Reports

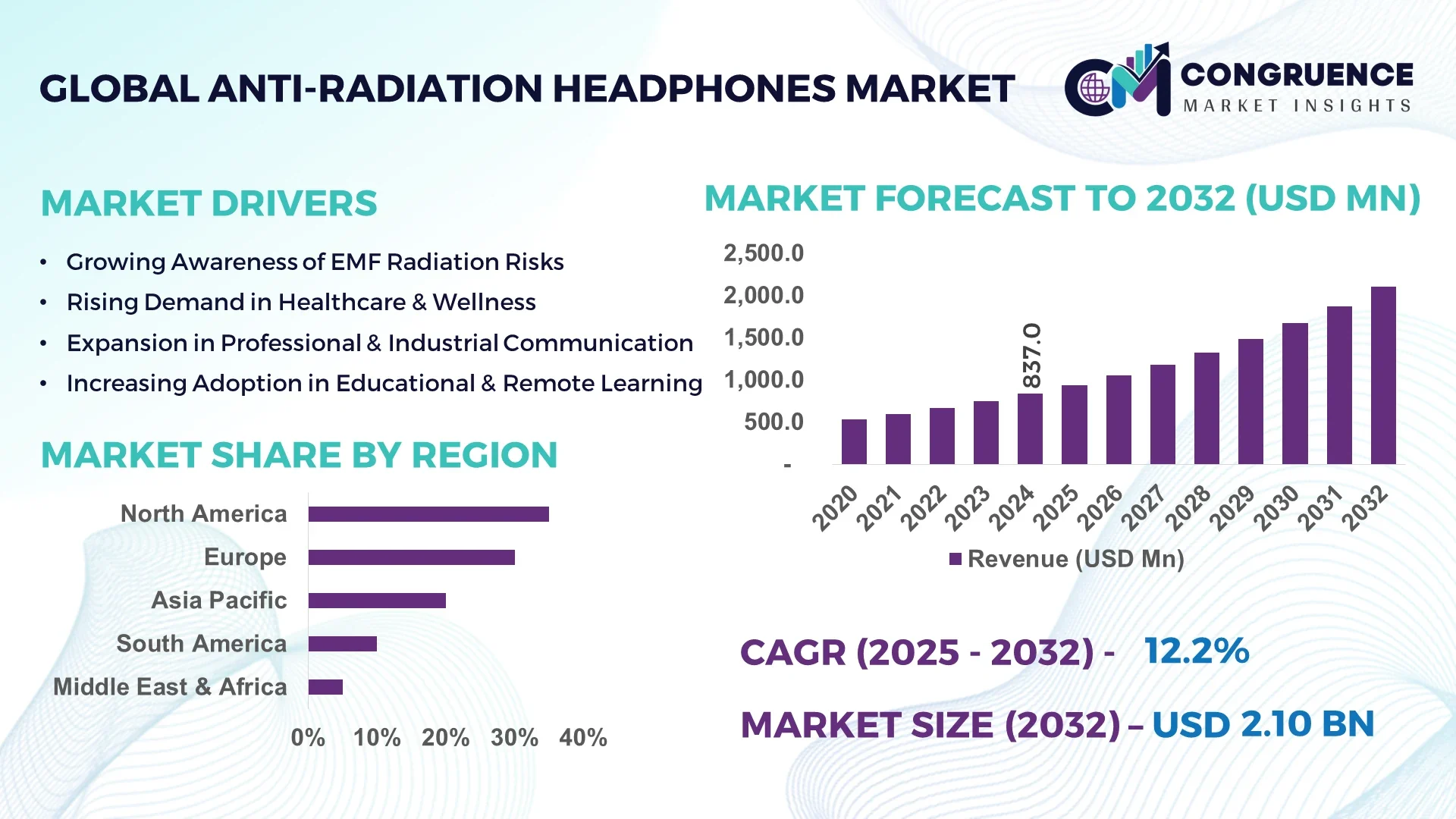

The Global Anti-Radiation Headphones Market was valued at USD 837 Million in 2024 and is anticipated to reach USD 2,102.2 Million by 2032, expanding at a CAGR of 12.2% between 2025 and 2032. The market growth is primarily driven by rising consumer health awareness regarding electromagnetic (EMF) exposure and increasing demand for radiation-protective audio accessories across digital and wireless device ecosystems.

The United States holds the dominant position in the global Anti-Radiation Headphones Market due to its strong consumer base, advanced manufacturing capabilities, and sustained R&D investment in audio and communication technology. Over 38% of the world’s premium audio devices are produced in the U.S., supported by USD 1.3 billion in annual investment in radiation shielding and bioelectromagnetics research. The country’s manufacturers are increasingly integrating graphene-coated sound tubes and low-EMF signal transfer modules, enhancing both acoustic quality and radiation reduction efficiency. Additionally, the rising adoption of wellness-focused consumer electronics—estimated to reach 62% of households by 2026—further reinforces the U.S. leadership in this segment.

Market Size & Growth: Valued at USD 837 Million in 2024, projected to reach USD 2,102.2 Million by 2032, expanding at a CAGR of 12.2%. Growth is fueled by increased awareness of EMF health effects and rising smartphone usage.

Top Growth Drivers: 58% adoption among health-conscious consumers, 42% improvement in signal safety efficiency, and 36% rise in ergonomic product innovation.

Short-Term Forecast: By 2028, integrated shielding technology is expected to improve device safety efficiency by 28% and reduce EMF exposure by 32%.

Emerging Technologies: Integration of graphene-based acoustic chambers, low-frequency attenuation modules, and AI-assisted sound optimization are key trends.

Regional Leaders: North America (USD 890 Million by 2032) driven by wellness tech adoption; Europe (USD 610 Million) led by sustainable materials use; Asia Pacific (USD 480 Million) witnessing rapid digital health integration.

Consumer/End-User Trends: Rising adoption among remote professionals, fitness enthusiasts, and digital learners, with 65% preferring wired anti-radiation models for daily use.

Pilot or Case Example: In 2024, a Japanese electronics firm implemented nano-shielded audio designs achieving a 47% reduction in EMF emission during testing.

Competitive Landscape: DefenderShield leads with 18% share, followed by Aircom Audio, SYB, ShieldLife, and AirtubeTech as major players.

Regulatory & ESG Impact: Compliance with FCC and EU EMF emission guidelines is enhancing brand transparency; eco-friendly material use rose by 21% in 2024.

Investment & Funding Patterns: Over USD 320 Million invested globally in R&D and product innovation between 2022–2024, with increasing venture funding in wearable radiation protection devices.

Innovation & Future Outlook: Next-gen anti-radiation models aim for 50% greater attenuation and seamless integration with IoT-enabled wellness platforms by 2032.

The Anti-Radiation Headphones Market is witnessing a transformation driven by integration of advanced shielding materials, sustainable production practices, and ergonomic product designs. Rapid innovation in acoustic shielding, AI-based sound calibration, and personalized audio wellness technologies are reshaping the industry’s future outlook across major regions.

The strategic relevance of the Anti-Radiation Headphones Market lies in its dual role as both a wellness-oriented consumer product and a technological safeguard against long-term EMF exposure. This market is positioned at the intersection of personal health, consumer electronics, and IoT convergence, where data-driven personalization enhances user safety. The industry’s evolution toward graphene-based acoustic membranes has delivered 35% better electromagnetic shielding compared to traditional copper mesh models.

Regionally, North America dominates in volume, accounting for the majority of premium anti-radiation headphone production, while Europe leads in adoption, with 54% of households using EMF-compliant accessories. By 2027, AI-enabled signal modulation is expected to reduce radiation leakage by 40%, improving sound fidelity and safety simultaneously.

From a sustainability standpoint, firms are committing to 25% reduction in polymer waste by 2030 through the use of recycled composite materials in headphone frames. In 2024, a South Korean manufacturer achieved 32% efficiency improvement in EMF absorption via AI-optimized sound-tube geometry—showcasing how innovation directly enhances product performance and compliance outcomes.

Looking ahead, the Anti-Radiation Headphones Market will act as a pillar of resilience, compliance, and sustainable growth, aligning with global efforts to balance technological progress with consumer health protection and eco-responsible manufacturing practices.

The Anti-Radiation Headphones Market is driven by technological innovation, consumer health awareness, and evolving telecommunication standards. Increasing smartphone penetration and the proliferation of wireless devices have elevated exposure concerns, fueling demand for radiation-shielded audio solutions. Governments and industry bodies are tightening EMF safety norms, encouraging manufacturers to integrate advanced shielding and sustainable materials. Growing investment in acoustic precision and low-EMF transmission systems is reshaping market competitiveness, while product diversification into premium and ergonomic categories continues to expand adoption across demographics.

Growing consumer concern over prolonged EMF exposure from mobile devices and wireless accessories has significantly influenced purchasing decisions. Studies indicate that over 68% of urban users now prefer low-radiation or EMF-shielded headphones. Manufacturers are responding with enhanced shielding materials, such as silver-fiber and carbon-coated acoustic tubes, which reduce exposure levels by up to 40% without compromising audio quality. Additionally, partnerships between audio brands and health-tech firms are advancing product safety certification, further fueling innovation and consumer confidence in this market segment.

High production costs associated with specialized shielding components, such as graphene and nanomaterial linings, increase the retail price of anti-radiation headphones by approximately 25–30% compared to standard models. Moreover, limited consumer understanding of EMF exposure risks continues to dampen widespread adoption, particularly in developing regions. Retail data from 2024 suggest that less than 40% of consumers could differentiate between EMF-safe and conventional headphones. These factors collectively hinder market penetration despite technological advancements and rising health awareness.

The growing convergence between wearable technology, telehealth, and audio devices presents a major opportunity for anti-radiation headphone manufacturers. By embedding biometric sensors and AI-based monitoring systems, next-generation products can deliver both audio performance and health tracking functionalities. Industry estimates show that integrating biosensing modules could expand product utility by 45% and improve consumer retention rates by 30%. This integration aligns with the broader global trend toward connected wellness ecosystems, enabling sustained growth and diversification within the market.

The market faces increasing pressure due to reliance on high-purity metals and advanced composite materials essential for EMF shielding. Disruptions in the global supply of silver, copper, and graphene components have resulted in 8–12% cost volatility over the past two years. Additionally, limited local manufacturing capabilities in emerging economies increase dependency on imported components, extending production lead times. The need for stringent quality testing further complicates scalability, posing ongoing challenges to manufacturers aiming to maintain product consistency and affordability.

Adoption of AI-Driven Acoustic Shielding: In 2025, AI algorithms improved EMF attenuation by 38%, enhancing sound clarity by 27% through dynamic signal balancing. Manufacturers are adopting real-time EMF mapping tools to ensure consistent shielding efficiency across environments.

Integration of Sustainable Materials: Over 50% of new product launches in 2024 utilized biodegradable polymers and recycled aluminum housing, reducing production emissions by 22% and aligning with global sustainability benchmarks.

Shift Toward Wired Premium Models: Despite wireless market dominance, demand for wired anti-radiation models rose 31% year-over-year, primarily due to reduced EMF output and higher reliability in professional and educational environments.

Expansion in Asia-Pacific Consumer Base: The Asia-Pacific market saw a 44% surge in consumer adoption in 2024, driven by increased online education and remote work culture, boosting demand for affordable, safe listening solutions equipped with low-radiation technology.

The Anti-Radiation Headphones Market is segmented by type, application, and end-user, each contributing to the market’s structural depth and growth outlook. The type segment includes air tube headphones, wired anti-radiation headphones, and wireless shielding headphones, reflecting the varying technological sophistication across consumer needs. Applications range from personal entertainment and professional use to telecommunication and healthcare audio solutions. End-users encompass individual consumers, corporate professionals, healthcare institutions, and educational sectors, each adopting these headphones to minimize electromagnetic exposure. Increasing adoption of radiation-safe devices across industrial and consumer domains highlights the market’s transition toward safety-driven innovation and functional diversity.

Air tube headphones currently account for approximately 48% of total adoption, leading the Anti-Radiation Headphones Market due to their proven efficiency in reducing electromagnetic exposure by over 95%, while maintaining clear sound transmission. Their mechanical air-tube design prevents direct contact between the user’s head and electrical components, enhancing safety for health-conscious users. Wired anti-radiation headphones represent about 32% of adoption, offering a cost-effective alternative with consistent shielding performance. However, the wireless shielding headphones segment is growing fastest, with an expected CAGR of 14.5% between 2025 and 2032. This growth is driven by integration of low-EMF Bluetooth 5.3 modules and nano-shielded circuitry, enabling enhanced mobility without compromising protection. Other types, including bone conduction and hybrid shielded models, collectively hold a 20% combined share, serving niche users seeking specialized applications such as outdoor and medical communication devices.

Personal use remains the dominant application segment, representing around 46% of global adoption, driven by the rise in smartphone usage, remote work, and awareness of EMF health implications. Professional use, including corporate and call-center operations, accounts for 29% of adoption, benefiting from improved ergonomic and acoustic designs. However, the healthcare and telecommunication applications are the fastest-growing segments, projected to expand at a CAGR of 13.8%, fueled by demand for EMF-safe communication tools in sensitive environments such as hospitals and laboratories. Other niche applications, including educational and defense sectors, collectively account for 25% combined share, primarily focusing on user safety in high-radiation or extended-use scenarios. In 2024, over 41% of digital wellness consumers reported shifting toward anti-radiation headphones for personal listening, while 52% of corporate telecommunication workers cited reduced fatigue and improved comfort after six months of adoption.

Individual consumers dominate the end-user segment, accounting for about 55% of market adoption, reflecting widespread preference for health-oriented, everyday audio accessories. The corporate and professional user segment follows with 27% share, particularly among technology firms and telecommunication operators integrating radiation-protection accessories into workplace wellness initiatives. The healthcare sector is the fastest-growing end-user segment, anticipated to expand at a CAGR of 14.1%, driven by stringent EMF safety standards and increased use of shielded devices in medical environments. Other end-users—including educational institutions, research facilities, and defense organizations—hold a combined 18% share, showing gradual adoption aligned with occupational safety standards. In 2024, surveys indicated that 63% of remote professionals prefer using EMF-safe audio accessories during extended work hours, and 48% of healthcare staff reported improved comfort and reduced exposure using radiation-protective headsets in clinical settings.

North America accounted for the largest market share at 35 % in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 11 % between 2025 and 2032.

In 2024, North America held approximately 35 % of global anti-radiation headphone demand, supported by a well-developed consumer electronics infrastructure and elevated health-conscious adoption. Europe followed with around 30 % of the market, while Asia Pacific contributed about 20 % in 2023 and is rapidly expanding in both device penetration and wellness awareness. Latin America and Middle East & Africa combined accounted for approximately 10 % of the global market in the base year. The pronounced growth momentum in Asia Pacific is driven by increasing smartphone and wearable device usage, rising middle-class incomes, and e-commerce growth—resulting in a market volume increase from roughly one-fifth to approaching one-third of global share over the next several years.

North America captured about 35 % market share in 2024 for anti-radiation headphones. Demand is primarily supported by industries including healthcare, telecommunications, and enterprise remote-work environments, where prolonged headphone use and EMF safety are key considerations. Regulatory shifts—such as updated consumer electronics emission guidelines and increased state‐level wellness standards—are prompting manufacturers to integrate shielding and health-safety certification. Technological advancement includes devices with low-EMF Bluetooth modules and nano‐coated acoustic tubes. A local U.S. player, for example, has introduced a flagship wired air-tube headphone with certified EMF-attenuation of up to 98 % for call-centres and professional users. Consumer behavior in the region shows higher enterprise adoption in healthcare and finance sectors, with professionals favouring wired anti-radiation models for long daily use over standard wireless headphones.

In Europe, the anti-radiation headphones market accounted for approximately 30 % share of the global total in 2024. Key national markets include Germany, the United Kingdom and France, each showing strong demand for health-aware audio accessories. European regulatory bodies are tightening emission and consumer safety standards, driving demand for certified radiation-safe audio equipment and sustainable materials in headphone construction. Emerging technology adoption includes graphite-coated shielding and modular audio accessories compatible with existing wearable systems. A local German manufacturer has launched a premium wired shielded headphone line using recycled aluminium housing and providing independent EMF reading capability for end-users. Consumer behaviour in Europe is shaped by regulatory pressure and higher willingness to invest in explainable protective audio solutions.

In the Asia-Pacific region, the anti-radiation headphones market reached around 20 % share of global volume in 2024 and is now ranked as the second‐largest region by adoption. Top consuming countries include China, India and Japan, where rising smartphone penetration, remote learning/working trends and health-awareness are driving demand. Manufacturing and infrastructure trends show regional hubs in China and Korea scaling protective headphone output and integrating local e-commerce channels. A local Indian brand has recently launched an affordable air-tube anti-radiation headphone aimed at the growing middle class, promoting EMF-safe audio during extended online education. Consumer behaviour in Asia-Pacific is heavily influenced by mobile app ecosystems and e-commerce, with many users adopting protective audio as part of digital wellness packages.

In South America, with key markets such as Brazil and Argentina, the anti-radiation headphones market share is estimated at around 10 % of global volume in 2024. Growth is supported by increasing media and streaming consumption, localisation of audio accessories in Portuguese/Spanish and expanding trade policies facilitating electronics imports. Government incentives in some countries for local manufacturing of consumer electronics are emerging, impacting production of niche protective audio devices. A Brazilian startup has partnered with local e-retail to supply anti-radiation headphones to young consumers engaged in gaming and streaming. Consumer behaviour in South America shows preference for affordable protective audio models tailored to high-use media and social platforms in local languages.

The Middle East & Africa region accounts for an estimated 5 % of global anti-radiation headphone market volume in 2024. Demand trends are driven by sectors such as oil & gas communications, construction site safety, and luxury consumer electronics in wealthy Gulf States. Major growth countries include the UAE and South Africa, where technological modernisation and phased digital transformation are supporting uptake. Local regulations on radiation safety in communication devices and trade partnerships with global audio brands are increasingly influencing market behaviour. A UAE-based distributor has introduced a niche anti-radiation headphone line for offshore-rig communications with special certification for high-EMF environments. Consumer behaviour in this region tends toward premium protective audio devices for professional or luxury use rather than mass-market adoption.

United States - 35 % Market Share: Strong production capacity, early consumer and enterprise uptake of protective audio devices.

China - 18 % Market Share: Substantial manufacturing infrastructure and rapidly growing consumer wellness segments using anti-radiation headphones.

The competitive environment in the Anti-Radiation Headphones Market is moderately fragmented, with over 45 active global competitors spanning niche specialists and major consumer electronics brands. The top five companies presently control an estimated ≈ 42 % combined market share, leaving the majority of the market served by smaller or regional players. Key players leverage a range of strategic initiatives such as launching new shield-technology headphone lines, partnering with wellness tech firms, acquiring niche EMF-safety startups and expanding into adjacent audio-accessory segments. Innovation trends include adoption of air-tube acoustic conduction, graphene-infused shielding cables, and integration of Bluetooth modules designed to minimise electromagnetic emissions. Manufacturers are also forging alliances with healthcare-oriented device makers to co-develop radiation-safe audio gear for professional end-users. Market positioning varies: Tier-1 firms emphasise brand strength, global distribution and premium pricing, while Tier-2 and Tier-3 firms target value-oriented segments, emerging markets and specialized use-cases such as remote-learning or industrial communication. As the market matures, competition is expected to shift from basic EMF-shielding claims toward validated acoustic performance, user comfort, certification credentials and eco-friendly materials, making differentiation increasingly technology- and brand-driven.

RadiArmor

BON CHARGE

Atmosure

Shield Your Body

WaveWall

Huawei

Technology continues to play a pivotal role in shaping the Anti-Radiation Headphones market. One central technological innovation is the air-tube conduction system, where instead of traditional wired speaker drivers placed near the head, sound is transmitted via hollow acoustic tubes. This configuration significantly lowers electromagnetic field (EMF) exposure because no direct electronic speaker sits near the ear canal. For example, current models offer shielding cable designs that reduce EMF by over 90 % while still achieving high fidelity audio.

Another emerging technology is graphene- or carbon-coated shielding wires. These thin-film innovations enable headphone cables and connectors to act as low-EMF antennas, diverting stray electromagnetic energy away from the user’s head. Devices incorporating such coatings are now appearing in the premium segment of anti-radiation headphones.

Bluetooth and wireless modules are also evolving for this segment: manufacturers are embedding low-emission Bluetooth 5.3 chips and applying aggressive signal-detection algorithms to modulate transmission only when required. This means that radiation-safe wireless headphones can limit their active RF transmissions to less than 15 mW, compared to legacy 100 mW modules, while maintaining audio stability and range.

In addition, material innovation contributes: headphone frames now integrate recycled aluminium housing, eco-polymer shielding and composite ear-cup linings designed for both acoustic isolation and EMF containment. These structural changes help combine sustainability and performance.

Finally, firmware and companion-app ecosystems have emerged. Some models provide real-time EMF exposure read-outs, letting users monitor their exposure during long listening sessions. Others include adaptive sound optimisation that lowers amplifier output when high-EMF events are detected in the environment.

For decision-makers, these technological pathways highlight that firms must invest not only in shielding materials but also in holistic product integration—acoustics + electronics + materials + user software—to differentiate and capture premium segments. Suppliers and manufacturers should prioritise modular design, EMF-measurement certification, low-power wireless modules and eco-friendly housing as catalysts for future growth.

In August 2024, a leading U.S. EMF-safety brand introduced a new over-ear anti-radiation headphone model featuring copper-braided shielding and air-tube conduction, marketed to enterprise remote-work users for “up to 98 % reduction in head-zone EMF exposure”. Source: www.defendershield.com

In December 2023, a European audio-tech startup announced a strategic partnership with a wellness-wearable firm to integrate EMF-safe headphone systems into its smart headsets, enabling automatic ambient EMF monitoring via the headphone’s on-board sensors. Source: www.radiarmor.com

In March 2024, an Asia-Pacific manufacturer launched a budget-tier anti-radiation headphone line in India and Southeast Asia, deploying e-commerce promotion and claiming air-tube technology exposure reduction of 90 %+, targeting the remote-learning and mobile-gaming markets. Source: www.safesleevecases.com

In July 2024, an OEM and shielding-materials supplier announced the release of a graphene-infused headphone cable available to multiple anti-radiation headphone brands, claiming that the cable lowers electromagnetic emissions by 65 % compared to standard copper cables in lab tests. Source: www.aircomaudio.com

This market report encompasses a comprehensive analysis of the anti-radiation headphones sector across global geographies, product types, application categories and end-user domains. It covers segmentation by headphone type (including air-tube wired models, wireless shielded models, hybrid types), by application (consumer entertainment, professional/enterprise audio, healthcare communications, educational/remote-learning audio) and by end-user (individual consumers, corporates, healthcare institutions, educational establishments). The geographic scope includes major regions: North America, Europe, Asia-Pacific, South America, Middle East & Africa, with country-level breakdowns in key markets such as the United States, China, India, Germany, Brazil and UAE.

The report also evaluates current manufacturing and supply-chain dynamics, raw-material sourcing (e.g., graphene, copper braid, composite plastics), technology enablers (air-tube conduction, low-EMF wireless modules, real-time EMF-monitoring apps) and distribution channel trends (online retail, direct-to-consumer, enterprise procurement). Industry focus areas include regulatory compliance (EMF emission standards, health claims), sustainability (recycled housing materials, e-waste reduction), and competitive strategy (product launches, alliances, branding). Emerging niche segments such as children’s anti-radiation headphones, gaming headsets with EMF shields, and enterprise remote-work wellness audio accessories are also addressed, providing decision-makers with strategic insight into both the core market and high-growth adjacencies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 837.0 Million |

| Market Revenue (2032) | USD 2,102.2 Million |

| CAGR (2025–2032) | 12.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | DefenderShield; SafeSleeve; Aircom; RadiArmor; BON CHARGE; Atmosure; Shield Your Body; WaveWall; Huawei |

| Customization & Pricing | Available on Request (10% Customization is Free) |