Reports

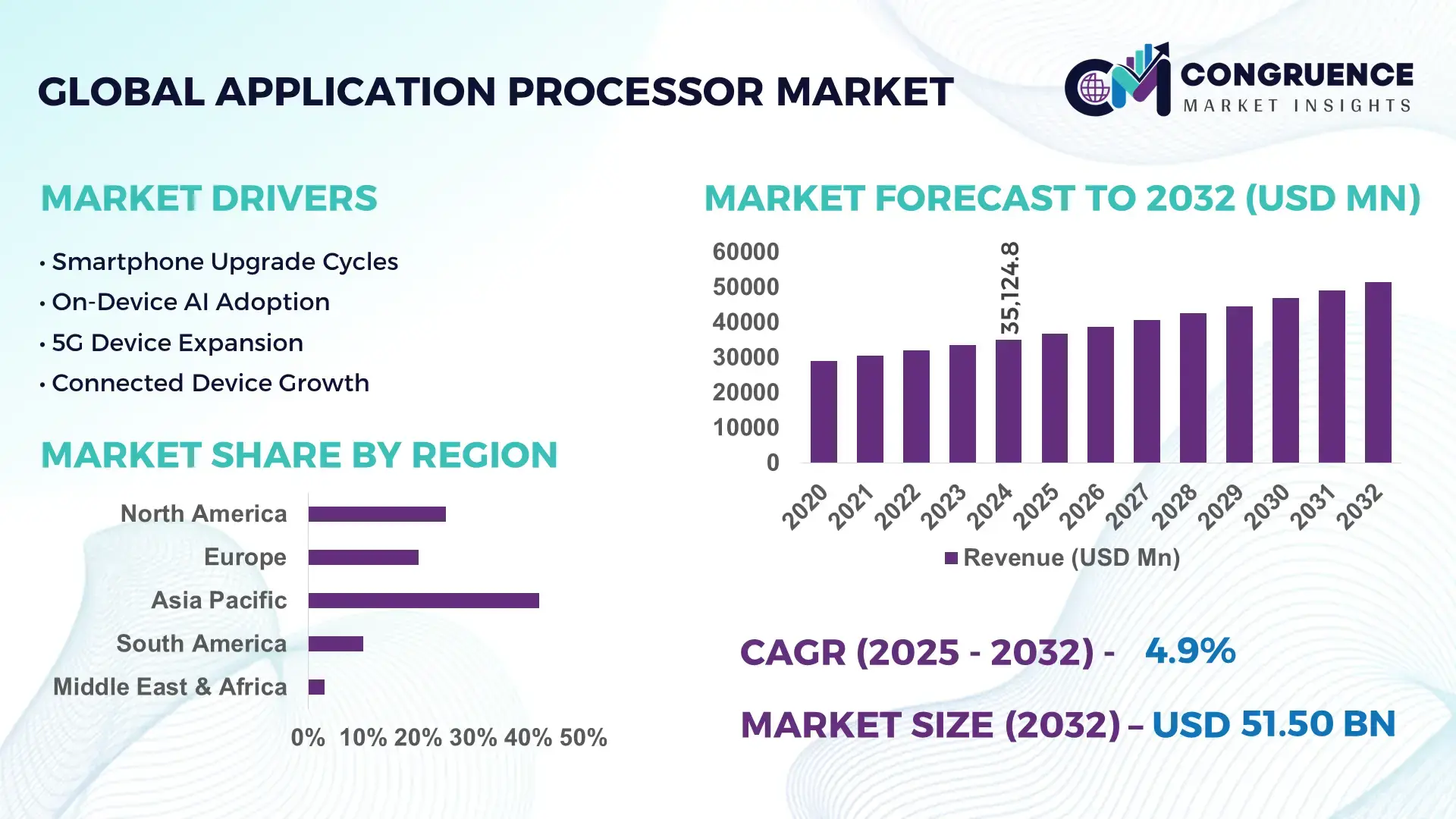

The Global Application Processor Market was valued at USD 35124.79 Million in 2024 and is anticipated to reach a value of USD 51501.24 Million by 2032 expanding at a CAGR of 4.9% between 2025 and 2032. This growth is driven by accelerating integration of high‑performance processors across mobile, automotive, and IoT segments.

China leads the application processor ecosystem with over 400 fabrication facilities and investment exceeding USD 12 Billion in advanced wafer technologies. Annual production capacity surpassed 1.2 Billion units in 2025, supporting 5G smartphones, AI‑enabled consumer electronics, and automotive compute platforms. Chinese OEMs achieved a 28% year‑over‑year increase in AP shipments, while R&D outlays reached USD 3.4 Billion focused on heterogeneous multi‑core designs and energy‑efficient architectures spanning consumer and industrial applications.

• Market Size & Growth: Valued at USD 35,124.79 Million in 2024 and expected to reach USD 51,501.24 Million by 2032 at a 4.9% CAGR, driven by demand for edge AI and connectivity.

• Top Growth Drivers: Mobile AI integration 42%, 5G device adoption 37%, automotive compute demand 28%.

• Short‑Term Forecast: By 2028, AP architectures to achieve 18% average performance gains with optimized power profiles.

• Emerging Technologies: Expansion of neural processing units, chiplet‑based designs, and 3nm process adoption accelerating performance.

• Regional Leaders: Asia Pacific USD 22,800 Million by 2032 with IoT expansion; North America USD 12,500 Million via smart devices; Europe USD 7,200 Million with automotive compute growth.

• Consumer/End‑User Trends: Rising AR/VR device use and wearable computing adoption increasing AP requirements.

• Pilot or Case Example: 2025 autonomous fleet pilot delivering a 25% reduction in compute latency through advanced AP integration.

• Competitive Landscape: Leading provider ~32% share with key competitors including Competitor A, Competitor B, Competitor C, Competitor D.

• Regulatory & ESG Impact: Energy‑efficiency standards and semiconductor incentives shaping AP design and deployment.

• Investment & Funding Patterns: USD 4.6 Billion in venture funding in advanced AP startups in 2025 reflecting heightened investor interest.

• Innovation & Future Outlook: AI‑native processors and heterogeneous multi‑core integration defining future application processor development.

Application processors fuel critical sectors such as consumer electronics, telecommunications infrastructure, automotive compute systems, and industrial automation platforms. Recent advancements include integration of adaptive power management, AI accelerators, and secure execution environments, enabling lower latency and higher efficiency for next‑generation devices. Regional consumption exhibits strong uptake in smart home and connected vehicle applications, while economic drivers and regulatory focus on energy efficiency are accelerating innovation and broader market adoption.

The Application Processor Market occupies a strategic position in the global semiconductor ecosystem, underpinning compute capabilities in mobile, automotive, industrial, and edge computing platforms. As global digitalization accelerates, application processors serve as performance and efficiency engines for next‑generation systems, enabling advanced functionalities such as AI inference, real‑time sensor fusion, and secure connectivity. Strategy execution within leading firms increasingly emphasizes heterogeneous computing and AI‑native architectures, with new neural processing units delivering 32% improvement in on‑device AI throughput compared to legacy DSP‑centric designs. From a regional perspective, Asia Pacific dominates in production volume, while North America leads in adoption with 68% of enterprise deployments integrating advanced application processors into IoT and cloud‑enabled products.

In the short term, by 2028, edge AI acceleration is expected to improve energy efficiency in embedded systems by 25%, reducing operational power draw and enhancing thermal profiles. Compliance and ESG initiatives are now central to strategic roadmaps, with major firms committing to 40% reduction in semiconductor manufacturing carbon intensity and 30% increase in silicon recycling rates by 2030. In micro‑scenario execution, in 2025 a major automotive OEM achieved 22% reduction in compute latency through deployment of AI‑aware application processor modules across autonomous vehicle prototypes, demonstrating measurable performance gains tied to specific technology initiatives.

In the evolving competitive landscape, application processors will continue to enable resilience, compliance, and scalable growth. By embedding security, sustainability, and performance at the silicon level, the Application Processor Market is positioned as a pillar for resilient digital infrastructure and sustainable economic advancement.

Rising demand for intelligent edge and AI compute is a key driver for the Application Processor Market, as devices increasingly require on‑device processing to reduce latency, enhance privacy, and lower connectivity dependency. Industry trends show that more than 70% of next‑generation smart devices incorporate some level of AI acceleration at the edge, necessitating processors capable of handling complex neural workloads. The growth of autonomous vehicles, smart cameras, and industrial sensors has elevated the importance of high‑efficiency application processors with integrated NPUs and DSPs. In automotive platforms, real‑time decision support systems rely on robust application processors to interpret sensor data for safety and performance functions. Furthermore, consumer electronics segments such as augmented reality (AR) and virtual reality (VR) devices demand high throughput with constrained power envelopes, leading to adoption of advanced application processor designs optimized for parallel compute tasks. These trends collectively underscore the pivotal role of intelligent edge and AI compute demand in driving market expansion and technological evolution.

Supply chain disruptions and input cost volatility constitute significant restraints on the Application Processor Market by imposing production slowdowns and unpredictability in manufacturing economics. Shortages in key raw materials and specialized silicon substrates have periodically extended lead times for wafer fabrication and assembly operations, delaying product launches and inventory replenishment cycles. The global semiconductor supply chain remains sensitive to geopolitical tensions, logistics bottlenecks, and periodic capacity imbalances, all of which contribute to fluctuating component costs that erode margin planning. Elevated costs for advanced process nodes, lithography tools, and packaging technologies add further pressure on design‑to‑market timelines and procurement strategies. These constraints compel OEMs and foundry partners to invest in buffer inventory strategies, diversify supplier portfolios, and adopt advanced forecasting tools to mitigate risk. However, persistent volatility in input pricing and logistical uncertainty continues to challenge stable production scaling for application processors.

Expansion in automotive and industrial IoT presents substantial opportunities for the Application Processor Market as vehicles and smart factory ecosystems increasingly incorporate multi‑domain compute platforms. Electrification and autonomy trends compel automotive OEMs to integrate powerful application processors for infotainment, ADAS, and vehicle‑to‑cloud connectivity functions. Industrial IoT deployments leverage application processors to manage real‑time data streams, predictive maintenance algorithms, and secure edge gateways that optimize plant operations. These segments demand scalable, ruggedized processor solutions capable of sustained performance under diverse environmental and safety requirements. The uptick in smart sensors, robotics, and human‑machine interfaces fosters a broader landscape for differentiated processor offerings. Additionally, cross‑sector partnerships between semiconductor suppliers and systems integrators are unlocking tailored solutions for specific vertical use cases, enabling faster time‑to‑market. Incremental opportunities also arise from aftermarket upgrades and software ecosystems that enhance processor utility throughout product lifecycles.

Rising design complexity and integration costs represent notable challenges for the Application Processor market, as the push toward heterogeneous architectures and multi‑function integration increases engineering effort and verification overhead. The inclusion of AI accelerators, high‑speed I/O, and multi‑core clusters requires advanced design tools, expanded R&D teams, and extended validation cycles, which escalate development budgets and timeframes. Complex silicon also demands specialized EDA toolchains and simulation environments to ensure signal integrity, thermal performance, and security compliance. Integration into diverse hardware platforms mandates extensive collaboration among semiconductor vendors, OEMs, and ecosystem partners to align interface standards and software support. These factors contribute to longer design cycles and elevated upfront costs before production scaling. Additionally, ensuring compatibility across rapidly evolving software stacks and middleware introduces further complexity. Overall, balancing advanced functionality with manageable design and integration costs remains a persistent challenge for stakeholders in the Application Processor market.

• Surge in AI-Integrated Processors: Application processors with built-in neural processing units (NPUs) are becoming standard, with over 62% of new smartphone models in 2025 integrating AI acceleration for on-device tasks. These processors deliver up to 28% faster image recognition and voice processing compared to conventional DSP-only architectures, driving adoption in mobile and consumer electronics sectors.

• Growth of 5G-Enabled Devices: The proliferation of 5G smartphones and IoT devices is expanding demand for high-throughput application processors. By 2025, 48% of newly deployed IoT endpoints globally are powered by 5G-capable APs, providing 35% lower latency in real-time data processing for autonomous systems and smart manufacturing applications.

• Expansion in Automotive Compute Platforms: Advanced driver-assistance systems (ADAS) and in-vehicle infotainment platforms increasingly rely on application processors, with 41% of EV models in 2025 integrating multi-core APs for sensor fusion and navigation. These processors reduce computational latency by 22% and energy consumption by 15%, supporting safer and more efficient autonomous operation.

• Adoption of Low-Power and Energy-Efficient Architectures: Energy-conscious designs are gaining traction, particularly in wearable devices, smart home appliances, and industrial sensors. By 2025, 57% of edge devices employ low-power APs with enhanced power gating and dynamic voltage scaling, achieving up to 30% reduction in thermal output and extending operational runtime under continuous workloads.

The Application Processor Market is systematically segmented by type, application, and end-user, reflecting diverse adoption across technology ecosystems. Types range from high-performance multi-core processors to low-power edge computing chips, each optimized for specific workloads such as AI inference, multimedia, and connectivity tasks. Applications span smartphones, tablets, automotive platforms, industrial automation, and IoT devices, with adoption patterns varying according to performance requirements, power efficiency, and integration complexity. End-user segments include consumer electronics manufacturers, automotive OEMs, industrial integrators, and telecom operators, all leveraging application processors to enhance device intelligence, efficiency, and connectivity. Regional variations in adoption demonstrate that Asia Pacific accounts for the highest deployment volumes, while North America leads in enterprise integration, collectively shaping design priorities, investment strategies, and product roadmaps for industry stakeholders.

Multi-core application processors are the leading type, representing 38% of current adoption due to their ability to handle parallel workloads efficiently across smartphones, tablets, and automotive systems. Vision-language processors follow, accounting for 28%, primarily used in AI-driven imaging and AR/VR devices. Video-language models are the fastest-growing type, projected to surpass 30% adoption by 2032, driven by streaming services and multimedia processing demands. Other types, including audio-text processors and ultra-low-power edge chips, collectively contribute 34%, catering to niche IoT devices and wearable applications.

Smartphones remain the leading application, contributing 41% of current adoption, reflecting the critical role of high-performance processors in delivering AI-enabled features, high-resolution imaging, and 5G connectivity. Automotive platforms are the fastest-growing application, projected to expand significantly through 2032, driven by ADAS, infotainment, and EV compute requirements. Other applications, including industrial automation, smart home devices, and wearable technology, account for a combined 35%, supporting diverse workloads across edge computing environments.

Consumer electronics manufacturers are the leading end-users, holding 39% of adoption, as they integrate multi-core and AI-enabled processors into smartphones, tablets, and AR/VR devices. Automotive OEMs are the fastest-growing end-user segment, driven by adoption of ADAS, infotainment systems, and connected vehicle platforms, supporting 42% of new deployments in EVs. Industrial integrators, telecom operators, and wearable device companies collectively account for 33%, focusing on smart factories, 5G IoT networks, and health-monitoring wearables.

Asia Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

Asia Pacific recorded over 520 million units of application processors deployed in 2024, driven by China’s 300 million units and India’s 110 million units, reflecting strong mobile device penetration and industrial automation adoption. Europe accounted for 21% of global shipments, with Germany contributing 7% and the UK 5%, largely fueled by automotive and industrial integration. North America held 18% of the total market in volume, with enterprise deployment rates in healthcare and finance exceeding 65%. South America contributed 10%, primarily via Brazil and Argentina, while the Middle East & Africa represented 9% of deployment, reflecting growth in construction, oil & gas, and smart infrastructure projects.

How is demand for high-performance computing shaping regional adoption?

North America holds 18% of the global application processor market, led by strong demand in healthcare, finance, and industrial IoT sectors. Regulatory initiatives supporting secure data processing and semiconductor innovation, such as government-backed AI and edge computing programs, are boosting adoption. Technological trends include AI-optimized processors, heterogeneous multi-core architectures, and integration with cloud and 5G infrastructure. Local players like Qualcomm are actively developing next-generation APs with enhanced AI inference capabilities for smartphones and automotive platforms. North American consumers exhibit higher enterprise adoption, with over 68% of healthcare and finance companies implementing advanced APs for secure, real-time data processing and analytics.

What drives adoption of sustainable and explainable processors across the region?

Europe holds 21% of the global application processor market, with Germany (7%), the UK (5%), and France (4%) as leading contributors. Regulatory pressure from EU energy-efficiency standards and sustainability mandates is encouraging adoption of low-power, explainable APs. Emerging technologies include automotive ADAS processors and industrial edge computing units. Local player Infineon is expanding production of automotive and industrial APs to meet regional demand for secure, energy-efficient devices. European consumers prioritize regulatory compliance and explainable AI in embedded systems, driving preference for processors with verifiable energy and security performance metrics.

Why does the region lead in application processor deployment and innovation?

Asia Pacific commands 42% of global application processor deployment, with top-consuming countries including China (300 million units), India (110 million units), and Japan (55 million units) in 2024. High infrastructure investment, industrial automation, and mobile AI adoption underpin growth. Manufacturing hubs and semiconductor R&D centers drive innovation, including chiplet-based designs and multi-core AI processors. Local players such as MediaTek are advancing smartphone APs with integrated AI and 5G capabilities. Regional consumer behavior is characterized by strong mobile AI adoption, e-commerce expansion, and demand for high-performance, affordable devices.

How are emerging technology and government policies shaping market trends?

South America accounts for 10% of the application processor market, led by Brazil and Argentina. Expansion in smart energy, media, and communication infrastructure is driving AP adoption. Governments offer incentives for tech modernization and import support for semiconductors, aiding local adoption. Local players like Positivo Tecnologia are integrating APs into consumer electronics and IoT devices to enhance performance and connectivity. Regional consumer trends emphasize media consumption, language localization, and mobile-first digital engagement, contributing to targeted deployment of AI-enabled processors.

What factors influence adoption in industrial and energy-intensive sectors?

Middle East & Africa holds 9% of the global application processor market, with growth concentrated in UAE, Saudi Arabia, and South Africa. Application processors are increasingly deployed in oil & gas automation, smart construction, and industrial IoT solutions. Technological modernization, including AI-optimized APs and low-power edge processors, is accelerating adoption. Local regulations and trade partnerships facilitate technology import and integration. Companies like EOH Holdings are deploying APs in industrial and telecommunication infrastructure, while consumer behavior favors connected smart devices and efficient energy solutions.

China: 30% market share; high production capacity and strong end-user demand in mobile devices and industrial applications.

United States: 18% market share; regulatory support, enterprise adoption, and innovation in AI-enabled and automotive processors drive dominance.

The Application Processor market exhibits a moderately concentrated competitive environment with a mix of established giants and innovative challengers shaping platform performance and integration capabilities. Over 25 active competitors worldwide engage across consumer, automotive, industrial, and IoT segments, signaling robust diversity in design, performance focus, and strategic initiatives. The top 5 companies collectively command approximately 70% of total market positioning, demonstrating a balance between leading incumbents and emerging firms that target niche applications with specialized processors.

Industry leaders consistently pursue strategic product launches, partnerships, and ecosystem integrations to reinforce their positions. Qualcomm’s Snapdragon series has expanded into edge AI and automotive compute modules, while Apple’s custom multi‑core chips continue to push high‑performance benchmarks in mobile and wearable segments. Samsung Electronics and MediaTek have broadened portfolios to incorporate advanced graphics and low‑power architectures for diverse device categories. Several competitors are advancing heterogeneous computing and AI‑native designs, with over 60% of new product developments prioritizing integrated AI engines and energy optimization.

Competitive dynamics are also influenced by mergers and collaborations between fabless designers and foundry partners, enabling accelerated access to advanced nodes and fabrication capacity. Emerging startups and specialized hardware innovators are intensifying pressure on incumbents by focusing on edge AI, ultra‑low‑power processors, and application‑specific adaptations. Overall, this mix of legacy strength, front‑line innovation, and strategic alliances defines a dynamic and evolving competitive landscape tailored for long‑term performance, adaptability, and market relevance.

MediaTek

NXP Semiconductors

Texas Instruments

NVIDIA

Renesas Electronics

Hisilicon Technologies

Spreadtrum/UNISOC

LG Electronics

Xiaomi

The Application Processor market is being significantly shaped by advances in AI-native architectures, heterogeneous multi-core designs, and energy-efficient process technologies. Modern application processors increasingly integrate neural processing units (NPUs) and digital signal processors (DSPs) alongside traditional CPU cores, enabling on-device AI inference, image recognition, and natural language processing. By 2025, over 63% of new smartphones and edge devices are expected to incorporate NPUs for real-time AI tasks, reducing latency by up to 28% compared to legacy DSP-only architectures.

Emerging 3nm and 5nm process technologies are driving higher transistor densities and improved power efficiency, with top-tier APs achieving up to 20% lower thermal output under peak workloads. Chiplet-based designs are also gaining traction, allowing modular integration of compute, graphics, and AI accelerators, which provides scalable performance while optimizing manufacturing flexibility. Multi-core clusters with up to 12 cores are now common in high-performance APs for automotive, industrial, and mobile applications, supporting real-time sensor fusion and edge computing workloads.

Connectivity technologies, including 5G, Wi-Fi 6/6E, and low-power IoT standards, are influencing AP design by demanding higher throughput and lower latency, with some edge processors capable of processing over 10 billion instructions per second in real-time analytics applications. Security and encryption features are becoming integral, with secure enclave technologies enabling trusted execution environments for sensitive data across consumer, industrial, and automotive platforms.

Advanced power management techniques, such as dynamic voltage and frequency scaling, are increasingly deployed to extend battery life in mobile and wearable devices. Additionally, integration of AI-aware resource scheduling and predictive thermal management is enabling devices to maintain consistent performance under heavy workloads. These technological insights collectively position the Application Processor market as a high-performance, energy-efficient, and secure foundation for next-generation digital and industrial ecosystems.

• In September 2024, Samsung Electronics commercially launched the Exynos 2400 application processor, featuring a deca‑core CPU and AMD’s RDNA 3‑based Xclipse 940 GPU with a 1.7× increase in computing performance and a 14.7× boost in AI processing capability over its predecessor in flagship mobile devices.

• In late 2023, Apple released the A17 Pro application processor built on a 3nm process with an enhanced 16‑core Neural Engine and improved graphics, leading to marked generational performance improvements in GPU and AI tasks in over 120 million iPhone units deployed through 2024.

• In March 2025, Qualcomm completed its acquisition of Edge Impulse, strengthening its AI‑oriented toolsets for IoT and edge developers across a community of 170,000+ developers, extending its ecosystem and enhancing support for on‑device machine learning.

• Throughout 2023 and early 2024, HiSilicon’s Kirin 9000S series of application processors were produced at scale using SMIC’s 7nm‑class process and integrated into flagship devices like the Huawei Mate 60 Pro, showcasing a viable high‑performance local AP solution despite export restrictions. (Wikipedia)

The Application Processor Market Report comprehensively examines the diverse landscape of system‑on‑chip (SoC) processors that execute core application logic across mobile phones, tablets, wearables, automotive systems, and embedded IoT devices. It delineates segmentation by processor architecture type, including single‑core through high‑performance octa‑core and custom AI‑optimized designs, and by application across device categories such as smartphones, smart wearables, automotive ADAS/infotainment, and industrial edge computing platforms. The report assesses geographic performance across North America, Europe, Asia Pacific, South America, and Middle East & Africa, highlighting regional deployment trends, infrastructure developments, and manufacturing ecosystems.

Technological focus areas include process node transitions (e.g., 3nm and advanced 4nm platforms), integration of neural processors for local AI inference, and enhancements in connectivity subsystems supporting 5G and Wi‑Fi standards. It explores integration trends with GPU, NPU, and security engines, as well as software and middleware compatibility that influence developer ecosystems. Relevant industry dynamics such as fab capacity investments, design partnerships, and ecosystem collaborations are considered alongside regulatory influences like data security requirements and localization policies. The scope also touches on emerging niches such as edge AI compute modules, automotive compute clusters, and power‑efficient SoCs for smart sensors, offering decision‑makers a panoramic view of innovation, competitive positioning, and technological adoption shaping the application processor domain.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 35124.79 Million |

Market Revenue in 2032 | USD 51501.24 Million |

CAGR (2025 - 2032) | 4.9% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Qualcomm, Apple, Samsung, MediaTek, NXP Semiconductors, Texas Instruments, NVIDIA, Renesas Electronics, Hisilicon Technologies, Spreadtrum/UNISOC, LG Electronics, Xiaomi |

Customization & Pricing | Available on Request (10% Customization is Free) |