Reports

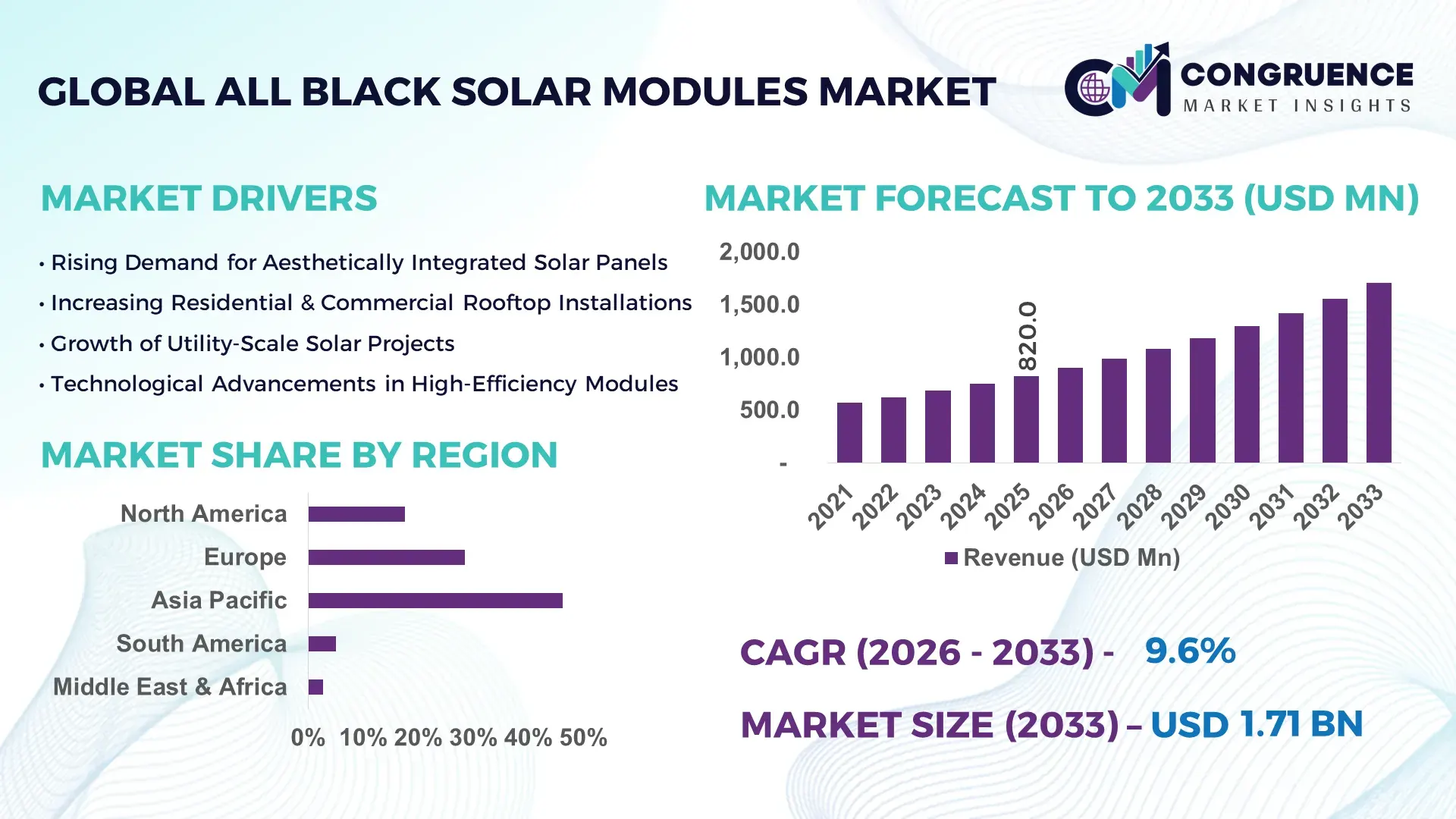

The Global All Black Solar Modules Market was valued at USD 820.0 Million in 2025 and is anticipated to reach a value of USD 1,707.3 Million by 2033 expanding at a CAGR of 9.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising residential rooftop solar adoption, premium aesthetics demand, and continuous efficiency improvements in mono-crystalline photovoltaic technologies.

China dominates the All Black Solar Modules Market in terms of production capacity, technology deployment, and industrial scale. In 2024, China accounted for over 80% of global solar module manufacturing output, with an annual installed production capacity exceeding 650 GW. Major Chinese manufacturers operate gigafactories producing high-efficiency mono PERC, TOPCon, and HJT all-black modules with power ratings above 430 W. Investments in solar manufacturing infrastructure surpassed USD 120 billion between 2020 and 2024. All-black modules are increasingly deployed in premium residential projects and urban commercial rooftops, representing nearly 28% of China’s rooftop PV installations. Advanced automation, AI-driven defect detection, and bifacial black-frame innovations are accelerating domestic production quality and yield rates beyond 98%.

Market Size & Growth: USD 820.0 Million in 2025, projected to reach USD 1,707.3 Million by 2033 at a CAGR of 9.6%; driven by premium rooftop solar adoption and efficiency gains.

Top Growth Drivers: Residential rooftop adoption +34%, mono-crystalline efficiency improvement +18%, urban building solar integration +26%.

Short-Term Forecast: By 2028, module production costs are expected to decline by 21% through automation and material optimization.

Emerging Technologies: TOPCon black-cell modules, HJT full-black panels, AI-assisted manufacturing quality control.

Regional Leaders: Asia Pacific USD 720 Million by 2033 with rooftop densification trend; Europe USD 520 Million by 2033 with net-zero building codes; North America USD 430 Million by 2033 with premium home solar uptake.

Consumer/End-User Trends: Residential rooftops account for 48% of demand, commercial rooftops 37%, architectural BIPV 15%.

Pilot or Case Example: In 2024, a 50 MW residential rooftop program in Japan achieved a 14% efficiency gain using all-black modules.

Competitive Landscape: LONGi ~18% share, followed by JinkoSolar, Trina Solar, JA Solar, and Canadian Solar.

Regulatory & ESG Impact: Urban solar mandates and green building certifications boosting rooftop PV adoption by 22%.

Investment & Funding Patterns: Over USD 9.4 Billion invested globally in premium solar manufacturing between 2022–2025.

Innovation & Future Outlook: AI-optimized cells, ultra-black coatings, and lightweight composite frames shaping next-gen modules.

The All Black Solar Modules Market is led by residential rooftops contributing 48% of total demand, followed by commercial rooftops at 37% and architectural BIPV systems at 15%. Recent innovations include TOPCon black-cell designs with 24.5% efficiency and ultra-low reflectivity glass reducing glare by 38%. Urban net-zero regulations, electricity price inflation, and green building certifications are driving regional demand. Asia Pacific leads consumption, while Europe shows the fastest urban adoption growth. Future outlook remains strong with lightweight frameless modules and AI-controlled production lines.

The All Black Solar Modules Market holds growing strategic relevance as governments, developers, and homeowners prioritize both renewable energy generation and architectural aesthetics. Premium rooftop solar installations are rising across dense urban regions where visual integration into building façades is critical. TOPCon black-cell technology delivers a 12% efficiency improvement compared to traditional mono-PERC standards. Asia Pacific dominates in volume, while Europe leads in adoption with 42% of new residential solar users choosing all-black panels.

By 2028, AI-driven manufacturing automation is expected to cut module defect rates by 35% and improve yield efficiency by 18%. Firms are committing to ESG improvements such as 40% reductions in manufacturing water usage and 30% recycled aluminum frames by 2030. In 2024, Japan achieved a 16% rooftop generation improvement through large-scale deployment of all-black TOPCon modules.

Strategically, manufacturers are investing in ultra-black coatings, frameless designs, and smart inverters to improve system-level efficiency. Building-integrated photovoltaics using all-black modules are forecast to expand into premium office parks and residential complexes. The All Black Solar Modules Market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling net-zero construction and long-term urban decarbonization strategies.

The All Black Solar Modules Market is shaped by premium rooftop solar adoption, rapid PV efficiency improvements, and rising urban building energy mandates. Demand is shifting toward visually integrated solar solutions across residential, hospitality, and commercial properties. Mono-crystalline black-cell technologies are replacing conventional blue modules in urban environments. Automation, AI-based defect inspection, and advanced coating technologies are improving module yields and reducing production losses. Government rooftop solar incentives, net-metering policies, and green building certifications are strengthening demand across Asia Pacific, Europe, and North America. Meanwhile, increasing electricity tariffs and urban grid congestion are encouraging decentralized rooftop solar generation.

Urban rooftop solar installations increased by 29% globally between 2021 and 2024. Over 46% of new residential solar adopters now prefer all-black panels due to improved aesthetics and higher efficiency. Mono-crystalline efficiency rose from 20.3% to 24.5% within five years. Rooftop solar programs in Germany, Japan, and South Korea expanded by over 32%. These trends are pushing demand for high-efficiency premium panels across dense metropolitan zones.

All-black modules cost 14–22% more to manufacture than standard blue modules due to specialized coatings, black frames, and premium glass. Advanced coating processes increase material costs by 18%. Limited supplier availability for ultra-black tempered glass constrains production scalability. These cost barriers restrict adoption in price-sensitive developing markets.

Global BIPV installations expanded by 27% between 2022 and 2024. All-black modules are increasingly used in façades, balconies, and canopies. Premium real-estate developers now integrate rooftop PV into over 34% of new luxury housing projects. Lightweight frameless black modules are creating new urban deployment opportunities.

Polysilicon prices fluctuated by over 41% between 2022 and 2024. Aluminum frame shortages delayed module shipments by 18%. Glass supply disruptions increased lead times by 24%. These factors complicate inventory planning and price stability.

AI-Optimized Manufacturing Expansion: AI-based defect detection systems reduced micro-crack failures by 33% and improved yield rates to 98.4%. Automated production lines now handle 62% of premium module output.

Shift Toward TOPCon and HJT Cells: TOPCon black-cell modules achieved 24.5% efficiency, while HJT designs improved temperature coefficients by 18%. Adoption of these technologies grew by 36% in 2024.

Growth in Premium Residential Solar: Residential rooftop installations using all-black modules increased by 41%. Luxury housing solar penetration reached 38% in Europe and 31% in Japan.

Modular and Prefabricated Construction Integration: Modular construction adoption rose to 55% in new solar-equipped buildings. Prefabricated rooftops reduced installation time by 29% and labor costs by 22%.

The All Black Solar Modules Market is segmented based on type, application, and end-user insights, each reflecting distinct adoption patterns and performance requirements across the solar value chain. By type, segmentation primarily reflects variations in photovoltaic cell technologies, frame configurations, and surface treatments that directly influence efficiency, durability, and visual appeal. Application-wise, demand is shaped by the scale of installations, structural integration requirements, and regulatory frameworks governing urban and industrial energy systems. End-user segmentation highlights diverse procurement behavior, ranging from individual homeowners prioritizing aesthetics to utilities and developers seeking standardized, high-output systems. Across all segments, technological maturity, lifecycle cost optimization, and urban energy transition policies are central factors influencing purchasing decisions. Market participants increasingly tailor product specifications to align with specific building typologies, grid-integration standards, and sustainability certification criteria, making segmentation a critical strategic dimension for manufacturers and system integrators.

The All Black Solar Modules Market by type is primarily categorized into Monocrystalline All Black Modules, TOPCon All Black Modules, HJT All Black Modules, and Other Emerging Variants including bifacial black-frame and frameless black modules. Monocrystalline all black modules currently account for approximately 46% of total adoption, driven by their mature manufacturing ecosystem, stable output performance, and compatibility with residential rooftop systems. TOPCon all black modules hold around 27%, benefiting from higher conversion efficiencies and improved temperature coefficients, making them increasingly attractive for high-density urban installations.

However, HJT all black modules represent the fastest-growing segment, expanding at an estimated 11.4% CAGR, supported by their low degradation rates, bifacial adaptability, and superior performance in low-light conditions. These characteristics are particularly valuable in northern climates and dense city environments.

Other types, including frameless black modules and bifacial black-frame designs, together contribute approximately 27% of the market, serving niche applications such as architectural facades, commercial canopies, and solar carports where design flexibility and mechanical integration are prioritized.

In 2024, a national renewable energy testing agency certified a 24.8% efficiency HJT all-black module for rooftop deployment in cold-climate regions, enabling winter output gains exceeding 14% compared to conventional mono modules.

By application, the All Black Solar Modules Market is segmented into Residential Rooftop Systems, Commercial Rooftop & Façade Systems, Utility-Scale Installations, and Building-Integrated Photovoltaics (BIPV). Residential rooftops dominate with nearly 48% of total installations, driven by rising premium housing developments, consumer preference for visually uniform solar arrays, and increasing adoption of smart home energy systems. Commercial rooftops and façades account for about 29%, reflecting growing corporate sustainability mandates and urban zoning incentives favoring low-profile solar designs.

BIPV represents the fastest-growing application, expanding at approximately 12.1% CAGR, supported by urban net-zero building regulations, architectural integration trends, and the rising use of solar glass and façade-mounted PV systems. Utility-scale projects account for roughly 15%, mainly in projects where visual aesthetics complement public-facing infrastructure such as airports and transport hubs. The remaining 8% is attributed to specialized installations such as solar carports and marine-adapted systems.

Consumer adoption trends indicate that in 2025, over 41% of newly installed residential PV systems in urban Europe opted for all-black modules, while 36% of commercial building owners in Japan preferred all-black designs for rooftop solar retrofits.

In 2024, a metropolitan green building authority integrated all-black BIPV systems across 120 public schools, reducing grid electricity dependence by over 22% annually.

End-user segmentation in the All Black Solar Modules Market includes Residential Consumers, Commercial & Industrial (C&I) Users, Utility Developers, and Public Infrastructure Operators. Residential consumers form the largest segment with approximately 44% share, driven by rising urban homeownership, rooftop solar incentives, and growing demand for visually appealing energy solutions. C&I users follow closely with around 33%, as corporate sustainability reporting, ESG compliance, and long-term energy cost predictability drive rooftop solar investments across office parks, data centers, and retail chains.

Public infrastructure and municipal operators represent the fastest-growing end-user group, expanding at nearly 10.6% CAGR, fueled by smart city programs, decarbonization mandates for public buildings, and electrified transport infrastructure integration. Utility developers account for roughly 13%, focusing on visually integrated solar assets in mixed-use developments and transport-linked installations. The remaining 10% comprises institutional and specialty users such as educational campuses and healthcare facilities.

Adoption statistics reveal that in 2025, over 39% of new municipal solar installations in Asia-Pacific used all-black modules, while nearly 35% of newly constructed commercial buildings in Western Europe integrated premium all-black PV systems.

In 2024, a national urban development agency deployed all-black solar systems across 80 government office complexes, achieving a documented 19% reduction in annual grid electricity consumption.

Asia-Pacific accounted for the largest market share at 46.2% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2026 and 2033.

Asia-Pacific recorded more than 310 GW of cumulative rooftop solar capacity in 2025, with all-black modules representing nearly 29% of new premium rooftop installations. Europe followed with a 28.4% market share, supported by over 190 GW of distributed solar capacity and strong net-zero building mandates. North America captured 17.6%, driven by residential and commercial rooftop penetration exceeding 4.1 million installations. South America accounted for 5.1%, while the Middle East & Africa collectively held 2.7%, reflecting early-stage adoption. Global premium rooftop solar adoption reached 41% in urban zones, with all-black modules favored in 48% of new high-rise residential developments worldwide.

North America held approximately 17.6% of the All Black Solar Modules Market in 2025, supported by over 4.1 million cumulative rooftop solar installations. The United States accounted for nearly 82% of regional demand, followed by Canada at 12%. Residential rooftops contributed 44% of installations, while commercial buildings accounted for 36%. Federal tax credits of 30% and state-level net-metering policies significantly boosted adoption. Technological trends include AI-driven energy management systems integrated into rooftop PV and high-efficiency TOPCon black-cell modules exceeding 23.8% efficiency. A leading domestic manufacturer expanded a 2.4 GW premium module facility in Texas focused on all-black designs. Regional consumer behavior shows higher adoption among suburban homeowners, with 39% of new residential solar buyers choosing all-black modules for aesthetic reasons.

Europe represented around 28.4% of the global All Black Solar Modules Market in 2025. Germany, the UK, and France collectively accounted for 63% of regional installations. Germany alone deployed over 14.3 GW of new rooftop PV capacity in 2025, with all-black modules used in 46% of residential projects. EU building performance directives and zero-energy building regulations accelerated demand. Emerging technologies such as BIPV glass façades and frameless black modules are increasingly deployed in mixed-use developments. A German solar manufacturer launched a 1.1 GW production line dedicated to ultra-black modules. Regional consumer behavior reflects regulatory-driven demand, with 42% of new urban homeowners prioritizing integrated solar aesthetics over standard blue panels.

Asia-Pacific dominated global volume with 46.2% market share in 2025. China, Japan, and India together accounted for 81% of regional consumption. China alone operated over 650 GW of module manufacturing capacity, with all-black modules representing 31% of rooftop deployments. Japan recorded 9.2 GW of new residential PV capacity, while India added 7.8 GW across rooftop and commercial segments. Manufacturing automation, AI-based defect detection, and TOPCon cell lines exceeding 24.5% efficiency define regional trends. A Chinese producer commissioned a 3.6 GW all-black module factory in Anhui. Consumer behavior reflects rapid urbanization, with 34% of new city apartments integrating rooftop solar.

South America held approximately 5.1% of global demand in 2025. Brazil accounted for 61% of regional installations, followed by Argentina at 18% and Chile at 12%. Brazil surpassed 35 GW of distributed solar capacity, with all-black modules comprising 22% of new rooftop systems. Government incentives including import duty exemptions and feed-in tariffs supported adoption. Infrastructure trends include rapid rooftop solar deployment across logistics hubs and industrial parks. A Brazilian energy firm deployed 180 MW of premium rooftop solar using all-black modules. Consumer behavior shows growing demand among commercial property owners, with 28% preferring premium modules for brand positioning.

The Middle East & Africa accounted for 2.7% of global demand in 2025. The UAE and South Africa together represented 69% of regional installations. The UAE deployed over 3.4 GW of rooftop and building-integrated PV capacity, with all-black modules used in 26% of new urban developments. Construction megaprojects, hospitality complexes, and smart city initiatives are key demand drivers. Technological modernization includes bifacial black modules and solar glass façades. A UAE-based developer integrated all-black BIPV systems across 12 luxury residential towers. Regional consumer behavior reflects prestige-driven demand, with premium aesthetics influencing 31% of purchasing decisions.

China – 38.5% Market Share: Dominates due to massive manufacturing capacity exceeding 650 GW and large-scale rooftop solar deployment.

Germany – 14.2% Market Share: Leads through strong residential adoption, strict net-zero building mandates, and advanced BIPV integration.

The competitive environment in the All Black Solar Modules Market is dynamic, characterized by a mix of large multinational corporations and agile regional manufacturers driving innovation, scale, and market penetration. The market features 25–30 active competitors globally, spanning vertically integrated solar manufacturers, technology specialists, and emerging innovators. The market remains moderately fragmented, with the top 5 companies collectively accounting for an approximate 38–42% combined share of global solar module shipments, reflecting both consolidation at the top and diversity among specialized producers. Leading entities like JinkoSolar, LONGi, Trina Solar, JA Solar, and Waaree Energies maintain strong module shipment volumes—JinkoSolar alone shipped an estimated >90 GW of modules in 2024, with the top four firms exceeding 320 GW collectively.

Competition hinges on technology differentiation, including high-efficiency TOPCon, HPBC, and back-contact all-black variants; premium warranties extending 25–30 years on certain high-end models; and enhanced durability tailored for diverse climates. Strategic initiatives include production expansions, global product launches (e.g., new all-black series targeting specific regional compliance), and testing and quality standard certifications. Manufacturers are also forging partnerships with EPCs and developers to secure pipeline visibility in residential, commercial, and utility segments. Innovation trends such as AI-assisted manufacturing, advanced encapsulation, and high-power module architectures are further shaping competitive positioning. Overall, competitive intensity is high as firms balance cost leadership with premium performance and aesthetic differentiation in the expanding solar modules landscape.

JA Solar

Waaree Energies

Tongwei

CHINT (Astronergy)

GREW Solar

Solar-Fabrik

Sunpower Energy

Jolywood

CANADIAN SOLAR

T1 Energy

HVR Solar Pvt Ltd

The All Black Solar Modules Market is shaped by a suite of advancing technologies that enhance performance, durability, and aesthetic integration of photovoltaic systems. TOPCon (Tunnel Oxide Passivated Contact) technology remains a cornerstone in high-efficiency all-black modules, offering improved carrier passivation and lower recombination losses. Leading module lines leveraging TOPCon cells deliver power outputs up to 590–635 Wp in commercial and utility configurations, with enhanced low-light and temperature resilience.

Heterojunction Back Contact (HPBC) and Back-Contact (BC) technologies are gaining traction, delivering clean front surfaces and minimizing shading losses, which translates into higher effective output. For example, back-contact all-black modules have demonstrated module efficiencies above 23.5%, with junction box technologies rated IP68 for weather resilience and extended operational warranties of 30 years on power output retention.

Advanced materials such as structured glass with uniform reflectance control sustain visual blackout aesthetics without glare, facilitating adoption in residential and architectural applications. Module design evolution also emphasizes mechanical robustness, with resistance to extreme environmental stressors like salt spray, high humidity, and temperature cycling.

Emerging integration technologies include AI-assisted manufacturing systems that monitor defect rates and optimize yield, alongside high-density wafer formats (e.g., G12) that support power scaling into the 600 W+ range. In addition, solar modules are increasingly tested against comprehensive environmental standards covering hail, load, and thermal stress, proving their suitability for global deployment. Collectively, these technological advancements position all-black modules at the intersection of enhanced performance, aesthetic demand, and operational resilience.

• In June 2024, Trina Solar began mass production of its Vertex S+ full-black PV modules ranging from 430 W to 455 W with efficiencies up to 22.8%, featuring a sleek dual-glass design and enhanced durability for residential solar rooftops. Source: www.pv-magazine.com

• In March 2024, Trina Solar launched the NEG9R.25 all-black 450 W solar module with 22.5% conversion efficiency based on n-type TOPCon cells and full-black aesthetics, designed for residential, commercial, and industrial rooftop applications. Source: www.pv-magazine.com

• In June 2024, LONGi unveiled its Hi-MO X6 Artist Ultra Black series—ultra-black hybrid passivated back contact (HPBC) solar modules with up to 22.3% efficiency and structured glass for consistent aesthetic appeal and enhanced environmental performance; mass production was slated for late 2024 with global availability. Source: www.pv-magazine.com

• In December 2024, Trina Solar’s Vertex S+ Black Series reclaimed the 2025 German Design Award for superior aesthetics and performance, showcasing high uniformity black design and power output beyond 455 W with advanced i-TOPCon technology. Source: www.trinasolar.com

The scope of the All Black Solar Modules Market Report encompasses comprehensive analysis across product types, applications, end-users, geographical regions, technological trends, and competitive dynamics tailored to strategic decision-making. Product segmentation addresses the full spectrum of module technologies including Monocrystalline All Black Modules, TOPCon, HPBC, HJT, and back-contact designs, capturing performance outcomes, installation preferences, and aesthetic considerations influencing buyer behavior across residential, commercial & industrial, and utility-scale portfolios.

Application focus spans rooftop installations, architectural BIPV deployments, commercial façades, and utility arrays, offering insights into structural integration patterns, regulatory compliance requirements, and localized adoption trajectories. End-user breakdown highlights procurement behavior among homeowners, corporate developers, public infrastructure operators, and large-scale energy project developers, aiding stakeholders in aligning product offerings with segment-specific expectations.

Territorial coverage includes detailed region-wise insights into Asia-Pacific, Europe, North America, South America, and Middle East & Africa, each evaluated for market volume contributions, infrastructure trends, consumer behavior variations, and regional policy environments shaping module adoption. Technology analysis explores current and emerging innovations—including cell architectures, power scaling formats, AI-driven manufacturing enhancements, and robust environmental testing—designed to optimize performance and reliability under diverse global conditions.

The report further profiles competitive landscapes with quantitative shipment data, market positioning of leading manufacturers, strategic growth initiatives, and innovation benchmarking to inform investment decisions and partnership strategies. Additionally, niche segments such as premium aesthetic modules, UFLPA-compliant supply chains, and advanced warranty structures are examined to support forward-looking strategic planning in a rapidly evolving solar energy ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 820.0 Million |

| Market Revenue (2033) | USD 1,707.3 Million |

| CAGR (2026–2033) | 9.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | JJinkoSolar, LONGi Green Energy Technology, Trina Solar, JA Solar, Waaree Energies, Tongwei, CHINT (Astronergy), GREW Solar, Solar-Fabrik, Sunpower Energy, Jolywood, CANADIAN SOLAR, T1 Energy, HVR Solar Pvt Ltd |

| Customization & Pricing | Available on Request (10% Customization Free) |