor readings, and usage trends. For example, in the mining industry, predictive maintenance has helped reduce equipment downtime by up to 25% through early intervention alerts. These benefits are further enhanced by machine learning models that continuously improve forecasting accuracy. As a result, predictive maintenance not only improves asset uptime but also significantly cuts maintenance costs, inventory waste, and labor inefficiencies—making it a major adoption catalyst for asset-centric enterprises.

Despite its advantages, the Asset Reliability Software market faces limitations due to integration complexities with existing legacy systems. Many industrial environments still operate with outdated control systems, proprietary protocols, and fragmented data architectures that lack the interoperability needed for seamless software deployment. Upgrading or replacing these infrastructures often demands significant capital investment and extended downtime, which can delay software implementation. Additionally, compatibility challenges between modern platforms and older machinery impede data collection accuracy and system performance. In sectors like utilities and manufacturing, transitioning to modern asset reliability systems without disrupting ongoing operations requires careful change management and workforce upskilling. These factors act as barriers for small and medium-sized enterprises that may lack the technical and financial resources to undertake full-scale digital transformation.

The rapid adoption of cloud-based asset management platforms presents a key opportunity in the Asset Reliability Software market. Cloud-native solutions offer unmatched flexibility, real-time collaboration, and remote accessibility, enabling companies to scale operations across multiple sites without heavy infrastructure costs. With the rise of global industrial automation, enterprises are increasingly turning to SaaS-based asset reliability tools that facilitate centralized monitoring and predictive diagnostics. For instance, cloud deployments can reduce time-to-value by enabling fast implementation and easy updates. This model is particularly attractive to sectors like transportation and logistics, where distributed assets and mobile equipment require decentralized management. Furthermore, cloud integration supports enhanced cybersecurity, compliance monitoring, and AI-powered analytics—features essential for organizations operating in regulated industries. As digital transformation accelerates, cloud-based offerings are poised to become a preferred deployment strategy.

A major challenge hindering the Asset Reliability Software market is the growing shortage of skilled professionals capable of managing and interpreting asset performance data. Implementing advanced reliability platforms requires expertise in condition monitoring, predictive analytics, industrial IoT systems, and software integration. However, many organizations struggle to find or train personnel with the necessary skillsets to effectively leverage these technologies. The lack of qualified reliability engineers and data analysts limits the impact of software adoption and slows operational ROI. This challenge is particularly pronounced in developing regions and traditional industries where workforce digitization lags. Moreover, the need for ongoing training to keep pace with evolving technologies adds to organizational costs and complexity. Addressing this skill gap is essential for maximizing the value of asset reliability systems.

• Integration of Digital Twin Technology: Digital twin implementation is gaining traction across industrial operations, enabling real-time simulation of physical assets through virtual models. In 2024, over 30% of Fortune 500 manufacturing companies adopted digital twins to optimize performance and failure prediction. Asset reliability platforms are increasingly embedding digital twin modules to simulate stress conditions, asset wear, and process inefficiencies. This trend is enhancing predictive maintenance strategies and improving decision-making related to capital expenditure and resource planning.

• Adoption of Modular and Prefabricated Construction: The growing use of modular and prefabricated construction methods is impacting the Asset Reliability Software market significantly. Off-site construction requires precision asset coordination and predictive performance tracking, which is fueling demand for high-accuracy reliability tools. Particularly in Europe and North America, construction firms are investing in software that can manage logistics, asset usage, and uptime across decentralized production sites. Automated prefabrication is also minimizing labor dependency, placing higher reliability expectations on critical machinery and systems.

• Growth of Mobile Asset Management Solutions: Mobile access to asset reliability systems is emerging as a major operational enhancement, especially for field technicians. In 2024, more than 45% of industrial maintenance teams utilized mobile-first platforms to access diagnostics and work orders in real-time. These mobile tools are boosting productivity, reducing maintenance cycle time, and facilitating instant data uploads from remote or hazardous locations. The trend is pushing vendors to develop lighter, faster, and more responsive mobile modules that seamlessly integrate with enterprise platforms.

• Increasing Use of Condition-Based Monitoring (CBM): Condition-based monitoring is becoming a core feature of advanced asset reliability platforms. Unlike traditional time-based maintenance, CBM uses live sensor data to assess the real-time health of assets. In heavy industries such as oil & gas and power generation, CBM adoption rose by 38% year-over-year in 2024. This approach helps companies detect abnormalities, optimize maintenance schedules, and prevent unexpected failures—leading to significant cost reductions and increased operational efficiency.

The Asset Reliability Software market is segmented by type, application, and end-user categories, each revealing unique adoption patterns and strategic priorities. Types include solutions such as Asset Performance Management (APM), Computerized Maintenance Management Systems (CMMS), and Enterprise Asset Management (EAM). Applications span across predictive maintenance, failure diagnostics, lifecycle planning, and compliance tracking. End-user sectors range from manufacturing and energy to transportation and utilities. Among these, predictive maintenance and asset lifecycle optimization are the most emphasized across global markets, driven by the need for efficiency and regulatory compliance. Industrial firms are customizing solutions to align with vertical-specific standards, while growing interest in mobile and cloud-based deployments is further shaping market segmentation. Technological interoperability, industry 4.0 alignment, and analytics-driven features continue to influence preferences across segments.

Asset Performance Management (APM) leads the type segment due to its robust capabilities in delivering predictive analytics, root cause failure analysis, and lifecycle optimization. APM systems are widely deployed in energy, manufacturing, and chemical industries to reduce equipment downtime and support sustainability goals. The fastest-growing segment is Computerized Maintenance Management Systems (CMMS), as industries modernize their maintenance operations with centralized task scheduling, inventory tracking, and mobile-enabled workflows. CMMS platforms are particularly popular among mid-sized enterprises transitioning from manual systems. Enterprise Asset Management (EAM) solutions hold steady demand, especially in large, multi-site organizations requiring full asset visibility and compliance oversight. Other niche offerings, such as Reliability-Centered Maintenance (RCM) software, are also gaining attention in sectors with mission-critical infrastructure like defense and aerospace. Overall, the diversification of features and integration capabilities across types is helping businesses tailor solutions to their specific operational and regulatory needs.

Predictive maintenance remains the dominant application in the Asset Reliability Software market due to its clear ROI through cost reduction, asset longevity, and productivity gains. In sectors like oil & gas and manufacturing, predictive systems allow early identification of equipment faults, reducing unplanned downtime. The fastest-growing application is lifecycle asset management, propelled by industries seeking better control over capital assets from acquisition to retirement. This is particularly relevant in infrastructure and utilities, where long asset lives demand proactive strategy. Failure diagnostics, compliance management, and performance benchmarking also represent critical application areas, especially in industries under strict regulatory scrutiny. Emerging applications such as energy efficiency optimization and AI-assisted fault detection are expanding the scope of reliability platforms beyond maintenance, turning them into tools for strategic planning and operational excellence.

Manufacturing is the leading end-user of Asset Reliability Software, owing to its extensive use of heavy machinery, automation systems, and need for consistent production output. Manufacturers leverage these platforms to avoid production halts, maintain compliance, and streamline maintenance scheduling. The energy and utilities sector is the fastest-growing end-user group, driven by aging infrastructure, environmental compliance mandates, and the need to optimize distributed assets. Power generation companies are heavily investing in software that ensures grid reliability and asset integrity. Other key end-users include transportation and logistics companies, which use these platforms to manage vehicle fleets and depot equipment reliability. Meanwhile, the healthcare and pharmaceutical industries are adopting asset reliability tools to comply with strict hygiene and operational standards, particularly in labs and production environments. Collectively, the varied end-user base underscores the market’s cross-industry relevance and the increasing prioritization of uptime, safety, and asset health.

North America accounted for the largest market share at 35.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2025 and 2032.

The demand in North America is driven by early adoption of industrial automation, advanced digital infrastructure, and proactive maintenance strategies in energy and manufacturing. Meanwhile, Asia-Pacific is experiencing a surge in infrastructure development and industrial modernization, particularly in emerging economies like India, China, and Southeast Asian countries. As industries in these regions transition toward Industry 4.0, the need for intelligent asset monitoring and predictive maintenance solutions is accelerating. Europe is also showing strong performance, backed by regulatory compliance pressures and sustainability initiatives. The global landscape is being reshaped by cloud adoption, smart sensor integration, and AI-enhanced asset tracking. Governments and enterprises alike are focusing on reducing unplanned downtime and optimizing capital asset performance, which further fuels the market expansion across all regions.

Industrial Maintenance Modernization Accelerates Software Integration

North America held a dominant position in the Asset Reliability Software market with a market share of 35.4% in 2024. The regional demand is largely driven by the energy, oil & gas, and manufacturing sectors that prioritize predictive maintenance and compliance reporting. Government-backed digital transformation initiatives and regulatory frameworks such as OSHA and ISO standards have compelled industries to adopt advanced reliability platforms. Furthermore, industrial automation is thriving in the U.S. and Canada, where factories are deploying AI-integrated systems to forecast and prevent equipment failure. Cloud-based asset monitoring tools and mobile-enabled solutions are also witnessing high adoption as enterprises aim to minimize operational disruptions and labor costs. In addition, an increasing number of industrial AI startups and software providers are contributing to regional competitiveness and product innovation.

Smart Compliance Technologies Drive Asset Lifecycle Efficiency

Europe accounted for approximately 28.6% of the global Asset Reliability Software market in 2024. Countries like Germany, France, and the UK are leading adopters due to strong regulatory oversight and industrial digitization efforts. The European Union’s sustainability and emissions directives are encouraging companies to invest in software that enhances asset performance and reduces waste. Industry leaders are incorporating digital twin models and machine learning into maintenance workflows to align with circular economy goals. Notable momentum is seen in manufacturing, chemicals, and utilities, where aging infrastructure demands more precise asset tracking. The emergence of regulatory bodies such as the European Green Deal Office is pushing industries to adopt intelligent systems for asset monitoring, energy management, and risk reduction. Enhanced connectivity and 5G-enabled factory ecosystems are also accelerating software deployment across major European economies.

Infrastructure Modernization Fuels Software Deployment in Emerging Economies

Asia-Pacific ranked as the fastest-growing region in the Asset Reliability Software market in 2024, with China, India, and Japan leading consumption volumes. The region is experiencing rapid infrastructure growth, especially in transportation, manufacturing, and utilities, which drives the demand for robust asset management tools. Industrial sectors in China are adopting AI-enhanced maintenance systems to reduce equipment downtime and improve output efficiency. In India, the “Make in India” initiative is promoting the digital transformation of production facilities with modern asset reliability frameworks. Japan continues to lead in robotics-integrated platforms for asset performance management. Additionally, growing investments in smart city development and regional innovation clusters—such as Singapore’s AI ecosystem and South Korea’s Industry 4.0 hubs—are pushing software vendors to offer scalable, multilingual, and mobile-enabled solutions to match local operational demands.

Energy Infrastructure Optimization Boosts Digital Reliability Investments

South America’s Asset Reliability Software market is gaining traction, with Brazil and Argentina emerging as key contributors. In 2024, the region captured approximately 7.8% of the global market. Brazil’s energy and utility sectors are investing in real-time asset monitoring systems to improve grid performance and reduce blackouts. Infrastructure development and government programs supporting industrial modernization are further amplifying demand. Argentina’s manufacturing and transportation sectors are incorporating cloud-based CMMS tools to streamline maintenance workflows. Trade agreements with North American and European partners are promoting the exchange of technologies, making advanced platforms more accessible. While digital adoption is slower than other regions, increased awareness about operational efficiency, reduced lifecycle costs, and environmental accountability is steadily driving the implementation of asset reliability solutions.

Oil & Gas Digitization and Construction Growth Drive Software Uptake

The Middle East & Africa region continues to expand its footprint in the Asset Reliability Software market, with the UAE, Saudi Arabia, and South Africa driving demand. In 2024, the region contributed 5.6% of global market volume. The oil & gas sector, a cornerstone of the Middle East economy, is adopting AI-integrated reliability systems to minimize downtime and ensure safety compliance in high-risk environments. In South Africa, the mining and construction industries are integrating mobile CMMS platforms to monitor dispersed assets in real time. Government-backed initiatives like Saudi Vision 2030 are promoting the digital transformation of key industries. Meanwhile, growing regional participation in global trade is prompting local companies to meet international standards for asset integrity and performance. Software localization, cloud infrastructure growth, and an increasing number of public-private partnerships are further supporting the regional market evolution.

United States – 31.2% market share

Strong industrial digitalization, advanced automation capabilities, and widespread cloud infrastructure drive the U.S. dominance in the Asset Reliability Software market.

China – 16.4% market share

High-volume manufacturing and rapid adoption of AI-powered predictive maintenance tools place China among the top countries leading the Asset Reliability Software market.

The competitive landscape of the Asset Reliability Software market is marked by the presence of over 60 active global and regional vendors offering a wide array of predictive maintenance, asset management, and performance optimization solutions. Market participants are strategically differentiating through AI-enhanced analytics, cloud-native platforms, mobile compatibility, and sector-specific customization. Leading companies are focusing on expanding their portfolios through modular upgrades, integrating condition-based monitoring, and embedding digital twin functionalities to meet evolving industry demands.

Strategic partnerships and mergers have intensified, particularly between software providers and industrial IoT companies, allowing for broader data integration and advanced diagnostics capabilities. Recent trends indicate a sharp rise in cross-industry collaborations, especially in manufacturing, oil & gas, and utilities, where real-time asset health tracking is becoming mission-critical. Innovation hubs in the U.S., Germany, and Japan are producing new reliability frameworks that incorporate edge computing and autonomous monitoring, influencing competition across all tiers. Additionally, startups offering cloud-first platforms are challenging established players by providing scalable and cost-effective solutions tailored for small and mid-sized enterprises. Overall, the market continues to evolve rapidly, with innovation speed and integration flexibility emerging as key competitive levers.

IBM Corporation

Siemens AG

GE Vernova

ABB Ltd.

SAP SE

Emerson Electric Co.

Bentley Systems Incorporated

Oracle Corporation

DNV AS

Aspen Technology Inc.

Schneider Electric SE

Fluke Corporation

IFS AB

AVEVA Group plc

The Asset Reliability Software market is undergoing rapid technological transformation, propelled by advancements in AI, IoT, edge computing, and data analytics. Modern platforms are increasingly incorporating machine learning algorithms to enable predictive diagnostics, anomaly detection, and automated maintenance recommendations. These capabilities allow users to monitor equipment performance in real time and reduce unplanned downtime. In 2024, over 65% of enterprises with asset-intensive operations integrated AI-powered condition monitoring systems into their maintenance workflows.

IoT sensor integration has become a foundational technology, capturing data points such as vibration, temperature, pressure, and energy consumption. These inputs are processed through cloud-based platforms that visualize asset health and provide actionable insights. Edge computing is gaining prominence, particularly in remote or hazardous locations, allowing data processing to occur close to the asset and ensuring real-time responsiveness without latency issues.

Digital twin technology is also reshaping asset lifecycle management. By creating virtual replicas of physical equipment, organizations simulate performance under various operating conditions, enhancing maintenance strategies and asset investment planning. Additionally, mobile-first platforms and AR-assisted maintenance tools are being deployed to support field technicians with instant diagnostics and guided repairs. These emerging technologies collectively empower businesses to optimize asset performance, improve safety, and reduce operational risks across sectors such as manufacturing, energy, transportation, and infrastructure.

• In February 2024, Siemens launched a cloud-native version of its COMOS Walkinside platform, integrating 3D visualization with real-time asset condition monitoring, aimed at process industries managing complex infrastructure.

• In October 2023, ABB unveiled its new Asset Performance Management suite integrated with AI-driven prescriptive analytics, reducing mean time to repair (MTTR) by 22% across pilot industrial operations in Europe.

• In March 2024, Emerson Electric introduced a mobile diagnostics app connected to its Plantweb™ ecosystem, enabling technicians to conduct on-the-spot reliability assessments with embedded AR guidance tools.

• In December 2023, Bentley Systems released an update to its iTwin platform, enhancing digital twin synchronization speed by 40% and adding integration with real-time IoT feeds for predictive asset analytics.

The Asset Reliability Software Market Report comprehensively covers the full spectrum of solutions, including Asset Performance Management (APM), Computerized Maintenance Management Systems (CMMS), Enterprise Asset Management (EAM), and Reliability-Centered Maintenance (RCM) software. It analyzes how these tools are deployed across a variety of applications such as predictive maintenance, real-time asset monitoring, lifecycle tracking, compliance management, and failure diagnostics.

The report spans key geographic markets including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into country-level trends in the United States, China, Germany, India, Brazil, and the UAE. It evaluates sector-specific adoption in industries like manufacturing, oil & gas, utilities, transportation, pharmaceuticals, and mining. Particular attention is given to the increasing demand from mid-sized enterprises for cloud-based and mobile-enabled platforms.

Additionally, the report explores the growing influence of emerging technologies, such as digital twins, AI-enhanced analytics, and edge computing, which are shaping the next generation of asset reliability systems. It also considers niche and emerging areas such as remote diagnostics in offshore facilities and AR-supported maintenance tools for field technicians. The scope is designed to provide decision-makers with actionable intelligence on product innovation, strategic deployments, and competitive differentiation.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3,887.38 Million |

|

Market Revenue in 2032 |

USD 7,248.74 Million |

|

CAGR (2025 - 2032) |

8.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM Corporation, Siemens AG, GE Vernova, ABB Ltd., SAP SE, Emerson Electric Co., Bentley Systems Incorporated, Oracle Corporation, DNV AS, Aspen Technology Inc., Schneider Electric SE, Fluke Corporation, IFS AB, AVEVA Group plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |