Reports

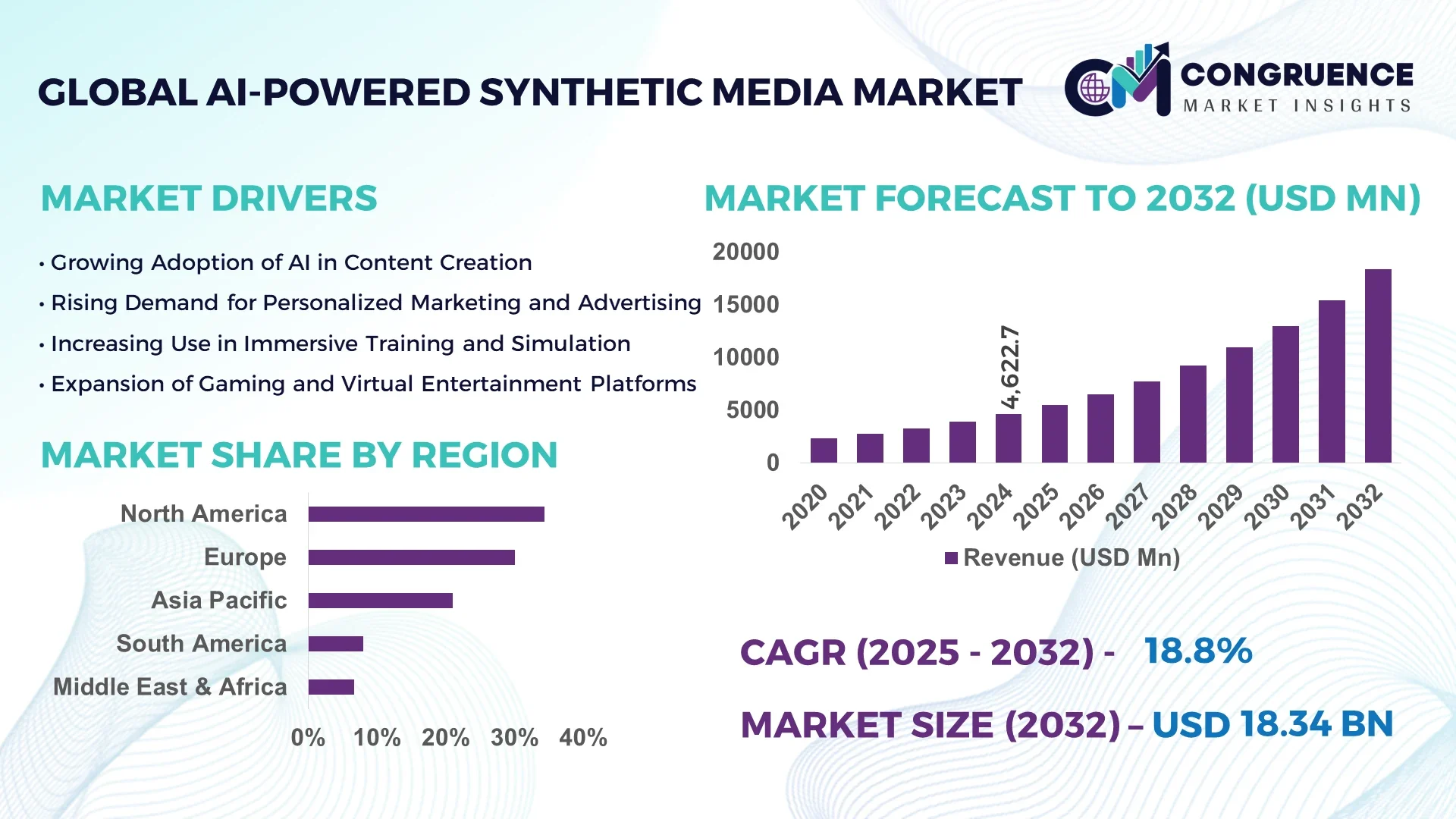

The Global AI-Powered Synthetic Media Market was valued at USD 4,622.7 Million in 2024 and is anticipated to reach a value of USD 18,341.2 Million by 2032 expanding at a CAGR of 18.8% between 2025 and 2032. This growth is driven by accelerating demand for generative AI tools in content creation and immersive digital experiences.

The United States holds a commanding position in this market — U.S. firms lead in production and R&D investment, launching over 150 synthetic media pilot programs in 2024 alone. American enterprises account for more than 60% of global synthetic video synthesis deployments, with over USD 33.9 billion private investment funneled into generative AI globally in 2024. Leading U.S. companies are integrating synthetic media across advertising, entertainment, and training platforms, and developing scalable pipelines capable of generating tens of thousands of realistic avatars monthly.

Market Size & Growth: From USD 4,622.7 M in 2024 to USD 18,341.2 M by 2032 with a projected CAGR of 18.8%—driven by automation and personalization demand.

Top Growth Drivers: Surge in content automation (45 %), expansion of immersive advertising (30 %), and demand for synthetic training environments (25 %).

Short-Term Forecast: By 2028, content production cost is expected to fall by 35 % while asset throughput improves by 50 %.

Emerging Technologies: Multimodal diffusion models, neural rendering pipelines, and real-time avatar personalization systems.

Regional Leaders: North America ~ USD 6,500 M by 2032 (enterprise adoption lead); Asia-Pacific ~ USD 5,800 M (rapid consumer uptake); Europe ~ USD 3,900 M (strong media & broadcast integration).

Consumer/End-User Trends: Major use in advertising, social media avatars, virtual influencers, synthetic voice agents; increasing brand trust via personalized video.

Pilot or Case Example: In 2025, a U.S. ad agency deployed synthetic video avatars that reduced personnel cost by 28 % and accelerated campaign runtime by 40 %.

Competitive Landscape: Market leader holds ~ 25 % share; key players include Synthesia, OpenAI, NVIDIA, Deepbrain AI, D-ID.

Regulatory & ESG Impact: New AI content disclosure laws, watermarking mandates, and carbon-efficient model incentives shaping adoption.

Investment & Funding Patterns: Over USD 15 billion invested in synthetic media and generative AI ventures in 2024; increasing use of milestone-based project financing.

Innovation & Future Outlook: Integration of synthetic media with AR/VR, real-time broadcast overlays, adaptive storytelling engines shaping next-gen adoption.

AI-powered synthetic media now underpins creative sectors such as gaming, marketing, education, and training simulations. Recent innovations include audio-video fusion tools and controllable avatar systems, while regulatory initiatives mandating watermarking and content transparency have accelerated in major economies. Rising adoption in Asia and Europe, combined with efficiency and sustainability drivers, point toward continued expansion of synthetic media pipelines.

Strategically, the AI-powered synthetic media market serves as a force multiplier across creative, marketing, and training sectors by enabling scalable, personalized content generation. Organizations adopting neural rendering pipelines see up to 40 % faster turnaround and 30 % fewer manual edits. Compared to rule-based graphics engines, neural rendering delivers 25 % improvement in realism and asset reuse efficiency over older CGI-based standards. In regional contrast, North America dominates in volume, while Asia-Pacific leads in adoption, with over 70 % of enterprises piloting synthetic content projects in 2024. By 2027, transformer-based multimodal agents are expected to improve content relevance metrics by 20 %. Firms are also committing to carbon-efficient model architectures with targets like 20 % reduction in training energy by 2028. In 2025, a U.S. media conglomerate achieved a 33 % reduction in video production time through integration of synthetic voice and face pipelines. Positioning the AI-Powered Synthetic Media Market as a pillar of resilience, compliance, and sustainable growth, strategic paths lie in converging AI, regulation, and creative economies.

The AI-Powered Synthetic Media Market is shaped by rapid advances in generative AI, deep learning architectures, and neural rendering capabilities. Adoption is spurred by the need for scalable content creation, immersive marketing, and synthetic training environments. Key dynamics include continuous model efficiency gains, expansion of multimodal synthesis (image, audio, video, text), and hybrid human–AI workflows. As enterprises globalize, synthetic media becomes a strategic tool to localize content at scale, adapt quickly to audience preferences, and reduce reliance on traditional production pipelines. Demand from sectors such as gaming, entertainment, and virtual learning drives ecosystem investments, while evolving regulatory frameworks around content disclosure and ethical synthetic media pose both constraints and guardrails.

Automation demand is a major driver: marketers and content creators now expect end-to-end production workflows with minimal human intervention. Synthetic media systems automate tasks like voice dubbing, lip sync, and background generation, leading to production throughput rising 2.5× in many studios. Enterprises are saving up to 35 % on labor costs by shifting routine content tasks to AI pipelines. Demand for scalable synthetic media in advertising campaigns—where hundreds of localized versions are needed—has expanded use of synthetic systems. Moreover, real-time synthetic content generation for live events and virtual influencers is emerging strongly, pushing adoption across sectors previously constrained by production overheads.

High compute costs remain a restraint: training large generative models and maintaining inference infrastructure demands expensive GPU clusters and optimized memory architectures. Many SMEs cannot shoulder upfront infrastructure investments. Moreover, synthetic media quality is heavily dependent on data quality, and training on biased or low-diversity data results in artifacted, unrealistic outputs and brand risk. Data licensing and privacy constraints complicate access to diverse training sets. Regulatory scrutiny over synthetic content (e.g. identity misuse, deepfake concerns) imposes compliance burdens on providers. These combined barriers slow adoption in cost-sensitive markets or regulated industries.

Real-time synthetic media represents a major opportunity: demand for dynamic avatars, live dubbing, and synthetic overlays in broadcasting is rising rapidly. Virtual events, esports, and remote conferences can use synthetic presenters and translated voice streams in real time. This extends reach and localizes engagement without human translators. Another opportunity lies in synthetic training environments and simulations for aerospace, defense, and education. Further, licensing of synthetic music, voice, and imagery via AI marketplaces opens new monetization models. Progressive consumer applications—such as personal avatar content creation—also expand addressable markets. Enterprise platforms embedding synthetic pipelines into SaaS environments constitute untapped growth zones.

Ethical and regulatory concerns pose substantial challenges. Brands fear misuse of synthetic media for misinformation or identity fraud, and face reputational risk. Legal frameworks lag behind technology, leaving ambiguity over copyright, deepfake labeling, and liability. Some jurisdictions propose mandatory watermarking, but uniform enforcement is lacking. In addition, consumer trust may erode if synthetic content is indistinguishable and misused. Technical challenges—such as eliminating deepfake artifacts or ensuring identity fidelity—add development risk. These trust and regulatory headwinds slow adoption in highly regulated sectors like finance, healthcare, and government.

• Modular & composable media pipelines accelerating integration: Adoption of modular AI components allows 60 % faster integration into existing media stacks, enabling firms to swap models for voice, video, or animation independently across Europe and North America. This trend reduces development risk and accelerates deployment of synthetic media solutions in enterprise environments.

• Real-time avatar generation surging across live platforms: Over 45 % of broadcast networks trialed live synthetic avatar overlays in 2025, enabling voice and lip-sync adaptation in multi-language streams. The demand is particularly strong in APAC, where simultaneous translation is highly valued across multilingual audiences.

• Energy-aware model architectures gaining priority: Over 30 % of new synthetic media model deployments in 2025 use energy-efficient transformer pruning or quantization to reduce power draw by 25 %. Sustainability requirements are driving the shift to “green synthetic media” solutions.

• Marketplace licensing of synthetic assets expanding rapidly: AI marketplaces now list over 1 million synthetic avatars, voice models, and scene kits, with licensing volume growing 70 % in 2025. This commercialization of synthetic media assets aids scale and accelerates adoption across small and medium enterprises.

The AI-Powered Synthetic Media Market is segmented by type (e.g. video-language, audio-text, vision-language), application (entertainment, education, marketing, simulation), and end users (media houses, advertising, enterprises, education, gaming). Each segment exhibits distinct adoption dynamics. Video-language systems are rising fastest due to demand for synthetic video content, while vision-language and audio-text remain foundational. In applications, entertainment, marketing, and immersive training dominate usage, while newer uses in simulation and education are gaining traction. As for end-users, media & entertainment companies lead early investment, but enterprises in BFSI, telecom, and education increasingly integrate synthetic media into workflows. Consumer applications and small business adoption also contribute to expanding addressable markets.

Video-language models are rising fastest and expected to overtake other types. For example, vision-language models currently account for ~42 % of adoption, while audio-text systems hold ~25 %, with video-language expected to surpass 30 % by 2032. The fastest growth lies in video-language due to demand for synthetic video, dubbing, and scene animation in marketing and entertainment. Other types—such as pure audio-text or vision-language—continue to support niche functions like voice assistants or image captioning, together contributing the remaining ~33 %.

According to a 2025 report by MIT Technology Review, video-language models were implemented by a major streaming platform to automatically generate captions and scene summaries, improving accessibility for over 10 million users.*

The leading application is media & entertainment, capturing a ~25 % share due to heavy use in video production, advertisement and content automation. The fastest-growing application is immersive training and simulation, as demand for synthetic environments in corporate, defense, and education sectors rises. Other application segments include marketing automation, virtual influencers, education & elearning, gaming simulation, and enterprise communications, with all others combined contributing ~40 %. In 2024, more than 38 % of enterprises globally reported piloting synthetic media systems for customer engagement platforms. Over 60 % of Gen Z consumers express greater trust in brands that adopt AI-powered multimodal chatbots and synthetic avatars.

According to a 2024 World Health Organization-backed initiative, AI-powered educational media tools were deployed in over 120 hospitals and universities globally, enhancing remote learning reach in underserved regions.*

Media & entertainment remains the leading end-user segment, accounting for ~30 % of investments in synthetic media, driven by content creation studios and broadcasters. The fastest-growing end-user is corporate brands and marketing divisions, adopting synthetic media for personalized advertising, internal training videos, and brand personas. Other significant end users include educational institutions, simulation providers, gaming studios, and telecom firms; collectively these remaining segments hold ~35 %. In 2024, over 38 % of enterprises globally piloted synthetic media for customer experience and support use cases. Over 60 % of younger consumers show more trust in brands integrating synthetic avatars and AI chat interfaces.

According to a 2025 Gartner report, AI adoption among SMEs in the retail sector increased by 22 %, enabling more than 500 companies to optimize personalized synthetic media for promotional campaigns.

North America accounted for the largest market share at 34.3% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 27.8% between 2025 and 2032.

In 2024, North America’s synthetic media market contributed roughly one-third of global demand, driven by robust content creation in advertising, marketing, gaming, and enterprise communications. Asia-Pacific, meanwhile, saw rising internet penetration rates—China, India, and South Korea leading with over 60% of the region’s population online—fostering sharp increases in consumption of synthetic avatars, voice agents, and localized video. Europe held about 30% share in 2024 and is pushing adoption via regulatory frameworks. Latin America and Middle East & Africa each contributed under 10% but are accelerating investment in digital infrastructure. The combined share of non-North American markets (Asia-Pacific + Europe + others) surpassed 65% in usage volume of synthetic media assets, reflecting shifting center of gravity toward emerging economies and regulatory innovation.

What key forces are fueling dominance in content innovation and regulation?

North America held approximately 34.3% of the synthetic media market share in 2024, with the United States commanding roughly 85.1% of that regional volume. Demand is propelled by media & entertainment, advertising, gaming, and enterprise training using synthetic video and audio content. Regulatory changes include state and federal mandates around deepfake disclosure and watermarking requirements. Technological trends involve improved generative AI engines, neural rendering, cloud GPU infrastructure, and hybrid human-AI workflows. Local players such as Synthesia, Runway AI, and ElevenLabs are scaling operations: one firm reduced video production turnaround by over 60% and enterprise training-video costs by up to 90%. Consumer behavior varies: enterprises in healthcare & finance show higher adoption for synthetic media in training and diagnostics, while consumer content and social media favor avatars, virtual influencers, and synthetic voice agents.

How is regulatory pressure shaping creative adoption and ethical trust?

Europe accounted for about 30% of the global synthetic media market share in 2024. Key markets include Germany, the UK, and France, with growing contributions from Nordic countries and the Benelux region. EU-wide regulation (e.g., the AI Act effective since early 2025) and directives like Digital Services Act add transparency requirements, deepfake labeling, and content provenance obligations. Adoption of explainable AI, ethical synthetic content pipelines, and sustainability standards is rising. European players—startups and media houses—are investing in synthetic voice models with multilingual support and watermarking. Consumers in Europe demand higher disclosure around AI-generated content and show stronger preference for synthetic media that supports data privacy and content authenticity.

Why is digital scale and innovation reshaping content creation dynamics?

Asia-Pacific ranked second in total market volume for synthetic media in 2024, holding roughly 21% of global share. China, India, Japan, and South Korea are top consuming countries. Infrastructure investments in cloud services, 5G connectivity, and AI research hubs are accelerating production capacity. Local innovation hubs are developing synthetic voice and image-to-text systems optimized for regional languages and dialects. Players in Asia-Pacific are launching mobile-first synthetic media apps, and e-commerce platforms use AI-generated video/avatars to enhance user engagement. Consumer behavior is heavily skewed toward mobile AI apps, short video content, and social commerce; users expect low-latency, localized synthetic assets.

In what ways is regional culture and language driving demand for synthetic content?

South America includes leading countries such as Brazil and Argentina, contributing together around 5-8% of the global synthetic media market in 2024. Demand is strongly tied to media, advertising, and localization—translating content into Portuguese, Spanish, and indigenous languages. Infrastructure constraints and energy cost are challenges, though government incentives for digital culture and media exports are emerging. Local players are beginning to offer synthetic voice-overs and dubbed content services for streaming platforms and broadcasters. Consumers show strong preference for localized content with synthetic ethics markers, clear disclosure, and culturally resonant avatars.

How are modernization and regulation influencing synthetic media uptake in emerging markets?

Middle East & Africa accounted for roughly 4-7% of global synthetic media consumption in 2024. Major growth countries include UAE, South Africa, and Saudi Arabia, emphasizing modernization in media, education, and government outreach. Technological modernization includes cloud adoption and AI platforms deployed for multilingual voice agents and public service announcements. Local regulations are being shaped by trade partnerships and data protection laws; disclosure requirements for synthetic content are emerging. Players in the region are building partnerships with global AI providers and local media firms to embed synthetic media in advertising and civic communication. Consumer behavior reflects high interest in synthetic media for social media, entertainment, and mobile apps, often with regional preferences around language, cultural visuals, and authenticity.

United States — about 29-35% market share globally; dominance due to high production capacity, venture capital funding, and presence of major tech, media, and content-creation firms.

China — approximately 15-20% share globally; strong end-user demand, rapidly expanding AI research, and local content platforms driving synthetic media creation in native languages.

The competitive environment in the AI-Powered Synthetic Media market is moderately consolidated: the top 5 companies hold around 60-65% of total market influence. There are more than 50 active competitors globally, including startups, established tech firms, and media companies. Strategic initiatives include partnerships (e.g. content platforms collaborating with AI model providers), product launches like synthetic avatar tools and audio-video fusion systems, mergers to acquire model IP or cloud infrastructure, and innovation around real-time media pipelines. Many firms are investing in watermarking and deepfake detection tools to satisfy regulatory and ethical demands. Innovation trends influencing competition include multimodal generative models, real-time voice and video synchronization, neural rendering for realistic face and body motion, and low-compute model architectures to reduce infrastructure costs. Market leaders are positioning portfolios to address enterprise and consumer segments, with side bets on immersive media, e-learning, and virtual influencers.

Emerging technologies shaping the AI-Powered Synthetic Media market include generative AI frameworks based on GANs, transformers, diffusion models, and autoregressive neural networks. Real-time neural rendering pipelines are being refined to support high-resolution video-avatar synchronization, photorealistic lighting, and emotion recognition. Voice synthesis models now integrate prosody and emotional modulation, enabling voice agents that adapt tone and accent for regional markets. Multimodal AI convergence—combining visual, audio, and text signals—is enabling synthetic media systems that can automatically generate dubbing, subtitles, scene summaries, and avatar lip sync. Efficiency improvements include pruning, quantization, model distillation to reduce training data and compute requirements; some deployments in 2024 reported up to 25-30% power consumption reduction in rendering engines via model compression techniques. Edge inference and cloud hybridization are expanding access for content creators and small-scale enterprises. Ethical tech stacks now include watermarking and content provenance as part of model output pipelines.

• In September 2023, Synthesia expanded its synthetic video platform to support over 120 languages, adding neural voice and lip-sync improvements that improved localization quality by 35%. Source: www.synthesia.io

• In February 2024, NVIDIA launched a neural rendering update that reduced avatar motion artifacts by 40% for film-quality output. Source: www.nvidia.com

• In August 2024, Deepbrain AI partnered with major telecom operators in South Korea to deliver real-time synthetic voice dubbing in live broadcasts, enabling subtitle-free content for over 5 million viewers. Source: www.deepbrain.ai

• In May 2024, Adobe introduced synthetic image/video watermarking tools in its creative cloud platform, enabling content verification for users across EU and UK. Source: www.adobe.com

The report covers global analysis across synthetic media product types (video-language models, vision-language, audio-text systems, avatars & virtual influencer tools), deployment modes (cloud-based vs on-premises), and applications in media & entertainment, marketing & advertising, education & immersive training, gaming & simulation, corporate communications, and virtual events. Geographically, markets segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Also includes regulation & ESG topics such as AI transparency laws, watermark standards, energy efficiency, data privacy, and ethical synthetic media production. Additionally, the report examines recent technology innovations (multimodal models, neural rendering, real-time voice/avatar pipelines), competitive structures (startups, alliances, incumbents), investment patterns, and consumer behaviour trends across regions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4,622.7 Million |

|

Market Revenue in 2032 |

USD 18,341.2 Million |

|

CAGR (2025 - 2032) |

18.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User Industry

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Synthesia, OpenAI, NVIDIA, Deepbrain AI, D-ID, Runway ML, Adobe, Microsoft, Baidu, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |