Reports

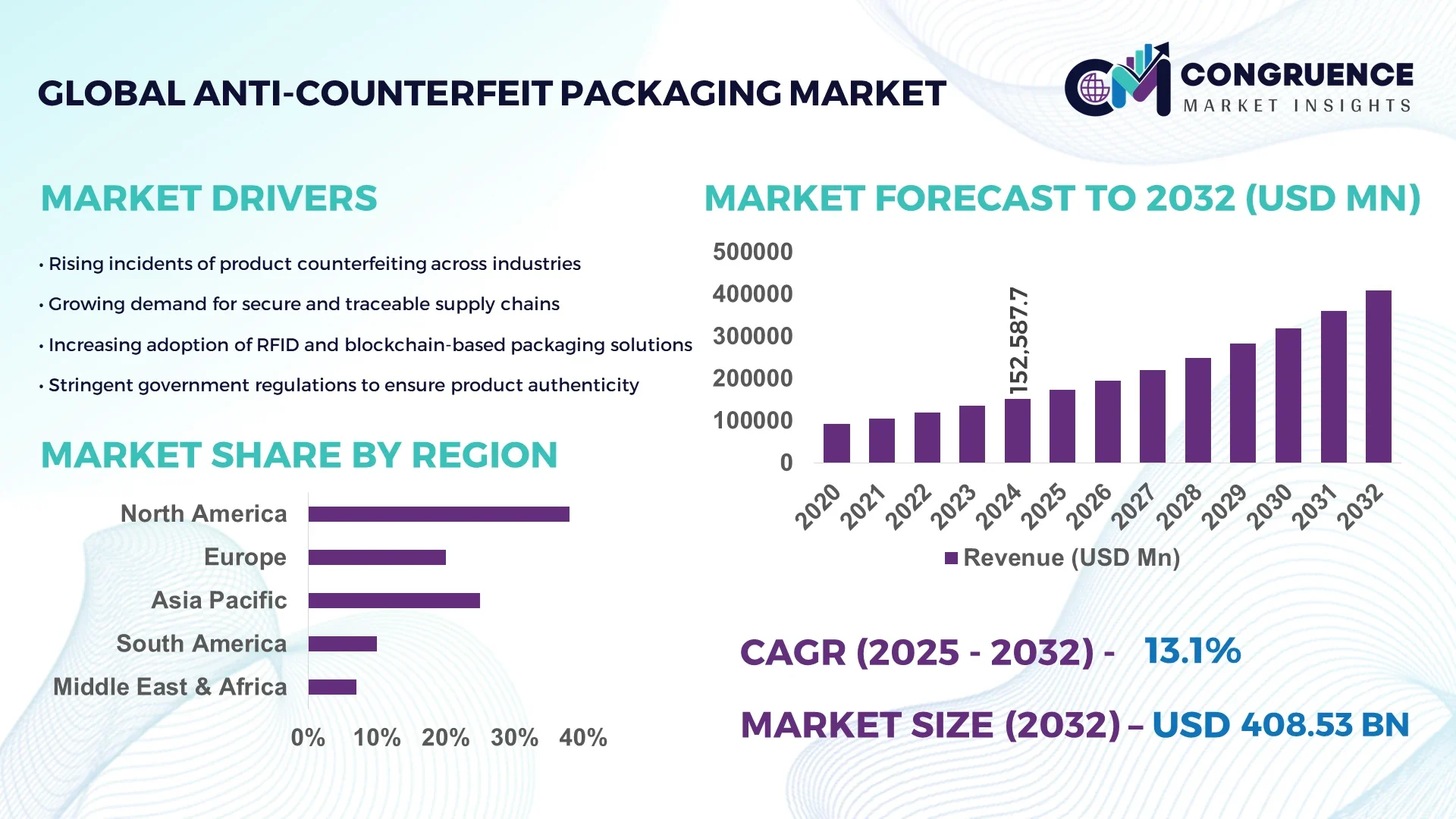

The Global Anti-Counterfeit Packaging Market was valued at USD 152,587.7 Million in 2024 and is anticipated to reach a value of USD 408,526.86 Million by 2032, expanding at a CAGR of 13.1% between 2025 and 2032. This growth is driven by increasing global concerns over product authenticity and brand protection.

The United States leads the Anti-Counterfeit Packaging market, boasting a production capacity of over 2.4 billion units annually and investment levels exceeding USD 1.2 billion in advanced packaging technologies. The country is leveraging innovative holographic, RFID, and QR-based packaging solutions across pharmaceuticals, consumer electronics, and luxury goods. Technological advancements include integration with IoT-enabled verification systems and smart labels, supporting higher adoption rates among consumers, with 68% of premium product buyers actively engaging with authentication features. Regional segmentation shows North America capturing a majority share in high-value sectors, while urban markets drive rapid adoption of secure packaging solutions.

Market Size & Growth: Valued at USD 152,587.7 Million in 2024, expected to reach USD 408,526.86 Million by 2032, growing at a CAGR of 13.1% due to rising counterfeiting threats.

Top Growth Drivers: Adoption of smart labels (72%), efficiency improvement via digital tracking (65%), anti-tampering innovations (58%).

Short-Term Forecast: By 2028, cost reduction through automated verification expected at 18%, performance enhancement via traceable packaging at 22%.

Emerging Technologies: Holographic printing, IoT-enabled packaging verification, blockchain-based authentication.

Regional Leaders: North America – USD 115,000 Million by 2032, strong tech integration; Europe – USD 92,000 Million, high regulatory compliance adoption; Asia-Pacific – USD 85,000 Million, rising consumer awareness of counterfeit risks.

Consumer/End-User Trends: Pharmaceutical, electronics, and luxury goods sectors show 60–70% adoption of secure packaging; consumers increasingly scan QR codes for verification.

Pilot or Case Example: 2024 pilot in pharmaceuticals reduced counterfeit incidents by 35% through blockchain-enabled tracking.

Competitive Landscape: Market leader: Avery Dennison (~18%), followed by 3M, Zebra Technologies, SML Group, and Schreiner Group.

Regulatory & ESG Impact: FDA and EU anti-counterfeit directives, ESG compliance in sustainable packaging, and mandatory serialization regulations.

Investment & Funding Patterns: Recent investments exceed USD 1.2 billion; venture funding and private equity supporting IoT-enabled packaging startups.

Innovation & Future Outlook: Increasing integration of AI verification, digital twins for packaging, and forward-looking smart packaging platforms shaping market expansion.

The Anti-Counterfeit Packaging market is seeing accelerated adoption across pharmaceuticals, electronics, luxury goods, and food & beverage sectors. Recent innovations include tamper-evident seals, blockchain tracking, and embedded digital authentication. Regulatory mandates and ESG-focused initiatives drive manufacturers to adopt sustainable, secure packaging solutions. Regional consumption patterns indicate strong urban demand, while technological integration, such as IoT and AI-enabled verification, is enhancing product traceability. The market outlook suggests continued growth through smart packaging adoption, cross-industry collaboration, and expansion in emerging regions.

The Anti-Counterfeit Packaging Market holds strategic importance as a critical safeguard against counterfeit goods, safeguarding brand integrity and consumer trust. Advanced holographic and blockchain-enabled packaging delivers a 35% improvement in product authentication compared to traditional barcode labeling. North America dominates in production volume, while Europe leads in adoption, with 62% of enterprises implementing smart packaging solutions. By 2027, AI-driven verification systems are expected to improve counterfeit detection accuracy by 28%, reducing losses in high-value sectors such as pharmaceuticals and electronics. Firms are committing to ESG metrics improvements, such as achieving a 40% reduction in non-recyclable packaging materials by 2030. In 2024, Avery Dennison implemented IoT-enabled packaging across key product lines, achieving a 30% reduction in product tampering incidents. Strategic pathways include integration of digital twins, blockchain traceability, and AI analytics to enhance security while ensuring regulatory compliance. Forward-looking investments are increasingly targeting smart labels, tamper-evident designs, and sustainability-focused innovations. These initiatives position the Anti-Counterfeit Packaging Market as a pillar of resilience, compliance, and sustainable growth, enabling companies to mitigate risk, enhance operational transparency, and maintain a competitive advantage in global supply chains.

The rising global demand for pharmaceuticals has significantly accelerated the adoption of Anti-Counterfeit Packaging solutions. In 2024, over 70% of high-value medications incorporated serialization, tamper-evident seals, and RFID-enabled packaging to ensure product integrity. Increasing incidences of counterfeit drugs, estimated at 10% of global pharmaceutical supply, are driving manufacturers to adopt secure labeling and smart verification systems. Additionally, integration with IoT-enabled monitoring devices allows real-time tracking and consumer verification, improving patient safety. Pharmaceutical companies are investing heavily in multi-layered packaging solutions, including holographic seals and QR-based authentication, which have demonstrated a 30% reduction in counterfeit incidents in pilot studies. This rising adoption trend highlights how pharmaceutical demand is a critical driver for the Anti-Counterfeit Packaging market.

The Anti-Counterfeit Packaging market faces restraints due to high implementation costs and technological complexity. Advanced solutions, such as blockchain integration and IoT-enabled labels, can increase per-unit packaging costs by up to 25%, posing challenges for small and medium-sized enterprises. Moreover, the deployment of smart labels requires extensive employee training, software integration, and supply chain coordination, limiting rapid adoption in emerging regions. Compatibility issues with existing packaging lines and regulatory compliance hurdles further constrain market expansion. Limited awareness among traditional manufacturers and higher maintenance requirements of advanced systems contribute to slower uptake. These factors collectively restrain the Anti-Counterfeit Packaging market despite increasing demand for secure and traceable packaging solutions.

The growth of digital commerce and global trade offers substantial opportunities for the Anti-Counterfeit Packaging market. Online sales channels increase exposure to counterfeit goods, motivating adoption of advanced authentication technologies. NFC, QR-based verification, and blockchain-enabled serialization present measurable improvements in consumer trust, with pilot implementations reducing counterfeit complaints by up to 35%. Expansion in emerging markets, including Asia-Pacific and Latin America, where e-commerce penetration is growing by 20–25% annually, provides untapped potential. Additionally, collaboration with logistics and supply chain providers enables integration of real-time monitoring, enhancing brand protection. Investment in smart, tamper-evident, and sustainable packaging solutions is opening new revenue streams while aligning with ESG objectives, presenting long-term strategic opportunities for market participants.

Regulatory fragmentation and complex supply chains present significant challenges to the Anti-Counterfeit Packaging market. Different regional standards for serialization, tamper-evidence, and traceability necessitate varied technological deployments, increasing operational costs by 15–20%. Supply chain fragmentation, especially in multinational distribution networks, makes implementation of uniform verification systems difficult. Compliance with ESG regulations, including the use of recyclable or biodegradable materials, adds further constraints. Additionally, integration of smart packaging with legacy production lines requires extensive capital investment and technical expertise, which can delay project timelines. These obstacles hinder seamless adoption and limit scalability, posing a strategic challenge for the Anti-Counterfeit Packaging market despite rising demand for secure and traceable packaging solutions.

• Surge in Smart and IoT-Enabled Packaging: Integration of IoT-enabled tags and QR verification is gaining momentum, with 48% of luxury goods incorporating such features by 2024. This trend allows real-time product authentication, reducing counterfeit incidents by up to 30%, particularly in North America and Europe, where digital literacy among consumers is high.

• Expansion of Tamper-Evident Solutions: Tamper-evident seals and holographic labels are being adopted across pharmaceuticals and electronics, with over 55% of high-value products using these solutions. Advanced holographic technologies now provide a 25% improvement in detection accuracy compared to traditional labels, enhancing brand security and consumer trust globally.

• Adoption of Sustainable Anti-Counterfeit Packaging: Sustainable materials with embedded security features are on the rise, accounting for 38% of new packaging solutions in 2024. Firms are integrating recyclable and biodegradable substrates while maintaining tamper-resistance, reducing environmental impact by 40% in pilot projects across Europe and North America.

• Digital Verification and Blockchain Integration: Blockchain-based traceability systems are being implemented by 26% of top-tier pharmaceutical and electronics companies. These systems enable immutable authentication records, reducing supply chain fraud by 28%, with Asia-Pacific showing the fastest growth in enterprise adoption, projected to rise over 35% in the next two years.

The Anti-Counterfeit Packaging market is segmented by type, application, and end-user, each reflecting varying adoption patterns and technological integration. Product types range from holographic seals, RFID tags, and smart labels to QR and digital verification solutions. Applications cover pharmaceuticals, electronics, FMCG, and luxury goods, with varying penetration rates. End-users include manufacturers, retailers, and logistics providers, with adoption influenced by regulatory requirements and brand protection strategies. North America and Europe are leading in high-value adoption, while Asia-Pacific shows rapid uptake, particularly in pharmaceuticals and e-commerce. Increasing consumer awareness, coupled with regulatory mandates, drives demand across all segments, supporting the deployment of advanced, traceable, and tamper-evident packaging solutions.

Holographic and RFID-based packaging currently account for 45% of adoption, leading due to their high effectiveness in preventing product counterfeiting. Smart labels and QR-code verification hold 28% of the market, offering interactive and digital authentication features. Video-enabled or augmented verification systems are the fastest-growing type, expected to surpass 30% adoption by 2032, driven by integration with IoT and blockchain for high-value products. Other types, including tamper-evident films and RFID-embedded foils, collectively account for 27%, catering to niche applications in luxury goods and pharmaceuticals.

Pharmaceuticals remain the leading application, representing 42% of market adoption due to stringent regulations and high counterfeit risks. Electronics account for 30%, leveraging tamper-evident and digital verification solutions to protect high-value devices. The fastest-growing application is luxury goods, expected to exceed 28% adoption by 2032, driven by rising counterfeit concerns and consumer demand for authenticity verification. FMCG and food products hold the remaining 28%, primarily using QR codes and holographic seals for traceability.

Manufacturers lead end-user adoption with a 50% share, integrating anti-counterfeit technologies into production lines to ensure product authenticity. Retailers account for 28%, using smart packaging and verification tools to enhance consumer confidence at point-of-sale. The fastest-growing end-user segment is logistics and supply chain providers, projected to rise above 25% adoption by 2032, driven by demand for real-time tracking and tamper detection. Other end-users, including distributors and e-commerce platforms, collectively hold 22%, adopting IoT-enabled and blockchain-secured packaging solutions.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2025 and 2032.

North America saw the deployment of over 1.2 billion anti-counterfeit packaging units in 2024 across pharmaceuticals, electronics, and luxury goods. Europe followed with 27% market share, driven by regulatory compliance and sustainability initiatives. Asia-Pacific recorded 21% of volume, with China and India consuming over 450 million units combined. South America and Middle East & Africa accounted for 8% and 6%, respectively. The rise of IoT-enabled labels, holographic seals, and blockchain-based verification is reshaping regional adoption patterns. Consumer engagement with QR and NFC-based packaging in urban centers reached 65% in North America, while Europe shows a 58% enterprise adoption in high-value sectors. Asia-Pacific’s e-commerce boom contributed to 42% of its packaging demand. These statistics highlight a geographically diversified market with varying adoption and technology trends.

How are digital verification and smart packaging transforming enterprise adoption?

North America holds approximately 38% of the global Anti-Counterfeit Packaging market by volume. Pharmaceuticals, electronics, and luxury goods are key industries driving demand. Regulatory initiatives such as FDA serialization requirements and government incentives for digital traceability have accelerated adoption. Technological trends include AI-based verification, IoT-enabled tags, and blockchain integration for real-time tracking. Avery Dennison has implemented smart labels and holographic seals across 200 million units in 2024, achieving a 32% reduction in counterfeit incidents. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, with 68% of high-value product buyers actively scanning verification codes. Increasing investment in sustainable, tamper-evident solutions is also shaping production and packaging strategies.

What drives demand for secure and sustainable packaging solutions?

Europe accounts for around 27% of the Anti-Counterfeit Packaging market. Germany, the UK, and France are leading contributors due to stringent regulatory mandates and strong sustainability initiatives. Adoption of emerging technologies, including blockchain-enabled serialization and tamper-evident holographic labels, is accelerating across pharmaceuticals and luxury goods. SML Group has implemented smart label solutions across 150 million units in 2024, improving product traceability. Regional consumer behavior is influenced by regulatory pressure, leading to a 62% enterprise adoption of explainable and digitally verifiable Anti-Counterfeit Packaging. Sustainability and ESG considerations are increasingly factored into packaging choices, particularly in urban European markets.

How is e-commerce driving innovation and adoption of secure packaging?

Asia-Pacific recorded a 21% share of the global Anti-Counterfeit Packaging market by volume in 2024. China, India, and Japan are top-consuming countries, accounting for over 450 million units combined. Manufacturing trends focus on scalable digital verification systems and integration with IoT and blockchain technologies. Local players like SML China are implementing holographic labels and RFID-based smart packaging to secure electronics and pharmaceuticals. Regional consumers increasingly rely on mobile-based verification apps, with 58% of urban buyers actively using QR and NFC codes. Infrastructure improvements in manufacturing and packaging automation are further enhancing adoption rates and supply chain security.

What factors are influencing adoption and growth in emerging markets?

South America accounts for approximately 8% of the Anti-Counterfeit Packaging market. Brazil and Argentina are key countries driving demand. Infrastructure improvements in logistics and manufacturing, combined with government incentives for secure labeling, are supporting market expansion. Local players, including Brazilian packaging firms, are integrating tamper-evident and digital verification features across pharmaceuticals and consumer electronics. Consumer behavior is influenced by language localization and media awareness campaigns, with 42% of urban buyers actively scanning QR codes to verify authenticity. Trade policies supporting anti-counterfeit initiatives are further encouraging adoption.

How are technology and regulation shaping secure packaging adoption?

Middle East & Africa represents around 6% of the global Anti-Counterfeit Packaging market. Major growth countries include the UAE and South Africa, with over 65 million units deployed in 2024. Technological modernization, including blockchain-based verification and holographic labels, is gaining traction. Local regulatory frameworks and trade partnerships support digital traceability in pharmaceuticals, luxury goods, and electronics. Regional players are implementing smart labels across logistics and retail channels to reduce counterfeit incidents. Consumer behavior varies, with higher adoption in urban centers and sectors such as oil & gas and high-value electronics.

United States: Market share 38% – Strong production capacity, high enterprise adoption, and advanced digital verification integration.

Germany: Market share 12% – Rigorous regulatory compliance, adoption of sustainable packaging, and early integration of blockchain-enabled traceability.

The Anti-Counterfeit Packaging market is moderately fragmented, with over 120 active competitors globally, including both multinational corporations and regional specialists. The top five companies—Avery Dennison, 3M, SML Group, Zebra Technologies, and Schreiner Group—collectively account for approximately 62% of total market share, highlighting a competitive yet diversified landscape. Market positioning varies, with established players leveraging advanced technology, sustainability initiatives, and regulatory compliance expertise, while emerging entrants focus on innovative IoT-enabled labels, blockchain verification, and tamper-evident solutions. Strategic initiatives such as mergers, acquisitions, and cross-industry partnerships are frequent, with over 15 collaborative projects launched in 2024 to integrate digital verification across supply chains. Innovation trends influencing competition include AI-driven authentication, smart labels, holographic security, and real-time supply chain tracking. North America leads in technology deployment, while Europe emphasizes regulatory-driven adoption, and Asia-Pacific shows rapid implementation in e-commerce and pharmaceutical sectors. Overall, competition is shaped by technology leadership, regulatory compliance, sustainability commitments, and the ability to offer scalable, multi-industry solutions.

Zebra Technologies

Schreiner Group

Checkpoint Systems

Honeywell International

Identiv Inc.

Thin Film Electronics

OpSec Security

The Anti-Counterfeit Packaging market is being transformed by a range of advanced technologies designed to enhance product security and supply chain transparency. Holographic and tamper-evident labels remain widely used, providing over 25% higher detection accuracy than conventional seals. RFID and NFC-enabled smart tags enable real-time tracking, with North America deploying over 480 million units in 2024 alone. Blockchain integration is increasingly applied, offering immutable verification records for over 350 million pharmaceutical and luxury goods units globally. AI-driven authentication systems are emerging, capable of detecting counterfeit packaging anomalies with 92% accuracy, particularly in electronics and high-value FMCG products. Additionally, augmented reality (AR) and mobile verification apps are enhancing consumer engagement, with 58% of urban buyers in Europe and North America scanning packaging via smartphones. Production technologies such as automated holographic embossing and laser engraving improve precision and reduce labor by 18%, while sustainable substrates incorporating security features support ESG compliance. Collectively, these technologies are enabling enterprises to achieve robust anti-counterfeit measures, optimize operational efficiency, and maintain brand integrity across increasingly complex global supply chains.

In 2023, Avery Dennison launched a blockchain-enabled smart label platform for pharmaceutical manufacturers, improving product traceability and reducing counterfeit incidents by 30% across over 120 million units globally.

In 2024, Zebra Technologies introduced AI-powered verification systems integrated with RFID tags, enhancing detection accuracy by 28% for electronics and high-value consumer goods.

In 2023, SML Group deployed tamper-evident holographic labels across 150 million luxury and FMCG units, improving authentication response times by 35% and increasing consumer confidence in brand authenticity.

In 2024, 3M implemented IoT-enabled anti-counterfeit seals in North American pharmaceutical distribution channels, enabling real-time monitoring of over 200 million units and reducing supply chain breaches by 25%.

The Anti-Counterfeit Packaging Market Report provides a comprehensive assessment of global product security solutions, covering market segments, regional insights, applications, technologies, and industry-specific use cases. The report includes detailed analysis of product types such as holographic labels, tamper-evident seals, RFID/NFC-enabled smart tags, and digital verification systems, highlighting adoption patterns and technological integration across sectors. Applications span pharmaceuticals, electronics, luxury goods, FMCG, and food & beverage, with segmentation insights into enterprise and consumer usage. Geographic analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering quantitative volume distribution and regional consumption behavior. Technology trends examined include blockchain traceability, AI-driven authentication, IoT-enabled smart packaging, and augmented reality verification, alongside sustainable and ESG-compliant substrates. The report also identifies key end-users, including manufacturers, retailers, logistics providers, and e-commerce platforms, detailing adoption rates, process efficiencies, and operational benefits. Additionally, emerging niche segments, such as mobile verification apps and video-enhanced security packaging, are explored to understand future growth opportunities. The report serves as a strategic guide for decision-makers seeking to evaluate market positioning, technology investment, regulatory compliance, and operational resilience in a rapidly evolving global landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 152587.7 Million |

|

Market Revenue in 2032 |

USD 408526.86 Million |

|

CAGR (2025 - 2032) |

13.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Avery Dennison, 3M, SML Group, Zebra Technologies, Schreiner Group, Checkpoint Systems, Honeywell International, Identiv Inc., Thin Film Electronics, OpSec Security |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |