Reports

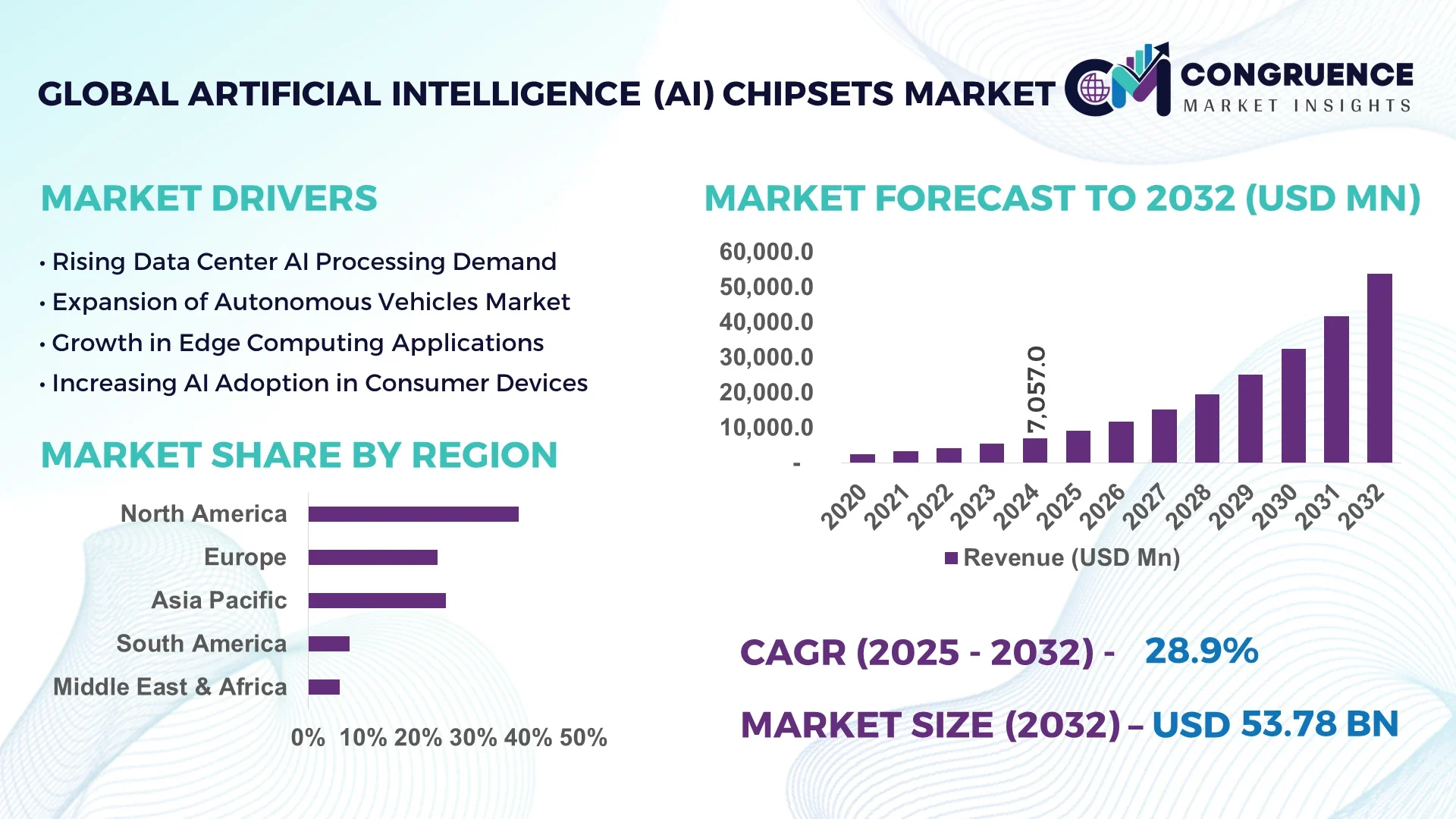

The Global Artificial Intelligence (AI) Chipsets Market was valued at USD 7,057.0 Million in 2024 and is anticipated to reach a value of USD 53,782.8 Million by 2032 expanding at a CAGR of 28.9% between 2025 and 2032.

China leads the marketplace through expansive national fabrication facilities, with wafer-foundry capacities exceeding 1 million 12-inch equivalent wafers per month. It continues to channel multibillion-dollar investments into advanced AI chipset R&D centers focused on edge-AI and deep-learning SoCs. Key industry applications include AI inference in autonomous vehicles, smart manufacturing vision systems, and next-generation telecom network accelerators, supported by rapid prototyping of AI hardware verified in pilot production.

The Artificial Intelligence (AI) Chipsets Market spans major industry sectors such as data center compute, automotive onboard AI, industrial robotics, consumer electronics (smartphones, AR/VR devices), and healthcare instrumentation. Data centers contribute a significant portion of chipset consumption through rack-scale AI accelerators used for model inference. In automotive, in-vehicle AI chipsets power driver-assistance systems and real-time sensor fusion. Recent technological innovations include heterogeneous integration of CPU-GPU-NPU components, 3D packaging with high-bandwidth interposers, and adaptive voltage-frequency scaling for energy-aware AI workloads. Regulatory and environmental drivers such as energy-efficiency mandates are encouraging low-power AI chipset designs. Economically, rising urbanization and smart-city deployments are boosting regional consumption in Asia-Pacific and Latin America. Emerging trends include the integration of photonic interconnects, hardware security enclaves, and domain-specific neural processing units targeted at real-time inferencing. The future outlook points toward increasing convergence of AI chipset functionality across edge and cloud environments, with modular design frameworks facilitating faster time-to-market for customized AI solutions.

Artificial Intelligence (AI) Chipsets Market transformation is being driven by AI-powered design automation, real-time workload profiling, and advanced on-chip optimization. AI-led electronic design automation (EDA) tools now generate optimized layout configurations that reduce power leakage and improve thermal distribution in high-density chiplet assemblies. Moreover, AI-driven test and validation frameworks analyze billions of gate-level simulation events to pinpoint defects early in the production process, raising yield rates by measurable margins. On the operations side, AI-based predictive maintenance systems deployed in fabrication plants monitor tool health in real-time, enabling unscheduled downtime to drop by double-digits, while throughput improves significantly. Within the Artificial Intelligence (AI) Chipsets Market, these interventions help manufacturers launch higher-performance chipsets with improved energy efficiency, tighter power-performance envelopes, and faster production ramp-up cycles. AI-enhanced process control also enables adaptive wafer-level tuning, dynamically adjusting voltages for varying workloads to ensure consistent performance. In sum, AI is redefining how Artificial Intelligence (AI) Chipsets Market participants design, validate, produce, and operate, embedding intelligence throughout the value chain and unlocking superior efficiency, reliability, and flexibility for industry decision-makers and professionals.

“In 2024, an AI-based layout optimization system reduced average power consumption of a production AI inference SoC design by 15 %, while reducing thermal hotspots so that on-chip temperature variance dropped by 8 % during high-load test phases.”

The Artificial Intelligence (AI) Chipsets Market Dynamics reflect a rapidly evolving value chain shaped by convergence of multiple technological and commercial trends. Decision-makers observe growing vertical collaboration between chipset designers, foundries, and end-users, accelerating system-level co-design. Meanwhile, modular chiplet architectures are replacing monolithic designs to enable faster customization. Supply-chain dynamics are also critical: demand for advanced packaging substrates and high-performance interconnects is leading to capacity expansions in specialized material suppliers. At the same time, geopolitical forces are prompting regional nurturing of domestic supply ecosystems. Eco-design certifications and energy-efficiency audits are increasingly embedded into development cycles, altering priorities in chipset development roadmaps. The Artificial Intelligence (AI) Chipsets Market is thus defined by intersecting influences—from collaborative design models to advanced manufacturing ecosystems—creating a complex, opportunity-rich environment for stakeholders.

Expanding requirements in sectors such as automotive, surveillance, industrial automation, and smart consumer devices are driving the need for chipsets optimized for low-latency edge inferencing. This surge is compelling design houses to invest in ultra-low-power NPUs and energy-efficient logic fabrics. Recent wafer fab surveys indicate emerging logic nodes tailored for edge AI, offering 20–30 % reductions in power per inference compared to prior generations, while maintaining throughput. For decision-makers, supporting this driver requires strategic alignment of design, packaging, and fab capacity to deliver highly power-efficient, compact AI chipsets for on-device intelligent tasks.

The Artificial Intelligence (AI) Chipsets Market faces constraints due to extended lead-times in advanced fabs and variability in yield rates for cutting-edge nodes like 3 nm/2 nm. Yield losses—measured in wafer rejects—remain at 10–15 % for the most advanced multilayer architectures. These pressures lead to supply bottlenecks, increase time-to-market cycles, and raise per-unit wafer production costs. As a result, chipset providers must balance pushing cutting-edge performance improvements against maintaining stable manufacturing pipelines and cost-effective volume deliveries.

Fragmenting complex AI chiplets into heterogeneously integrated modules allows reuse of proven IP blocks and simplified scaling. Industry prototypes show that modular die-stacked AI chiplets can reduce design iteration time by up to 40 %, facilitating faster customization for vertical markets such as automotive L2+/L3, smart robotics, and flexible consumer electronics. This trend enables firms in the Artificial Intelligence (AI) Chipsets Market to deliver tailored solutions more quickly and at lower NRE cost.

As performance densities escalate, managing on-chip thermal hotspots and power integrity becomes increasingly complex. Chipset designs targeting high-performance AI workloads must now incorporate multi-die power mesh systems, microfluidic cooling channels, or novel substrate materials. Implementing such systems adds design, validation, and production complexity, requiring new toolchains and manufacturing capabilities. Decision-makers must navigate these technical barriers to avoid thermal throttling and ensure reliable, long-term operation of AI-focused chipsets.

Modular chiplet integration accelerating time-to-market: A rising trend sees end-users selecting modular chiplet-based AI chipset platforms. By assembling pre-qualified IP blocks—CPU, GPU, NPU—design houses achieve development cycle reductions of 30-40 %. This modular integration streamlines both prototyping and mass customization workflows.

Energy-aware AI chiplet designs gaining traction: New power management schemes, including dynamic voltage and frequency scaling tailored to AI inference workloads, are now embedded in leading designs. These schemes yield measurable reductions in wafer-level energy draw—some platforms now operate with 25 % lower average power consumption during typical AI workloads.

Hardware security enclaves becoming standard: Secure AI inference is driving inclusion of hardware-based trust zones and encryption hardware in chipsets. Recent deployments in industrial control AI platforms show that chipsets with integrated security modules meet certification requirements while maintaining full real-time processing performance.

Photonic interconnects for scalable AI architectures: Adoption of on-chip or near-chip photonic links in advanced AI accelerators is rising. These interconnects enable 10× higher inter-die bandwidth with reduced electromagnetic interference, supporting emerging multi-chiplet AI systems designed for real-time analytics and autonomous systems.

The Artificial Intelligence (AI) Chipsets Market is structured into clearly defined segments based on type, application, and end-user categories, each serving distinct roles within the broader industry ecosystem. By type, the market includes GPU chipsets, ASIC chipsets, FPGA chipsets, CPU chipsets, and emerging neuromorphic processors. Applications span from data center processing and edge computing to autonomous vehicles, robotics, and consumer electronics. End-user segments include technology and cloud service providers, automotive manufacturers, industrial automation firms, and healthcare technology companies. Each segment demonstrates differing adoption patterns, driven by technological suitability, deployment scale, and sector-specific innovation cycles. The interplay between these categories determines chipset design priorities, manufacturing strategies, and regional investment flows, making segmentation analysis essential for strategic planning and market positioning.

In the Artificial Intelligence (AI) Chipsets Market, GPU chipsets hold the leading position due to their unmatched parallel processing capabilities, making them indispensable for training large-scale AI models and performing high-volume inferencing tasks. Their architecture enables efficient handling of complex neural network computations, which is critical for AI workloads in data centers and high-performance computing environments. The fastest-growing segment is ASIC chipsets, driven by their highly optimized designs for specific AI workloads, such as natural language processing and image recognition, offering greater efficiency and lower power consumption compared to general-purpose processors. FPGA chipsets maintain a niche yet important role, providing flexibility in prototyping and deployment of specialized AI solutions in sectors like defense and aerospace. CPU chipsets, while not the primary drivers for AI-specific functions, continue to play an enabling role in hybrid systems where general-purpose processing is needed alongside AI accelerators. Neuromorphic processors, though at an early stage of commercialization, are attracting growing interest for their potential to mimic biological neural systems, enabling low-power, real-time AI processing in edge devices.

Data center processing represents the leading application in the Artificial Intelligence (AI) Chipsets Market, supported by the continuous expansion of AI-driven services, cloud platforms, and large-scale model training demands. These environments require high-performance, scalable chipsets capable of delivering massive computational throughput. The fastest-growing application is autonomous vehicles, fueled by advancements in sensor fusion, real-time decision-making algorithms, and the need for ultra-low-latency processing to ensure passenger safety. Edge computing applications are also gaining traction, particularly in industrial IoT and smart city infrastructure, where AI chipsets enable local data processing to reduce latency and bandwidth usage. Robotics applications, encompassing industrial automation, collaborative robots, and autonomous drones, rely on specialized chipsets to manage real-time control and vision-based navigation. Consumer electronics, including AI-enabled smartphones, AR/VR devices, and smart home systems, continue to integrate AI chipsets to enhance user experience and device intelligence, ensuring broad adoption across multiple end-use scenarios.

Technology and cloud service providers lead the end-user segment in the Artificial Intelligence (AI) Chipsets Market, as they operate large-scale data centers and deliver AI-as-a-service platforms that depend on high-performance computing infrastructure. Their investment in AI chipset deployment is driven by the need to handle ever-increasing volumes of AI model training and inference workloads with maximum efficiency. The fastest-growing end-user category is the automotive sector, propelled by the rapid integration of AI systems in autonomous driving, advanced driver assistance systems, and in-vehicle infotainment solutions. Industrial automation companies also represent a significant share, utilizing AI chipsets to power predictive maintenance, quality control, and robotics-based manufacturing processes. Healthcare technology firms are emerging as critical adopters, leveraging AI chipsets for diagnostic imaging, predictive analytics, and personalized treatment planning. Smaller yet notable contributions come from defense, energy, and telecommunications industries, where AI chipsets are embedded into mission-critical systems requiring secure, reliable, and real-time processing capabilities.

North America accounted for the largest market share at 38.2% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 27.8% between 2025 and 2032.

The North American market benefits from strong investments in AI infrastructure, high penetration of cloud service providers, and mature semiconductor manufacturing capabilities. Meanwhile, Asia-Pacific’s accelerated growth is fueled by rising AI adoption across manufacturing, automotive, and consumer electronics industries, particularly in China, Japan, and South Korea. Both regions are witnessing increasing demand for advanced processors capable of handling complex AI workloads, driving innovation in GPU, ASIC, and FPGA technologies.

North America held approximately 38.2% of the global Artificial Intelligence (AI) Chipsets market in 2024, driven by a robust ecosystem of technology companies, AI startups, and hyperscale data center operators. The United States remains the largest contributor, supported by strong demand from sectors such as autonomous vehicles, cloud computing, defense, and healthcare analytics. Regulatory support for AI innovation and federal investments in semiconductor manufacturing have further strengthened the market position. Technological advancements such as next-generation GPUs, neuromorphic processors, and edge AI chipsets are enabling faster processing speeds and energy-efficient computing, aligning with the region’s digital transformation agenda.

Europe accounted for around 23.5% of the Artificial Intelligence (AI) Chipsets market in 2024, with Germany, the UK, and France being the leading contributors. The market is shaped by the European Union’s stringent data protection laws, AI ethics frameworks, and sustainability-focused semiconductor production policies. Industries such as automotive manufacturing, industrial automation, and healthcare are key adopters of AI chipsets. The adoption of emerging technologies such as edge AI, AI-enabled robotics, and smart city infrastructure is accelerating. Europe’s coordinated approach to AI governance, combined with strong R&D capabilities, positions the region as a hub for ethical and sustainable AI chipset innovation.

Asia-Pacific ranked second in market size in 2024 and is the fastest-growing region in the Artificial Intelligence (AI) Chipsets industry. China, Japan, and India lead consumption, supported by expansive electronics manufacturing, 5G infrastructure deployment, and large-scale AI adoption in sectors such as retail, healthcare, and industrial automation. The region is home to major semiconductor fabrication plants and innovation hubs that are pioneering advancements in AI-specific hardware. Governments across Asia-Pacific are actively supporting AI R&D, creating favorable environments for local and global companies to expand their AI chipset production and distribution capabilities.

South America accounted for a smaller share of the global Artificial Intelligence (AI) Chipsets market in 2024, with Brazil and Argentina emerging as the key markets. Growing investments in cloud computing infrastructure, fintech, and smart agriculture are driving demand for AI chipsets. Brazil’s technology sector is rapidly integrating AI-powered solutions across finance, healthcare, and e-commerce, while Argentina is witnessing growth in AI-enabled manufacturing processes. Regional governments are offering tax incentives and trade agreements to encourage AI adoption, while infrastructure upgrades and energy sector modernization are enabling broader AI chipset deployment.

The Middle East & Africa region is experiencing growing demand for Artificial Intelligence (AI) Chipsets, driven by applications in oil & gas, construction, defense, and smart city projects. The UAE, Saudi Arabia, and South Africa are leading markets, supported by national AI strategies and investments in digital infrastructure. The adoption of AI in predictive maintenance, industrial automation, and public services is accelerating. Regulatory frameworks encouraging AI innovation and partnerships with global semiconductor firms are enhancing the region’s AI capabilities. Technological modernization in data centers and telecom networks is also contributing to the expansion of AI chipset demand.

United States – 32.5% Market Share

Strong dominance in AI chipset design and production, backed by leading tech companies and hyperscale cloud service providers.

China – 25.8% Market Share

High manufacturing capacity and rapid adoption of AI in industrial, consumer electronics, and smart city applications.

The competitive environment in the Artificial Intelligence (AI) Chipsets Market features approximately 15–20 active competitors, ranging from fabless semiconductor firms to integrated device manufacturers and foundries offering packaged AI accelerators. Leading participants maintain strong market positioning by pursuing strategic initiatives such as partnerships with hyperscale cloud operators and automotive OEMs, launching purpose-built AI accelerator chipsets, or acquiring niche design houses to expand their IP portfolios. Several firms are adopting licensing models for AI architectures to broader device ecosystems. Innovation trends shaping competition include advances in chiplet modularity, secure AI enclave integration, and heterogeneous integration of CPU-GPU-NPU subsystems. Players are also implementing next-generation interposer technologies and silicon photonic links. Firms differentiate through low-power edge-AI modules, domain-specific inference engines, and highly parallel training accelerators, making R&D pipeline and alliance formation critical to maintaining leadership in a fast-moving, technology-intensive market.

NVIDIA

Intel

AMD

Qualcomm

Samsung Electronics

MediaTek

Broadcom

Xilinx (part of AMD)

Qualcomm

Graphcore

Current and emerging technologies reshaping the Artificial Intelligence (AI) Chipsets Market include high-bandwidth memory (HBM) stacking, 3D integrated chiplet architectures, photonic interconnects, and domain-specific neural processing units (NPUs). HBM stacking enables up to tenfold higher memory throughput, critical for model training workloads. Chiplet architectures, employing standardized mesh interconnects, shorten design cycles and allow modular reuse across product lines. On-chip photonic links now deliver gigabit-scale inter-die communication with minimal latency and reduced electromagnetic interference, making multi-chip assemblies more scalable. Secure enclaves embedded within AI chipsets ensure encrypted inference pipelines and protection of IP in edge deployments. Additionally, energy-adaptive logic fabrics based on dynamic voltage-frequency scaling (DVFS) tailored to neighbor-aware AI inference workload profiles are emerging. In edge AI, neuromorphic cores replicating spiking neuron models are being prototyped to achieve real-time processing with milliwatt-level power envelopes. Together, these technologies are enabling differentiated performance, scalability, energy efficiency, and security in AI chipset design—critical levers for decision-makers in procurement and development.

In Q1 2023, a leading fabless designer unveiled a new edge-AI chipset featuring integrated dual NPUs and memory-aware power gating, enabling real-time vision processing with device-level power consumption below 0.5 W.

In late 2023, a major AI accelerator provider entered a strategic partnership with an automotive OEM to co-develop a compact inference module optimized for lidar and radar fusion, targeting SAE Level-4 autonomy.

In mid-2024, an integrated manufacturer launched a modular AI chipset platform combining CPU, GPU, and programmable logic blocks in a single interposer, supporting rapid customization for robotics and industrial AI applications.

In early 2024, a chiplet architecture consortium released an open standard silicon-photonic interconnect aimed at enabling scalable multi-die AI systems with ten times higher bandwidth than traditional copper interconnects.

This Report encompasses a comprehensive assessment of the Artificial Intelligence (AI) Chipsets Market across multiple dimensions, providing decision-makers with clarity on structure and focus. Geographically, it covers regional landscapes of North America, Europe, Asia-Pacific, South America, and Middle East & Africa, assessing regional infrastructure, manufacturing ecosystems, and deployment scenarios. Segmentation includes technology types such as GPU, ASIC, FPGA, CPU, and neuromorphic processors; application verticals spanning data centers, automotive systems, edge computing, consumer electronics, industrial automation, robotics, and healthcare instrumentation; and end-user categories including cloud service providers, automotive OEMs, industrial integrators, healthcare tech firms, and consumer device makers. The report also analyzes emerging niches such as photonic-coupled chiplet assemblies, secure enclave-enabled inference modules, and ultra-low-power neuromorphic edge AI processors. Insights on manufacturing trends (foundry versus in-house production), digital transformation drivers, sustainability mandates, and competitive strategies are regularly updated. This scope ensures a strategic and holistic view—empowering stakeholders across procurement, design, investment, and policy functions to navigate the evolving AI chipset landscape.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 7,057.0 Million |

| Market Revenue (2032) | USD 53,782.8 Million |

| CAGR (2025–2032) | 28.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | NVIDIA, Intel, AMD, Qualcomm, Samsung Electronics, MediaTek, Broadcom, Xilinx (part of AMD), Qualcomm, Graphcore |

| Customization & Pricing | Available on Request (10% Customization is Free) |