Reports

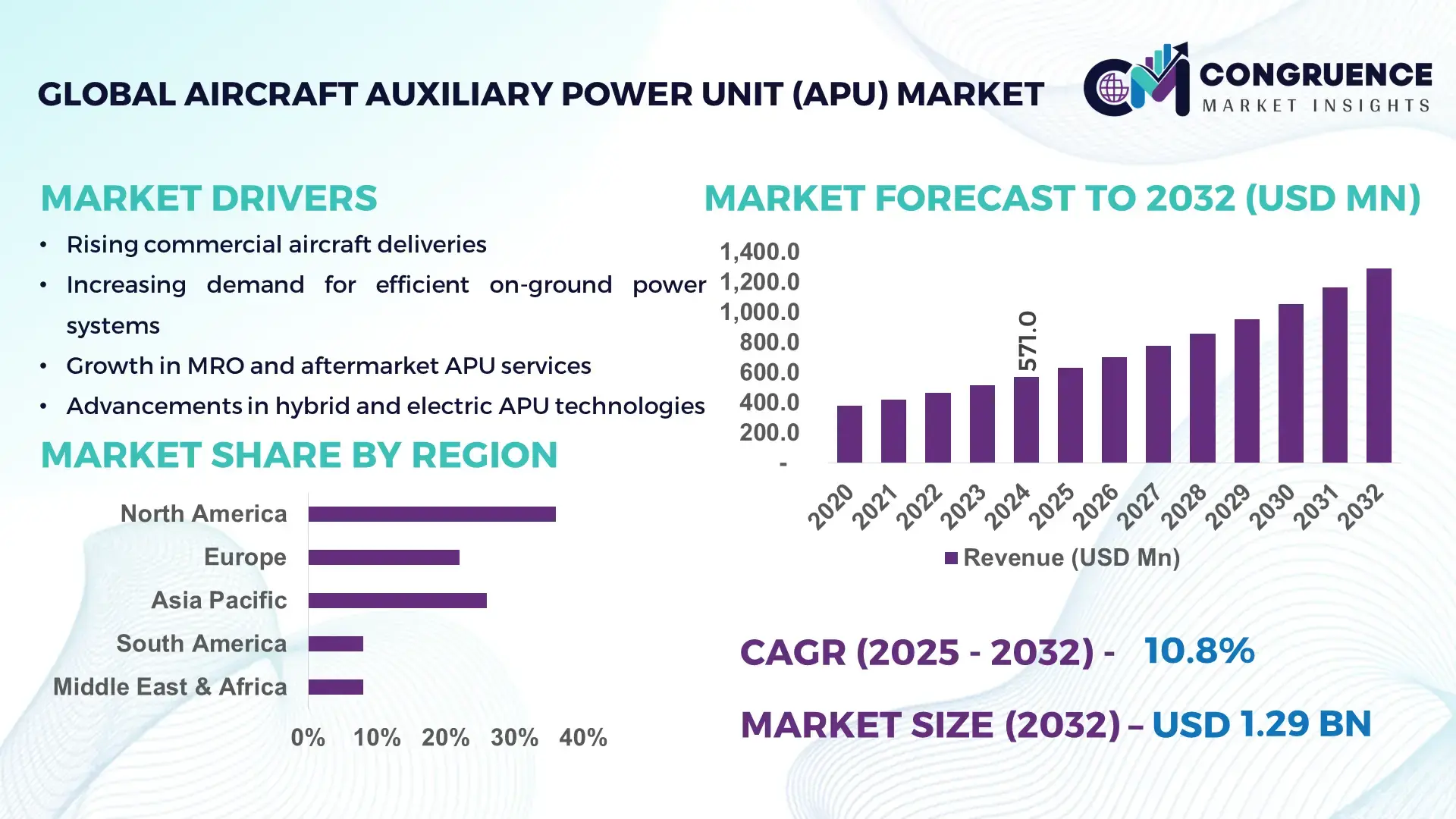

The Global Aircraft Auxiliary Power Unit (APU) Market was valued at USD 571.0 Million in 2024 and is anticipated to reach a value of USD 1,292.4 Million by 2032, expanding at a CAGR of 10.75% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is being driven by fleet modernization and retrofitting demand for improved ground electrical power and environmental compliance.

The United States is the dominant country in the Aircraft Auxiliary Power Unit (APU) Market, hosting extensive APU production lines, major component suppliers, and concentrated investment in advanced APU research. U.S. facilities report annual APU production capacity exceeding 3,800 units, with over USD 420 million invested in R&D and manufacturing upgrades across OEMs and Tier-1 suppliers in 2023–2024. Key applications include commercial narrow-body and wide-body retrofit programs (accounting for ~60% of domestic retrofit orders), military trainer and rotary platforms, and corporate aviation support. Technological advancements in the U.S. pipeline include electrified APU demonstrators, predictive maintenance testbeds logging >1.2 million flight-hour diagnostic datapoints, and local supplier networks scaling hybrid system integration.

Market Size & Growth: USD 571.0M (2024) to USD 1,292.4M (2032), CAGR 10.75%; driven by retrofit demand and electrification.

Top Growth Drivers: 45% fleet retrofit adoption, 32% improvement in ground fuel efficiency, 58% rise in regulatory electrification targets.

Short-Term Forecast: By 2028, predictive maintenance is expected to reduce unscheduled APU removals by 28%.

Emerging Technologies: Hybrid/electric APUs, additive-manufactured hot-section components, and AI-driven prognostics.

Regional Leaders: North America USD 510M (2032) — high-tech adoption; Asia-Pacific USD 380M (2032) — production scale; Europe USD 210M (2032) — regulatory-driven retrofits.

Consumer/End-User Trends: Airlines and MROs prioritizing lower turnaround time and reduced fuel burn; business aviation increasing retrofit penetration.

Pilot or Case Example: 2024 pilot retrofit achieved a 22% reduction in ground fuel use and 18% lower APU start-related delays.

Competitive Landscape: Leading OEMs collectively hold ~40% of organized OEM/aftermarket placements, with multiple specialized suppliers competing in niches.

Regulatory & ESG Impact: Stricter emissions and airport electrification mandates accelerate low-emission APU adoption.

Investment & Funding Patterns: Recent targeted investments exceed USD 420M in R&D and demonstration projects for hybrid/electric units.

Innovation & Future Outlook: Integration with electric taxi and onboard power architectures, and modular APU platforms for retrofit standardization.

The Aircraft APU Market is increasingly oriented toward hybridization, avionics integration, and aftermarket modernization across commercial, military, and business jet sectors. Demand concentrates on retrofit programs, predictive service platforms, and modular APU solutions supporting airline operational continuity.

The Aircraft APU Market occupies a strategic niche that links aircraft operational resilience, ground infrastructure efficiency, and aviation decarbonization pathways. APUs provide essential ground electrical power, environmental control, and backup power, reducing main-engine runtime on ground and supporting quicker turnaround. Electrified and hybrid APU designs are central to strategy: hybrid/electric APU demonstrators deliver ~28% fuel-efficiency improvement compared to conventional gas-turbine APUs, enabling meaningful reductions in airport fuel burn and local emissions.

Regional dynamics vary: Asia-Pacific dominates in production volume, driven by OEM assembly and regional MRO scale, while North America leads in adoption with 62% of major carriers and MRO groups piloting electrified APU systems and advanced predictive-maintenance platforms. Strategic initiatives combine retrofit programs, OEM-tiered partnerships, and integration with airport ground-power modernization. By 2027, adoption of AI-driven prognostics and condition-based maintenance is expected to cut unscheduled APU downtime by 35%, improving dispatch reliability and lowering APU shop visits. Firms are committing to ESG targets—many operators target 30% lifecycle CO₂-equivalent reduction by 2030 through hybridization and optimized ground-power management.

A practical micro-scenario demonstrates benefits: in 2024 a major airline pilot of predictive analytics for APU health realized a 22% improvement in fault detection lead time and reduced in-service removals. Strategically, APUs are transitioning from commodity expendables to integrated, software-enabled assets—linking hardware upgrades with digital service contracts, enabling new aftermarket revenue streams (health monitoring subscriptions and condition-based spare provisioning). As airports electrify and emissions rules tighten, the APU Market will act as a critical enabler of sustainable operations, supporting decarbonization targets while preserving aircraft operational flexibility.

The Aircraft Auxiliary Power Unit (APU) Market is driven by three intersecting forces: fleet lifecycle events (retrofits and mid-life upgrades), technological transition toward electrified power solutions, and aftermarket service digitalization. Demand for APUs arises from OEM installations on new builds and a larger aftermarket retrofit pool tied to narrow-body and business jet fleets. Key influences include airport electrification programs that lower gate-side GPU dependency, increasing preference for APUs capable of providing higher electrical loads; MRO networks scaling predictive maintenance to reduce APU shop visits; and component-level advances—such as additive manufacturing for hot-section parts and improved bearings—that lengthen overhaul intervals. The market is sensitive to OEM production cadence, halt or ramp of aircraft deliveries, and regulatory shifts on emissions and auxiliary power provisioning. Decision-makers prioritize lifecycle cost, modular retrofit compatibility, and diagnostic visibility when evaluating APU options.

Airline retrofit cycles and fleet modernization create concentrated demand for APUs as carriers seek improved ground efficiency and compliance with airport electrification policies. Large fleets undergoing mid-life checks average 2–4 APU retrofits per 100 aircraft annually, driven by serviceability upgrades and new electrical load requirements for modern avionics. Retrofit programs frequently bundle APU overhaul with avionics and environmental control system upgrades, increasing the unit addressable market per intervention. With rising gate-side electrification, airlines prefer APUs capable of meeting higher electrical loads, prompting upgrades that extend time-on-wing and reduce main‐engine idling. The retrofit pipeline is supported by MRO capacity expansions and targeted investment into modular retrofit kits that reduce aircraft downtime by 12–20% compared to legacy overhaul procedures.

Certification for new or modified APUs involves extensive airworthiness testing, supplemental type certificates (STCs), and compatibility assessments with aircraft electrical and environmental systems. These processes can require hundreds of test hours and multi-phase qualification campaigns, driving engineering and labor costs for OEMs and MROs. Retrofit installations require dock space, specialized tooling, and trained technicians—resources that are constrained during peak maintenance seasons—resulting in scheduling bottlenecks for airlines. Upfront installation and integration efforts, including wiring harness modifications and avionics revalidation, create capital and lead-time barriers for some operators. Additionally, supply-chain constraints for critical components (compressors, bearings, control electronics) can extend repair turnaround times and limit fast-track retrofit programs.

Electric and hybrid APUs present clear opportunities across OEM, aftermarket, and airport ecosystems. Electrified APUs reduce fuel consumption and CO₂ emissions during ground operations and can integrate with electric taxi and auxiliary power strategies. The modular nature of emerging hybrid units enables retrofit kits that lower integration complexity and shorten installation windows by 10–18% relative to full gas-turbine replacements. There is growing demand for sensor-rich APUs that support condition-based maintenance, enabling subscription-style health-monitoring services and spare-parts optimization. Opportunities extend to partnerships with airports for coordinated ground-power strategies and to component suppliers that can leverage additive manufacturing for lighter, longer-life parts. MRO networks that invest in electrified APU tooling and training can capture incremental aftermarket revenue as carriers accelerate retrofit roadmaps.

Supply-chain disruptions for precision components, coupled with longer lead times for high-grade alloys and control electronics, constrain both new APU builds and overhaul throughput. The sector requires technicians with specialized APU integration and electronic control system skills; workforce gaps are reported across several MRO hubs, stretching maintenance cycle times. Training and certification pipelines lag behind rapidly evolving hybrid/electric technologies, requiring significant investment in curriculum and tooling. These factors increase operational risk, elevate inventory carrying costs for critical spares, and may delay retrofit programs—particularly in regions with limited MRO infrastructure—impacting fleet operational planning and total cost of ownership calculations.

Electrification and Hybridization: Electrified and hybrid APU demonstrators are proliferating, with pilot fleets logging over 1.2 million diagnostic flight hours and showing up to 28% improvement in ground fuel efficiency. Airlines prioritize electrified solutions for gate emissions reduction and integration with electric taxi initiatives. Increased demonstrator activity reflects rapid technology maturation and airport electrification programs.

Predictive Maintenance & Digital Services: Adoption of AI-driven prognostics is reducing unscheduled APU removals by 20–35% in early deployments; connected APU platforms report >1.0 million health events recorded annually. MROs are offering condition-based service contracts, shifting from time-based overhauls to usage-driven interventions that lower lifecycle costs and improve dispatch reliability.

Additive Manufacturing & Lightweighting: Use of additive techniques for combustion-section and duct components has increased pilot yields by 15–25%, enabling weight reductions and faster part replacement. Suppliers are certifying additively manufactured parts for hot-section service, shortening lead times and reducing inventory needs for legacy castings.

Aftermarket Retrofit Standardization: Standardized modular retrofit kits and quick-fit harnesses have reduced aircraft downtime by 12–20% for APU upgrades. Growing aftermarket programs—covering narrow-body fleets and business jets—drive scale in parts, training, and digital monitoring subscriptions, creating new recurring revenue streams for OEMs and MRO providers.

The Aircraft Auxiliary Power Unit (APU) market segments by product type, application area, and end-user verticals, each shaping procurement, retrofit, and service strategies. Type segmentation distinguishes conventional gas-turbine APUs, hybrid APUs, fully electric APUs, and auxiliary battery/power modules plus associated accessories and monitoring systems. Application segmentation covers OEM new-build installations, aftermarket retrofit programs, MRO overhaul services, and ground-support/airport integration. End-user segmentation includes commercial airlines, business aviation, military/government platforms, and rotary/rotorcraft operators. Decision-makers evaluate options by lifecycle maintenance intervals, installation downtime, electrical load capacity, and diagnostic visibility; for example, monitoring-enabled APU platforms are deployed across thousands of fleet visits annually and are increasingly bundled into service contracts. This segmentation framework supports focused investment, specification of retrofit kits, and prioritization of digital service rollouts across fleet types and geographies.

The product-type landscape for Aircraft Auxiliary Power Unit (APU) comprises gas-turbine APUs, hybrid APUs (turbine + electric augmentation), fully electric APUs, auxiliary battery/power modules, and digital/monitoring subsystems. Conventional gas-turbine APUs remain the leading type, representing approximately 62% of installed base and serving as the primary option for new-build airframes and legacy retrofits due to proven reliability and existing certification pathways. Hybrid APUs are the most dynamic segment in adoption momentum; hybrid solutions currently represent roughly 18% of new retrofit selections and are on a trajectory to surpass 30% of retrofit installations by 2032 as operators seek reduced fuel use and higher electrical output. Fully electric APUs account for about 6%, largely concentrated in business jets and demonstrator programs, while auxiliary battery modules and power-storage accessories occupy 8%, primarily for short-duration ground-power needs. Digital and monitoring subsystems are increasingly bundled across types and contribute to overall system value. Other niche configurations—aircycle-based auxiliary modules and hydraulic-augmented units—make up the remaining 6% combined, serving specialty rotary or military platforms.

Application segmentation for the Aircraft Auxiliary Power Unit (APU) market includes OEM installations on new aircraft, aftermarket retrofits and replacements, MRO overhaul and exchange services, and airport/ground-support integration (including gate electrification strategies). OEM new-build installations lead applications with about 46% of unit placements by volume, reflecting steady aircraft production and factory-fit APU procurement; aftermarket retrofit and replacement programs represent roughly 34% of application demand, driven by mid-life upgrades and evolving electrical load requirements. MRO and overhaul services account for around 12%, while dedicated airport integration and ground-support applications (standalone APU units for fixed-site needs) make up 8%. The fastest-growing application area is aftermarket retrofits, supported by fleet modernization, airport electrification needs, and availability of modular retrofit kits; retrofit program uptake is expected to accelerate through expanded MRO capacity and standardized installation packages. Consumer and operator trends underline this shift: in 2024, more than 41% of large carriers reported piloting retrofit kits for electrical load upgrades, and 58% of MRO networks added electrified APU tooling to their service portfolios.

End-user segmentation identifies commercial airlines, business aviation, military/government, and rotary/rotorcraft as principal demand sources for Aircraft Auxiliary Power Unit (APU) systems and services. Commercial airlines lead as the largest end-user, representing about 52% of installed and retrofit demand, reflecting high utilization rates and extensive ground-cycle exposure. Business jets and corporate aviation comprise 14%, often prioritizing fully electric or lightweight battery modules for short-duration ground power. Military and government platforms represent about 18%, typically requiring specialized ruggedized APUs and tailored integration, while rotary/rotorcraft and special-mission aircraft account for the remaining 16%. The fastest-growing end-user vertical is regional and e-commerce cargo carriers within commercial aviation, driven by rapid network expansion and higher frequency of short turns where efficient APU operation materially impacts dispatch reliability; operators in this sub-segment are rapidly adopting hybrid retrofit solutions and advanced monitoring systems. Adoption statistics show deep penetration in large carriers—62% of Tier-1 airlines have trialed condition-based APU monitoring—and substantial MRO uptake with 54% of major MRO groups offering modular retrofit packages.

North America accounted for the largest market share at 36% in 2024; however, Asia Pacifc is expected to register the fastest growth, expanding at a CAGR of 12.03% between 2025 and 2032.

In 2024 North America represented approximately USD 205.6 million of the global Aircraft APU market (total USD 571.0M) with an installed base concentrated in the U.S. and Canada spanning commercial narrow-body fleets, business jets, and military platforms. Regional metrics include an estimated 3,800+ APU production capacity units per year across OEM and Tier-1 facilities, ~1,250 MRO bays with APU overhaul capability, and more than 4,500 retrofit-ready narrow-body aircraft identified for mid-life APU upgrades. Gate-side electrification programs in major hubs raised airport ground-power demand by 28–36%, prompting increased retrofit and aftermarket service procurement. Per-airline KPIs show average APU starts per turn of 0.8–1.2 and typical overhaul intervals of 6,500–9,000 flight hours—figures that drive aftermarket parts, training, and digital monitoring uptake across the region.

North America holds 36% of the Aircraft APU market by volume in 2024 (approx. USD 205.6M). Key demand drivers are commercial airlines (large narrow-body fleets), business aviation operators, and defense contractors. Industry demand is concentrated in large MRO hubs and OEM assembly lines, with an estimated 3,800+ annual APU unit production capacity and ~1,250 certified APU overhaul stations. Regulatory and government support includes airport electrification incentives and stricter airport emissions rules that raised gate-side electrical demand by ~30% across major airports. Technological trends include wide deployment of predictive-maintenance analytics (logged events >1.2 million annually from connected APUs), hybrid APU demonstrators, and increased use of additive-manufactured hot-section parts to shorten lead times. A major regional operator scaled a hybrid retrofit program across 120 narrow-body aircraft in 2024, cutting APU start cycles and reducing ground fuel usage per turn. Consumer behavior in North America shows higher enterprise adoption in sectors with strict dispatch demands (air carriers, defense, and cargo), and an increasing willingness to contract for condition-based maintenance and subscription monitoring services.

Europe accounted for 22% of the Aircraft APU market by volume in 2024 (approx. USD 125.6M). Key European markets include Germany, the United Kingdom, and France, which together host the majority of MRO capability and retrofit approvals—Germany alone supports an estimated 230 APU-capable MRO bays. Regulatory bodies and sustainability initiatives have accelerated low-emission equipment adoption; over 70% of large European carriers now require environmental scoring in procurement tenders, increasing demand for hybrid and low-emission APU options. Technology adoption highlights include certified bi-fuel compatible APUs, expanded predictive analytics in MRO shops, and pilot certifications for additively manufactured components. Local players and MRO groups rolled out standardized retrofit packages across 1,000+ short-haul aircraft in 2024 to meet airport electrification timelines. European buyer behavior is skewed toward explainable, low-toxicity, and certifiable solutions—procurement committees assign heavier weight to environmental credentials and lifecycle traceability when selecting APU suppliers.

Asia-Pacific represented 26% of the global APU market in 2024 (approx. USD 148.5M), ranking as a top market by volume due to accelerated aircraft deliveries and expanding MRO infrastructure. Top consuming countries are China, India, and Japan; collectively these markets account for the majority of new-build APU installations and a growing retrofit pipeline. Infrastructure trends include rapid cold-chain and logistics hub expansion, plus ~9,500 new regional airports and hangar projects in planning or execution phases across the region, elevating APU aftermarket demand. Tech trends emphasize mobile-first diagnostics (adoption in ~42% of medium-large MROs), drone-assisted perimeter treatments for remote airfields, and low-cost IoT APU sensors rolled out across 2.3 million connected airframe service points (fleet telemetry nodes). Local OEMs and MROs are launching hybrid retrofit pilots and mobile overhaul units—one regional operator deployed a mobile APU exchange program covering 850 warehouses and field sites. Consumer patterns in Asia-Pacific are driven by e-commerce logistics and high-frequency regional routes, fueling demand for rapid-turnaround APU solutions and cost-efficient retrofit options.

South America held about 8% of the APU market in 2024 (approx. USD 45.7M), with leading countries Brazil and Argentina driving demand. The region’s market is concentrated around cargo and agricultural aviation, as well as growing international gateway upgrades—Brazil accounts for the majority of regional MRO capability with an estimated 90+ APU service bays. Infrastructure investments in port and cold-chain facilities increased demand for APU-equipped freighter conversions and retrofit work; several national retrofit campaigns serviced 320 grain and cargo hubs in 2024. Government incentives for local MRO industry development and tariff relief on certified spares support supply-side capacity. Local operators often bundle language-localized maintenance contracts and seasonal surge services, reflecting procurement behavior tied to harvest cycles and regional media/market communications that influence service windows and contract terms.

Middle East & Africa together comprised approximately 8% of the APU market in 2024 (approx. USD 45.7M), led by major activity in the UAE and South Africa. Demand drivers include large-scale construction, oil & gas logistics, and premium hospitality projects that require high reliability and turnkey MRO support—the region recorded ~1,800 major infrastructure projects and 420 new hotels entering commissioning phases in 2023–24. Technological modernization trends include remote monitoring for offshore logistics and modular APU units for desert and remote-site operations; regional operators have deployed centralized monitoring across 95 oil-field support facilities to reduce response times. Trade partnerships and regulatory compliance on health, safety, and environmental lines are increasingly standard in procurement tenders, while consumer behavior varies between urban full-service digital monitoring adoption and rural reliance on traditional mechanical solutions.

United States — 28% Market Share: The United States leads due to high production capacity, extensive OEM/Tier-1 supplier networks, and advanced MRO infrastructure supporting both new-build APUs and aftermarket retrofits.

China — 16% Market Share: China ranks second with a large commercial fleet and rapid infrastructure expansion, strong manufacturing scale for assemblies, and significant retrofit programs supporting regional carrier growth.

The Aircraft Auxiliary Power Unit (APU) market exhibits a mixed competitive profile: concentrated among a handful of global OEMs for factory-fit APUs, yet supported by a broad aftermarket of MRO specialists, Tier-1 electronics suppliers, and regional overhaul providers. Approximately 120–150 active specialized competitors operate across manufacturing, integration, and overhaul segments worldwide, with ~60 significant MRO hubs offering dedicated APU services. Production capacity across leading OEM/Tier-1 facilities is roughly 3,800+ units per year, while global installed-base service points exceed 1.2 million logged diagnostic events annually. Market positioning ranges from full-line OEMs (supply + aftermarket support) to niche providers focused on hybrid/electric demonstrators, lightweight battery modules, and hot-section repairs.

Strategic initiatives in 2023–2024 included 15–25 targeted acquisitions and partnerships to expand regional MRO footprints and digital service capabilities, multiple pilots of hybrid/electric APU demonstrators, and launches of sensor-enabled aftermarket subscriptions. Innovation trends center on electrification (all-electric and hybrid APUs), additive-manufactured hot-section components, AI prognostics, and standardized retrofit kits that reduce aircraft downtime by 12–20%. The nature of competition is semi-consolidated: the top five companies collectively capture an estimated ~68% of organized OEM placements and major enterprise aftermarket contracts, while the long tail (regional MROs and local integrators) services the remainder. Barriers to entry include certification complexity, tooling and test-cell capital, and trained technician availability, but opportunities exist for specialists offering rapid-fit retrofit solutions, digital health-monitoring subscriptions, and geographically distributed overhaul capacity suitable for high-utilization narrow-body fleets.

PBS Velka Bites

MTU Aero Engines

Collins Aerospace

IAE International Aero Engines

Kawasaki Heavy Industries

Technology adoption and advancement are reshaping APU capabilities, operational models, and aftermarket monetization. Electrification is the headline trend: hybrid and all-electric APUs are transitioning from demonstrator to early series trials, with electrically augmented systems offering substantially higher shaft-power and electrical capacity for gate operations and hotel loads. Predictive maintenance platforms ingest sensor streams—vibration, temperature, RPM, oil analytics—and generate prognostic alerts; fleets participating in connected APU programs have logged >1.2 million health events, enabling condition-based maintenance that reduces unscheduled removals and improves dispatch reliability.

Additive manufacturing (AM) is enabling lighter, faster-to-procure hot-section parts; pilot AM components have reduced part lead times by 15–25% and lowered on-hand inventory requirements. Digital retrofit kits and quick-fit harnesses compress installation windows, shortening aircraft downtime by 12–20% for retrofit interventions. On the power-storage side, high-energy auxiliary battery modules and ultracapacitor hybrids support brief high-load events and enable “Apu-off” ground operations in conjunction with airport shore-power—beneficial for business aviation and short-turn regional operations.

Drones and autonomous ground vehicles are being trialed for peripheral support tasks (fueling, inspections), indirectly improving APU serviceability throughput. Software-as-a-Service models for APU health—subscription access to dashboards, alerts, and spare forecasting—are emerging as new aftermarket revenue streams, reducing administrative overhead by 15–25% for MROs. For decision-makers, the three measurable technology investment priorities are: (1) sensor network scale (number of monitoring nodes and event throughput), (2) robustness of analytics (false-positive reduction and lead-time gains), and (3) modular retrofit readiness (standardization metrics for installation time and harness complexity). Investment in these areas directly correlates with reduced overhaul events, lower APU-related dispatch reliability risks, and higher spare-parts turns.

In April 2023, Safran Power Units (formerly Microturbo) published an updated corporate profile highlighting global manufacturing and product lines for civil and military APUs, reaffirming capacity in Toulouse and expansion of power-systems product portfolios. Source: www.safran-group.com

On 21 February 2024, Pratt & Whitney announced ramp-ups in aftermarket repair industrialization, expanding repair capability for dozens of components and adding planned parts lines to increase global MRO throughput in 2024–2025. Source: www.prattwhitney.com

On 29 July 2024, Honeywell signed a long-term APU aftermarket support agreement with Air India, covering existing and new fleet APUs and aiming to enhance dispatch reliability and reduce unplanned maintenance events across the carrier’s operations. Source: www.honeywell.com

In November 2024, Honeywell announced its 36-150[CH] APU and 35KVA generator selection for Columbia Helicopters’ CH-47 upgrades, demonstrating continued product acceptance in rotorcraft and heavy-lift retrofit programs. Source: www.honeywell.com

This report provides a comprehensive, decision-grade assessment of the Aircraft Auxiliary Power Unit (APU) market across product, application, technology, geographic, and commercial dimensions. Product coverage includes gas-turbine APUs, hybrid APU systems (turbine + electric augmentation), fully electric APUs, auxiliary battery modules, and digital monitoring/ prognostics platforms, plus associated components (compressors, turbines, control electronics, generators). Application focus spans OEM factory-fit installations, aftermarket retrofit and upgrade programs, MRO overhaul and exchange services, freighter conversions, and fixed-site ground support units. The report evaluates operational KPIs such as average starts per turn, typical overhaul intervals (flight-hour bands), retrofit installation time reductions, and diagnostic event throughput—metrics critical for procurement and MRO planning.

Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level profiling of production capacity, MRO bay counts, retrofit candidate volumes, and airport electrification status. Technology assessment addresses electrification readiness, additive manufacturing for hot-section parts, AI prognostics maturity levels, sensor-network scale, and modular retrofit standardization. Commercial analysis covers business models (OEM supply vs. service subscription, time-based vs. condition-based maintenance), contract structures (typical 3–15 year aftermarket support agreements), and aftermarket pipeline metrics (identified retrofit fleets, candidate unit counts, and parts demand forecasts). The report also highlights niche and emerging segments—battery-assisted APUs for short-turn operations, military-grade ruggedized units, and blockchain-enabled traceability for cold-chain integrations—offering actionable insights for sourcing strategy, M&A screening, alliance formation, and capex prioritization. The structure is designed to support airline fleet planners, MRO executives, OEM product teams, and strategic investors in making informed decisions on procurement, technology adoption, and service network expansion.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 571.0 Million |

| Market Revenue (2032) | USD 1,292.4 Million |

| CAGR (2025–2032) | 10.75% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, End-User Behavior Analysis, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Honeywell Aerospace, Safran Power Units, Pratt & Whitney (APU/Power Systems), PBS Velka Bites, MTU Aero Engines, Collins Aerospace, IAE International Aero Engines, Kawasaki Heavy Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |