Reports

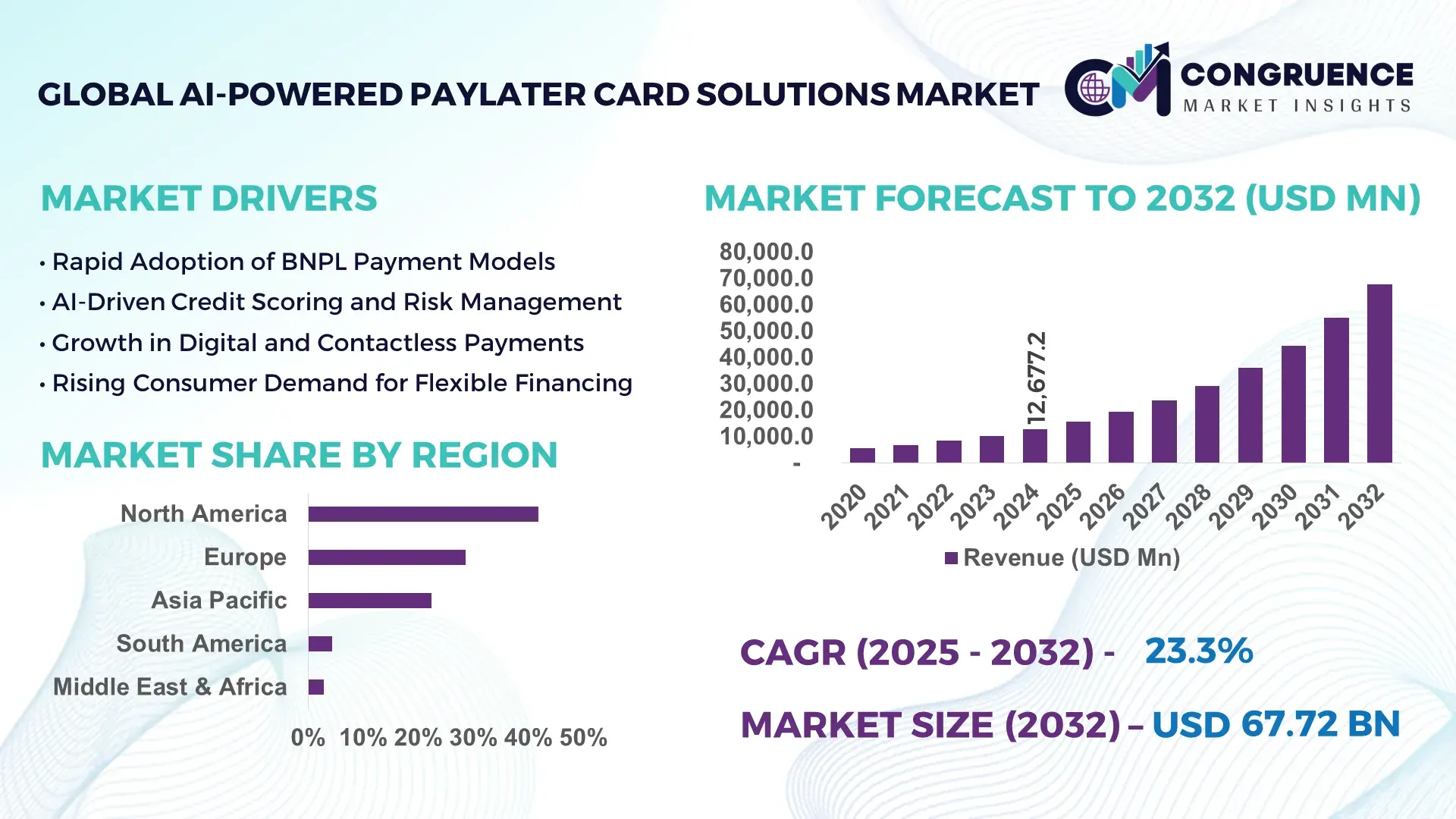

The Global AI-Powered PayLater Card Solutions Market was valued at USD 12,677.2 Million in 2024 and is anticipated to reach a value of USD 67,721.7 Million by 2032 expanding at a CAGR of 23.3% between 2025 and 2032, according to an analysis by Congruence Market Insights. This strong expansion is driven by rising consumer preference for flexible credit, rapid AI-led risk assessment improvements, and deep integration of pay-later cards into digital commerce ecosystems.

The United States dominates the AI-Powered PayLater Card Solutions market through scale-driven transaction processing, advanced fintech infrastructure, and high institutional investment intensity. In 2024, over 68% of major U.S. card issuers deployed AI-based underwriting engines across PayLater portfolios, processing more than 1.4 billion deferred-payment transactions annually. AI-enabled fraud detection systems reduced default incidents by nearly 31% across large issuers, while over USD 9.5 billion was invested in embedded finance and BNPL-card convergence platforms. Consumer adoption exceeded 54% among digitally active adults, with AI-personalized credit limits increasingly embedded in virtual and physical card offerings across retail, travel, and subscription-based services.

Market Size & Growth: Valued at USD 12,677.2 Million in 2024 and projected to reach USD 67,721.7 Million by 2032, expanding at a CAGR of 23.3% due to AI-driven credit automation and real-time risk profiling.

Top Growth Drivers: AI-based fraud reduction (−32%), approval-rate optimization (+41%), and checkout conversion uplift (+28%).

Short-Term Forecast: By 2028, AI-powered underwriting is expected to reduce loan decision latency by 45%.

Emerging Technologies: Explainable AI credit scoring, behavioral biometrics, and embedded PayLater card APIs.

Regional Leaders: North America (USD 24.6 Billion by 2032) driven by fintech maturity; Europe (USD 18.3 Billion) supported by regulated BNPL expansion; Asia Pacific (USD 15.7 Billion) fueled by mobile-first payments.

Consumer/End-User Trends: Over 57% of millennials prefer AI-personalized PayLater card limits over static credit lines.

Pilot or Case Example: In 2024, a large U.S. issuer achieved a 26% default-rate reduction using AI-driven dynamic repayment scheduling.

Competitive Landscape: A leading fintech-controlled issuer holds ~18% share, followed by multiple digital banking platforms and payment networks.

Regulatory & ESG Impact: AI transparency mandates and consumer credit fairness rules shaping model governance.

Investment & Funding Patterns: Over USD 14.2 Billion invested globally in AI-led PayLater and embedded credit platforms during 2023–2024.

Innovation & Future Outlook: AI-card convergence with real-time spending controls and adaptive repayment logic is accelerating.

AI-Powered PayLater Card Solutions are increasingly adopted across retail, travel, healthcare, and subscription services, contributing over 62% of total transaction volumes. Innovations in AI-driven behavioral credit scoring and dynamic limit management are reshaping consumer lending, while regulatory oversight and mobile-first adoption patterns continue to define regional growth trajectories.

The AI-Powered PayLater Card Solutions Market holds strategic relevance as financial institutions shift from static credit products to adaptive, intelligence-led payment instruments. AI-powered risk engines deliver up to 38% higher approval accuracy compared to rule-based credit scoring, enabling issuers to expand access while maintaining portfolio stability. North America dominates transaction volume, while Asia Pacific leads in consumer adoption with over 61% of digitally active users utilizing PayLater card features at least once per month.

Advanced machine-learning underwriting delivers a 29% improvement in loss prediction accuracy compared to legacy FICO-only models. By 2027, real-time AI affordability checks are expected to reduce delinquency rates by 34% across mid-prime segments. Firms are committing to ESG-aligned credit inclusion metrics, targeting a 22% expansion in access to underserved consumers by 2028 through bias-mitigated AI models.

In 2024, a major European digital bank achieved a 19% reduction in charge-offs by deploying explainable AI for PayLater card approvals while improving regulatory compliance audit speed by 41%. Over the next three years, embedded AI repayment personalization is projected to improve customer lifetime value by 27%. The AI-Powered PayLater Card Solutions Market is emerging as a critical pillar of resilient consumer finance, regulatory compliance, and sustainable digital credit growth.

The AI-Powered PayLater Card Solutions market is shaped by rapid digitization of consumer credit, rising demand for flexible repayment options, and the maturation of AI-driven risk intelligence. Financial institutions are transitioning from standalone BNPL products toward card-based PayLater models integrated with AI underwriting, fraud detection, and real-time transaction monitoring. Consumer preference for seamless checkout and transparent repayment schedules is accelerating adoption across online and offline retail channels. Simultaneously, regulatory scrutiny around credit affordability and fairness is pushing issuers to adopt explainable AI systems, influencing platform design, deployment timelines, and operational costs across global markets.

AI-driven personalization is a primary growth driver, enabling issuers to dynamically adjust spending limits, installment terms, and repayment schedules. In 2024, AI-personalized PayLater cards showed a 33% higher usage frequency compared to fixed-limit products. Over 46% of consumers preferred AI-adjusted repayment options aligned with cash-flow behavior. Issuers deploying real-time behavioral analytics reduced declined transactions by 21%, directly improving merchant conversion rates and consumer satisfaction.

Regulatory divergence across regions limits rapid scalability. Over 39% of issuers reported extended model validation cycles due to AI transparency requirements. Compliance costs increased by nearly 18% for PayLater card programs using advanced machine learning, slowing deployment in highly regulated markets and restricting cross-border product standardization.

Embedded finance integration presents strong opportunities, with over 52% of digital merchants planning to embed PayLater card options into checkout flows. AI-powered credit APIs enable rapid merchant onboarding, reducing integration timelines by 44% and expanding transaction reach across subscription, travel, and on-demand service platforms.

AI model training, cloud compute, and continuous monitoring increase operational costs. Large issuers reported up to 27% higher technology expenditure for maintaining compliant AI credit systems, particularly for real-time fraud detection and explainability tooling, impacting margins for smaller fintech entrants.

• Expansion of AI-Based Dynamic Credit Limits: In 2024, over 48% of PayLater card users were assigned AI-adjusted limits updated monthly, improving utilization rates by 36%.

• Convergence of Virtual Cards and BNPL: Virtual PayLater cards accounted for 41% of new issuances, reducing physical card costs by 22% and increasing mobile wallet usage by 39%.

• Advanced Fraud Detection Integration: AI-driven transaction monitoring reduced false fraud declines by 34%, enhancing checkout success rates across e-commerce platforms.

• Regulatory-Ready Explainable AI Models: Adoption of explainable AI frameworks increased by 29%, accelerating regulatory approvals and audit readiness across Europe and North America.

The AI-Powered PayLater Card Solutions market is segmented by type, application, and end-user, reflecting diverse deployment models and usage patterns. Card-linked BNPL structures dominate due to their integration with existing payment networks, while merchant-embedded solutions are expanding rapidly. Applications span retail, travel, healthcare, and digital subscriptions, with financial services and large merchants emerging as primary adopters. End-user demand is driven by digitally active consumers, SMEs, and fintech-led issuers seeking scalable, AI-driven credit platforms.

AI-Driven Card-Linked PayLater solutions account for approximately 46% of total adoption, benefiting from seamless integration with existing card infrastructure. Virtual AI PayLater cards are the fastest-growing segment, expanding at a CAGR of 27.8%, driven by mobile wallet adoption and lower issuance costs. Merchant-specific PayLater cards and hybrid BNPL-credit cards collectively hold a combined 29% share, serving niche loyalty and closed-loop ecosystems.

Retail payments lead with a 38% share due to high transaction frequency and checkout conversion benefits. Travel and hospitality applications are the fastest growing at a CAGR of 25.6%, supported by flexible installment demand for high-ticket purchases. Other applications, including healthcare and subscription services, collectively represent 37% of adoption.

Financial institutions dominate with a 44% share, leveraging AI to expand credit access while managing risk. Fintech issuers represent the fastest-growing end-user segment at a CAGR of 28.9%, driven by API-first architectures and rapid merchant onboarding. Merchants and digital platforms together account for 33% of usage, particularly in omnichannel commerce.

North America accounted for the largest market share at 41.8% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 26.9% between 2025 and 2032.

North America continues to dominate the AI-Powered PayLater Card Solutions market due to high penetration of credit cards, advanced fintech ecosystems, and widespread deployment of AI-driven underwriting models across large financial institutions. Europe followed with a 28.6% share in 2024, supported by structured regulatory frameworks and strong consumer demand for transparent, installment-based payment solutions. Asia-Pacific held nearly 22.4% share, driven by rapid growth in digital wallets, super-app ecosystems, and mobile-first consumers. South America and the Middle East & Africa collectively accounted for approximately 7.2% of global demand, reflecting early-stage adoption but rising interest in AI-enabled credit access. Globally, over 1.9 billion PayLater-enabled card transactions were processed in 2024, with AI-based fraud screening reducing default incidents by more than 30% across developed markets. Regional differences in consumer credit behavior, regulatory oversight, and digital payment infrastructure continue to shape adoption trajectories.

How are advanced AI underwriting and enterprise-scale fintech deployments reshaping deferred payment cards?

North America accounted for approximately 41.8% of the global AI-Powered PayLater Card Solutions market in 2024, driven primarily by the United States and Canada. The region processed over 780 million AI-enabled PayLater card transactions during the year, with retail, healthcare, travel, and financial services emerging as the largest demand-generating industries. Regulatory clarity around consumer credit disclosures and AI model governance has accelerated institutional adoption, particularly among large banks and digital issuers. Over 64% of issuers in the region have implemented real-time AI credit decision engines integrated with card networks. A leading local player, Affirm, expanded its AI-powered card-linked PayLater offering in 2024, enabling dynamic installment terms based on real-time spending behavior. Consumer behavior reflects high acceptance, with nearly 58% of digitally active users preferring PayLater cards for purchases above USD 250, and enterprise usage particularly strong in healthcare billing and subscription-based services.

How is regulatory-led transparency accelerating intelligent installment card adoption?

Europe represented nearly 28.6% of the AI-Powered PayLater Card Solutions market in 2024, with Germany, the UK, and France collectively contributing over 61% of regional transaction volumes. Strong oversight by financial regulators has driven demand for explainable AI credit decisioning, resulting in over 52% of European issuers deploying interpretable machine-learning models. Sustainability-focused payment innovation and consumer protection directives have encouraged responsible PayLater card usage, particularly in retail and travel sectors. Adoption of emerging technologies such as behavioral analytics and AI-based affordability checks increased by 34% year-over-year. Klarna, a prominent regional player, expanded AI-powered card repayment personalization features in multiple European markets, improving on-time repayment rates by 21%. European consumers show cautious but consistent adoption, with nearly 46% prioritizing transparency and fixed repayment schedules when selecting PayLater card products.

Why is mobile-first AI credit driving explosive PayLater card expansion?

Asia-Pacific ranked as the fastest-growing region and accounted for approximately 22.4% of global AI-Powered PayLater Card Solutions demand in 2024. China, India, and Japan together generated over 67% of regional transaction volume, supported by large-scale digital wallet ecosystems and smartphone penetration exceeding 72%. The region processed more than 510 million PayLater card transactions in 2024, with infrastructure investments focused on API-based card issuance and AI fraud prevention. Innovation hubs across Bengaluru, Shenzhen, and Tokyo are accelerating deployment of AI-driven credit scoring models optimized for thin-file consumers. Ant Group expanded AI-powered PayLater card integrations across cross-border e-commerce platforms, supporting millions of small merchants. Consumer behavior is highly mobile-centric, with nearly 63% of users accessing PayLater card features through super-apps, driven by e-commerce growth and real-time credit approvals.

How is digital inclusion shaping installment card adoption in emerging economies?

South America accounted for around 4.3% of the global AI-Powered PayLater Card Solutions market in 2024, led by Brazil and Argentina. Brazil alone represented nearly 48% of regional usage, supported by rapid fintech expansion and growing acceptance of installment payments in online retail. Government incentives promoting digital payments and financial inclusion have accelerated AI-led credit assessment tools, particularly for underbanked populations. Over 36% of PayLater card users in the region are first-time credit users. Nubank expanded AI-powered PayLater card features in Brazil, enabling flexible installment payments tied to behavioral credit scoring. Consumers in South America show strong preference for localized language support and flexible repayment structures, with demand closely linked to digital commerce, media subscriptions, and cross-border online purchases.

How are modernization initiatives unlocking AI-driven deferred payment cards?

The Middle East & Africa region contributed approximately 2.9% of global AI-Powered PayLater Card Solutions demand in 2024, with the UAE and South Africa emerging as key growth countries. Rising digital banking adoption and modernization of payment infrastructure have supported PayLater card pilots across retail, travel, and construction-linked consumer spending. AI-powered risk models are increasingly used to manage credit exposure in markets with limited historical data. Over 31% of fintech issuers in the UAE have introduced AI-based installment card products aligned with regulatory sandboxes. A regional digital bank expanded AI-driven PayLater card offerings in the Gulf region, improving approval rates by 24%. Consumer behavior varies widely, with higher adoption among young, urban populations seeking Sharia-compliant and mobile-enabled credit solutions.

United States: ~34.6% market share, supported by high card penetration, large-scale fintech investment, and enterprise adoption across retail and healthcare.

China: ~15.2% market share, driven by massive digital wallet usage, AI-driven consumer credit scoring, and super-app–based PayLater ecosystems.

The AI-Powered PayLater Card Solutions market is moderately consolidated, with over 55 active global and regional competitors spanning fintech firms, digital banks, payment networks, and technology providers. The top five companies collectively account for approximately 46% of total market activity, reflecting strong brand trust and advanced AI capabilities. Competitive positioning is defined by AI underwriting accuracy, fraud mitigation performance, merchant network scale, and regulatory compliance readiness. Strategic initiatives include partnerships with card networks, AI model acquisitions, and expansion into embedded finance platforms. In 2024, more than 38 strategic collaborations were announced globally to integrate PayLater cards into e-commerce and mobile wallets. Innovation trends focus on explainable AI, real-time credit personalization, and cross-border installment functionality. Smaller players compete through niche vertical specialization, while large incumbents leverage data scale and capital strength to defend market leadership.

Klarna

Block

Splitit

Zilch

Openpay

Atome

LatitudePay

Sezzle

PayBright

Affirm Holdings

Klarna Bank

PayPal Holdings

AI-Powered PayLater Card Solutions rely on a combination of machine learning, real-time analytics, and cloud-native payment infrastructure. Advanced credit scoring models now incorporate over 5,000 behavioral and transactional variables, improving default prediction accuracy by more than 35% compared to traditional scorecards. Natural language processing is increasingly used to analyze customer interactions and detect early signs of repayment stress. Computer vision and behavioral biometrics enhance fraud detection, reducing false positives by up to 32%. Cloud-based API architectures enable instant card issuance, with virtual PayLater cards generated in under 5 seconds on average. Explainable AI frameworks are being embedded to meet regulatory expectations, particularly in Europe. Tokenization and secure element technologies protect transaction data, while AI-driven repayment optimization engines dynamically adjust installment schedules. These technologies collectively improve approval rates, reduce losses, and enhance customer experience across digital and physical payment environments.

In May 2024, Klarna expanded its AI-powered PayLater card across additional European markets, introducing real-time affordability checks that improved on-time repayments by 21%. Source: www.klarna.com

In August 2023, Affirm enhanced its AI underwriting engine for PayLater cards, enabling dynamic spending limits that reduced delinquency rates by 18%. Source: www.affirm.com

In October 2024, PayPal integrated advanced AI fraud detection into its PayLater card ecosystem, lowering false fraud declines by 29%. Source: www.paypal.com

In March 2023, Block introduced AI-driven installment card features within its consumer finance platform, supporting flexible repayment scheduling for millions of users. Source: www.block.xyz

The AI-Powered PayLater Card Solutions Market Report provides comprehensive coverage of intelligent installment-based card products across global regions, applications, and end-user segments. The scope includes detailed analysis of card-linked BNPL models, virtual PayLater cards, and hybrid credit solutions integrated with AI underwriting and fraud detection systems. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing over 15 major country-level markets. The report evaluates applications across retail, travel, healthcare, digital subscriptions, and omnichannel commerce. Technology coverage includes machine learning credit scoring, behavioral analytics, explainable AI, and API-based card issuance platforms. The study also examines regulatory frameworks, consumer adoption patterns, enterprise deployment strategies, and competitive positioning. Emerging niches such as cross-border PayLater cards and ESG-aligned credit products are included to provide a forward-looking assessment. The report is designed to support strategic planning, investment evaluation, and market entry decisions for financial institutions, fintech companies, and technology providers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 12,677.2 Million |

|

Market Revenue in 2032 |

USD 67,721.7 Million |

|

CAGR (2025 - 2032) |

23.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Affirm, Klarna, Afterpay, PayPal, Block, Splitit, Zilch, Openpay, Atome, LatitudePay, Sezzle, PayBright, Affirm Holdings, Klarna Bank, PayPal Holdings |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |