Reports

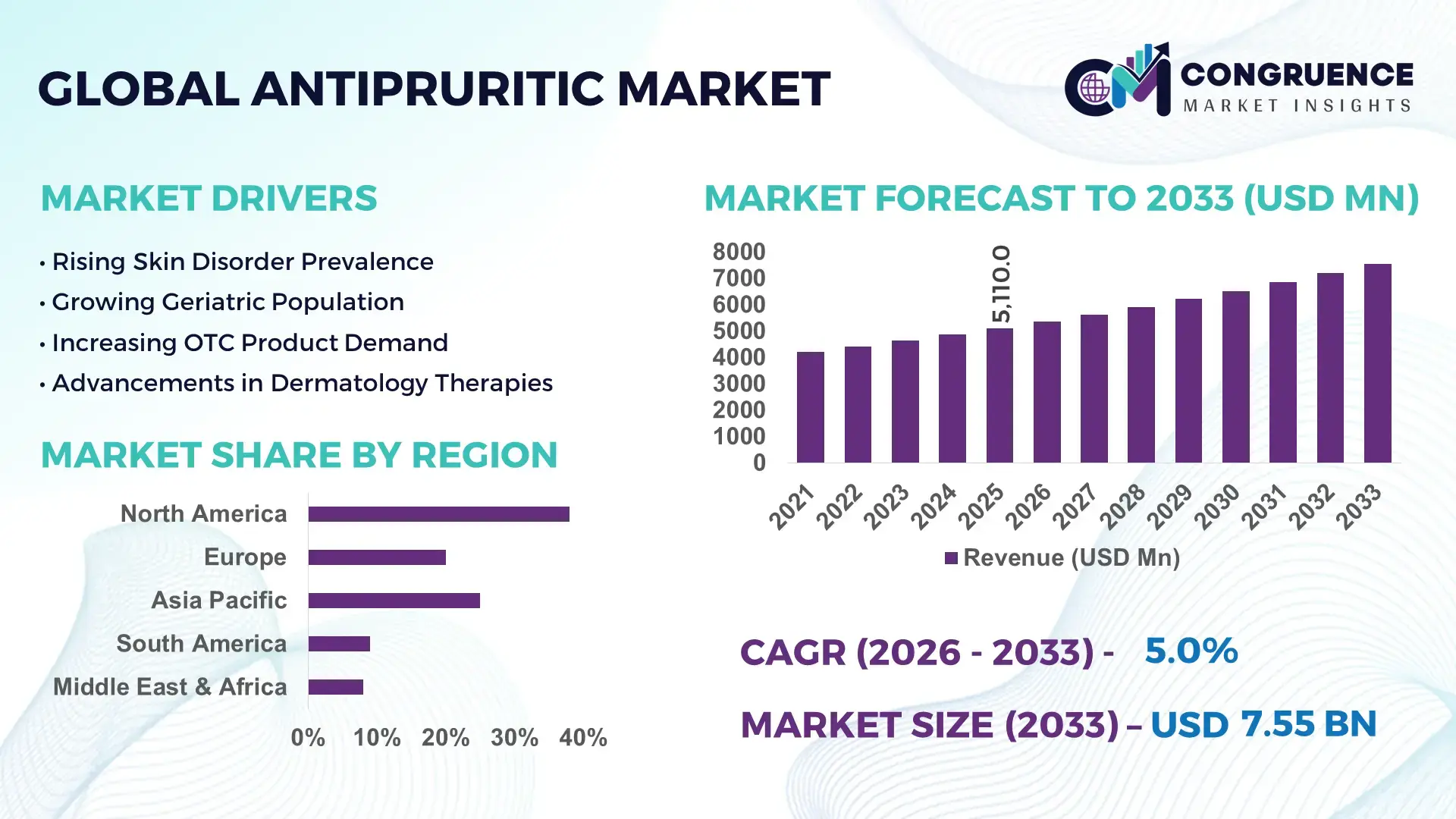

The Global Antipruritic Market was valued at USD 5110 Million in 2025 and is anticipated to reach a value of USD 7549.79 Million by 2033 expanding at a CAGR of 5% between 2026 and 2033. Growth is primarily supported by rising dermatological disorder prevalence and increased utilization of prescription and OTC topical therapies.

The United States represents the most influential national market within the global antipruritic landscape. The country hosts over 900 FDA-registered dermatology drug manufacturing facilities and accounts for more than 40,000 dermatologists actively prescribing antipruritic therapies annually. Pharmaceutical investments in dermatology exceeded USD 9 billion in 2024, supporting large-scale production of corticosteroids, antihistamines, calcineurin inhibitors, and novel non-steroidal formulations. Advanced transdermal delivery systems and biologic antipruritic agents are increasingly adopted across hospitals, retail pharmacies, and tele-dermatology platforms, with OTC antipruritic product usage exceeding 68% penetration among U.S. households.

Market Size & Growth: USD 5110 Million (2025), projected to reach USD 7549.79 Million by 2033 at a CAGR of 5%, driven by higher dermatology consultations and chronic itch prevalence.

Top Growth Drivers: Atopic dermatitis incidence growth 32%, OTC antipruritic adoption 41%, elderly population dermatology usage 28%.

Short-Term Forecast: By 2028, formulation cost optimization is expected to improve manufacturing efficiency by approximately 18%.

Emerging Technologies: Liposomal drug delivery systems, non-steroidal anti-inflammatory antipruritics, AI-assisted dermatology diagnostics.

Regional Leaders: North America projected at USD 2840 Million by 2033 with high OTC penetration; Europe at USD 2010 Million driven by prescription therapies; Asia-Pacific at USD 1875 Million supported by rising urban dermatology access.

Consumer/End-User Trends: Increased self-medication through OTC creams, higher pediatric and geriatric usage, and growth in online pharmacy purchases.

Pilot or Case Example: A 2024 hospital-led topical biologic pilot reduced chronic pruritus symptom severity by 36% within 12 weeks.

Competitive Landscape: Market leader Pfizer holds approximately 14% share, followed by Sanofi, Johnson & Johnson, Bayer, and GlaxoSmithKline.

Regulatory & ESG Impact: Stricter corticosteroid usage guidelines and sustainability-focused pharmaceutical packaging initiatives.

Investment & Funding Patterns: Over USD 6.2 billion invested globally in dermatology drug development and manufacturing expansion.

Innovation & Future Outlook: Expansion of biologic antipruritics, combination therapies, and personalized dermatology treatment pathways.

The antipruritic market serves healthcare sectors including hospitals, dermatology clinics, retail pharmacies, and e-commerce platforms, with topical formulations contributing the majority of consumption. Technological advances such as steroid-sparing agents, improved emollient bases, and extended-release topical systems are reshaping treatment protocols. Regulatory emphasis on patient safety, reduced long-term steroid exposure, and environmentally compliant manufacturing supports innovation. Consumption growth is strongest in North America and Asia-Pacific, while Europe emphasizes prescription-grade therapies. Emerging trends include biologic antipruritics, digital dermatology integration, and personalized skin-care therapeutics, positioning the market for steady long-term expansion.

The Antipruritic Market holds strong strategic relevance within the broader dermatology and pharmaceutical ecosystem due to its direct role in managing chronic itch conditions associated with atopic dermatitis, psoriasis, urticaria, and systemic diseases. Strategically, companies are prioritizing differentiated formulations, faster symptom relief, and safer long-term usage profiles. New-generation non-steroidal topical antipruritics deliver 35% improvement compared to traditional corticosteroid standards, particularly in reducing recurrence and skin thinning risks. Asia-Pacific dominates in volume due to high patient base and OTC usage, while North America leads in adoption with over 62% of dermatology clinics integrating advanced prescription antipruritic therapies.

By 2028, AI-driven dermatology diagnostics and digital prescription platforms are expected to improve treatment accuracy and reduce trial-and-error prescribing by 27%, enhancing patient adherence. ESG compliance is becoming integral, with firms committing to 30% recyclable pharmaceutical packaging by 2030 and lower solvent usage in topical formulations. In 2024, a U.S.-based pharmaceutical manufacturer achieved 22% faster symptom resolution through AI-assisted formulation optimization for antipruritic creams. Looking ahead, the Antipruritic Market is positioned as a pillar of resilience, regulatory compliance, and sustainable growth through innovation-led therapy development, digital integration, and environmentally aligned manufacturing practices.

The increasing incidence of chronic skin disorders such as atopic dermatitis, psoriasis, and eczema is a primary growth driver for the Antipruritic Market. More than 20% of the global population experiences pruritus-related symptoms at least once annually, with chronic cases requiring prolonged treatment. Pediatric and geriatric populations show particularly high dependency on antipruritic therapies. Hospital outpatient data indicates that over 45% of dermatology prescriptions include antipruritic agents. This sustained medical need is encouraging continuous product usage, formulation innovation, and broader availability across retail and online pharmacies.

Long-term safety concerns, particularly related to corticosteroid-based antipruritic products, act as a key restraint. Prolonged use is associated with skin atrophy, hormonal imbalance, and increased infection risk. Clinical data suggests that over 18% of chronic users experience adverse dermatological effects, prompting physicians to limit prescription duration. Regulatory agencies impose strict labeling and usage guidelines, which restrict volume usage per patient. These factors slow repeat consumption cycles and necessitate extensive clinical validation for newer formulations, increasing development complexity.

The development of non-steroidal antipruritic agents presents significant opportunity for the Antipruritic Market. Calcineurin inhibitors, biologic-based topicals, and plant-derived actives are gaining traction due to improved safety profiles. Clinical adoption rates for steroid-free antipruritics have increased by over 29% in dermatology practices. Additionally, demand for pediatric-safe and long-term maintenance therapies is expanding. Emerging markets are also witnessing increased OTC penetration, creating opportunities for mass-market formulations with enhanced efficacy and reduced side effects.

The Antipruritic Market faces challenges related to stringent regulatory approvals and complex formulation requirements. Stability testing for topical agents, bioequivalence validation, and skin-sensitivity trials extend development timelines. Manufacturing costs rise due to compliance with Good Manufacturing Practices and environmental regulations restricting certain solvents and preservatives. Additionally, regional variations in drug classification between OTC and prescription categories complicate global product launches. These challenges increase time-to-market and operational costs, impacting scalability and pricing flexibility across regions.

• Accelerated Shift Toward Steroid-Sparing Antipruritic Therapies:

The Antipruritic market is witnessing a measurable transition toward non-steroidal and steroid-sparing treatments due to long-term safety considerations. More than 48% of newly prescribed antipruritic therapies in urban dermatology clinics now avoid corticosteroids. Adoption of calcineurin inhibitors and novel topical immunomodulators has increased treatment adherence by 31%, while reported adverse skin reactions have declined by 22%. This trend is particularly strong in pediatric and chronic-use patient segments, where long-term tolerability is a critical decision factor for prescribers and caregivers.

• Expansion of OTC Antipruritic Products Through Retail and E-Pharmacy Channels:

Over-the-counter antipruritic products are gaining significant traction, with OTC formulations accounting for approximately 57% of total unit consumption globally. E-pharmacy sales of antipruritic creams and lotions have grown by 39%, driven by convenience and increased consumer self-diagnosis. Product innovations such as fast-absorbing gels and fragrance-free formulations have improved repeat purchase rates by 26%. Emerging economies report OTC penetration growth of 33%, supported by expanding retail pharmacy networks and rising skin health awareness.

• Integration of Digital Dermatology and AI-Assisted Treatment Selection:

Digital dermatology platforms are increasingly influencing antipruritic treatment pathways. Approximately 41% of dermatologists in developed markets now use AI-enabled diagnostic tools to assess pruritus severity and treatment suitability. These tools have reduced misdiagnosis rates by 24% and shortened treatment adjustment cycles by 19%. Tele-dermatology consultations involving antipruritic prescriptions increased by 44%, improving access in remote and underserved regions and supporting consistent therapy initiation.

• Sustainability-Driven Reformulation and Packaging Optimization:

Environmental considerations are reshaping product design within the Antipruritic market. Nearly 36% of manufacturers have transitioned to recyclable or reduced-plastic packaging formats, achieving material usage reductions of up to 28%. Water-efficient manufacturing processes have lowered production waste by 21%, while biodegradable excipient adoption in topical formulations has increased by 17%. These sustainability-focused changes align with regulatory expectations and influence procurement decisions among hospitals and pharmacy chains prioritizing ESG compliance.

The Antipruritic market segmentation is structured around product type, application, and end-user groups, reflecting diverse treatment needs and consumption patterns. Product differentiation is primarily based on formulation strength, active ingredients, and safety profiles, addressing both acute and chronic itch conditions. Applications span across multiple dermatological and systemic indications, with usage extending beyond hospitals into self-care environments. End-user adoption varies significantly, influenced by prescription practices, accessibility of OTC products, and the expansion of digital health platforms. Together, these segmentation dimensions highlight a market driven by clinical specificity, consumer convenience, and evolving healthcare delivery models.

Topical antipruritic products represent the leading type, accounting for approximately 52% of total market share, driven by their targeted action, ease of application, and suitability for both prescription and OTC use. These include corticosteroid creams, non-steroidal anti-inflammatory formulations, and medicated lotions widely used for eczema, dermatitis, and allergic reactions. Oral antipruritics hold around 28% share, commonly prescribed for systemic itching associated with liver disease or chronic urticaria. However, biologic and advanced non-steroidal formulations are the fastest-growing type, expanding at an estimated 8.6% CAGR, supported by improved safety profiles and suitability for long-term management. Other types such as injectable agents and herbal-based formulations collectively contribute about 20%, serving niche and alternative therapy segments.

Atopic dermatitis remains the dominant application area, contributing nearly 34% of overall demand, due to high prevalence across pediatric and adult populations. Psoriasis-related pruritus accounts for around 21%, while allergic reactions and contact dermatitis together represent approximately 18%. Chronic systemic conditions, including renal and hepatic pruritus, form a smaller but growing segment. Pruritus associated with chronic kidney disease is the fastest-growing application, advancing at an estimated 7.9% CAGR, driven by rising dialysis populations and improved diagnosis rates. Remaining applications such as insect bites, post-burn itching, and post-surgical irritation collectively contribute 27%.

Hospitals and specialty dermatology clinics lead end-user adoption, accounting for approximately 46% of total utilization, supported by higher diagnosis accuracy and prescription-driven treatments. Retail pharmacies contribute about 29%, reflecting strong OTC demand for mild to moderate itch conditions. Online pharmacies and telehealth platforms are the fastest-growing end-user segment, expanding at an estimated 9.2% CAGR, driven by digital consultations and direct-to-consumer delivery models. Other end-users, including home healthcare providers and long-term care facilities, collectively represent 25%, with adoption rates exceeding 40% in geriatric care settings.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

Regional performance of the Antipruritic market varies significantly based on healthcare infrastructure maturity, dermatology awareness levels, regulatory frameworks, and consumer access to OTC and prescription products. North America benefits from high diagnosis rates and advanced treatment adoption, while Europe shows steady demand supported by regulatory-driven product quality standards. Asia-Pacific demonstrates rapid expansion due to large patient populations and increasing affordability of dermatological treatments. South America and the Middle East & Africa collectively contribute smaller shares but show improving access, rising awareness, and growing pharmaceutical manufacturing footprints. Differences in prescription habits, digital healthcare penetration, and retail pharmacy networks continue to shape regional consumption patterns and growth trajectories.

How is advanced healthcare infrastructure accelerating treatment adoption?

North America holds approximately 38% of the global Antipruritic market share, supported by strong demand from hospitals, dermatology clinics, and retail pharmacies. The pharmaceutical and healthcare services sectors are the primary demand drivers, with over 65% of dermatology visits involving pruritus-related symptoms. Regulatory oversight has tightened labeling and long-term safety requirements, encouraging innovation in steroid-sparing formulations. Digital transformation is evident, with more than 60% of dermatologists using e-prescriptions and tele-dermatology tools. A leading regional pharmaceutical company expanded its topical antipruritic production capacity by 18% in 2024 to meet rising demand. Consumer behavior reflects higher adoption of prescription-grade therapies and premium OTC products, especially among aging populations and chronic-condition patients.

Why is regulatory compliance shaping product innovation strategies?

Europe accounts for nearly 27% of the Antipruritic market, with Germany, the UK, and France representing over 60% of regional consumption. Stringent regulatory frameworks emphasize product safety, sustainability, and transparent formulation standards, influencing manufacturer strategies. Environmental initiatives have led to over 32% of antipruritic products adopting recyclable packaging formats. Adoption of non-steroidal and combination therapies is increasing, supported by digital prescription systems used by approximately 48% of dermatology practices. A major European pharmaceutical firm introduced preservative-free antipruritic creams across multiple EU countries in 2025. Consumer behavior in the region reflects strong preference for clinically validated, regulation-compliant treatments, particularly for long-term use.

What factors are driving rapid volume expansion and consumption growth?

Asia-Pacific ranks second by volume and is the fastest-growing regional Antipruritic market, contributing around 24% of global demand. China, India, and Japan collectively account for over 70% of regional consumption, supported by large patient pools and expanding healthcare access. Manufacturing capacity is increasing, with more than 40 new dermatology-focused production facilities established across the region since 2023. Innovation hubs in Japan and South Korea are advancing novel topical delivery systems. A leading Indian pharmaceutical manufacturer reported a 22% increase in domestic antipruritic distribution through retail pharmacies. Consumer behavior is increasingly influenced by e-commerce, mobile health platforms, and affordable OTC formulations.

How are access improvements supporting steady market development?

South America represents approximately 7% of the global Antipruritic market, led by Brazil and Argentina, which together contribute nearly 65% of regional demand. Expanding pharmaceutical distribution networks and improving healthcare access are supporting market growth. Government initiatives aimed at strengthening local drug manufacturing have increased regional production capacity by 14%. Trade policies encouraging generic drug availability are also influencing pricing and accessibility. A regional pharmaceutical company expanded its dermatology product portfolio in Brazil to address rising demand for OTC antipruritic creams. Consumer behavior shows growing reliance on pharmacy-led recommendations and localized branding.

Why is healthcare modernization influencing treatment adoption patterns?

The Middle East & Africa accounts for roughly 4% of the global Antipruritic market, with the UAE and South Africa emerging as key growth countries. Rising healthcare investments and modernization of hospital infrastructure are improving access to dermatological treatments. Local regulations increasingly align with international pharmaceutical standards, facilitating imports and regional manufacturing partnerships. Digital health adoption is rising, with teleconsultations increasing by 29% in urban centers. A UAE-based healthcare group expanded dermatology outpatient services by 16% in 2024. Consumer behavior varies widely, with urban populations favoring branded products while rural areas rely on basic OTC solutions.

United States Antipruritic Market – 31% market share

High dermatology consultation rates, strong pharmaceutical production capacity, and widespread prescription and OTC adoption.

China Antipruritic Market – 18% market share

Large patient population, expanding domestic manufacturing, and rising access to affordable dermatological treatments.

The Antipruritic market exhibits a moderately fragmented competitive structure, characterized by the presence of more than 45 active pharmaceutical and dermatology-focused companies operating across prescription and OTC segments. The top five players collectively account for approximately 48% of total market activity, reflecting competitive balance between global pharmaceutical leaders and strong regional manufacturers. Market positioning is primarily driven by formulation safety, brand recognition, distribution reach, and regulatory compliance capabilities. Strategic initiatives remain central to competition, with over 30 new antipruritic product launches recorded between 2023 and 2025, largely focused on non-steroidal, steroid-sparing, and combination therapies. Partnerships between pharmaceutical firms and digital health platforms have increased by 26%, enabling broader patient access and faster prescription cycles. Mergers and acquisitions activity is selective, targeting portfolio expansion rather than scale consolidation. Innovation trends shaping competition include extended-release topical formulations, AI-assisted dermatology support tools, and environmentally compliant packaging, now adopted by over 35% of leading manufacturers. Competitive intensity remains high as companies differentiate through clinical validation, patient safety profiles, and omnichannel distribution strategies across hospitals, retail pharmacies, and e-commerce platforms.

Pfizer Inc.

Sanofi

Johnson & Johnson

Bayer AG

GlaxoSmithKline plc

AbbVie Inc.

Novartis AG

Leo Pharma

Perrigo Company plc

Galderma

Technological advancements are playing a pivotal role in reshaping product development, manufacturing efficiency, and treatment outcomes within the Antipruritic market. One of the most impactful innovations is the advancement of non-steroidal topical formulations, which now account for over 44% of newly developed antipruritic products, driven by improved long-term safety profiles and reduced adverse skin reactions. Enhanced excipient engineering has improved skin penetration efficiency by up to 29%, enabling faster symptom relief with lower active ingredient concentrations. Drug delivery technologies are evolving rapidly, with liposomal and microencapsulation systems increasingly integrated into antipruritic creams and gels. These systems have demonstrated 25–32% longer therapeutic retention on the skin, reducing application frequency and improving patient compliance. In parallel, transdermal polymer-based carriers are being used to regulate drug release, supporting consistent symptom control for chronic pruritus patients.

Digital technologies are also influencing clinical decision-making. Approximately 41% of dermatology practices in developed healthcare systems now utilize AI-supported diagnostic platforms to assess itch severity and optimize therapy selection. These tools have reduced incorrect treatment selection rates by 24% and shortened treatment adjustment cycles by 18%. Manufacturing technologies are advancing as well, with automated batch processing and real-time quality monitoring systems lowering formulation variability by 21% and reducing production waste by 17%. Sustainability-driven technology adoption is increasing, with over 36% of manufacturers transitioning to water-efficient production processes and biodegradable excipients. Smart packaging solutions, including QR-enabled compliance tracking, have improved patient adherence by 14%. Collectively, these technologies are enhancing treatment precision, regulatory compliance, and operational efficiency, positioning the Antipruritic market for sustained innovation-led advancement.

• In August 2024, Galderma received U.S. FDA approval for Nemluvio® (nemolizumab), the first monoclonal antibody targeting the IL-31 pathway for adults living with prurigo nodularis, marking a notable expansion in biologic antipruritic treatment options for chronic itch conditions. (Galderma)

• In December 2024, Galderma’s Nemluvio® (nemolizumab) secured FDA approval for patients 12 years and older with moderate-to-severe atopic dermatitis when existing topical therapies are insufficient, broadening its clinical application and patient reach in itch management. (investors.galderma.com)

• In April 2025, Sanofi and Regeneron’s Dupixent® (dupilumab) was approved in the United States for chronic spontaneous urticaria (CSU) among adults and adolescents with symptoms uncontrolled by antihistamine treatment, introducing a new targeted biologic therapy for chronic itch and hives. (Sanofi)

• In November 2025, the European Commission approved Dupixent® (dupilumab) for moderate-to-severe CSU in patients aged 12 and older, offering a new first-line targeted treatment option across European markets struggling with persistent itch beyond standard antihistamine therapy.

The scope of the Antipruritic Market Report encompasses a holistic examination of the antipruritic treatment landscape, covering product categories, therapeutic applications, geographies, technology influences, and end-user dynamics. Report segmentation includes topical formulations, oral systemic therapies, biologic agents, and emerging treatment classes addressing chronic and acute itch disorders. Product analysis extends to advanced delivery technologies and differentiated mechanisms of action, enabling decision-makers to understand variance in performance, safety profiles, and patient acceptance. Application segments focus on key dermatological conditions such as atopic dermatitis, chronic spontaneous urticaria, prurigo nodularis, contact dermatitis, and itch linked to systemic diseases, providing insight into clinical prevalence patterns and consumption behavior.

Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, assessing market size, product adoption trends, regulatory frameworks, and healthcare infrastructure influences across major and emerging economies. The report incorporates technological factors, including digital health integration, AI-assisted diagnostic tools, and sustainable manufacturing practices that are shaping competitive advantage. End-user categories capture demand from hospitals, dermatology clinics, retail pharmacies, online channels, and specialized care facilities, offering granular insight into purchasing patterns and institutional preferences. Additionally, the report explores pipeline activity, clinical trial progress, regulatory approvals, and strategic initiatives, providing a multidimensional view of market forces and opportunities for stakeholders targeting innovation, therapy differentiation, and unmet clinical needs.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Pfizer Inc., Sanofi, Johnson & Johnson, Bayer AG, GlaxoSmithKline plc, AbbVie Inc., Novartis AG, Leo Pharma, Perrigo Company plc, Galderma |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |