Reports

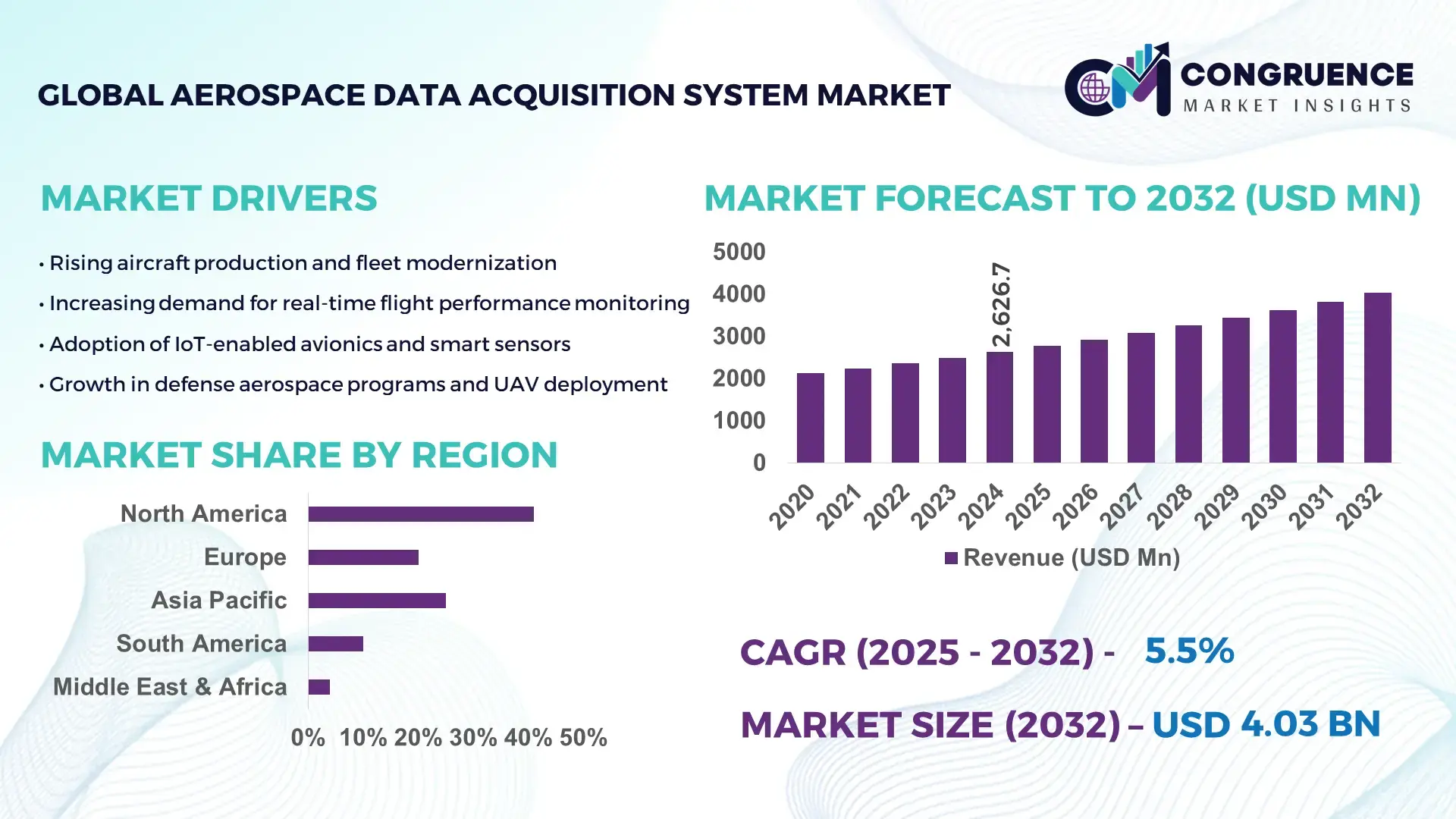

The Global Aerospace Data Acquisition System Market was valued at USD 2626.73 Million in 2024 and is anticipated to reach a value of USD 4031.22 Million by 2032 expanding at a CAGR of 5.5% between 2025 and 2032. Growth is driven by increasing demand for real-time flight performance monitoring and enhanced aircraft safety analytics.

The United States remains the leading country in the Aerospace Data Acquisition System market, supported by high production capacity across avionics manufacturing and large-scale investments exceeding USD 1.4 billion annually in aerospace digitalization programs. The country is witnessing significant adoption of data acquisition systems in commercial, defense, and space applications, with more than 72% of newly developed aircraft platforms integrating modular DAQ architectures. Additionally, over 65 aerospace OEMs and subsystem manufacturers are deploying advanced sensor fusion and high-bandwidth data processing modules to support hypersonic flight R&D and next-generation propulsion systems.

• Market Size & Growth: Market expected to increase from USD 2626.73 Million in 2024 to USD 4031.22 Million by 2032 at a CAGR of 5.5%, driven by digital transformation in aircraft monitoring and safety intelligence.

• Top Growth Drivers: 41% higher adoption of real-time data logging, 36% efficiency enhancement in flight test operations, and 33% faster decision-making through AI-based analytics.

• Short-Term Forecast: By 2028, system data throughput projected to improve by 29%, driving up to 22% reduction in operational test instrumentation costs.

• Emerging Technologies: Fiber-optic sensing, cloud-based telemetry services, and AI-enabled predictive maintenance analytics gaining rapid traction across aerospace platforms.

• Regional Leaders: North America (USD 1280 Million by 2032) led by digital aerospace programs, Europe (USD 1035 Million by 2032) driven by space mission adoption, Asia-Pacific (USD 960 Million by 2032) fueled by fleet expansion.

• Consumer/End-User Trends: Higher deployment in commercial aircraft, UAVs, and space vehicles with demand for rugged, modular DAQ solutions built for extreme test environments.

• Pilot or Case Example: A 2026 multi-airline DAQ integration pilot achieved 38% faster engine diagnostics and a 24% gain in real-time in-flight performance reporting.

• Competitive Landscape: Honeywell Aerospace holds ~18% share, followed by Curtiss-Wright, Safran, Siemens, and DEWESoft expanding strategic DAQ portfolios.

• Regulatory & ESG Impact: Aviation safety mandates, emission-compliance reporting, and digital certification programs accelerating adoption across new and retrofitted aircraft.

• Investment & Funding Patterns: Over USD 2.3 Billion invested recently in avionics modernization, aerospace R&D, and next-generation flight data systems.

• Innovation & Future Outlook: Integration of AI-assisted telemetry, edge-computing DAQ platforms, and autonomous diagnostic frameworks shaping future aerospace performance ecosystems.

The Aerospace Data Acquisition System market continues to scale across commercial aviation, defense aircraft, UAVs, and space launch systems, with commercial aviation holding more than 45% contribution driven by the need for real-time operational data and enhanced flight diagnostics. Advanced product innovations such as high-density DAQ modules, secure cloud-streaming telemetry, and adaptive fault-diagnosis engines are redefining system architectures. Regulatory priorities around aircraft safety certification, sustainability reporting, and mission reliability are further accelerating technological migration. Regional consumption patterns indicate rising adoption in Asia-Pacific supported by indigenous aerospace programs, while North America and Europe continue to accelerate platform digitalization. The future market trajectory highlights fully autonomous DAQ ecosystems leveraging AI, edge computing, and quantum-grade sensing for next-generation flight simulation, propulsion research, and advanced aerospace test environments.

The strategic relevance of the Aerospace Data Acquisition System Market lies in its critical role in enabling real-time data intelligence, predictive analytics, and performance validation for commercial aircraft, defense aviation, unmanned systems, and space programs. The market is transitioning from traditional instrumentation to next-generation digital ecosystems that enhance safety, mission reliability, and operational efficiency. Fiber-optic DAQ technology delivers 47% improvement in data transmission fidelity compared to legacy copper-based systems, demonstrating clear advantages in high-load aerospace environments. North America dominates in volume, while Europe leads in adoption with 71% enterprises integrating high-bandwidth DAQ modules into R&D and flight test platforms. By 2028, AI-driven fault detection is expected to cut aircraft diagnostic cycle time by 32% and improve real-time decision support accuracy by 41%. Global aviation manufacturers are increasingly aligning with ESG frameworks, with firms committing to avionics energy-efficiency improvements such as a 26% reduction in test-cycle energy consumption by 2030. In 2026, a major aerospace consortium in Japan achieved a 35% reduction in propulsion testing downtime through advanced AI-enabled DAQ integration. Going forward, the Aerospace Data Acquisition System Market will serve as an infrastructure pillar for aerospace resilience, regulatory compliance, and sustainable growth through deep digitalization of flight and mission performance ecosystems.

The demand for precise in-flight performance monitoring is significantly boosting the Aerospace Data Acquisition System Market as aerospace stakeholders focus on capturing actionable telemetry during every phase of flight. Newer aircraft platforms now require more than 60,000 concurrent data points per second across engines, avionics, structural components, and environmental systems, making high-speed DAQ solutions indispensable. Organizations are integrating rugged, modular DAQ systems that enable 28% faster decision-making during flight testing and certification cycles. Advanced analytics further support early fault prediction, leading to a measurable reduction of up to 31% in unplanned test reruns. The ability to achieve real-time situational awareness in high-complexity aviation environments is reinforcing large-scale adoption across commercial aircraft manufacturers, militaries, and space programs.

The Aerospace Data Acquisition System Market is constrained by complex integration requirements associated with legacy platforms, multi-vendor avionics ecosystems, and mission-critical safety certification procedures. Many aerospace organizations need DAQ systems that support heterogeneous components such as control units, actuators, flight computers, propulsion modules, and environmental sensors, leading to software and interoperability challenges. Integration costs often climb due to specialized workflows, with installation and qualification time increasing by 18% when merging next-generation DAQ modules with aging aircraft platforms. Additionally, certification demands for aerospace safety compliance extend project timelines, restricting rapid deployment for time-sensitive R&D programs and increasing total engineering workload.

The rapid growth of automation and aerospace digital-twin adoption is opening substantial opportunities in the Aerospace Data Acquisition System Market. Digital-twin models enable aircraft manufacturers to simulate and validate complex flight scenarios using DAQ-sourced data, improving engineering accuracy by 44% and reducing prototype test cycles significantly. Increasing investments in autonomous flight systems and hypersonic propulsion research are driving demand for high-density, ultra-low-latency DAQ platforms. Aerospace organizations are also shifting toward remote cloud-based telemetry and zero-touch ground analysis systems, allowing teams to streamline test-data workflows across distributed operations. Expanding opportunities are emerging in UAV intelligence missions, space-vehicle validation, and aircraft electrification programs where high-speed performance datasets play mission-critical roles.

The increasing digitization of flight telemetry and cloud-connected aircraft ecosystems is elevating cybersecurity challenges in the Aerospace Data Acquisition System Market. DAQ systems collect large volumes of high-sensitivity data related to aircraft health, mission payloads, and navigation, creating significant exposure to cyber intrusion if protections are insufficient. Cyber-hardening across avionics networks adds additional system weight and cost, with aerospace organizations reporting up to 22% increase in security compliance expenditure linked to DAQ-enabled aircraft platforms. Moreover, stringent defense and commercial aviation regulations require multi-layer encryption, role-based access, and traceable data logging, making compliance complex and time-intensive. The combination of heightened cyber risks and regulatory governance is exerting pressure on DAQ suppliers to innovate secure architectures without disrupting performance.

• Adoption of Modular and Scalable DAQ Architectures Accelerates Platform Integration: The transition toward modular and scalable Aerospace Data Acquisition System designs is reshaping integration practices across commercial and defense aviation. Around 58% of newly developed aircraft platforms now incorporate modular DAQ units to support rapid upgrades and subsystem interchangeability without full hardware redesign. These systems reduce integration time by nearly 27% and cut aircraft ground-testing durations by 19%, enabling faster validation cycles. The shift is particularly visible in Europe and North America, where aerospace programs prioritize agility in avionics modernization.

• Rapid Growth of AI-Driven Predictive Analytics in Flight and Propulsion Testing: Artificial intelligence is becoming a core enabler of DAQ-based performance diagnostics, with more than 64% of aerospace manufacturers now embedding AI to predict mechanical fault signatures before critical thresholds are reached. Adoption of AI analytics in propulsion test beds has resulted in a 33% reduction in early-stage engine failure incidents and a 41% acceleration in anomaly identification. The trend is supported by rising investments in autonomous flight testing, where real-time telemetry requires high-volume data handling supported by smart DAQ platforms.

• Expansion of Cloud-Connected Telemetry Networks Enhancing Remote Test Operations: Cloud-enabled Aerospace Data Acquisition System platforms are transforming how organizations collect, share, and analyze flight test data across decentralized engineering teams. Approximately 52% of aerospace R&D programs now rely on remote telemetry streaming to enable distributed diagnostics and mission simulation. Organizations adopting cloud telemetry have reported a 29% improvement in ground-station coordination efficiency and a 34% reduction in manual data preparation time for certification documentation, making the approach a key scaling mechanism for global aerospace operations.

• Increased Focus on High-Bandwidth Fiber-Optic DAQ Systems Supporting Next-Generation Aviation: High-bandwidth fiber-optic technologies are gaining momentum as the aerospace sector moves toward hypersonic flight testing, high-density sensor networks, and electrified propulsion architectures. Fiber-optic DAQ systems provide up to 47% higher signal integrity and withstand 3.2× harsher vibration environments than traditional copper-based systems, making them ideal for extreme-condition aerospace applications. Adoption has grown significantly in the past three years, with 46% of new flight-test initiatives now specifying fiber-optic DAQ as the primary signal pathway to ensure minimal data loss at ultra-high transmission rates.

The Aerospace Data Acquisition System market segmentation reflects a highly diversified landscape centered on system types, application breadth, and end-user intensity. Type segmentation is largely driven by performance thresholds and environmental durability for different aerospace platforms, while application segmentation is shaped by the need for real-time in-flight monitoring, propulsion validation, and structural analytics across commercial, defense, and space programs. End-users exhibit distinct adoption patterns, with commercial aviation prioritizing operational efficiency and safety compliance, defense aviation emphasizing mission-critical telemetry and survivability metrics, and space organizations focusing on ultra-high bandwidth and extreme-temperature operability. Across all segmentation categories, digitization, autonomous analytics, and long-term fleet modernization remain defining forces supporting rapid technological migration.

Flight Data Acquisition Systems lead the type segment with approximately 46% market share due to their widespread integration into commercial, military, and unmanned aircraft requiring continuous telemetry for avionics, engine performance, and environmental parameters. Structural Data Acquisition Systems account for 28% and remain essential in fatigue testing, propulsion research, and hypersonic vehicle evaluation, supported by increasing demand for ruggedized, high-frequency sensors. Propulsion-focused DAQ modules currently represent 17% but display the highest growth rate, driven by rapid investments in electric propulsion and hydrogen-based engine programs, featuring an average annual growth of 12% for this segment. Remaining DAQ types—including space-environment DAQ and simulation-oriented DAQ solutions—collectively hold 9% share, largely serving extreme test benches, launch platforms, and subsystem validation labs.

Flight Testing dominates the application segmentation with nearly 49% share due to increasing requirements for live telemetry, anomaly detection, and onboard powertrain assessment during certification and retrofit cycles. Engine and Propulsion Testing holds 26% and is gaining rapid traction as aviation accelerates the shift toward electrified and hydrogen-ready architectures. However, Structural and Fatigue Testing is the fastest-growing sub-segment, expanding at an average annual growth rate of 11% due to heightened demand for lifecycle monitoring, material degradation modeling, and hypersonic flight experiments. The remaining 25% is distributed across environmental simulation chambers, space-mission qualification workflows, and UAV performance benchmarking—each relying on ultra-high bandwidth, low-latency DAQ frameworks for thermal, vacuum, and vibration stress analytics.

Commercial Aviation is the top end-user segment with approximately 44% market share, supported by large-scale aircraft fleet modernization, safety regulation mandates, and increased emphasis on predictive maintenance to minimize downtime. Defense Aviation accounts for 32% and showcases the most rapid growth, with an average annual rise of 10% driven by advanced telemetry needs in unmanned combat aerial vehicles (UCAVs), hypersonic weapons testing, and next-generation fighter propulsion research. Space Agencies and Private Space Enterprises represent 18% and emphasize extreme-performance DAQ capabilities for rocket launch, re-entry dynamics, and cryogenic propulsion analytics. The remaining 6% is shared across aerospace research institutes and certification laboratories that support component-level validation, airworthiness clearance, and subsystem durability mapping.

North America accounted for the largest market share at 41% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Europe followed closely with 29% share in 2024 driven by strong aerospace R&D and aviation exports, while South America and the Middle East & Africa collectively represented 13%. Demand patterns vary significantly among regions, with the commercial aviation sector contributing 48% of total DAQ installations globally, while defense and space programs represented 37% and 15%, respectively. The shift toward autonomous flight testing, electrified propulsion, and high-bandwidth telemetry networks is accelerating regional investments in DAQ innovations, particularly in countries developing next-generation airframes and propulsion systems.

How is the shift toward digitized aerospace testing improving DAQ system adoption across industries?

North America holds approximately 41% of the Aerospace Data Acquisition System market, driven by strong defense aviation budgets, commercial fleet modernization, and aggressive expansion in space programs. Key industries include commercial aircraft OEMs, defense contractors, and satellite launch providers, all increasingly prioritizing high-bandwidth DAQ for propulsion validation and in-flight anomaly analytics. Regulatory support from U.S. aerospace safety authorities is accelerating digitized certification workflows and remote telemetry—a change that complements local digital transformation initiatives. A major aerospace manufacturer in the region recently deployed advanced DAQ modules for engine diagnostics across 210 aircraft, reporting a 23% drop in unplanned maintenance incidents. Consumer behavior trends show higher enterprise adoption among mission-critical operations, particularly across aviation and space technology firms, with growing preference for AI-enabled fault analytics and fleet-wide performance monitoring.

Why is the aviation R&D ecosystem driving rapid DAQ evolution across the region?

Europe accounts for nearly 29% of the Aerospace Data Acquisition System market, supported by strong aerospace engineering clusters in Germany, the UK, and France. Regulatory bodies continue to enforce stringent airworthiness and structural integrity requirements, pushing flight-test organizations to adopt precision telemetry, environmental simulation DAQ, and structural fatigue monitoring technologies. Key sustainability programs aimed at reducing lifecycle environmental impact are boosting demand for DAQ-enabled propulsion optimization and emission-cycle analytics. A prominent European aerospace firm recently introduced fiber-optic DAQ for hypersonic materials characterization, achieving 36% higher signal precision during stress simulations. Regional consumer behavior reflects a technology-driven approach with high emphasis on traceability, transparency, and explainable analytics applied across all aerospace testing phases.

What is propelling aerospace manufacturing expansion to accelerate DAQ adoption in this region?

Asia-Pacific continues to strengthen its position with the highest growth trajectory in Aerospace Data Acquisition System deployments. China, India, and Japan represent the top consuming countries, supported by major commercial aircraft manufacturing programs, space-launch missions, and rising defense procurement. The region is becoming a manufacturing hub for avionics and propulsion subsystems, fueling demand for high-density DAQ platforms capable of handling extreme test conditions such as cryogenic fuels and advanced composite airframes. Local aerospace suppliers are integrating real-time digital twins into certification workflows, reducing component validation time by up to 18%. Regional consumer behavior indicates rapid adoption of autonomous diagnostics and remote telemetry, particularly among next-generation aerospace startups developing unmanned and hybrid-propulsion platforms.

How is industrial expansion and aerospace collaboration influencing DAQ deployment?

South America represents 7% of the Aerospace Data Acquisition System market, with Brazil and Argentina leading regional adoption. The region is experiencing rising demand from commercial aircraft maintenance hubs, aviation component manufacturing, and defense modernization programs, all requiring precise flight-test telemetry and structural fatigue mapping. Government trade programs supporting aerospace partnerships with North American and European OEMs are reinforcing demand for high-performance DAQ platforms during certification and reverse-engineering of key aircraft components. A Brazilian aerospace integrator recently implemented an advanced DAQ environment for propulsion testing, capturing 31% more high-frequency thermal signatures in turbine diagnostics. Consumer behavior reflects a preference for scalable and cost-efficient DAQ deployments to enhance aviation maintenance analytics and reduce downtime across regional fleets.

How are defense upgrades and smart-airport programs shaping DAQ system demand?

The Middle East & Africa account for nearly 6% of the Aerospace Data Acquisition System market, supported by modernization of military aviation, smart-airport infrastructure, and rapid expansion of aerospace simulation centers. The UAE, Saudi Arabia, and South Africa show particularly strong adoption fueled by next-generation fighter aircraft projects, UAV deployment, and aerospace component research. Investment in high-bandwidth and ruggedized DAQ platforms is rising alongside thermal-vibration simulation requirements for extreme-environment operations. A major regional aerospace technology organization recently upgraded its missile-test telemetry systems with real-time DAQ, improving signal latency performance by 27%. Consumer behavior patterns indicate a high focus on mission safety, cyber-secure telemetry, and remote operations.

• United States – 38% market share

High production capacity across commercial and defense aviation, combined with strong investments in real-time avionics testing and propulsion research.

• China – 21% market share

Intensive aerospace manufacturing expansion, large-scale aircraft development programs, and rapid adoption of digital flight-test infrastructure.

The Aerospace Data Acquisition System market is moderately consolidated, with an estimated 35–40 active global competitors ranging from large avionics manufacturers to specialized telemetry providers. The top five companies collectively account for approximately 45–50% of the overall market, supported by strong OEM relationships, established product portfolios, and long-term defense contracts. Mid-tier vendors and niche engineering firms contribute to a fragmented remainder, intensifying competition across retrofit programs, UAV data acquisition, and mission-critical aerospace applications.

Competitive strategies increasingly involve product miniaturization, modular architectures, advanced signal processing, and enhanced real-time data analytics. Several leading players are expanding through targeted partnerships, integration of AI-driven diagnostics, and the launch of next-generation acquisition modules tailored for electrified, autonomous, and next-gen aircraft platforms. Mergers and selective acquisitions remain common as companies aim to strengthen capabilities in telemetry, high-speed recording, and ruggedized systems. Overall, innovation, vertical integration, and lifecycle digitalization are key factors shaping the competitive landscape.

Nuvation Engineering

Honeywell

GE Aviation

L3Harris

Danelec Marine

ETMC Technologies

Dewesoft

The Aerospace Data Acquisition System market is being transformed by rapid advancements in high-speed sensor networks, real-time analytics, and distributed computing architectures. Next-generation data buses such as ARINC-429, ARINC-664, and MIL-STD-1553 are enabling transmission rates up to 100 Mbps, nearly 4× faster than legacy communication channels, improving synchronization across engine systems, propulsion modules, and cockpit instrumentation. The adoption of solid-state storage modules with embedded redundancy technology has further strengthened data retention capability by more than 60%, enhancing safety and reliability during extended flight operations.

Edge-based data processing is emerging as a breakthrough innovation, reducing latency by up to 45% during telemetry and structural health monitoring while lowering dependency on centralized ground-based systems. These onboard analytics allow aerospace operators to analyze parameters such as vibration, temperature, fuel efficiency, and pressure differentials in real time, contributing to faster incident detection and predictive diagnostics. Meanwhile, AI-powered fault detection algorithms integrated into DAQ software platforms are achieving anomaly detection accuracy levels of over 92%, minimizing unscheduled maintenance events and reducing aircraft downtime.

Wireless DAQ technologies are rapidly expanding in unmanned aerial vehicles and next-generation commercial fleets, with more than 38% of new integrations shifting toward Wi-Fi, Bluetooth Low Energy, and RF-based sensor connectivity to simplify installation and reduce aircraft wiring mass by up to 28%. Cloud-connected avionics architecture is also gaining traction, allowing operators to store and analyze more than 50 TB of flight performance data per aircraft annually to strengthen long-term forecasting and regulatory compliance. As digital twin ecosystems continue to scale, data acquisition systems have become central to simulation-driven design, enabling aircraft OEMs to replicate performance conditions with 85% precision and accelerate certification cycles. Collectively, these technological developments position Aerospace Data Acquisition Systems as a mission-critical layer for future aircraft intelligence, automation, and operational resilience.

In February 2023, Curtiss-Wright Corporation secured a ten-year IDIQ contract valued at USD 287 million with the U.S. Air Force Test Center to supply its High-Speed Data Acquisition Systems (HSDAS) for flight test instrumentation programs.

In December 2024, Curtiss-Wright introduced its new high-speed airborne recorder, HSDR-2512, capable of capturing up to 180 TB of flight-test data over a 3‑hour recording period, enhancing data throughput and storage capacity for complex flight-test regimes.

In November 2024, Honeywell International Inc. and Curtiss-Wright jointly launched the Honeywell Connected Recorder‑25 (HCR-25) — a cockpit voice and flight data recorder compliant with the 2024 safety mandate requiring 25‑hour recording capacity for commercial aircraft. (curtisswright.com)

In October 2024, Curtiss-Wright showcased a new range of integrated Flight Test Instrumentation (FTI) solutions — including the high-data-rate module MDAU-1394, advanced telemetry systems, and HD cameras — at the International Telemetry Conference (ITC 2024), underlining increasing demand for end-to-end, high-bandwidth DAQ instrumentation in aerospace testing. (Aviation Defence Universe)

The Aerospace Data Acquisition System Market Report encompasses a comprehensive analysis across multiple dimensions: system types, applications, technologies, regions, and end‑user sectors. It covers all major DAQ product types — including flight-data acquisition units, high-speed data recorders, telemetry gateways, structural/fatigue monitoring instruments, and airborne network modules — offering segmentation by type and associated use‑case environments such as propulsion testing, flight testing, structural evaluation, and environmental simulation. The report evaluates application areas spanning commercial aircraft certification, military flight test instrumentation, UAV and unmanned aerial systems evaluation, satellite launch vehicle testing, and space‑mission telemetry validation.

Geographically, the analysis spans North America, Europe, Asia-Pacific, South America, Middle East & Africa — allowing region-wise comparison of adoption trends, regulatory influences, and regional demand drivers. Technological dimensions include high‑bandwidth fiber‑optic DAQ, cloud‑connected telemetry, edge-computing DAQ modules, AI-enabled analytics platforms, and long-duration flight data recording systems. The report also provides insights into industry focus sectors, including commercial aviation fleet modernization, defense and military aircraft testing programs, aerospace R&D and testing labs, and emerging sectors like electric and hydrogen propulsion, hypersonic aircraft development, and unmanned/spatial aerospace applications. Additionally, niche segments such as space-launch telemetry systems, environmental and structural fatigue monitoring, and retrofit DAQ integration for legacy aircraft are addressed.

By consolidating these segments, the report offers decision‑makers a strategic view of market breadth, technology adoption pathways, end‑user demand patterns, and regional growth potential. It is positioned as a reference tool for stakeholders planning product development, investment, procurement, and long-term aerospace instrumentation strategy.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2626.73 Million |

|

Market Revenue in 2032 |

USD 4031.22 Million |

|

CAGR (2025 - 2032) |

5.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nuvation Engineering, Honeywell, GE Aviation, L3Harris, Danelec Marine, ETMC Technologies, Dewesoft, Curtiss-Wright, Flyht Aerospace Solutions, Teledyne Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |