Reports

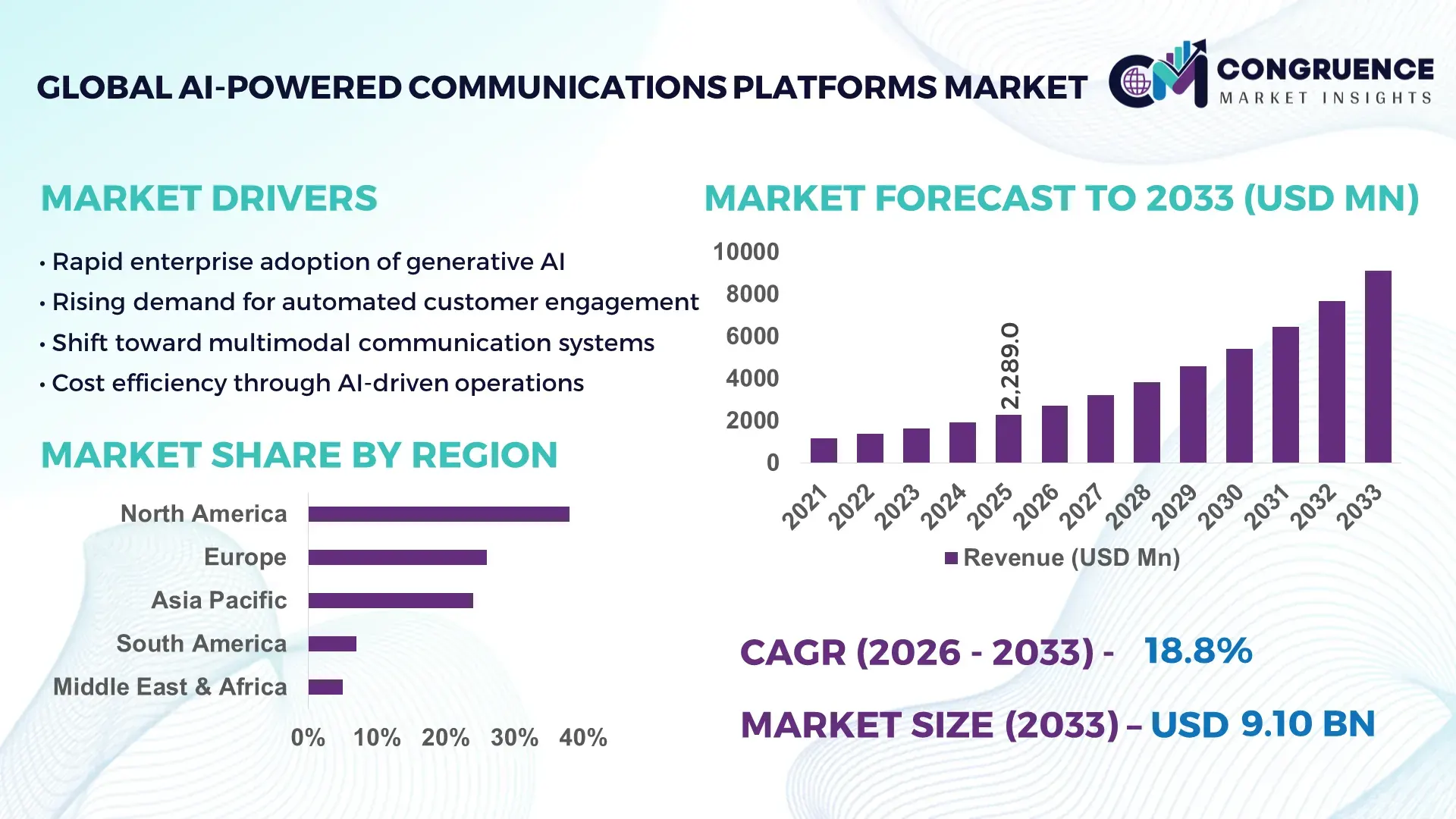

The Global AI-Powered Communications Platforms Market was valued at USD 2,289.0 Million in 2025 and is anticipated to reach USD 9,100.3 Million by 2033, expanding at a CAGR of 18.83% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by the rapid enterprise shift toward automated, data-driven customer engagement and omnichannel interaction management.

The United States leads the global AI-Powered Communications Platforms landscape through large-scale cloud infrastructure, advanced AI R&D ecosystems, and high enterprise digitization. The country hosts over 40% of global hyperscale data centers supporting real-time conversational AI, while annual enterprise spending on AI-driven communication systems exceeded USD 18 billion in 2024. More than 65% of Fortune 500 firms deploy AI contact centers across telecom, BFSI, and healthcare, with generative AI models increasingly embedded in voice, video, and messaging workflows. Venture investment in U.S.-based conversational AI firms surpassed USD 6.5 billion in 2023–2024, and over 1.2 million AI-enabled agents are now active in customer service operations nationwide.

Market Size & Growth: USD 2.29 billion in 2025 to USD 9.10 billion by 2033, driven by enterprise automation and omnichannel engagement.

Top Growth Drivers: 38% chatbot adoption across enterprises; 32% reduction in agent handling time; 27% improvement in customer resolution speed.

Short-Term Forecast: By 2028, AI routing and sentiment tools could cut average call handling time by 25%.

Emerging Technologies: Generative AI voice assistants, real-time translation engines, and multimodal conversational analytics.

Regional Leaders: North America USD 3.6 billion (deep cloud integration); Europe USD 2.1 billion (privacy-first AI deployment); Asia-Pacific USD 2.4 billion (rapid digital commerce uptake).

Consumer/End-User Trends: Rising self-service usage in banking, telecom, and e-commerce through AI chat and voice bots.

Pilot Example: In 2024, a global telecom operator reduced call escalations by 28% using AI triage systems.

Competitive Landscape: Market leader ~22% share, followed by four major cloud and CX automation providers.

Regulatory & ESG Impact: Stronger data localization rules and energy-efficient AI mandates shaping platform design.

Investment & Funding Patterns: Over USD 7 billion raised globally in AI communications startups (2023–2024).

Innovation & Future Outlook: Tight integration of CRM, analytics, and AI agents across enterprise workflows.

AI-Powered Communications Platforms are now embedded across telecom, BFSI, retail, healthcare, and government, with customer service and sales automation together accounting for over 55% of usage. Innovations in real-time speech analytics, automated compliance monitoring, and low-latency voice AI are reshaping deployments. Stricter data governance rules in Europe and India are accelerating privacy-by-design architectures, while Asia-Pacific’s mobile-first consumer base is fueling rapid adoption of AI chat and voice commerce tools. Hybrid cloud deployment, agentic AI workflows, and vertical-specific models are emerging as core growth themes.

AI-Powered Communications Platforms are becoming a foundational layer of digital enterprise strategy, linking customer experience, operational efficiency, and data intelligence into a single automated fabric. Organizations are shifting from reactive support models to proactive, AI-led engagement systems that anticipate customer needs, personalize interactions, and optimize workforce allocation. Large enterprises are integrating AI communications with CRM, ERP, and analytics stacks, enabling real-time decisioning across marketing, sales, and service functions.

Comparatively, Generative Voice AI delivers 30% faster query resolution than traditional IVR systems, reducing customer friction and improving satisfaction scores. Meanwhile, automated sentiment and intent detection engines are helping firms route 45–55% of inquiries to self-service channels without human intervention.

Regionally, Asia-Pacific dominates in deployment volume, driven by mobile-first economies and high digital payment usage, while North America leads in enterprise adoption with 68% of large firms using AI contact centers at scale.

In the short term, by 2028, multimodal AI assistants are expected to improve first-contact resolution rates by 35% while cutting average handling costs by 22%.

From a compliance and ESG standpoint, firms are committing to 20% reductions in data-center energy intensity by 2030 through more efficient AI inference architectures and greener cloud sourcing.

In a micro-scenario, in 2024 a major U.S. bank reduced call center downtime by 26% by deploying AI-driven predictive routing and real-time agent assistance tools.

Overall, the AI-Powered Communications Platforms Market is positioning itself as a pillar of resilient, compliant, and sustainable digital transformation—enabling enterprises to scale intelligently while maintaining trust, transparency, and operational continuity.

The AI-Powered Communications Platforms Market is shaped by rapid advances in conversational AI, cloud computing, and data analytics. Enterprises are prioritizing automation to control rising customer support costs while maintaining service quality. The shift toward omnichannel engagement—spanning voice, chat, SMS, social, and video—has intensified demand for unified AI platforms that centralize data and workflows. Integration with CRM, marketing automation, and workforce management tools is becoming standard, accelerating deployment cycles. At the same time, stricter data privacy laws, model governance requirements, and algorithmic transparency rules are influencing product design and regional rollout strategies. Talent shortages in AI engineering and high compute costs remain constraints, while open-source AI frameworks and specialized chips are gradually lowering barriers to adoption. Overall, competition is intensifying among cloud providers, CX vendors, and AI-native startups, driving continuous innovation and faster release cycles.

Large organizations are rapidly replacing legacy call centers with AI-enabled digital engagement hubs to reduce operational costs and improve customer experience. Studies show that AI routing and virtual agents can handle 40–60% of routine inquiries without human intervention, significantly lowering staffing requirements. Enterprises deploying AI co-pilots report 20–30% productivity gains for live agents through real-time suggestions, automated summarization, and sentiment guidance. Telecom, banking, and e-commerce sectors—together representing the majority of high-volume customer interactions—are leading adoption, with many firms running millions of AI-assisted conversations per month. The growing need for 24/7 support, multilingual communication, and instant response times further strengthens demand for intelligent platforms. As businesses scale globally, centralized AI communication layers reduce complexity, enable consistent service quality, and improve data-driven decision-making across regions and departments.

Strict data protection regulations such as GDPR in Europe, CCPA in California, and emerging AI governance laws are increasing compliance complexity for AI communications vendors. Many enterprises hesitate to deploy conversational AI at scale due to risks around data leakage, model hallucinations, and biased responses. Sensitive industries like healthcare and finance require robust encryption, audit trails, and explainability, which add technical overhead and deployment costs. Additionally, cross-border data localization rules limit centralized cloud processing, forcing firms to build regional infrastructure. Customer skepticism toward automated interactions—especially in high-stakes services like banking—can slow adoption unless transparency and reliability are proven. Integration with legacy systems also remains a barrier, as older contact centers lack modern APIs, creating delays, higher migration costs, and operational disruption.

Verticalized AI models tailored to sectors such as healthcare, finance, retail, and government represent a major growth opportunity. In healthcare, AI assistants can manage appointment scheduling, triage, and post-care follow-ups, reducing administrative workloads by up to 35%. In banking, compliance-aware AI can monitor conversations in real time to prevent mis-selling and fraud. Retailers are deploying AI sales assistants that combine product knowledge, inventory data, and personalized recommendations to boost conversion rates. As more firms seek domain-specific solutions rather than generic chatbots, vendors are investing in specialized datasets, industry partnerships, and pre-trained models. The rise of agentic AI—where systems autonomously complete multi-step workflows—further expands opportunities for end-to-end process automation across procurement, customer service, and back-office operations.

Training and running advanced conversational AI models require substantial cloud computing power, driving up operational expenses for both vendors and enterprises. Small and mid-sized businesses often struggle to justify these costs despite potential efficiency gains. Additionally, there is a global shortage of skilled AI engineers, data scientists, and MLOps specialists, slowing deployment timelines. Many organizations still rely on fragmented legacy systems that are difficult to integrate with modern AI platforms, leading to prolonged migration projects and business disruption. Performance reliability is another hurdle—latency issues, inaccurate responses, or system outages can undermine trust in automated communications. Cybersecurity risks, including prompt injection and data poisoning attacks, further complicate large-scale implementation and require continuous monitoring and defense mechanisms.

Surge in Generative Voice and Multimodal AI: Enterprise deployment of generative voice assistants grew by 42% in 2024, with firms reporting 28% faster query resolution and improved natural language handling across 35+ languages. Multimodal systems combining voice, text, and visual inputs are now being piloted in 18% of large contact centers, reducing escalations to human agents by nearly one-third.

Expansion of Real-Time Analytics and Sentiment AI: Adoption of real-time conversation analytics increased to 57% of AI-enabled call centers in 2024, helping organizations detect churn risk within 5–10 seconds of interaction. Firms using sentiment-aware routing achieved a 24% lift in customer satisfaction and a 19% reduction in repeat calls.

Growth of Autonomous AI Agents in Workflows: Autonomous AI agents capable of completing end-to-end tasks (refunds, ticket updates, billing changes) are now live in 22% of enterprises, cutting manual processing time by 30–40%. Early adopters report a 21% decline in back-office ticket volumes within the first year of deployment.

Rise in Modular and Prefabricated Construction (AI Integration Trend): While traditionally linked to construction, modular project ecosystems are increasingly embedding AI-powered communication layers for site coordination. Around 55% of new modular projects reported cost savings through automated scheduling, supply-chain chatbots, and AI-driven vendor coordination. Prefabrication sites using AI communication dashboards reduced on-site rework by 18% and shortened delivery timelines by roughly 20%, particularly in Europe and North America where digital project control is now standard.

The AI-Powered Communications Platforms Market is structured around type, application, and end-user dimensions that reflect how intelligent communication systems are built, deployed, and consumed across industries. On the type axis, the market spans vision-language, audio-text, video-language, and other multimodal architectures, each serving different interaction needs such as text chat, voice automation, or real-time visual understanding. Application-wise, adoption clusters around customer experience, sales and marketing automation, operations and workflow support, and enterprise knowledge systems, with varying intensity across sectors that handle high volumes of digital interactions. From an end-user perspective, large enterprises dominate usage due to scale and data availability, but SMEs, public sector bodies, and healthcare providers are increasingly integrating AI communications to improve service delivery, reduce manual workloads, and enhance compliance. Deployment models also vary—cloud-first architectures are common among tech-savvy firms, while regulated industries lean toward hybrid setups—creating a diverse, layered segmentation landscape rather than a single uniform market pattern.

Vision-language models currently represent the backbone of AI-powered communications, accounting for 42% of adoption because they enable systems to interpret images, documents, and visual interfaces alongside text—critical for support desks, retail catalog search, and document-heavy workflows. These models power use cases such as invoice processing, visual product identification, and screen-based troubleshooting, making them the most commercially embedded architecture today.

The fastest-growing type is video-language models (estimated ~28% CAGR), driven by the explosion of video-based customer engagement, remote assistance, and digital training environments. As enterprises shift toward live video support, automated meeting summarization, and AI-driven content moderation, demand for models that can analyze motion, speech, and visuals simultaneously is accelerating. Adoption in video-language systems is expected to surpass 30% by 2033, up from mid-teens penetration today.

Audio-text systems hold about 25% share, remaining vital for call centers, IVR modernization, and real-time transcription, but growing more steadily than newer modalities. Smaller niches—such as pure text conversational AI, emotion-recognition layers, and synthetic voice engines—together represent roughly 33% combined share, serving specialized needs like compliance monitoring, brand voice replication, and accessibility tools. These segments are not dominant individually but collectively broaden the ecosystem by enabling highly tailored industry solutions.

• In 2025, a major global cloud provider rolled out enterprise-grade video-language tooling that automatically generated chapter markers, searchable transcripts, and scene summaries for corporate training libraries used by more than 8 million employees worldwide.

Customer experience and support is the leading application area, representing about 45% of total usage, as organizations prioritize faster resolution times, 24/7 availability, and consistent service quality across chat, voice, and social channels. AI triage, sentiment detection, and automated ticket handling have made this segment mission-critical for telecom, banking, and e-commerce firms that process millions of interactions daily.

The fastest-growing application is sales and marketing automation (around 26% CAGR), propelled by personalized outreach, AI-driven lead scoring, and conversational commerce. Brands are increasingly using AI assistants to qualify leads, recommend products in real time, and close transactions within messaging apps, reducing dependence on human sales teams.

Operations and workflow automation accounts for roughly 25% combined share across use cases such as HR onboarding, IT help desks, procurement coordination, and field-service scheduling. Meanwhile, knowledge management and employee productivity tools are emerging rapidly, helping firms structure internal data, summarize meetings, and retrieve policies instantly through AI search and chat interfaces.

Consumer adoption is also reshaping demand: in 2025, over 38% of enterprises globally reported piloting AI-powered communications systems for customer experience, while more than 60% of Gen Z consumers indicated greater trust in brands that use multimodal AI chatbots for transparent, responsive support.

• In 2025, the World Health Organization documented that AI-powered digital triage and patient communication tools were active in over 150 hospitals globally, supporting early detection workflows for more than 2 million patients.

Large enterprises are the leading end-user segment with about 48% share, reflecting their ability to invest in data infrastructure, compliance frameworks, and custom AI models. Multinational firms use AI communications not only for customer support but also for internal coordination across distributed workforces, making this group structurally dominant.

The fastest-growing end-user category is small and medium-sized enterprises (estimated ~24% CAGR), fueled by low-code platforms, plug-and-play AI agents, and subscription-based pricing that lowers barriers to entry. Cloud-native SMEs in retail, logistics, and professional services are adopting AI chat, voice, and workflow tools to compete with larger players without expanding headcount.

Other contributors include public sector and government (≈15% share)—where AI is used for citizen services, grievance handling, and multilingual outreach—and healthcare providers (≈12% share), which deploy AI for appointment management, patient follow-ups, and administrative automation. In the U.S., 42% of hospitals were testing AI systems that integrate imaging data with patient records in 2025, illustrating cross-modal communication use cases beyond traditional chat.

Adoption trends show that 38% of enterprises worldwide were piloting AI communications platforms in 2025, while younger consumers increasingly expect AI-enabled, always-on brand interactions.

• A 2025 industry survey found that AI adoption among retail-focused SMEs rose by 22%, enabling more than 500 companies to streamline inventory coordination and personalize customer engagement at scale.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 20.5% between 2026 and 2033.

In 2025, North America deployed more than 1.2 million AI-enabled customer agents across enterprises, supported by over 45 hyperscale data centers optimized for real-time inference. Europe represented roughly 26% of global demand, driven by compliance-first architectures and sovereign cloud expansion, while Asia-Pacific contributed about 24% of total market usage, led by mobile commerce and digital payments. South America held approximately 7% share, with Brazil alone hosting over 180 large-scale AI contact center deployments. The Middle East & Africa region accounted for about 5% of global usage, but witnessed rapid pilot activity in smart cities, telecom, and energy sectors. By 2033, enterprise penetration of AI communications is projected to exceed 75% in North America, 68% in Europe, and 72% in Asia-Pacific, reflecting deep digital transformation across all major economies.

North America remains the most mature market, representing about 38% of global adoption in 2025, underpinned by deep cloud integration, advanced AI research ecosystems, and high enterprise digitization. The banking, financial services, healthcare, and telecom sectors are primary demand drivers, collectively accounting for more than half of regional usage due to high interaction volumes and strict service-level requirements. Large U.S. and Canadian firms are standardizing AI triage, sentiment analytics, and automated compliance monitoring across contact centers, reducing manual review workloads by roughly 25–30%. Government support for AI innovation—through research grants, sandbox programs, and federal cloud modernization initiatives—has accelerated deployment in public services and defense supply chains. Technologically, the region leads in generative voice systems, low-latency real-time translation, and multimodal analytics integrated with CRM platforms. Several local providers are investing heavily in agentic AI that can autonomously resolve complex customer tickets without human escalation. Consumer behavior in the region skews toward higher enterprise adoption in healthcare and finance, where reliability, explainability, and security are prioritized over cost alone.

Europe accounted for roughly 26% of global usage in 2025, with Germany, the United Kingdom, and France emerging as the most advanced markets. Germany leads in industrial and automotive applications, the UK in fintech and public services, and France in retail and e-commerce automation. Strong regulatory oversight from bodies such as data protection authorities and the EU AI Act framework is pushing vendors toward explainable, auditable, and privacy-preserving AI architectures. Many enterprises are migrating from public clouds to hybrid or sovereign cloud environments to comply with data localization requirements. Adoption of emerging technologies such as on-device AI inference, encrypted analytics, and federated learning is rising rapidly, particularly in healthcare and government. Sustainability initiatives are also shaping procurement, with organizations favoring energy-efficient AI models and green data centers. Local European firms are building multilingual conversational platforms optimized for regional languages, enabling seamless cross-border customer support. Consumer behavior reflects regulatory pressure that increases demand for explainable AI-powered systems, with businesses prioritizing transparency and auditability over speed alone.

Asia-Pacific is the fastest-expanding region by volume of new deployments, led by China, India, Japan, South Korea, and Southeast Asia. The region hosts some of the world’s largest digital ecosystems in e-commerce, fintech, and super-app platforms, creating massive demand for scalable AI communications. China leads in large-scale AI voice assistants and smart city pilots, while India is rapidly deploying AI chatbots across banking, government services, and telecom. Japan emphasizes high-accuracy speech AI for aging populations, and South Korea is advancing real-time translation and holographic customer service. Infrastructure investment in 5G networks, edge computing nodes, and AI data centers is accelerating regional capacity for low-latency applications. Innovation hubs in Singapore, Bengaluru, Shenzhen, and Tokyo are producing startups focused on multilingual AI, payment-linked chat systems, and conversational commerce. Local technology giants are embedding AI agents directly into mobile apps used by hundreds of millions of consumers. Regional behavior is heavily driven by e-commerce and mobile AI apps, where users expect instant, always-on digital support.

South America represented about 7% of global market usage in 2025, with Brazil and Argentina serving as the primary centers of activity. Brazil accounts for nearly 60% of regional deployments, driven by large telecom operators, digital banks, and government digitization programs. Argentina is emerging as a hub for AI talent and Spanish-language conversational platforms. Regional infrastructure improvements—including expanded fiber networks and cloud availability—are enabling faster real-time AI services, particularly in urban centers. The energy and utilities sector is adopting AI communications for outage management, customer billing queries, and field-service coordination. Governments are promoting digital inclusion initiatives that encourage AI-enabled citizen services in healthcare, taxation, and social programs. Several Brazilian startups are developing Portuguese-first AI assistants tailored to local dialects and regulatory requirements. Consumer demand is closely tied to media and language localization, with strong preference for AI systems that understand regional accents and cultural context.

The Middle East & Africa region held about 5% share in 2025, but is experiencing rapid modernization across oil & gas, construction, telecom, and public services. The UAE and Saudi Arabia are leading adoption through national AI strategies, smart city projects, and large-scale digital government platforms. South Africa is advancing AI communications in banking, retail, and mining operations, focusing on multilingual customer engagement. Energy companies are deploying AI assistants for field coordination, predictive maintenance alerts, and contractor management. Regional telecom operators are upgrading call centers with AI routing and real-time translation to serve diverse populations. Trade partnerships and investment zones in the Gulf are attracting global AI vendors to build localized data centers and research labs. Several Middle Eastern technology firms are developing Arabic-first conversational platforms optimized for formal and dialectal speech. Consumer behavior varies widely, but urban populations increasingly favor mobile-first AI services, while enterprises prioritize secure, cloud-based automation.

United States — 30% Market Share: Dominates due to large hyperscale cloud capacity, deep enterprise AI integration, and high demand from healthcare and finance.

China — 18% Market Share: Leads in deployment scale because of massive mobile ecosystems, government digital programs, and strong domestic AI platforms.

The AI-Powered Communications Platforms market features a highly competitive and partly consolidated landscape, with both global technology giants and specialized vendors vying for leadership. An estimated 60+ active competitors are engaged in delivering AI communication capabilities, encompassing conversational AI, voice assistants, messaging APIs, and multimodal interaction systems. Leading firms leverage robust AI R&D investments exceeding hundreds of millions annually, while numerous agile startups introduce niche innovations in voice recognition, sentiment analysis, and real-time translation. The top 5 companies collectively hold approximately 48–55% of overall deployment influence, indicating notable concentration among established players, but a broad long tail of challengers persists.

Strategic initiatives include ongoing partnerships between cloud hyperscalers and enterprise software integrators, product launches of advanced agentic AI suites, and M&A activity aimed at bolstering AI-native capabilities within broader communications portfolios. For example, traditional cloud and CRM platform providers are integrating large language model (LLM) enhancements directly into contact center and customer engagement workflows, resulting in measurable improvements in interaction quality and automation coverage. Innovation trends shaping competition include multimodal AI that unifies text, voice, and visual channels, low-latency telephony AI agents, and privacy-first conversational architectures suitable for regulated industries. Competitive differentiation now hinges on integration flexibility, multilingual support, and domain-specific compliance features, compelling vendors to deepen ecosystems with analytics providers, systems integrators, and telecom partners.

Anthropic

Amazon Web Services (Lex & Bedrock)

Salesforce (Einstein)

IBM (Watson Assistant)

Nuance Communications

SAP (Conversational AI)

Kore.ai

Rasa Technologies

Gupshup

Haptik

SoundHound

AI-Powered Communications Platforms are propelled by a convergence of advanced technologies that enable automated, intelligent interactions across text, voice, and visual channels. Large Language Models (LLMs) form the core technology, enabling natural language understanding, context retention, and generative dialogue capabilities. These models are increasingly integrated with speech recognition and synthesis technologies to support seamless real-time voice conversations, automated transcription, and voice-driven agent assist features. Multimodal AI frameworks—capable of interpreting text, audio, and visual inputs simultaneously—are gaining traction, particularly for use cases such as document-based support, visual troubleshooting, and video interaction summarization.

Real-time data pipelines embedded with AI inference accelerators and low-latency processing stacks are critical for ensuring responsive communications in contact centers and messaging platforms, especially where latency under 500 ms is required for acceptable user experience. Hybrid architectures combining edge computing and cloud-based AI inference are also emerging, enabling organizations to handle privacy-sensitive interactions locally while retaining cloud-level intelligence for heavy compute tasks. Semantic analytics and sentiment-aware routing technologies allow systems to dynamically prioritize interactions based on customer mood and urgency, enhancing quality of service metrics.

Providers are also embedding domain-specific NLP models—trained on industry lexicons and compliance guidelines—to support specialized sectors such as healthcare, finance, and public services, where regulatory constraints and contextual accuracy are paramount. Integrations with CRM, ERP, and workforce management systems are now standard, enabling unified data flows and automated workflow orchestration. Furthermore, open APIs and plug-in ecosystems facilitate extensibility, allowing third-party developers to build custom agents, connectors, and analytics modules tailored to enterprise needs. These technologies collectively shift communications from static, rule-based systems to adaptive, intelligent platforms that can scale across languages, industries, and interaction channels.

• In May 2025, Twilio unveiled its next-generation Customer Engagement Platform at SIGNAL 2025, enhancing conversational AI with ConversationRelay (general availability) and Conversational Intelligence (voice GA and messaging beta), alongside plans to roll out RCS, WhatsApp Business Calling, and a Compliance Toolkit to support trusted, compliant communications across channels for over 335,000 customer accounts and 10M+ developers. Source: www.twilio.com

• In October 2025, Salesforce launched Agentforce IT Service, enabling 24/7 conversational resolution of IT tickets via autonomous AI agents integrated directly with enterprise systems like Slack, automating incident and service request handling with 100+ pre-built connectors to major platforms including Google, IBM, Microsoft, Oracle NetSuite, Workday, and Zoom. Source: www.salesforce.com

• In October 2025, Tata Communications announced the launch of its Voice AI platform designed to transform BFSI customer journeys with an industry-first speech-to-speech solution, supporting 40+ languages and sub-500 ms latency interactions to deliver context-aware, multilingual engagement across channels. Source: www.prnewswire.com

• In October 2025, Salesforce and OpenAI expanded their strategic partnership to integrate OpenAI’s Frontier models with Salesforce’s Agentforce 360, enabling enterprises to access advanced AI reasoning, voice, and multimodal capabilities directly within CRM workflows and conversational interfaces for enhanced employee and customer experiences across sales, service, and commerce. Source: www.salesforce.com

The AI-Powered Communications Platforms Market Report offers a comprehensive evaluation of technologies, applications, regional dynamics, and user adoption patterns shaping the future of intelligent digital interaction systems. It encompasses technology segmentations such as conversational AI engines, voice analytics, multimodal interaction frameworks, speech-to-text/text-to-speech systems, and integration toolkits, detailing functional capabilities and deployment models. The report examines application domains including customer engagement, enterprise workflow automation, sales and marketing communication, internal collaboration, and compliance automation, highlighting how AI platforms streamline processes and enhance engagement.

Regional analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, profiling market volume distributions, infrastructure readiness, regulatory landscapes, and innovation ecosystems. The report also includes end-user insights across large enterprises, SMEs, government bodies, healthcare providers, and technology service firms, outlining adoption behaviors, priority drivers, and usage patterns. Technology coverage extends to emerging innovations such as agentic AI assistants, real-time sentiment routing, low-latency telephony AI, hybrid edge-cloud deployments, and industry-specific NLP adaptations tailored for regulated sectors.

Strategic focus areas include competitive benchmarking, partner ecosystems, platform extensibility, and integration trends with CRM and enterprise suite providers. The scope further identifies niche opportunities in multilingual support, privacy-preserving compute patterns, and verticalized AI solutions, delivering actionable intelligence for decision-makers prioritizing scalability, automation, and compliance in the evolving landscape of AI communications.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,289.0 Million |

| Market Revenue (2033) | USD 9,100.3 Million |

| CAGR (2026–2033) | 18.83% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | OpenAI, Google (Gemini), Microsoft (Copilot/Azure AI), Anthropic, Amazon Web Services (Lex & Bedrock), Salesforce (Einstein), IBM (Watson Assistant), Nuance Communications, SAP (Conversational AI), Kore.ai, Rasa Technologies, Gupshup, Haptik, SoundHound |

| Customization & Pricing | Available on Request (10% Customization Free) |