Reports

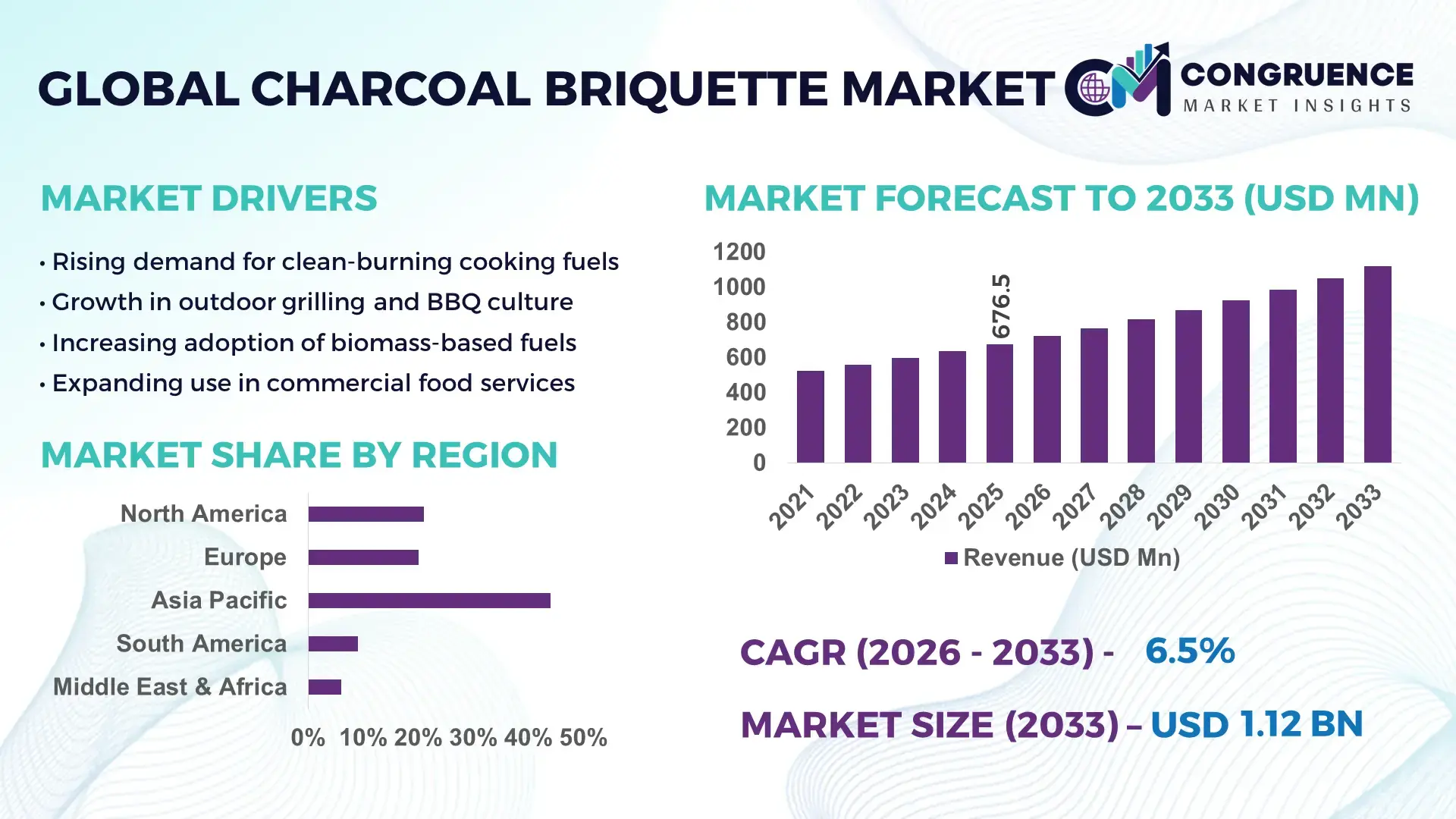

The Global Charcoal Briquette Market was valued at USD 676.45 Million in 2025 and is anticipated to reach a value of USD 1119.52 Million by 2033 expanding at a CAGR of 6.5% between 2026 and 2033. Growth is supported by rising demand for cleaner-burning solid fuels across residential cooking, commercial grilling, and small-scale industrial heating applications.

China represents the most influential country in the global charcoal briquette ecosystem, driven by its large-scale biomass processing infrastructure and integrated solid fuel manufacturing base. The country produces over 45 million metric tons of charcoal and charcoal-based fuels annually, supported by extensive agricultural residue availability such as rice husk, sawdust, and coconut shell. Industrial clusters in Guangdong, Shandong, and Fujian provinces host high-capacity briquetting facilities with automated extrusion and carbonization technologies exceeding 300,000 tons per plant per year. Capital investment in biomass densification equipment and carbon-neutral fuel alternatives has increased steadily, with briquettes widely adopted in food service, metallurgy pre-heating, and export-oriented barbecue fuel markets across East Asia, Europe, and the Middle East.

Market Size & Growth: Valued at USD 676.45 Million in 2025 and projected to reach USD 1119.52 Million by 2033 at a CAGR of 6.5%, driven by increasing substitution of traditional charcoal and firewood with uniform, low-emission briquettes.

Top Growth Drivers: Biomass fuel adoption +38%, thermal efficiency improvement +22%, deforestation-control compliance usage +19%.

Short-Term Forecast: By 2028, production cost optimization is expected to improve operational efficiency by approximately 16% through automated briquetting and drying systems.

Emerging Technologies: High-pressure screw extrusion, smokeless carbonization kilns, binder-free briquette formulation.

Regional Leaders: Asia-Pacific projected at USD 468 Million by 2033 with foodservice adoption growth, Europe at USD 312 Million driven by eco-fuel regulations, Africa at USD 189 Million supported by clean-cooking initiatives.

Consumer/End-User Trends: Commercial grilling, street food vendors, and small industrial users are shifting toward standardized briquettes for predictable burn time and heat output.

Pilot or Case Example: In 2024, an industrial biomass-to-briquette project in Southeast Asia achieved a 21% reduction in fuel waste and a 17% increase in combustion efficiency.

Competitive Landscape: Kingsford holds approximately 18% share, followed by Royal Oak, Duraflame, Green Heat, and Namchar.

Regulatory & ESG Impact: Clean cooking policies, biomass waste utilization mandates, and carbon reduction incentives are accelerating briquette adoption.

Investment & Funding Patterns: Over USD 420 Million invested recently in biomass densification plants, with growing use of public–private partnerships and green financing.

Innovation & Future Outlook: Advancements in low-ash briquettes, renewable binders, and integration with agricultural waste supply chains will shape long-term market expansion.

The charcoal briquette market serves diverse sectors including residential cooking, commercial foodservice, recreational grilling, and light industrial heating, with foodservice and hospitality accounting for the largest consumption contribution. Technological advancements such as smokeless briquettes, rapid-ignition products, and uniform-density extrusion are improving user convenience and energy efficiency. Regulatory pressure to reduce deforestation and indoor air pollution is encouraging adoption of biomass-based alternatives, particularly in Asia-Pacific and Africa. Regional consumption growth is strongest in urbanizing economies where clean cooking initiatives and fuel standardization are priorities. Looking ahead, the market is expected to benefit from circular economy models, increased agricultural residue utilization, and expanding export demand for premium-grade barbecue briquettes.

The Charcoal Briquette Market holds increasing strategic relevance as industries and governments prioritize cleaner solid fuels, biomass utilization, and energy efficiency within constrained regulatory environments. Strategically, charcoal briquettes support fuel standardization, predictable calorific output, and reduced particulate emissions compared to traditional lump charcoal. Advanced carbonization kilns deliver 28% higher thermal efficiency compared to earth-mound kilns, enabling producers to improve output consistency while lowering raw biomass losses. Asia-Pacific dominates in production volume, while Europe leads in adoption with nearly 41% of commercial foodservice enterprises using standardized briquettes for regulated grilling and heating operations.

From a future-pathways perspective, automation and digital process control are reshaping manufacturing strategies. By 2028, AI-enabled kiln temperature optimization is expected to cut fuel waste by 18% through real-time carbonization control and yield forecasting. Firms are committing to ESG performance improvements such as 25% reduction in non-renewable biomass usage by 2030 through agricultural residue sourcing and certified feedstock programs. In 2024, Indonesia achieved a 19% improvement in briquette yield consistency through semi-automated screw extrusion and moisture-control technology deployed at cooperative-scale facilities.

Strategically, charcoal briquettes are becoming integral to clean-cooking policies, export-grade barbecue fuel markets, and decentralized industrial heat applications. Forward-looking investment focuses on low-emission briquettes, binder-free formulations, and closed-loop biomass sourcing. Collectively, these developments position the Charcoal Briquette Market as a pillar of resilience, regulatory compliance, and sustainable growth within the global solid fuel value chain.

Rising demand for clean and standardized cooking fuels is a primary driver of the Charcoal Briquette Market, particularly in urban and regulated environments. Charcoal briquettes emit up to 30% less particulate matter compared to traditional firewood and irregular charcoal, making them suitable for compliance-driven commercial kitchens and street food operations. Foodservice operators increasingly prefer briquettes due to uniform size, consistent calorific value averaging 4,500–5,000 kcal/kg, and extended burn duration. Government-backed clean-cooking initiatives in Asia and Africa are encouraging transitions away from raw biomass, expanding household-level adoption. Additionally, export markets for barbecue fuel require standardized moisture content and ash levels, further reinforcing demand for engineered briquettes over conventional alternatives.

Feedstock supply variability remains a significant restraint for the Charcoal Briquette Market, directly affecting production stability and cost structures. Briquette manufacturing relies heavily on agricultural residues such as sawdust, rice husk, and coconut shell, which are subject to seasonal availability and competing industrial uses. Inconsistent moisture content and particle size increase preprocessing costs and reduce throughput efficiency by up to 14% in small and mid-scale plants. Additionally, informal biomass supply chains limit traceability, complicating compliance with sustainability certification requirements. In regions lacking organized residue collection infrastructure, transportation distances raise logistics costs, constraining scalability and discouraging capital investment in high-capacity briquetting facilities.

Clean-cooking policies and carbon reduction targets present substantial opportunities for the Charcoal Briquette Market. Governments are increasingly promoting processed biomass fuels as transitional alternatives to fossil-based cooking and heating solutions. Charcoal briquettes produced from agricultural waste can reduce lifecycle emissions by up to 35% compared to traditional charcoal. International development programs are supporting local briquette enterprises to replace firewood in urban households and institutional kitchens. Additionally, carbon credit mechanisms linked to reduced deforestation and lower indoor air pollution are opening new revenue streams for compliant producers. These policy-driven initiatives create long-term demand visibility and encourage formalization of production networks.

Regulatory compliance costs and technology gaps pose ongoing challenges to the Charcoal Briquette Market, particularly for small-scale producers. Emission standards, sustainability certifications, and worker safety requirements increase operational expenditures and necessitate capital investment in improved kilns and processing equipment. Modern carbonization systems can cost over 40% more than traditional setups, limiting adoption in price-sensitive markets. Furthermore, limited access to technical expertise hampers consistent quality control, leading to variable ash content and mechanical strength. These challenges slow market formalization and restrict the ability of producers to access premium export and institutional procurement channels.

Shift Toward Smokeless and Low-Emission Briquettes: Manufacturers are increasingly developing smokeless and low-volatile briquettes to meet stricter air-quality norms and commercial cooking requirements. Recent product specifications show particulate emission reductions of 25–35% compared to conventional lump charcoal, while ash content has been lowered to below 5% in premium grades. Over 48% of commercial foodservice operators now specify low-smoke briquettes for indoor or semi-enclosed grilling environments, reflecting a clear shift toward compliance-driven fuel selection.

Growing Use of Agricultural Residues as Primary Feedstock: The market is witnessing accelerated adoption of agricultural waste such as rice husk, coconut shell, corn cob, and sugarcane bagasse as briquette inputs. In major producing regions, over 62% of new briquette plants are designed to process multi-feedstock blends, improving raw material flexibility by nearly 30%. This transition has reduced dependence on hardwood charcoal and enabled biomass utilization rates exceeding 80% of locally available residues in organized production zones.

Automation and Process Standardization in Briquetting Plants: Automation in drying, carbonization, and extrusion stages is becoming a defining trend. Semi-automated production lines have demonstrated output consistency improvements of 20–27% and labor requirement reductions of approximately 18%. Digital moisture sensors and temperature-controlled kilns are now deployed in nearly 35% of mid-to-large facilities, supporting uniform density, higher mechanical strength, and improved burn-time reliability for export-grade briquettes.

Expansion of Commercial and Institutional End-Use Adoption: Demand from hotels, restaurants, catering services, and institutional kitchens is rising steadily. Commercial users account for nearly 44% of standardized briquette consumption, driven by predictable heat output and burn durations exceeding 3.5 hours per unit. In urban centers, institutional buyers report fuel waste reductions of up to 22% after switching from irregular charcoal to engineered briquettes, reinforcing long-term procurement contracts and stable demand patterns.

The Charcoal Briquette Market is segmented by type, application, and end-user, reflecting diverse performance requirements, consumption patterns, and regulatory expectations. Product type segmentation highlights variations in raw material composition, emission profile, and burn efficiency. Application-based segmentation underscores the dominance of cooking and grilling uses alongside emerging industrial and institutional demand. End-user segmentation further differentiates between residential households, commercial foodservice operators, and industrial or institutional buyers, each with distinct procurement criteria. Across segments, standardization, low-smoke performance, and sustainability compliance are key differentiators influencing purchasing decisions. This segmentation framework enables manufacturers and investors to align product development, capacity planning, and market entry strategies with high-demand use cases and rapidly evolving end-user preferences.

The Charcoal Briquette Market by type includes hardwood charcoal briquettes, biomass/agricultural residue briquettes, coconut shell briquettes, and mixed-feedstock or specialty briquettes. Hardwood charcoal briquettes currently account for approximately 46% of total adoption due to their stable calorific value, predictable burn time, and widespread acceptance in commercial grilling and export markets. Biomass and agricultural residue briquettes hold about 28%, benefiting from lower raw material costs and alignment with clean-cooking initiatives. Coconut shell briquettes represent nearly 16%, favored in premium barbecue and hookah applications for low ash content and high fixed carbon. Specialty and blended briquettes collectively contribute around 10%, serving niche industrial and institutional uses.

Biomass-based briquettes are the fastest-growing type, expanding at an estimated 7.8% annually, driven by deforestation controls and agricultural waste utilization mandates.

By application, cooking and grilling dominate the Charcoal Briquette Market with roughly 52% adoption, supported by consistent heat output, extended burn duration, and reduced smoke generation. Commercial foodservice and street food operations represent the largest share within this segment due to standardized fuel requirements. Industrial heating and metallurgy pre-heating applications account for about 21%, using briquettes for controlled thermal processes. Recreational and barbecue use contributes approximately 17%, while institutional cooking and other applications collectively represent 10%.

Institutional and commercial cooking applications are growing fastest at an estimated 6.9% annually, supported by urbanization and hygiene-focused fuel policies.

End-user segmentation shows commercial foodservice operators leading with around 44% share, driven by demand for uniform heat performance and predictable procurement volumes. Residential households account for approximately 33%, particularly in regions transitioning from firewood to cleaner solid fuels. Industrial and institutional users together represent about 23%, utilizing briquettes for controlled heating and bulk cooking needs.

Institutional users are the fastest-growing end-user group, expanding at an estimated 7.2% annually, fueled by public-sector clean energy programs and centralized procurement systems. Adoption among educational institutions, hospitals, and military facilities has increased steadily, with usage rates exceeding 40% in newly commissioned kitchens in select regions.

Asia-Pacific accounted for the largest market share at 48.6% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.3% between 2026 and 2033.

Asia-Pacific leads due to large-scale production and consumption across China, India, and Southeast Asia, with annual charcoal and briquette output exceeding 60 million metric tons. Europe followed with a 22.4% share in 2025, driven by regulated commercial grilling and sustainability mandates. North America held nearly 17.1%, supported by strong barbecue culture and commercial foodservice demand. South America accounted for 6.8%, while Middle East & Africa represented 5.1%, with accelerating adoption through clean-cooking programs. Regional differences are shaped by biomass availability, regulatory strictness, export orientation, and consumer cooking habits, resulting in varied demand intensity and product specifications across markets.

How is demand for standardized grilling fuels reshaping purchasing behavior?

North America accounted for approximately 17.1% of the Charcoal Briquette Market in 2025, supported by high per-capita consumption in residential grilling and commercial foodservice. The foodservice, hospitality, and recreational barbecue sectors are key demand drivers, with over 65% of commercial grills using briquettes for consistent heat control. Regulatory focus on emissions and workplace safety has encouraged adoption of low-smoke briquettes. Technological advancements include automated packaging, moisture-controlled storage, and digital inventory systems. Local players such as Kingsford are expanding low-ash and quick-ignition product lines. Consumer behavior in this region shows strong preference for premium, performance-certified briquettes, with higher spending per unit and strong seasonal demand spikes.

How are sustainability mandates influencing fuel standardization decisions?

Europe captured nearly 22.4% of the Charcoal Briquette Market in 2025, with Germany, the UK, and France leading consumption. Regulatory bodies emphasize deforestation prevention, certified biomass sourcing, and emission limits, driving demand for compliant briquettes. Over 58% of commercial foodservice operators in Western Europe specify sustainability-certified solid fuels. Adoption of advanced carbonization and traceability technologies is rising, particularly in export-focused markets. Local producers are investing in binder-free briquettes and recyclable packaging. Consumer behavior reflects regulatory pressure, with buyers prioritizing transparent sourcing, low-smoke performance, and compliance documentation in procurement decisions.

Why does large-scale production coexist with rapid consumption growth?

Asia-Pacific dominates the Charcoal Briquette Market by volume, accounting for 48.6% share in 2025. China, India, and Japan are the top consuming countries, supported by extensive agricultural residue availability and dense urban populations. Manufacturing hubs operate high-capacity briquetting plants exceeding 300,000 tons annually. Infrastructure investments focus on automated extrusion, carbonization kilns, and export logistics. Regional innovation hubs are advancing smokeless and high-density briquettes. Local producers in China and Indonesia are expanding export-grade production. Consumer behavior varies widely, with strong household adoption for cooking and growing commercial demand in urban foodservice clusters.

How are energy transitions shaping alternative solid fuel demand?

South America held around 6.8% of the Charcoal Briquette Market in 2025, led by Brazil and Argentina. Brazil remains a major producer, leveraging forestry residues and agricultural byproducts. Energy diversification and rural clean-cooking initiatives support briquette usage. Infrastructure development in biomass processing and export terminals strengthens regional supply chains. Government incentives promoting renewable biomass fuels are encouraging small and mid-scale briquetting operations. Local producers are integrating charcoal briquettes into metallurgical pre-heating and foodservice supply. Consumer behavior shows steady household adoption, with demand closely linked to regional cooking traditions and fuel affordability.

What role do clean-cooking and hospitality sectors play in adoption?

Middle East & Africa represented approximately 5.1% of the Charcoal Briquette Market in 2025 but shows the fastest growth momentum. Demand is driven by hospitality, tourism, and household cooking sectors, particularly in UAE, Saudi Arabia, and South Africa. Clean-cooking programs and fuel substitution policies are expanding briquette usage in urban centers. Technological modernization includes improved kiln efficiency and standardized packaging for export and hotel supply chains. Local players in East Africa are scaling agricultural waste briquettes. Consumer behavior emphasizes affordability, long burn time, and reduced smoke for indoor use.

China: 32.4% market share — Dominance supported by large-scale production capacity, integrated biomass supply chains, and strong export-oriented manufacturing.

United States: 14.7% market share — Leadership driven by high per-capita consumption, established commercial grilling culture, and advanced product standardization.

The Charcoal Briquette Market exhibits a moderately fragmented competitive structure, characterized by a mix of multinational brands, regional leaders, and a large base of small and mid-sized producers. More than 120 commercially active manufacturers operate globally, with the top five companies collectively accounting for approximately 46% of total market volume, indicating balanced competitive intensity rather than high consolidation. Leading players compete on product consistency, low-smoke performance, feedstock sourcing transparency, and packaging innovation.

Strategic initiatives increasingly focus on product launches such as fast-ignition briquettes, low-ash premium variants, and binder-free formulations. Over 38% of established manufacturers have introduced upgraded briquette lines within the last three years to meet regulatory and commercial foodservice requirements. Partnerships with agricultural cooperatives and biomass aggregators are expanding, enabling feedstock cost stabilization of up to 15%. Mergers and capacity expansions are primarily regional, with plant-scale upgrades improving output efficiency by 20–25%. Innovation trends include automated extrusion lines, controlled carbonization kilns, and recyclable packaging adoption exceeding 40% among top-tier brands. Competitive differentiation is driven less by price and more by compliance readiness, burn-time performance, and export-grade certification.

Kingsford Products Company

Royal Oak Enterprises

Duraflame, Inc.

Green Heat International

Namchar Group

Matsuri International

Saint Louis Charcoal Company

Carbonex Group

Coco Briquette Indonesia

Kingsford Products Company

Royal Oak Enterprises

Duraflame, Inc.

Technological innovation is playing a critical role in shaping the Charcoal Briquette Market, driving improvements in efficiency, product quality, and environmental compliance. Current production technology emphasizes automated extrusion, controlled carbonization, and precision drying, which together enhance calorific value consistency and reduce raw material losses by up to 22%. Semi- and fully-automated screw extruders now handle multi-feedstock inputs, enabling plants to process agricultural residues, sawdust, and coconut shells with uniform density, mechanical strength, and ash content below 5%. Digital moisture and temperature sensors integrated into carbonization kilns monitor real-time conditions, minimizing over- or under-carbonization and improving yield efficiency by approximately 18–20%.

Emerging technologies are further redefining market standards. Smokeless and low-volatile briquettes leverage binder-free formulations and high-pressure densification to reduce particulate emissions by 25–30%, meeting stricter indoor air quality regulations for commercial and institutional applications. Additive-based briquettes incorporating bio-resins or activated carbon are also gaining traction, providing improved ignition rates and thermal stability. In terms of process innovation, modular carbonization units capable of 50,000–300,000 tons per year are increasingly deployed across Asia-Pacific and Africa, reducing setup time and enhancing local manufacturing scalability.

Digital transformation trends are influencing operational efficiency, including predictive maintenance through IoT-enabled sensors and real-time energy monitoring, resulting in downtime reductions of 15–17%. Additionally, automated packaging and labeling systems support export compliance, with up to 42% of top-tier facilities adopting traceable digital workflows for product quality verification. Overall, technological advancements in production, emission control, and digital operations are positioning the Charcoal Briquette Market for higher sustainability, consistency, and competitive differentiation in both regional and international markets.

• In March 2024, The Good Charcoal Company launched its Super Briquettes with Lowe’s retail distribution in 15.4 lb bags, introducing the first Forest Stewardship Council‑certified charcoal briquettes designed for cleaner burn and sustainability appeal among premium grilling customers.

• In May 2025, Kingsford and Miller Lite revived the limited‑edition Kingsford x Miller Lite “Beercoal” charcoal briquettes made with real beer, marking a popular seasonal product return that blends consumer experience innovation with grilling flavor enhancement.

• In May 2025, Weber Stephen Products completed the acquisition of Charcoal House’s briquette assets to strengthen its premium fuel portfolio and scale manufacturing capabilities for consistent, high‑quality briquette offerings across North American and global markets.

• In July 2025, Kona Carbon introduced its Kona Pro Coconut Briquettes, a new product line leveraging coconut shell charcoal with enhanced burn performance and reduced ash characteristics, aimed at both commercial and backyard grilling segments.

The scope of the Charcoal Briquette Market Report encompasses comprehensive analysis across product types, end‑use applications, regional dimensions, and technological trends. The report details segmentation by type, including traditional hardwood charcoal briquettes, biomass and agricultural residue briquettes, coconut shell variants, and specialty blended fuels, highlighting their functional characteristics, quality metrics such as ash content and burn duration, and performance specifications for different user needs. Geographic coverage spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with detailed market volume distribution, adoption patterns, and regulatory landscape differences across each region.

Application segments include residential grilling and cooking, commercial foodservice and hospitality usage, industrial thermal processes, and recreational outdoor cooking. End‑user insights focus on household consumption behaviors, institutional procurement strategies, and commercial purchasing criteria influenced by performance, emissions, and compliance needs. The report also analyzes technology adoption in briquette manufacturing, such as automated extrusion lines, controlled carbonization systems, digital process control, and product differentiation through fast‑ignition and low‑smoke variants. It further examines quality assurance frameworks, packaging innovations, and traceability practices that affect supply chain performance and buyer confidence.

Emerging topics cover sustainability drivers, including eco‑friendly feedstock sourcing, biomass recycling, and environmentally certified product development. Niche segments such as premium flavored briquettes, hookah and specialty culinary briquettes, and water‑resistant packaging solutions are also explored. The report integrates competitive landscape assessments, strategic initiatives by key players, and future market opportunities informed by demographic shifts, consumer preferences, and technology trends, providing decision‑makers with actionable insights into the evolving global charcoal briquette ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 6.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Kingsford Products Company, Royal Oak Enterprises, Duraflame, Inc., Green Heat International, Namchar Group, Matsuri International, Saint Louis Charcoal Company, Carbonex Group, Coco Briquette Indonesia, Kingsford Products Company, Royal Oak Enterprises, Duraflame, Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |