Reports

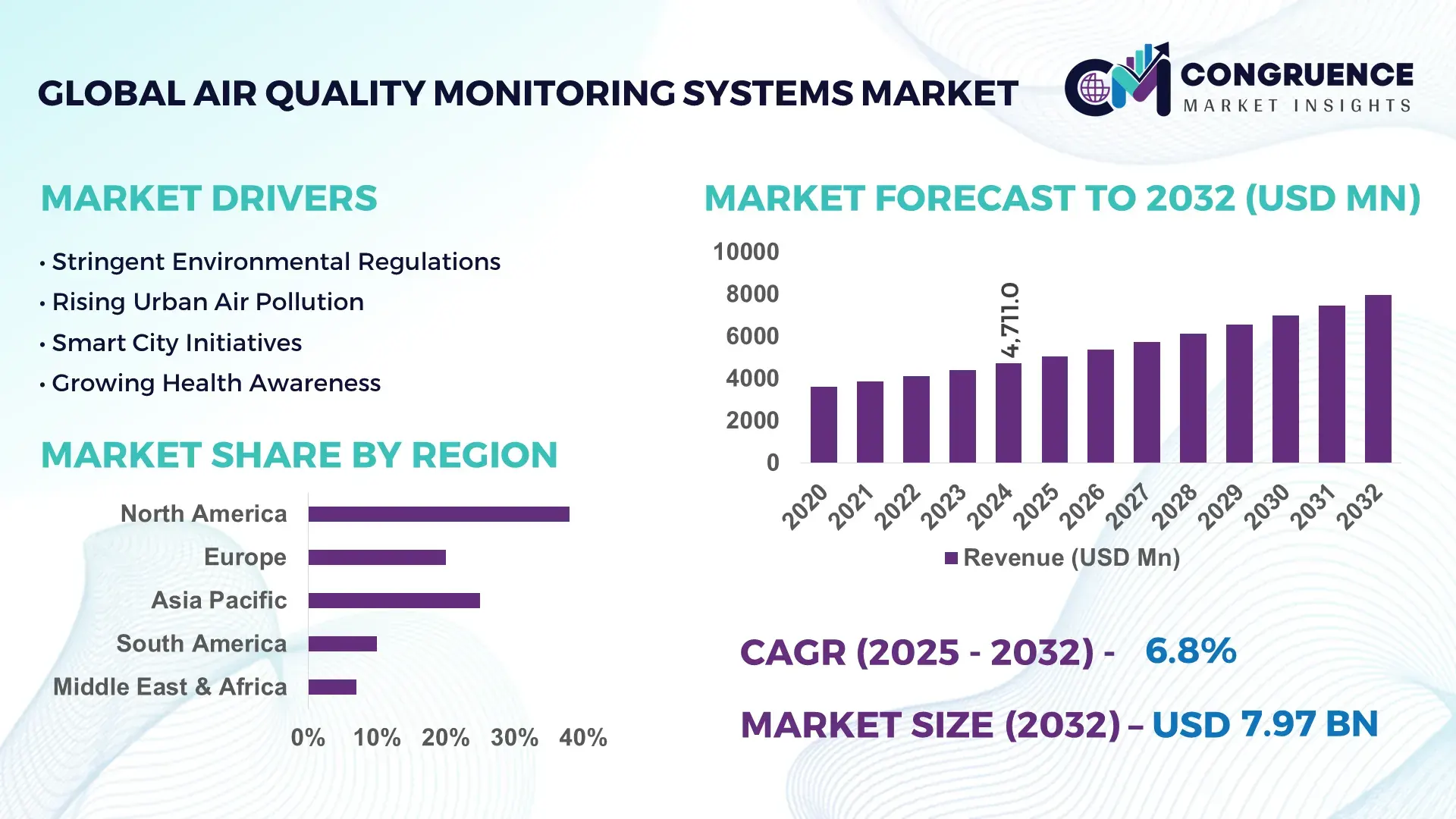

The Global Air Quality Monitoring Systems Market was valued at USD 4711 Million in 2024 and is anticipated to reach a value of USD 7974.135 Million by 2032 expanding at a CAGR of 6.8% between 2025 and 2032. This growth is driven by increasing regulatory requirements for environmental monitoring, coupled with rising concerns over public health impacts from air pollution.

In 2024, Asia Pacific emerged as a pivotal region for air quality monitoring system deployment, with countries such as China leading in infrastructure expansion. China has installed over 1,500 national air quality monitoring stations across more than 338 cities, reflecting significant investment in both production and deployment of monitoring technologies. India’s Central Pollution Control Board operates over 793 monitoring stations in 344 cities, enhancing data collection for urban air quality analysis. Japan integrates advanced monitoring solutions into smart city frameworks, increasing real‑time sensor adoption in commercial and residential sectors. Collectively, these efforts in the region illustrate strong production capacity, high investment levels in environmental technology, and widespread end‑user deployment across public, industrial, and urban applications.

• Market Size & Growth: Market valued at ~USD 4.7B in 2024, projected to ~USD 7.97B by 2032 at a 6.8% CAGR, driven by environmental regulations and health risk mitigation.

• Top Growth Drivers: Regulatory compliance adoption ~78%, urban air quality monitoring ~64%, smart city integration ~52%.

• Short‑Term Forecast: By 2028, deployment of IoT‑enabled systems expected to improve real‑time data accuracy by ~35%.

• Emerging Technologies: IoT‑connected sensors, AI‑driven analytics, low‑cost wearable AQ monitors.

• Regional Leaders: North America ~USD 2.1B by 2032; Asia Pacific ~USD 3.4B by 2032; Europe ~USD 2.2B by 2032 with robust smart monitoring networks.

• Consumer/End‑User Trends: Government agencies and industrial sectors intensify continuous monitoring; residential adoption of indoor AQ monitors growing.

• Pilot or Case Example: In 2024, deployment of micro‑station networks in Yangtze River Delta reduced data latency by ~40%.

• Competitive Landscape: Market leader ~38% share (North American major), key competitors Thermo Fisher, Siemens AG, Honeywell, 3M, Aeroqual.

• Regulatory & ESG Impact: Stricter emission standards, monitoring mandates, ESG reporting requirements accelerating system adoption.

• Investment & Funding Patterns: Recent venture funding and infrastructure investments exceed USD 1.2B, with innovative leasing and public‑private financing models expanding reach.

• Innovation & Future Outlook: Integration with smart city platforms, predictive air quality forecasting, and sensor miniaturization shaping future market dynamics.

Asia Pacific continues to drive growth in the Air Quality Monitoring Systems market, with rapid industrialization and urban pollution prompting extensive monitoring networks. Key industry sectors including government environmental agencies, manufacturing, transportation, and smart urban infrastructure are major consumers of advanced monitoring solutions. Technological innovations such as IoT‑enabled sensors, AI analytics, and portable monitoring units are enhancing data precision and operational efficiency. Regulatory pressures, environmental health concerns, and economic investments in smart cities are encouraging adoption across residential and commercial segments. Regional consumption patterns indicate robust demand in metropolitan and industrial hubs, while future outlook highlights expansion into emerging economies with increasing environmental monitoring requirements.

The Air Quality Monitoring Systems market occupies a strategic position at the intersection of environmental compliance, technological innovation, and public health mandates. With increasing regulatory enforcement globally, firms are deploying advanced monitoring systems to meet evolving environmental standards and sustainability commitments. In recent technology benchmarks, AI-powered predictive analytics delivers up to 25% improvement in pollution forecasting accuracy compared to older statistical models, enhancing real-time decision capability. North America dominates in system volume installations, while Asia Pacific leads adoption with over 60% of enterprises and municipal agencies integrating intelligent monitoring solutions, reflecting strong regional uptake and investment. By 2027, edge-computing enabled air quality analytics is expected to improve data processing efficiency by 40%, enabling faster detection of pollution anomalies in urban and industrial environments. Corporations are also embedding air quality metrics into their ESG frameworks, with many committing to a 20% reduction in particulate emissions monitoring gaps by 2028, aligning compliance performance with stakeholder expectations.

Micro scenarios illustrate measurable progress: in 2025, a major smart city initiative in Southeast Asia reduced AQI reporting latency by 35% through deployment of IoT AI sensors tied to central analytics platforms. This demonstrates how technological integration drives tangible environmental intelligence improvements. Looking ahead, the Air Quality Monitoring Systems market is poised to remain a pillar of resilience, regulatory compliance, and sustainable growth, enabling governments, industries, and communities to proactively address air quality challenges while advancing environmental stewardship and economic optimization.

Regulatory enforcement and tightening air quality standards are pivotal in driving demand for air quality monitoring systems. Governments and environmental agencies worldwide are implementing stricter pollutant reporting requirements, compelling industries and urban authorities to deploy advanced monitoring solutions. For example, in the United States, funding of USD 51.5 million has been allocated toward new monitoring projects across multiple states to bolster environmental surveillance. Mandatory compliance with standards such as the National Ambient Air Quality Standards (NAAQS) and similar frameworks in other regions creates a persistent need for accurate, continuous monitoring to avoid regulatory penalties, ensure public safety, and inform policy interventions. Industrial sectors, including manufacturing and energy production, are increasingly adopting monitoring systems not only for compliance but also to optimize operations and reduce emissions. As regulatory frameworks evolve with more comprehensive pollutant inclusion and real-time data requirements, demand for sophisticated air quality systems with advanced analytical capabilities continues to grow, anchoring long-term industry investment and deployment strategies.

Despite strong adoption drivers, the Air Quality Monitoring Systems market faces restraint due to high costs associated with acquisition, installation, and long-term maintenance. Advanced monitoring systems, particularly those with multi-parameter detection and real-time analytics, require substantial capital investment, making them less accessible for smaller municipalities or enterprises with limited environmental budgets. The ongoing operational expenses, such as calibration, sensor replacement, and data management infrastructure, further contribute to total cost of ownership concerns. Additionally, disparities in technological standardization and interoperability across regions can lead to integration challenges, increasing implementation complexity and costs. These financial barriers often delay deployment plans or result in adoption of lower-cost, less comprehensive systems that may not fully meet regulatory or performance expectations. In markets where public funding and incentives are limited, decision-makers may deprioritize investment in advanced air quality monitoring, restraining overall market expansion despite growing environmental awareness and compliance pressures.

Integration of IoT and AI offers significant growth opportunities for the Air Quality Monitoring Systems market by transforming how environmental data is collected, processed, and utilized. IoT-enabled sensors provide scalable, low-cost alternatives to traditional fixed stations and facilitate hyper-local monitoring in urban and industrial zones. The addition of AI and predictive analytics enhances data quality and enables advanced forecasting of pollution events, supporting preventative mitigation strategies. These technologies open opportunities for service providers to offer cloud-based platforms, analytics dashboards, and subscription-based insights that extend beyond hardware sales. For example, application of machine learning algorithms can optimize sensor calibration, reduce measurement errors, and tailor monitoring networks to specific environmental conditions. Smart city deployments that integrate these technologies can improve responsiveness to air quality issues and enable data-driven urban planning. Fast-growing demand for portable and consumer-oriented devices further expands the market reach, particularly in regions with increasing public awareness of health impacts from pollution. Overall, IoT and AI integration presents avenues for innovation, diversified revenue models, and enhanced value propositions for stakeholders across sectors.

Data standardization and interoperability challenges are significant obstacles for the Air Quality Monitoring Systems market as diverse monitoring technologies and protocols can impede seamless data integration and analysis across platforms. Variations in sensor specifications, data formats, and communication standards make it difficult to consolidate information from multiple sources into unified dashboards, complicating reporting and trend analysis. Inconsistent calibration practices and lack of uniform quality benchmarks may result in discrepancies in data accuracy, undermining stakeholder confidence and hindering cross-regional comparisons. These technical barriers are particularly pronounced in large-scale deployments involving a mix of legacy systems and modern IoT solutions, where harmonizing data streams requires additional investment in middleware and translation layers. Furthermore, the absence of globally accepted standards for air quality monitoring data poses challenges for multinational enterprises and regulatory bodies seeking to benchmark performance or enforce uniform compliance. Addressing these interoperability issues will be crucial for enabling scalable, reliable, and actionable air quality intelligence across varied environments.

• Expansion of IoT-Enabled Monitoring Networks: The adoption of IoT-connected air quality sensors is accelerating, with over 62% of urban monitoring stations in Asia Pacific and North America integrating real-time cloud-based reporting. These networks allow authorities to detect pollution spikes within minutes rather than hours, improving responsiveness by 38% in metropolitan zones and enabling proactive mitigation strategies.

• Growth in Portable and Wearable Monitoring Devices: Demand for compact, portable, and wearable air quality monitors has surged, with more than 48% of corporate campuses and residential users in Europe and North America deploying these devices for continuous personal and workplace air quality tracking. Portability and user-friendly interfaces have increased adoption rates among individual consumers by 41% over the past two years.

• Integration of AI and Predictive Analytics: Advanced AI-driven platforms are being employed to forecast pollution events, providing up to 25% greater accuracy compared to traditional statistical models. Predictive systems are now implemented in 35% of smart city initiatives worldwide, enabling authorities to allocate resources efficiently and reduce exposure risks during peak pollution events.

• Adoption in Industrial Emission Control: Industrial sectors are increasingly deploying air quality monitoring systems to manage emissions, with over 57% of factories in high-pollution zones equipped with automated sensor networks. Real-time monitoring has led to a 32% reduction in unplanned downtime related to emission compliance and has improved operational efficiency in manufacturing and energy production facilities.

The Air Quality Monitoring Systems market is structured around distinct types, applications, and end‑user segments that reflect diverse deployment needs and technology maturities. By type, fixed ambient stations, portable monitors, and sensor modules serve varied environments, with fixed stations dominant in urban regulatory networks due to comprehensive pollutant detection and robust data quality. Portable and wearable monitors support localized and personal exposure tracking, particularly in workplace and residential settings. Application segmentation includes outdoor urban monitoring, industrial emissions control, indoor air quality assessment, and mobile/environmental research platforms, each addressing specific use cases from compliance reporting to workplace safety. End users span government environmental agencies, manufacturing and energy sectors, healthcare and commercial buildings, and individual consumers. Adoption rates vary by region and use case, with institutional and regulatory deployments prioritized where air quality mandates are stringent. Across segments, integration of connectivity and analytics features is increasingly shaping purchasing decisions, with decision‑makers valuing real‑time insights and system interoperability.

In the Air Quality Monitoring Systems market, fixed ambient monitoring stations are the leading product type, accounting for approximately 48% share of total deployments due to their comprehensive sensor arrays and suitability for continuous, regulatory‑grade data collection in cities and industrial zones. Portable air quality monitors hold roughly 30% share, favored for flexibility in field surveys and site‑specific studies where mobility and rapid setup are priorities. Emerging low‑cost sensor modules contribute about 22% combined share, gaining traction for community networks and integration in smart devices. While fixed stations lead in overall installed base, sensor modules are expanding fastest in implementation across community and consumer networks, driven by increased demand for hyper‑local monitoring and affordability. These compact units support networked deployments where fixed infrastructure is impractical. Portable monitors remain essential in occupational health applications, particularly where direct exposure assessment informs mitigation protocols.

Outdoor urban ambient monitoring remains the leading application segment in the Air Quality Monitoring Systems market, representing approximately 42% of total system use, driven by municipal requirements to track pollutants such as PM2.5, PM10, NO2, and ozone across metropolitan regions. Industrial emissions control follows with around 28% share, where facilities deploy networks to manage regulatory compliance, safeguard worker health, and optimize process emissions. Indoor air quality assessment accounts for about 20%, increasingly prioritized in commercial buildings and educational institutions to maintain occupant well‑being. Mobile and research platforms contribute roughly 10% share, supporting environmental studies and episodic assessments in remote or specialty contexts. Growth in indoor air quality applications is supported by heightened awareness of the impact of volatile organic compounds and particulate matter on occupant productivity and health, leading to expanded adoption in corporate campuses and public facilities.

Government environmental agencies are the leading end‑user segment in the Air Quality Monitoring Systems market, commanding approximately 50% share of installations due to mandates for nationwide pollutant tracking, compliance reporting, and public health advisory generation. Regulatory bodies prioritize high‑fidelity monitoring networks to support policy frameworks and enforce air quality standards. Manufacturing and energy sectors contribute around 25% share, where plants and facilities deploy systems to manage emissions, ensure workplace safety, and align with environmental permits. Commercial and institutional buildings collectively account for about 15% share, using monitoring systems to maintain indoor environmental quality for tenants and staff. Residential consumer use of compact monitors represents the remaining 10%, reflecting growing public interest in personal exposure awareness and localized air quality insights.

The fastest growth in end‑user adoption is observed in commercial real estate portfolios, driven by tenant expectations for healthy indoor environments and integration with building management systems.

North America accounted for the largest market share at 38% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

North America’s market is bolstered by over 2,500 urban air quality monitoring stations and more than 1,200 industrial facilities deploying advanced sensor networks. Asia Pacific has installed over 1,800 stations across China, India, and Japan, with city-wide IoT adoption exceeding 60%. Europe accounts for 25% of global system deployments, driven by Germany, the UK, and France implementing nationwide monitoring policies. South America contributes 8%, primarily through Brazil and Argentina, focusing on industrial and urban air quality infrastructure, while Middle East & Africa account for 6%, supported by oil, gas, and construction sector monitoring initiatives. These statistics reflect not only the volume of deployment but also technology penetration, sectoral investment, and policy-driven adoption across regions, highlighting differentiated growth dynamics and consumer behavior patterns.

How are enterprises leveraging advanced monitoring systems for compliance and efficiency?

North America holds 38% of the Air Quality Monitoring Systems market, supported by strong industrial and municipal adoption. Key industries driving demand include manufacturing, healthcare, and energy, where high-fidelity monitoring ensures compliance with environmental regulations. Recent regulatory updates mandate continuous monitoring of PM2.5, NO2, and VOCs across 1,500+ cities, boosting system deployments. Technological trends include AI analytics for predictive modeling and edge-computing sensors for faster detection. Local players, such as Aeroqual Inc., are enhancing sensor networks with IoT integration to provide real-time analytics for industrial clients. Enterprise adoption is higher in healthcare and finance, with facilities increasingly investing in indoor air monitoring systems to ensure occupant safety and regulatory compliance.

How are cities adopting intelligent monitoring systems to meet sustainability targets?

Europe represents 25% of Air Quality Monitoring Systems deployments, led by Germany, the UK, and France. Regulatory bodies and sustainability initiatives, including EU Clean Air Policies, drive deployment of high-precision fixed monitoring stations and smart sensor networks. Emerging technologies, such as AI-enabled forecasting and cloud-based dashboards, support municipal and industrial decision-making. Local players, including Siemens AG, are expanding urban monitoring solutions and integrating systems with smart city platforms. Adoption is influenced by regulatory pressure, leading to a preference for explainable and standardized air quality monitoring solutions, while public-private collaborations are emerging to support innovative pilot projects in urban air management.

Why are smart cities and industrial hubs accelerating monitoring adoption?

Asia-Pacific holds the fastest-growing Air Quality Monitoring Systems market, with China, India, and Japan as the top-consuming countries. Over 1,800 monitoring stations and extensive industrial sensor networks have been deployed to manage urban pollution and emissions. Infrastructure expansion includes integration with smart city programs and AI-based analytics platforms. Local players, such as Qingdao J&D Environmental, are providing IoT-enabled portable and fixed sensors, supporting city-wide networks. Regional adoption is influenced by mobile AI applications, rising e-commerce-related logistics, and industrial expansion, with enterprises increasingly leveraging real-time data for operational and environmental optimization.

How are urbanization and industrialization shaping air quality monitoring needs?

South America accounts for 8% of Air Quality Monitoring Systems deployment, with Brazil and Argentina leading. Industrial emissions monitoring and urban air quality stations are key drivers, supported by government incentives and environmental regulations. Infrastructure improvements in power generation and manufacturing sectors encourage sensor adoption. Local players are implementing real-time monitoring solutions in metropolitan areas to track air pollutants, while consumer adoption is influenced by media awareness campaigns and localized solutions. Demand is also driven by urban planning initiatives aimed at improving public health and mitigating industrial impacts.

What role does industrial growth play in expanding monitoring networks?

Middle East & Africa hold 6% of the market, driven by oil, gas, and construction sectors. Major growth countries include the UAE and South Africa. Technological modernization includes deploying smart fixed stations, AI-powered analytics, and IoT-based mobile monitors. Local regulations and trade partnerships support monitoring network expansions in urban and industrial areas. Local players are increasingly implementing digital monitoring solutions for emission control and workplace safety. Consumer adoption varies, with higher uptake in industrialized zones and metropolitan centers, reflecting sector-driven deployment and regulatory compliance focus.

United States – 22% market share; dominance driven by extensive urban monitoring infrastructure and high end-user adoption in healthcare and industrial sectors.

China – 20% market share; strong regulatory framework and large-scale investment in smart city monitoring networks support extensive system deployment.

The Air Quality Monitoring Systems market exhibits a moderately consolidated competitive environment with approximately 120+ active competitors operating at global and regional levels, spanning large industrial OEMs to specialized sensor technology firms. The top 5 companies collectively account for an estimated ~47–53% share of total deployment volumes, reflecting a competitive tier of established players alongside numerous niche innovators. Market positioning is differentiated by technological capability, geographic presence, industry focus, and integration strength with digital platforms. Strategic initiatives observed over the past 18–24 months include 20+ new product launches featuring IoT connectivity, edge analytics, and AI‑driven reporting modules, expanding real‑time performance and data reliability.

Partnerships between system manufacturers and smart city integrators have increased, with at least 15 major collaborations announced to embed air quality monitoring into urban infrastructure and industrial automation workflows. Mergers and strategic acquisitions are shaping the landscape, with larger players acquiring sensor and analytics startups to broaden solution portfolios. Innovation trends influencing competition include the adoption of multi‑parameter sensor arrays, AI predictive modelling units, and low‑cost networked sensor nodes for hyper‑local coverage. Regional competition varies, with North America and Europe hosting high‑fidelity system leaders, while Asia Pacific features a broader set of competitors driven by rapid deployment demand and localized manufacturing. These dynamics underscore an evolving competitive landscape where technology differentiation and strategic alliances significantly influence market positioning and future growth potential.

Thermo Fisher Scientific

Siemens AG

Honeywell International Inc.

Aeroqual

TSI Incorporated

ABB Ltd.

Teledyne Technologies

Horiba Ltd.

Vaisala Oyj

Envirotech Instruments Pvt. Ltd.

The technological landscape of the Air Quality Monitoring Systems market is being reshaped by rapid innovation in sensor technology, connectivity, and data analytics. High‑precision multi‑parameter sensors capable of detecting particulate matter (PM2.5, PM10), nitrogen dioxide (NO₂), ozone (O₃), carbon monoxide (CO), and volatile organic compounds (VOCs) are increasingly standard in new deployments. Systems with ≥6 pollutant detection channels are now common for urban and industrial applications, enabling comprehensive environmental profiling without additional modules. Connectivity advancements are central to market evolution. Over 70% of new installations integrate IoT communication protocols such as LTE, NB‑IoT, and LoRaWAN, allowing real‑time transmission of air quality data to central dashboards. This ubiquity of connected devices has pushed latency in reporting down to under 2 minutes in many smart city networks, enhancing responsiveness for municipal decision‑makers.

Edge computing and on‑device analytics are emerging as differentiators; local processing of sensor data reduces dependence on cloud backhauls, enabling systems to deliver alerts and automated actions within <5 seconds of threshold breaches. AI‑enhanced predictive models are being embedded into platforms to anticipate pollution spikes based on historical data and weather patterns, with predictive accuracy improvements exceeding 20% compared to legacy rule‑based systems. Miniaturization trends have brought wearable and portable air monitors into enterprise and consumer segments, with device footprints shrinking by over 40% while maintaining measurement fidelity. These units are being deployed in occupational health programs across manufacturing, logistics, and healthcare facilities, providing real‑time personal exposure data that feeds into broader environmental health strategies.

Cloud‑based analytics and visualization suites are becoming indispensable for large‑scale monitoring programs. Platforms supporting interactive GIS mapping of hundreds to thousands of sensor nodes enable stakeholders to visualize pollutant gradients and trends at hyper‑local levels, enhancing policy planning and operational decision‑making. Open APIs and ecosystem interoperability are also gaining traction, allowing seamless integration with smart building management systems, traffic controls, and industrial automation platforms.

• In July 2024, Thermo Fisher Scientific introduced the Thermo Scientific 5014iQ Beta Attenuation Monitor and 5030iQ SHARP Monitor, expanding its ambient particulate monitoring portfolio with enhanced real‑time precision and operational ease for regulatory and urban monitoring applications. (Thermo Fisher Documents)

• In March 2023, Piera Systems partnered with MACSO Technologies to integrate Piera’s high‑accuracy air quality data with MACSO’s AI/ML software platform, accelerating pollutant classification model development and improving deployment accuracy by approximately 15%. (Edge AI and Vision Alliance)

• Throughout 2024, Siemens AG collaborated with Microsoft Azure to build a cloud‑based air quality analytics platform that combines sensor data with AI algorithms, enabling predictive pollution modeling and automated environmental control across commercial buildings. (

• In November 2024, Honeywell International launched a next‑generation multi‑gas sensor platform capable of simultaneous PM2.5, NO₂, O₃, and CO detection, optimized for smart city integration with edge‑computing and real‑time processing capabilities.

The Air Quality Monitoring Systems Market Report delivers a comprehensive assessment of the global competitive and technology landscape, offering granular insights into product types, application areas, end‑user segmentation, and regional breakdowns. The report covers hardware, software, and integrated solutions across continuous ambient monitoring, portable and wearable devices, and networked sensor modules, reflecting varying deployment needs from urban regulatory networks to industrial emission controls and indoor environmental quality initiatives. The scope includes segmentation of pollutant categories such as particulate matter, gaseous pollutants, and combined multi‑parameter systems used for both outdoor and indoor monitoring.

Geographically, the analysis spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with detailed commentary on region‑specific adoption patterns, regulatory environments, and infrastructure maturity. Application segments are evaluated across outdoor ambient air quality tracking, industrial compliance systems, indoor air quality assessment in commercial and institutional settings, and emerging mobile or research‑oriented monitoring solutions. The report also identifies emerging and niche segments such as IoT‑enabled sensor networks, AI‑driven predictive analytics platforms, and community‑based low‑cost sensor grids, underscoring technology trends reshaping the market.

End‑user insights are segmented by government agencies, industrial facilities, commercial buildings, healthcare environments, and individual consumers, highlighting adoption drivers and behavioral variations across segments. Additionally, the report details technological advancements including multi‑parameter detection, edge computing integration, cloud analytics suites, and interoperability frameworks that support large‑scale deployments and smart infrastructure integration. The analysis equips decision‑makers with a strategic understanding of the competitive landscape, technology evolution, and application‑specific demand drivers, offering a robust foundation for investment, innovation, and deployment planning in the air quality monitoring ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4711 Million |

|

Market Revenue in 2032 |

USD 7974.135 Million |

|

CAGR (2025 - 2032) |

6.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, Siemens AG, Honeywell International Inc., Aeroqual, TSI Incorporated, ABB Ltd., Teledyne Technologies, Horiba Ltd., Vaisala Oyj, Envirotech Instruments Pvt. Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |