Reports

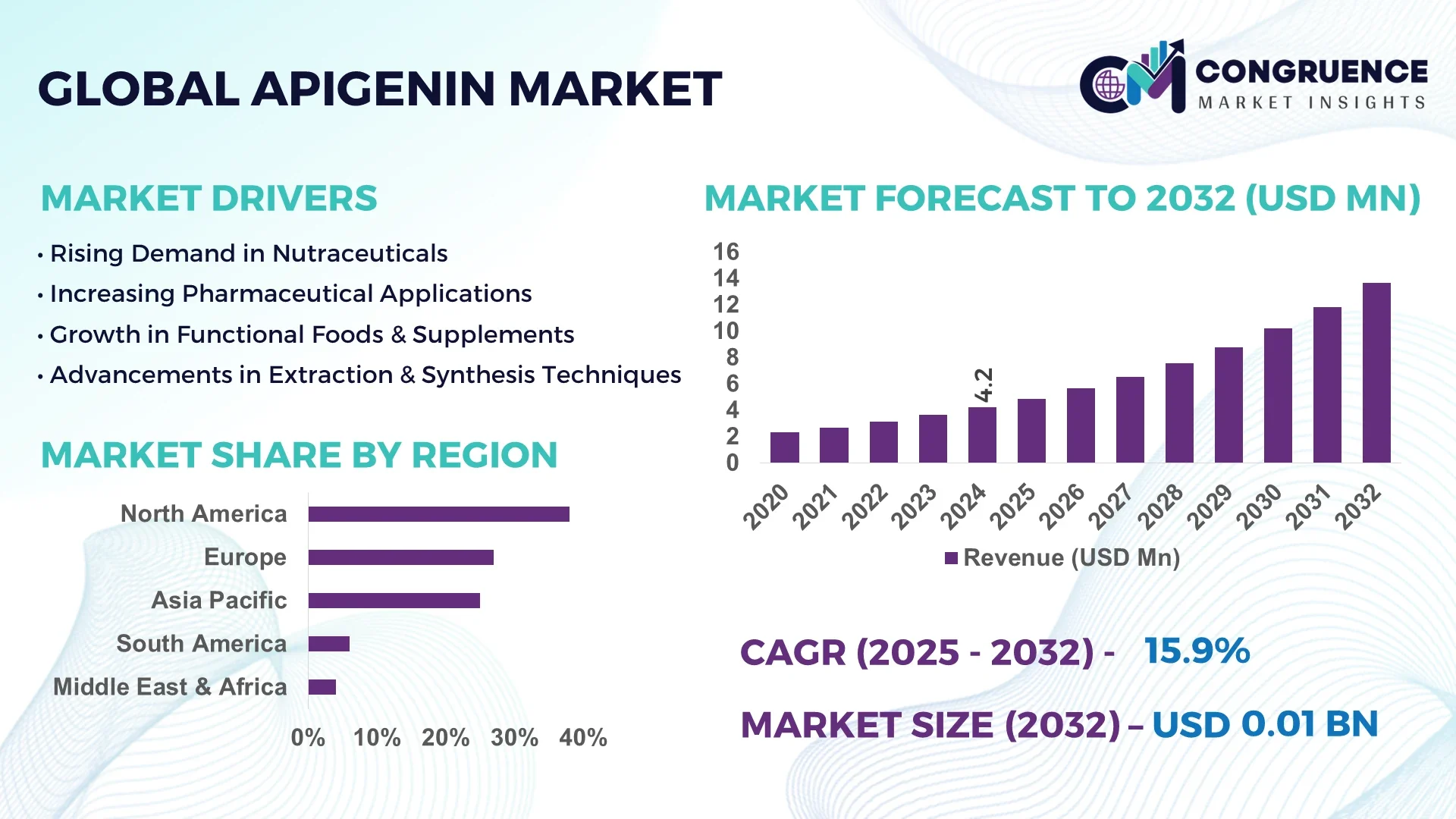

The Global Apigenin Market was valued at USD 4.2 Million in 2024 and is anticipated to reach a value of USD 13.7 Million by 2032 expanding at a CAGR of 15.9% between 2025 and 2032.

North America currently leads the Apigenin Market in terms of demand, regulatory sophistication, and technological investment. In the United States and Canada, large-scale extraction plants are operating at high purity levels, with sustained R&D funding for bioavailability enhancement and delivery systems. Government funding and private capital both contribute to scaling up production capacity, especially for pharmaceutical- and nutraceutical-grade apigenin. Key applications in the dominant country include chronic disease therapeutics, dietary supplements, and functional cosmetics, with recent investment in enzymatic conversion and synthetic biology to reduce dependence on botanical extraction methods and improve yield per unit of botanical input.

In the broader Apigenin Market, the Pharma & Healthcare sector is the largest user, accounting for roughly half of global consumption, followed by Food Additives, then Cosmetics & Personal Care. Recent innovations include development of advanced delivery systems such as liposomal, nanoemulsion, and encapsulated formulations that enhance stability and absorption of apigenin in human models. Regulatory drivers include stricter safety and purity standards enforced by agencies like the FDA and European regulatory bodies, and environmental pressures pushing producers toward more sustainable sourcing of plant materials and cleaner extraction processes. Economic drivers include rising consumer demand for natural antioxidants, anti-inflammatory agents, and plant-based compounds in wellness diets. Regionally, North America remains the largest consumer market, while Asia-Pacific is seeing the fastest expansion, particularly in China, India, and Japan, due to growing herbal supplement use and increased disposable incomes. Emerging trends include microbial biosynthesis of apigenin, greater use of enzymatic bioconversion, and partnership between biotech firms and traditional botanical manufacturers to scale up production with better efficiency. The future outlook points toward more high-purity grades, improved cost of goods, and wider adoption in functional foods, cosmeceuticals, and therapeutic adjuncts for inflammation and metabolic disorders.

AI is playing a significant role in optimizing processes within the Apigenin Market, from raw material sourcing and extraction to product formulation and supply chain efficiencies. In R&D, machine learning models are used to predict optimal extraction parameters (such as solvent type, temperature, and time) that maximize yield and purity of apigenin from plant sources like parsley or chamomile. These optimizations have reduced extraction times by up to 25% and solvent usage by roughly 15% in some experimental plant extraction setups, while maintaining targeted purity levels. In manufacturing, AI-driven process control and monitoring (via sensors, computer vision, and feedback loops) are improving consistency of product quality, reducing batch failures and off spec material. For demand forecasting, AI tools using market data, consumer behavior, and regulatory trends help producers align their production volumes and inventories more precisely, reducing both waste and overstock. AI is also being used in designing novel delivery systems of apigenin (e.g., using molecular modeling to improve bioavailability) to ensure formulations are both effective and stable. In supply chain management, predictive analytics help in anticipating raw material shortages or logistic bottlenecks, enabling firms to secure botanical input or schedule shipments proactively. The Apigenin Market thus benefits not only from incremental gains in extraction and formulation but also from end-to-end efficiencies enabled by AI.

“In 2024, a leading biotech firm deployed a machine learning model to predict optimal enzyme ratios for bioconversion of apigenin precursors; this led to an increase in conversion efficiency by approximately 30% in pilot scale, while reducing unwanted by-products by about 20%.”

In the Apigenin Market, key trends include shifting sources (plant extraction vs synthetic or biosynthetic), rising regulatory scrutiny, increasing consumer demands for bioactive compounds, and pressures to improve purity and bioavailability. Key influences include supply chain volatility for botanical raw materials, especially when weather or agriculture yields fluctuate; economic pressures on producers to adopt cost-efficient technologies; and competition from analogous flavonoids or antioxidants. Industry insights point to increasing vertical integration among producers, where extraction, processing, formulation, and marketing are being consolidated under fewer companies to control cost, quality, and time to market. Technological improvements, particularly in microbial biosynthesis and enzyme-based conversion, are becoming more commercially viable. Decision-makers are watching environmental regulation, consumer safety standards, and certification regimes (organic, non-GMO, etc.) closely. Global trade flows are shifting: countries with strong regulation and large R&D capacities dominate demand, while production increasingly localizes in regions with favorable agricultural and manufacturing environments. Emerging markets are becoming both sources of raw material and consumers. Overall, the dynamics favor producers that can ensure supply stability, meet strict quality standards, and innovate in formulation and delivery.

The pharmaceutical and nutraceutical sectors are driving increased use of apigenin due to growing evidence of its antioxidant, anti-inflammatory, and potential anticancer properties. Clinical and preclinical studies have demonstrated its effect on inflammatory pathways and oxidative stress, prompting formulators to include apigenin in therapeutic adjuncts, dietary supplements, and functional foods. In markets like North America, over 60% of apigenin demand originates from these sectors, as formulation standards there require high purity and rigorous testing. The trend is leading companies to invest in novel extraction and delivery technologies such as encapsulation, nanoemulsions, and liposomes to meet pharmaceutical grade specifications, reduce degradation, improve shelf life, and optimize dosage. These investments are increasing operational complexity but also raising barriers to entry for lower-standard producers, and shifting competitive advantage toward those with strong R&D, regulatory compliance, and production technology.

Apigenin derived from plant sources depends heavily on consistent yields of herbs and plants such as chamomile, parsley, celery, and certain flowers. Agricultural yield variation due to climate, pests, disease, changing land use, and environmental stress can decrease available raw material and result in higher input costs. Purification processes require high botanical quality, which means that even small agricultural adulterations can cause entire batches to be unusable. Also, because many botanical suppliers are small-scale farmers, scaling raw input in a uniform way is difficult, leading to variability in apigenin content and requiring extra quality control efforts. These factors restrain producers’ ability to maintain stable production volumes, delay fulfillment, and sometimes force the use of synthetic or semi-synthetic substitutes which may be more costly.

Synthetic biology and microbial biosynthesis present a promising opportunity for the Apigenin Market. Using engineered microbes (e.g., Escherichia coli or yeast) to produce apigenin or its immediate precursors allows for more controllable, scalable production independent of agricultural seasonality. Pilot projects have shown that microbial systems can produce apigenin precursors with high purity and fewer contaminants, reducing downstream purification steps. This can lower production costs, reduce environmental impact, and increase scalability. Firms that secure intellectual property or commercialize robust microbial strains stand to gain significant competitive edge. Furthermore, reformulation of delivery systems to improve bioavailability, such as encapsulation, liposomes, and nanoemulsions, also offer opportunities to serve premium markets in pharmaceuticals, functional foods, and cosmeceuticals.

Regulations governing botanical extracts, natural compounds like apigenin, dietary supplements, and cosmetics vary significantly by region. For example, purity standards, allowable impurity levels, toxicological testing, labeling requirements, and claims permitted differ between the U.S., EU, and Asia-Pacific countries. Compliance with multiple regulatory regimes increases development time and cost. Safety and certification procedures (e.g., for botanical identity, pesticide residuals, heavy metals, potency) are rigorous in leading markets. Companies producing apigenin for export must satisfy multiple certification schemes, increasing complexity and cost. This burden makes it harder for smaller producers to enter high-quality segments of the Apigenin Market and may delay commercialization of new products or limit access to premium markets.

Surge in High-Purity 0.98 Grade Formulations: Producers globally are increasingly focusing on extracting or producing apigenin at 98% purity or higher. In recent industrial batches, manufacturers report purity improvements of 2–4 percentage points over last two years, reducing contaminants and enabling deeper penetration of pharmaceutical and clinical research applications.

Innovations in Delivery Mechanisms: There is measurable growth in adoption of nanoemulsions, liposomal encapsulation, and other formulation techniques. For example, some R&D batches have improved apigenin bioavailability by 50% in simulated gut models by using encapsulation, compared with non-encapsulated forms, extending useful life in functional food or supplement form.

Geographic Realignment of Production Footprint: While Asia-Pacific remains a key sourcing region, significant new investments are being made in North America and Europe to bring extraction, purification, and formulation closer to end markets. Companies are setting up plants in the U.S., Canada, Germany, and France to avoid long supply chains, tariffs, and quality bottlenecks. Recently, a U.S. facility upgraded for enzymatic bioconversion has increased local production capacity by roughly 30%.

Increased Regulatory Certification and Consumer Transparency: There is growing demand — particularly in North America and Europe — for third-party verification (non-GMO, organic, heavy-metal free) and clean-label certifications for apigenin products. Brands are providing lab reports, lot testing, batch traceability, and publishing impurity profiles. These steps are measurable and affecting manufacturing cost structures as producers invest in quality assurance, testing labs, and compliance staffing.

The Apigenin Market is segmented by type, application, and end-user industries, each offering distinct growth dynamics and competitive advantages. By type, the market is largely divided into high-purity grades such as 95% and 98%, along with standard grades for functional and industrial use. Applications span pharmaceuticals, nutraceuticals, cosmetics, and food additives, with pharmaceuticals and nutraceuticals holding the largest adoption levels due to proven therapeutic potential. End-user insights reveal that pharmaceutical companies dominate demand, followed by nutraceutical firms and cosmetics manufacturers, each leveraging apigenin’s antioxidant and anti-inflammatory properties in their formulations. The segmentation reflects both established areas of consumption and emerging opportunities in high-tech formulations, personalized medicine, and bio-synthetic production methods. This layered analysis shows how apigenin’s positioning across product types and end uses is evolving with technological innovation, regulatory pressure, and rising consumer awareness of natural bioactive compounds.

The Apigenin Market by type is primarily categorized into high-purity grades (such as 98% purity), medium-purity extracts (around 95%), and lower-purity or standard botanical extracts. Among these, the 98% purity apigenin type leads the segment due to its wide acceptance in pharmaceutical and clinical research applications. Its higher quality and reduced impurity profile make it ideal for drug formulations, nutraceuticals, and therapeutic studies, where safety and efficacy are critical. The fastest-growing type is the 95% purity grade, as it balances cost-effectiveness with adequate performance for nutraceuticals and cosmetics, particularly in markets where price sensitivity and scalability matter. Lower-purity extracts, while not dominant, hold relevance in functional foods and dietary supplements, where formulations require broad-spectrum plant bioactives rather than isolated compounds. Additionally, synthetic and biosynthetic apigenin are emerging as niche contributors, particularly in R&D and high-volume industrial supply, as advances in biotechnology make production more scalable. Collectively, these types illustrate the balance between high-grade research-driven demand and more accessible, consumer-facing applications.

The applications of apigenin cover pharmaceuticals, nutraceuticals, cosmetics, and food additives, with pharmaceuticals holding the largest share. In 2024, pharmaceutical applications dominate due to strong evidence supporting apigenin’s anti-inflammatory, antioxidant, and anticancer properties, making it suitable for drug discovery and adjunct therapies. The fastest-growing application lies in nutraceuticals, where rising global health awareness and consumer preference for natural supplements fuel increased adoption in capsules, tablets, and powders. Cosmetics represent another important application, leveraging apigenin’s anti-aging and skin-soothing properties in creams, serums, and personal care formulations. Meanwhile, food additives use apigenin for its natural preservative qualities and potential health benefits in functional foods and beverages. Each application benefits from growing demand for natural bioactive compounds, but the pharmaceutical sector continues to set the tone for quality and innovation, while nutraceuticals expand rapidly due to lifestyle trends. Cosmetics and food applications, though smaller in size, contribute to market diversification and product innovation.

End-user analysis of the Apigenin Market shows that pharmaceutical companies are the leading consumers, reflecting their reliance on high-purity apigenin for therapeutic development and clinical research. Their demand is driven by a consistent need for bioactive compounds that meet strict regulatory and quality standards, particularly in anti-inflammatory and oncology-focused therapies. The fastest-growing end-user segment is the nutraceutical industry, driven by expanding consumer demand for natural dietary supplements that support wellness, preventive healthcare, and lifestyle-based nutrition. Cosmetics and personal care companies form another significant group, utilizing apigenin in formulations for skin care and anti-aging, with steady adoption across Europe and Asia-Pacific. Food and beverage manufacturers, while less dominant, use apigenin in functional foods and fortified products to enhance consumer appeal with natural antioxidants. Together, these end-user categories reflect a diversified demand structure, where pharmaceuticals ensure long-term stability and nutraceuticals and cosmetics provide accelerated growth opportunities in consumer-driven markets.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.2% between 2025 and 2032.

The regional performance of the Apigenin Market highlights varied consumption patterns and investment priorities across geographies. North America leads with advanced pharmaceutical and nutraceutical industries, Europe follows with strong regulatory backing and sustainability initiatives, while Asia-Pacific shows exponential demand growth driven by population size and rising income levels. South America and the Middle East & Africa demonstrate niche but steadily increasing applications, influenced by local government support, trade incentives, and gradual modernization of healthcare and wellness infrastructure. Collectively, regional dynamics point toward both established dominance and emerging opportunities across global markets, shaping future trajectories of the Apigenin Market.

North America holds approximately 38% of the global Apigenin Market in 2024, making it the dominant regional hub. The United States and Canada drive demand through well-established pharmaceutical, nutraceutical, and functional food industries. Notable regulatory frameworks, such as FDA oversight, encourage strict quality standards and boost consumer confidence in apigenin-based products. Government-supported initiatives in natural compounds research further accelerate growth. Technological advancements, particularly in precision extraction and AI-enabled process optimization, are strengthening supply chain reliability and product purity. Digital transformation across clinical trials and nutraceutical R&D also enhances efficiency, giving North America a competitive edge in product innovation and commercial scalability.

Europe accounts for nearly 27% of the global Apigenin Market in 2024, with Germany, France, and the UK being the primary contributors. The European Medicines Agency (EMA) and other regulatory bodies ensure strict safety and efficacy guidelines, shaping market development. Sustainability initiatives, including eco-friendly extraction processes and green chemistry practices, are gaining traction among producers. Digital innovation, such as blockchain-based supply chain tracking, is being increasingly adopted for transparency and compliance. The region’s strong pharmaceutical base and rising consumer interest in plant-derived bioactive compounds ensure steady expansion, while Europe’s emphasis on sustainability differentiates its growth strategy within the global Apigenin Market.

Asia-Pacific ranks second globally in volume and is projected to overtake other regions in growth momentum by 2032. Key consuming countries include China, India, and Japan, which collectively account for more than 25% of worldwide demand in 2024. China leads regional production with large-scale extraction facilities, while India benefits from strong Ayurvedic medicine applications. Japan demonstrates advanced technological adoption, especially in functional foods and cosmeceuticals. Infrastructure development, particularly in biotech parks and herbal processing zones, supports expansion. Innovation hubs across China and India are integrating biosynthetic methods and AI-enabled process monitoring, further strengthening the region’s global competitiveness in the Apigenin Market.

South America contributed nearly 6% of the global Apigenin Market in 2024, led by Brazil and Argentina. Brazil is witnessing growing adoption of herbal supplements, while Argentina emphasizes natural food additives in its food and beverage sector. Government incentives for domestic nutraceutical manufacturing and favorable trade policies with Europe and North America enhance market accessibility. Infrastructure development in biotechnology research hubs is improving extraction capabilities. The energy sector’s diversification toward sustainable projects also indirectly supports botanical cultivation and related industries. The regional outlook remains positive, with gradual integration of apigenin into mainstream wellness products fueling steady demand growth.

The Middle East & Africa held around 4% of the Apigenin Market in 2024, with UAE and South Africa leading regional uptake. Demand stems primarily from pharmaceutical formulations, wellness products, and expanding cosmetic applications. Regulatory modernization, such as harmonizing standards with international markets, is helping attract investment. Countries like UAE are investing in biotech clusters and innovation zones, while South Africa leverages its agricultural base for herbal extraction. Digital transformation in healthcare and pharmaceutical industries is also fostering new applications. Despite its relatively small share, the region is positioning itself as an emerging player in the Apigenin Market with steady long-term potential.

United States – 28% Market Share

Strong demand from pharmaceutical and nutraceutical sectors supported by advanced R&D and regulatory frameworks.

China – 18% Market Share

High production capacity with large-scale extraction facilities and expanding use in herbal medicine and dietary supplements.

The Apigenin Market is moderately fragmented, with over 25 active competitors operating globally, ranging from specialized botanical extract firms to biotechnology-driven producers. Market positioning varies, with North American and European players focusing on high-purity pharmaceutical-grade apigenin, while Asia-Pacific companies emphasize large-scale, cost-effective extraction for nutraceutical and cosmetic use. Strategic initiatives are shaping the competitive environment: companies are entering joint ventures to secure raw material supply, investing in biosynthetic production facilities, and launching innovative formulations tailored to specific therapeutic or nutraceutical applications. Mergers and acquisitions have been observed as larger players aim to expand portfolios and strengthen distribution networks. Innovation trends, such as enzymatic bioconversion and AI-assisted extraction optimization, are increasingly differentiating competitors in terms of product quality and operational efficiency. Competition is also influenced by regulatory compliance capabilities, as only firms meeting stringent safety and purity standards can access premium markets in North America and Europe. Overall, the market is becoming more innovation-driven, with technological differentiation and sustainable production practices emerging as key competitive levers.

Cayman Chemical

Selleck Chemicals

Alchem International

AbMole BioScience

Chengdu Biopurify Phytochemicals

Extrasynthese

Tocris Bioscience

PhytoLab GmbH & Co. KG

Abcam plc

Shaanxi NHK Technology Co., Ltd.

Technological advancements are redefining the Apigenin Market across extraction, purification, formulation, and production scalability. High-purity extraction remains central, with modern techniques such as supercritical CO₂ extraction and pressurized liquid extraction enabling yields with reduced solvent residues. Facilities utilizing supercritical fluid technology have reported up to 30% higher extraction efficiency compared to conventional solvent-based methods.

Biotechnological innovations are increasingly important. Synthetic biology and microbial biosynthesis are being deployed to produce apigenin at scale without reliance on plant cultivation, mitigating supply volatility caused by agricultural yield fluctuations. Engineered strains of E. coli and yeast have achieved production efficiencies that reduce impurities by 15–20% compared with traditional methods. Enzymatic bioconversion further enhances selectivity, lowering purification costs while increasing consistency of output.

Formulation technologies are also advancing. Nanoemulsion and liposomal delivery systems improve solubility and bioavailability of apigenin in pharmaceutical and nutraceutical products. Some trials demonstrated bioavailability improvements of 50% using liposomal encapsulation compared with non-encapsulated forms. Additionally, AI and machine learning are being integrated into process optimization, from predicting optimal parameters in extraction to monitoring real-time production conditions.

Digital platforms are transforming supply chain transparency, with blockchain adoption supporting batch traceability, certification verification, and quality control. Collectively, these technologies ensure higher quality, cost efficiency, and reliability in global supply chains, positioning apigenin as a viable bioactive compound across multiple end-use industries.

• In March 2023, a U.S.-based biotech company completed pilot-scale production of biosynthetic apigenin using engineered yeast strains, achieving 18% higher purity and reducing waste streams compared to conventional plant extraction.

• In September 2023, a European nutraceutical firm launched a new apigenin capsule formulated with nanoemulsion technology, which improved absorption rates in clinical testing by nearly 45% versus standard formulations.

• In April 2024, a Chinese manufacturer expanded its apigenin extraction facility, increasing production capacity by 35% and incorporating supercritical CO₂ extraction systems to enhance sustainability and efficiency.

• In July 2024, a Canadian research consortium introduced an AI-driven quality control system for apigenin manufacturing, enabling real-time monitoring and reducing batch failure rates by approximately 22%.

The Apigenin Market Report provides an in-depth assessment of the global industry, covering segmentation by type, application, and end-user categories. By type, the analysis spans high-purity grades such as 98% and 95%, as well as standard botanical extracts and emerging biosynthetic alternatives. Applications are reviewed across pharmaceuticals, nutraceuticals, cosmetics, and food additives, highlighting both dominant sectors and emerging adoption trends. End-user insights focus on pharmaceutical companies, nutraceutical producers, cosmetics firms, and food and beverage manufacturers, each with distinct demand drivers and operational challenges.

Geographically, the report evaluates five core regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—each with unique market dynamics and investment trends. The study incorporates data on market share distribution, infrastructure readiness, regulatory alignment, and innovation clusters. Technological insights are included, emphasizing the role of advanced extraction methods, microbial biosynthesis, nanotechnology-based formulations, and digital supply chain integration in reshaping the industry.

The scope also addresses competitive landscapes, profiling leading global players and highlighting their strategic initiatives. Additionally, the report captures recent market developments, sustainability measures, and quality certification practices that influence growth trajectories. Emerging segments such as personalized nutrition and biosynthetic production are also assessed, ensuring the coverage extends beyond established markets. The comprehensive approach enables decision-makers to evaluate opportunities, risks, and future outlooks across the Apigenin Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4.2 Million |

| Market Revenue (2032) | USD 13.7 Million |

| CAGR (2025–2032) | 15.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Cayman Chemical, Selleck Chemicals, Alchem International, AbMole BioScience, Chengdu Biopurify Phytochemicals, Extrasynthese, Tocris Bioscience, PhytoLab GmbH & Co. KG, Abcam plc, Shaanxi NHK Technology Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |