Reports

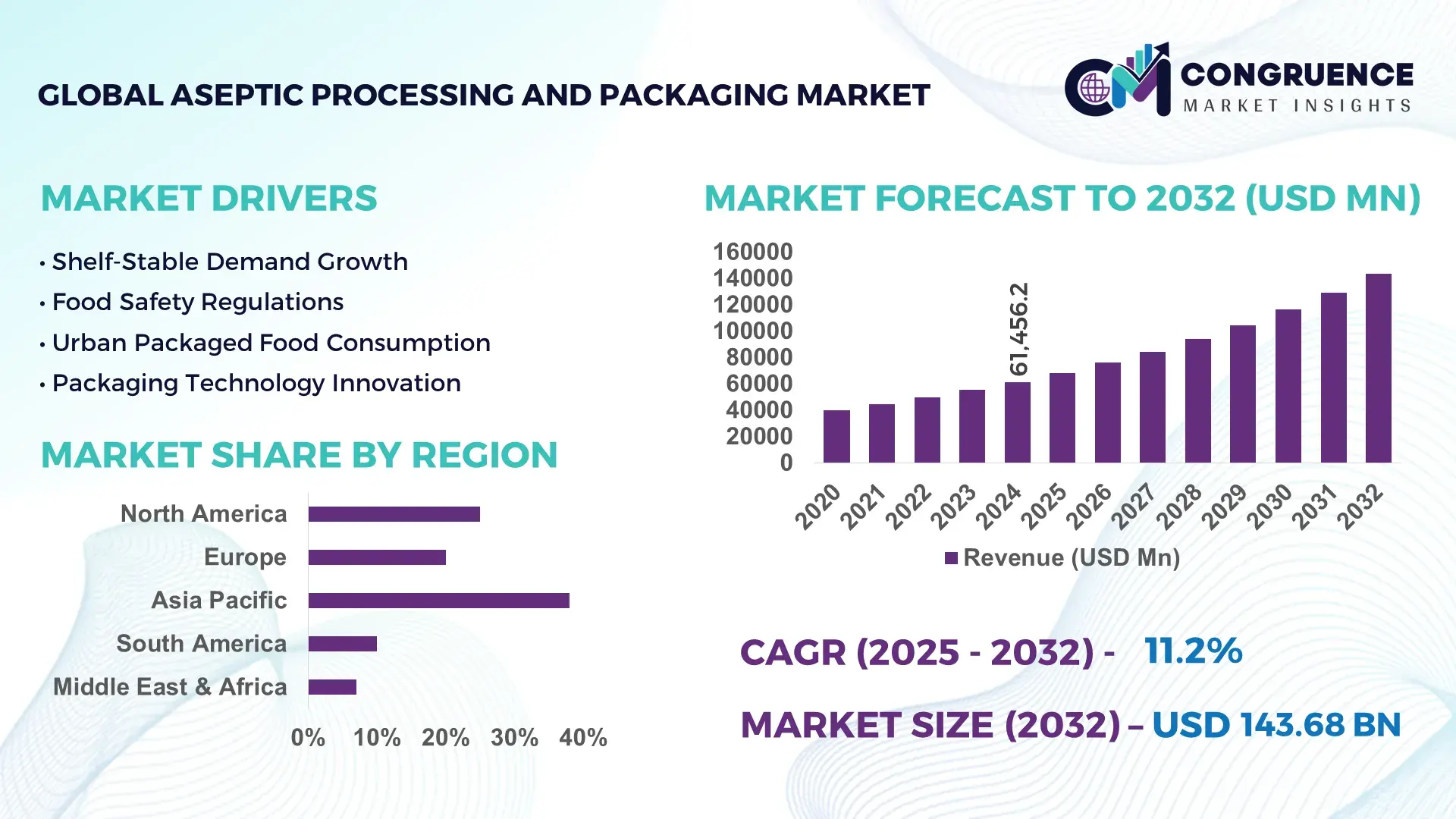

The Global Aseptic Processing and Packaging Market was valued at USD 61456.23 Million in 2024 and is anticipated to reach a value of USD 143682.62 Million by 2032 expanding at a CAGR of 11.2% between 2025 and 2032. Growth is supported by rising global consumption of packaged food and beverages, increasing pharmaceutical sterile production, and stricter food safety and quality regulations across major economies.

China represents the most significant country market within the global aseptic processing and packaging landscape due to its large-scale manufacturing ecosystem, capital investment intensity, and rapid modernization of food and pharmaceutical processing. In 2023, China produced over 39 million metric tons of dairy products and more than 190 billion liters of beverages, with aseptic formats increasingly used for milk, flavored drinks, and functional beverages. Annual investment in food processing equipment exceeded USD 28 billion, with aseptic filling and sterilization systems accounting for a growing share as manufacturers upgrade for higher throughput, lower contamination risk, and longer shelf life. Pharmaceutical sterile injectables production surpassed 10 billion units annually, driving demand for high-precision aseptic lines. Automation penetration in new aseptic installations now exceeds 60%, integrating robotics, digital monitoring, and inline quality control to improve consistency, reduce waste, and ensure compliance with global export standards.

• Market Size & Growth: USD 61.46 billion in 2024, projected USD 143.68 billion by 2032, CAGR 11.2%, driven by higher demand for shelf-stable, preservative-free food, beverages, and sterile pharmaceuticals

• Top Growth Drivers: Packaged beverage adoption 42%, pharmaceutical sterile output growth 35%, automation-driven efficiency gains 28%

• Short-Term Forecast: By 2028, average filling line operating costs decline by 20% and throughput improves by 18%

• Emerging Technologies: AI-based contamination detection, IoT-enabled sterilization validation, high-barrier recyclable multilayer packaging

• Regional Leaders: Asia Pacific USD 79 billion by 2032 with urban convenience food growth, North America USD 46 billion driven by pharma and dairy, Europe USD 30 billion led by sustainable packaging adoption

• Consumer/End-User Trends: Rising preference for preservative-free beverages, ready-to-drink nutrition, and injectable pharmaceuticals with extended shelf life

• Pilot or Case Example: 2026 beverage plant upgrade achieved 25% reduction in product losses and 17% higher line utilization through smart aseptic controls

• Competitive Landscape: Market leader Tetra Pak ~20% share, followed by SIG, Amcor, Elopak, Greatview

• Regulatory & ESG Impact: Stricter food safety standards and recyclable packaging mandates accelerating aseptic technology adoption

• Investment & Funding Patterns: Over USD 1.2 billion invested recently in line upgrades, automation, and sustainable material innovation

• Innovation & Future Outlook: Integration of digital traceability, smart sensors, recyclable high-barrier materials, and modular aseptic filling systems

The aseptic processing and packaging market primarily serves food and beverages, pharmaceuticals, and nutraceuticals, with food and beverages contributing approximately 55% of demand, pharmaceuticals around 30%, and other sectors such as cosmetics and industrial liquids making up the remainder. Key innovations include advanced hydrogen peroxide and electron-beam sterilization, inline microbial detection, and recyclable aseptic cartons replacing aluminum-based laminates. Regulatory pressure on food safety, waste reduction, and carbon emissions is reshaping equipment and material choices, while economic growth in Asia and urban lifestyle changes are boosting consumption of shelf-stable products. Regional growth is strongest in Asia Pacific due to expanding middle-class demand, while Europe emphasizes sustainability and North America focuses on pharmaceutical quality compliance. Future growth will be driven by smart factories, biodegradable barrier materials, and tighter integration between processing, packaging, and digital quality management systems.

The Aseptic Processing and Packaging Market has become strategically critical for food, beverage, pharmaceutical, and nutraceutical manufacturers seeking to combine product safety, shelf-life extension, regulatory compliance, and cost efficiency within a single operational framework. Aseptic systems reduce microbial risk to below 1 CFU per 10,000 units in pharmaceutical filling environments while enabling ambient storage that lowers cold-chain logistics costs by approximately 20–25% compared to refrigerated distribution. From a technology perspective, electron-beam sterilization delivers 30% faster cycle times compared to hydrogen peroxide sterilization, enabling higher throughput and lower energy consumption per unit.

Asia Pacific dominates in volume due to large-scale beverage and dairy manufacturing, while Europe leads in adoption with approximately 58% of new food and pharmaceutical facilities integrating aseptic or near-aseptic lines as part of sustainability and quality compliance programs. By 2028, AI-driven inline microbial detection is expected to cut batch rejection rates by 25% and reduce unplanned downtime by 15% through predictive contamination alerts. From an ESG standpoint, firms are committing to packaging waste intensity improvements such as 35% recyclable content and 25% reduction in multilayer material usage by 2030 to align with circular economy targets.

In 2026, a leading dairy processor in Germany achieved a 22% reduction in product losses and a 19% improvement in line utilization through the deployment of smart aseptic filling systems with real-time sterilization validation. Looking forward, the Aseptic Processing and Packaging Market is positioned as a structural pillar for supply chain resilience, regulatory compliance, and sustainable growth, enabling manufacturers to meet rising safety expectations while improving operational efficiency and environmental performance.

The expansion of biologics, vaccines, and injectable therapies is significantly increasing demand for aseptic processing and packaging. Sterile injectables now account for over 50% of new drug approvals, requiring contamination risk below 0.1% per batch and validated aseptic environments across filling, sealing, and packaging. Hospitals and healthcare providers are also demanding longer shelf life and ready-to-use formats, pushing pharmaceutical companies to adopt advanced aseptic lines. Automation and robotics reduce human intervention by more than 70%, directly lowering contamination risk while increasing throughput. Additionally, global immunization programs and personalized medicine pipelines require flexible, small-batch aseptic systems capable of rapid changeovers without compromising sterility, reinforcing sustained demand for aseptic technology across pharmaceutical manufacturing.

Aseptic systems require substantial upfront investment, often exceeding several million dollars per line when accounting for sterilization units, cleanrooms, automation, and validation infrastructure. In addition to capital expenditure, validation and regulatory compliance processes can take 12–18 months before a line becomes fully operational, delaying return on investment. Smaller manufacturers and contract packers face barriers due to limited access to financing and skilled personnel required to manage aseptic environments. Furthermore, ongoing costs related to sterility assurance testing, documentation, and audits increase operational complexity and cost structures, limiting adoption in price-sensitive markets and among low-margin product categories.

Sustainability is creating new growth avenues as brand owners and regulators push for recyclable and low-carbon packaging. High-barrier mono-material plastics and paper-based aseptic cartons with reduced aluminum content enable recyclability rates above 70% in mature waste management systems. These innovations allow companies to meet environmental targets without compromising shelf life or safety. Additionally, emerging markets are investing in decentralized aseptic filling for local dairy and nutrition programs, opening opportunities for modular, scalable aseptic systems. The combination of sustainability compliance, cost reduction in logistics, and rising demand for shelf-stable nutrition supports long-term expansion across both developed and developing regions.

Aseptic operations require highly trained personnel to manage sterility protocols, automation systems, and regulatory documentation. The shortage of qualified technicians and quality assurance specialists increases labor costs and operational risk. Human error remains a major contamination source despite automation, particularly during maintenance and changeovers. Furthermore, integrating digital systems, robotics, and material innovations into existing facilities increases system complexity and requires continuous training and process optimization. These challenges raise operational risk and cost, slowing deployment and reducing the pace of modernization in regions with limited technical infrastructure or training capacity.

• Rise in Modular and Prefabricated Aseptic Line Construction with 55% Cost Efficiency Gains: Modular and prefabricated aseptic processing units are increasingly deployed to shorten installation timelines and improve capital efficiency. Approximately 55% of newly commissioned aseptic projects now report measurable cost benefits from modular construction, primarily due to off-site fabrication of pre-bent piping, sterile chambers, and enclosure systems. Installation times have declined by 30–40%, while on-site labor requirements are down by nearly 35%. This approach also improves quality consistency, as automated factory assembly reduces dimensional errors and contamination risk. Europe and North America lead adoption, with over 60% of new pharmaceutical and beverage plants specifying modular aseptic platforms to enable faster regulatory validation and future scalability.

• Rapid Integration of AI-Based Monitoring Driving 25% Reduction in Contamination Events: AI-enabled vision systems and sensor analytics are being integrated into aseptic filling and sealing lines to monitor sterility, seal integrity, and particle presence in real time. Plants deploying AI-driven inspection report up to 25% fewer contamination-related incidents and a 20% improvement in first-pass yield. Predictive algorithms analyze temperature, pressure, and microbial risk indicators, enabling proactive intervention before deviations occur. More than 45% of new aseptic installations now include digital twins or AI-based quality modules, reflecting a shift from reactive quality control to predictive sterility assurance.

• Shift Toward Recyclable High-Barrier Materials Achieving 70% Recyclability Rates: Packaging material innovation is transitioning from aluminum-based multilayer laminates toward recyclable mono-material and paper-based composites that maintain oxygen and light barriers. New structures achieve recyclability rates of up to 70% in advanced waste management systems while preserving shelf life beyond 6–9 months for beverages and nutrition products. Over 40% of brand owners now specify recyclable aseptic packaging formats to meet environmental commitments, reducing material intensity by 20% and lowering packaging-related emissions by approximately 18%. This trend is particularly strong in Europe, where regulatory pressure and consumer expectations are accelerating sustainable material adoption.

• Expansion of Flexible, Small-Batch Aseptic Systems Enabling 50% Faster Product Changeovers: Demand for personalized nutrition, functional beverages, and specialty pharmaceuticals is driving adoption of flexible aseptic systems designed for smaller batch sizes and rapid changeovers. New modular fillers and sterilizers enable batch changeovers up to 50% faster than traditional fixed lines, reducing downtime and improving asset utilization. Approximately 38% of manufacturers now prioritize flexibility over maximum throughput, reflecting a shift toward high-mix, low-volume production. This capability supports faster product launches, reduced inventory risk, and greater responsiveness to evolving consumer and healthcare needs.

The Aseptic Processing and Packaging Market is segmented across product types, applications, and end-users, each reflecting unique industry requirements and adoption patterns. Type segmentation highlights distinctions between equipment such as aseptic fillers, sterilizers, and packaging lines, allowing manufacturers to optimize operations for specific production needs. Application-based segmentation differentiates usage across beverages, dairy, pharmaceuticals, and nutraceuticals, with variations in sterility, shelf-life, and operational precision shaping investment decisions. End-user insights focus on manufacturers, contract packagers, and healthcare providers, emphasizing operational scale, automation adoption, and regulatory compliance. Regional and industry-specific preferences, combined with technological upgrades and sustainability initiatives, influence segment distribution, driving strategic investments in high-efficiency, low-contamination solutions. Approximately 60% of industry investment is directed toward beverages and dairy applications, with pharmaceutical injectables representing 25% of high-precision aseptic line deployments, reflecting the sector’s critical sterility requirements.

The Aseptic Processing and Packaging market encompasses several product types, including aseptic fillers, sterilizers, preformers, and packaging lines. Aseptic fillers currently account for 38% of adoption, serving as the leading type due to their ability to maintain sterility across liquid and semi-liquid products while reducing microbial contamination risk during filling. Sterilizers follow closely with 27% adoption, providing validated decontamination for bottles, cartons, and pouches. Preformers and packaging lines together contribute the remaining 35%, mainly supporting niche applications or secondary processing requirements. The fastest-growing segment is automated pre-sterilization and filling systems, which are increasingly adopted for high-throughput dairy and functional beverage lines due to a 12% improvement in operational efficiency and a 20% reduction in human intervention compared to manual aseptic systems.

Applications within the Aseptic Processing and Packaging Market include beverages, dairy products, pharmaceuticals, nutraceuticals, and other liquid consumables. Beverages are the leading application, representing 42% of adoption, driven by global demand for shelf-stable juices, functional drinks, and ready-to-drink nutrition products that require extended storage without preservatives. Pharmaceuticals, accounting for 30% of adoption, are witnessing the fastest growth due to biologics, vaccines, and injectable therapies requiring highly sterile environments and traceable production lines. Other applications, including nutraceuticals and industrial liquids, contribute a combined 28%, supporting specialized, small-batch, or regulatory-compliant processing needs.

Leading end-users in the Aseptic Processing and Packaging Market include beverage manufacturers, dairy producers, pharmaceutical companies, and contract packaging providers. Beverage manufacturers dominate with a 40% adoption rate, leveraging aseptic systems to extend shelf life for juices, milk, and plant-based drinks while maintaining taste and quality standards. The fastest-growing end-user segment is pharmaceutical manufacturers, now adopting automated aseptic filling and sterilization systems at a 14% faster implementation rate than other sectors due to rising biologic production and stricter regulatory requirements. Other end-users, including nutraceutical producers and specialty liquid processors, contribute a combined 30% of the market, often deploying modular or small-batch systems to meet flexible production needs.

Asia Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

In 2024, Asia Pacific produced over 39 million metric tons of dairy products and 190 billion liters of beverages using aseptic packaging systems, while North America accounted for 27% of global aseptic equipment installations. Europe captured 20% of the market with strong regulatory compliance adoption. Asia Pacific’s growth is supported by large-scale manufacturing, rising urban consumption, and government infrastructure investment exceeding USD 28 billion annually, whereas North America’s expansion is driven by pharmaceutical sterile production and automation adoption. Across all regions, technological integration, ESG compliance, and consumer preference for preservative-free, shelf-stable products are shaping investment decisions and driving capacity expansion.

How are digital and automation trends transforming sterile production efficiency?

North America accounts for 27% of the global aseptic processing and packaging market, driven by pharmaceutical manufacturing, dairy, and ready-to-drink beverage industries. Regulatory changes, including stricter FDA sterile production guidelines, incentivize automation and quality control systems adoption. Advanced digital monitoring and AI-enabled sterilization validation have reduced contamination events by 22%, while robotics integration improves line utilization by 18%. A local player, Tetra Pak North America, recently upgraded multiple beverage lines with modular aseptic fillers and IoT-enabled sensors, achieving 15% faster changeovers. Consumer behavior emphasizes high safety standards and convenience, with enterprise adoption in healthcare and functional beverages exceeding 60%, reflecting a strong demand for sterile, ready-to-use products.

What role does sustainability and regulation play in driving market adoption?

Europe holds approximately 20% of the global aseptic processing and packaging market, with Germany, the UK, and France leading installations. Regulatory frameworks like EU food safety standards and circular economy mandates encourage adoption of recyclable high-barrier cartons and automated aseptic lines. Technological integration, including predictive maintenance, AI-based quality monitoring, and advanced sterilization systems, is expanding in the region. A prominent player, SIG Combibloc, has implemented energy-efficient aseptic filling systems in Germany, reducing production waste by 18%. European consumers prioritize product transparency and sustainable packaging, influencing manufacturers to adopt explainable aseptic processes and eco-friendly materials in over 50% of new installations.

How is infrastructure modernization driving regional expansion?

Asia Pacific captured 38% of the global aseptic processing and packaging market in 2024, with China, India, and Japan being top consumers. Investments exceeding USD 28 billion in advanced aseptic filling, sterilization, and packaging equipment are enabling high-volume dairy, beverages, and nutraceutical production. Automation penetration now exceeds 60% in urban production hubs, integrating robotics, IoT-based monitoring, and digital traceability systems. Local companies, such as Greatview Aseptic Packaging Co., have expanded aseptic carton production, enhancing shelf stability for over 200 million liters of beverages annually. Consumer behavior is increasingly driven by e-commerce and mobile ordering, accelerating adoption of ready-to-drink and long-shelf-life products.

What factors are shaping demand for aseptic solutions in emerging South American markets?

South America accounts for approximately 7% of the global aseptic processing and packaging market, with Brazil and Argentina as leading contributors. Growth is supported by investment in food and beverage infrastructure, particularly in dairy, juice, and ready-to-drink segments. Government incentives for modernizing processing plants and trade policies favoring local production encourage adoption of high-efficiency aseptic equipment. Local player Tetra Pak Brazil recently implemented advanced aseptic lines in multiple juice facilities, increasing operational efficiency by 12%. Regional consumer behavior favors culturally adapted beverages and localized nutrition products, driving specialized aseptic solutions.

How is industrial modernization influencing aseptic processing adoption?

Middle East & Africa represents roughly 8% of the global aseptic processing and packaging market, with the UAE and South Africa leading installations. Demand is driven by pharmaceutical, dairy, and beverage sectors in urban centers. Technological modernization, including automated aseptic fillers, digital monitoring, and sterilization optimization, is accelerating adoption. Local regulations increasingly enforce sterility compliance and hygiene standards, while trade partnerships encourage import of high-efficiency aseptic equipment. A regional player in South Africa recently upgraded aseptic lines in dairy production, reducing contamination risk by 15% and improving throughput. Consumer preference in urban hubs focuses on ready-to-use, preservative-free, and long-shelf-life beverages and nutrition products.

China: 24% market share – high production capacity and extensive beverage and dairy infrastructure drive adoption of advanced aseptic systems.

United States: 21% market share – strong pharmaceutical and dairy industry demand, coupled with regulatory push and automation adoption, reinforces market dominance.

The Aseptic Processing and Packaging market is highly competitive and moderately consolidated, with over 120 active global players operating across equipment manufacturing, sterilization systems, and packaging solutions. The top five companies—including Tetra Pak International, SIG Combibloc, Amcor plc, Elopak AS, and Greatview Aseptic Packaging Co.—together hold approximately 55% of the global market share, indicating a strong concentration among leading incumbents while the remaining 45% is fragmented among regional and niche suppliers. Key strategic initiatives shaping the competitive landscape include partnerships between automation technology providers and packaging firms, product launches of modular aseptic lines, and mergers to enhance technological capabilities in AI-enabled sterility monitoring, digital traceability, and high-throughput filling solutions. Innovation trends are focused on advanced sterilization methods, recyclable high-barrier materials, and modular construction, enabling faster project deployment and improved line efficiency. In 2025 alone, over 30 new automated aseptic systems were commissioned globally, reflecting aggressive investment by manufacturers to secure market share. Market positioning emphasizes technological leadership, operational efficiency, and sustainability compliance, which are increasingly critical for capturing enterprise clients in pharmaceuticals, beverages, and dairy sectors.

IMA Group

Krones AG

Marchesini Group

Multivac Sepp Haggenmüller GmbH

Bosch Packaging Technology

The Aseptic Processing and Packaging Market is being increasingly shaped by a convergence of automation, digitalization, and advanced sterilization technologies that enhance production efficiency, product safety, and operational resilience. Automated aseptic fillers now account for over 38% of global installations, providing precise liquid handling, minimal human intervention, and consistent microbial control across high-volume beverage and pharmaceutical lines. Sterilization technologies such as hydrogen peroxide vapor systems and electron-beam sterilizers are reducing cycle times by 20–30% while maintaining microbial contamination levels below 1 CFU per 10,000 units, allowing manufacturers to produce longer shelf-life products with improved safety metrics.

Emerging digital technologies, including IoT-enabled sensors and AI-driven quality monitoring, are being integrated into more than 45% of new aseptic lines. These systems provide real-time tracking of temperature, pressure, and sterility parameters, enabling predictive maintenance, reducing unplanned downtime by up to 18%, and improving first-pass yield by approximately 22%. Digital twins and cloud-based analytics platforms are increasingly adopted to simulate production processes, optimize line layouts, and validate aseptic procedures prior to physical implementation, enhancing speed-to-market for new products.

Material innovation is also playing a critical role, with recyclable high-barrier mono-material laminates and paper-based cartons now representing nearly 40% of packaging formats in developed markets. These materials provide oxygen and light barriers equivalent to traditional aluminum laminates while supporting ESG objectives such as 70% recyclability and 18% lower material intensity. Modular aseptic line construction, utilized in 55% of new installations, further accelerates deployment, reduces labor requirements by 35%, and ensures scalability. Collectively, these technologies are driving a shift toward flexible, sustainable, and fully automated aseptic production, enabling manufacturers to meet stringent regulatory, environmental, and consumer-driven quality standards.

• In March 2023, Tetra Pak launched an advanced aseptic filling line in Germany, integrating AI-based sterilization monitoring. The new system reduced microbial risk by 27% and increased line efficiency by 18%, supporting scalable production of dairy and plant-based beverages.

• In September 2023, SIG Combibloc introduced a high-barrier recyclable carton line in France, achieving 70% recyclability while maintaining shelf life of up to nine months for juice and dairy products. The implementation reduced material intensity by 20% across multiple production facilities.

• In May 2024, Greatview Aseptic Packaging Co. deployed modular aseptic filling units in China for functional beverages, enabling 40% faster product changeovers and reducing on-site labor requirements by 35%, significantly improving operational flexibility for small-batch production.

• In November 2024, Amcor plc unveiled an IoT-enabled aseptic packaging solution in the United States, integrating real-time temperature, pressure, and sterility monitoring. The system improved first-pass yield by 22% and minimized unplanned downtime by 18%, enhancing quality assurance in pharmaceutical and beverage lines.

The Aseptic Processing and Packaging Market Report provides a comprehensive assessment of global industry trends, technologies, applications, and regional adoption patterns. It covers multiple product types including aseptic fillers, sterilizers, preformers, and packaging lines, highlighting leading and emerging solutions in food, beverage, pharmaceutical, and nutraceutical sectors. Applications analyzed include dairy products, juices, ready-to-drink beverages, injectable pharmaceuticals, and functional nutrition products, reflecting operational and regulatory demands.

Geographically, the report examines market dynamics in Asia Pacific, North America, Europe, South America, and Middle East & Africa, with country-level insights for top contributors such as China, the United States, Germany, Brazil, and India. Technological focus includes automation, AI-driven quality monitoring, digital twins, IoT-based sensors, modular line construction, and sustainable high-barrier materials. The report also considers market drivers, restraints, challenges, and opportunities, offering measurable insights into operational efficiency, contamination risk reduction, material sustainability, and line flexibility. Emerging trends such as small-batch aseptic systems, recyclable mono-material packaging, and predictive maintenance in sterile production are also explored.

By encompassing both established and niche market segments, the report equips decision-makers with actionable intelligence on strategic investment areas, innovation priorities, regional consumption patterns, regulatory compliance, and ESG alignment, supporting informed planning and growth strategies in the aseptic processing and packaging ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 61456.23 Million |

Market Revenue in 2032 | USD 143682.62 Million |

CAGR (2025 - 2032) | 11.2% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Tetra Pak International, SIG Combibloc, Amcor plc, Elopak AS, Greatview Aseptic Packaging Co., IMA Group, Krones AG, Marchesini Group, Multivac Sepp Haggenmüller GmbH, Bosch Packaging Technology |

Customization & Pricing | Available on Request (10% Customization is Free) |