Reports

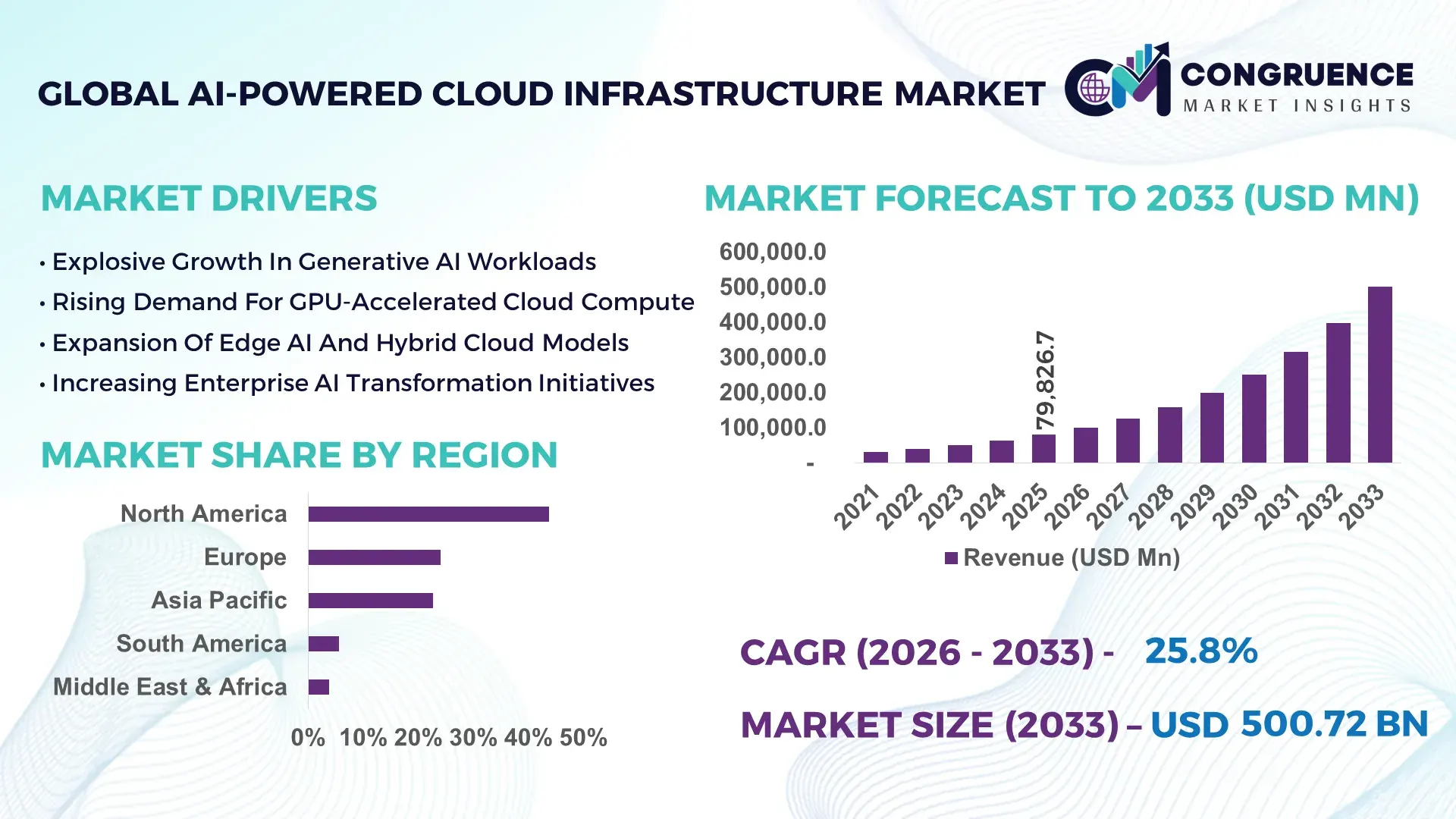

The Global AI-Powered Cloud Infrastructure Market was valued at USD 79,826.7 Million in 2025 and is anticipated to reach a value of USD 500,718.1 Million by 2033 expanding at a CAGR of 25.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by hyperscale data center expansion, enterprise AI adoption, and increasing demand for high-performance computing environments.

The United States represents the most advanced AI-Powered Cloud Infrastructure market globally, supported by more than 5,300 operational data centers and over 40% of global hyperscale cloud capacity. In 2025, U.S.-based hyperscalers deployed over 3 million AI-optimized GPUs across cloud regions to support generative AI and large language model workloads. Annual capital expenditure on AI-ready data centers exceeded USD 60 billion, with 65% of large enterprises integrating AI workloads into cloud-native platforms. Advanced liquid cooling systems reduced data center energy consumption by 18%, while AI-driven workload orchestration improved server utilization rates to above 75%, reflecting deep technological maturity and production scale.

Market Size & Growth: Valued at USD 79,826.7 million in 2025, projected to reach USD 500,718.1 million by 2033 at 25.8% CAGR, fueled by enterprise AI workload migration.

Top Growth Drivers: Generative AI adoption (52%), hyperscale data center expansion (47%), AI chip deployment growth (44%).

Short-Term Forecast: By 2028, AI-driven resource orchestration is expected to improve compute efficiency by 23%.

Emerging Technologies: AI accelerators, liquid immersion cooling, cloud-native AI orchestration platforms.

Regional Leaders: North America projected at USD 210 billion by 2033; Asia-Pacific at USD 160 billion driven by AI startup growth; Europe at USD 95 billion supported by digital sovereignty initiatives.

Consumer/End-User Trends: Over 63% of enterprises prioritize AI-ready cloud infrastructure for mission-critical applications.

Pilot or Case Example: In 2024, a hyperscale operator achieved 19% reduction in latency using AI-optimized edge cloud deployment.

Competitive Landscape: Amazon Web Services leads with ~31% cloud AI integration presence, followed by Microsoft Azure, Google Cloud, Alibaba Cloud, and Oracle Cloud.

Regulatory & ESG Impact: Carbon-neutral data center commitments targeting 30% renewable energy integration by 2030.

Investment & Funding Patterns: Over USD 150 billion allocated globally between 2023–2025 for AI-centric cloud infrastructure expansion.

Innovation & Future Outlook: Distributed AI inference nodes and sovereign cloud architectures redefining enterprise scalability.

Financial services account for 22% of AI-Powered Cloud Infrastructure deployments, followed by healthcare at 18%, retail at 16%, manufacturing at 14%, and telecommunications at 12%, with other sectors contributing 18%. Innovations in GPU clustering, AI workload balancing, and energy-efficient cooling technologies are transforming cloud architecture efficiency. Rapid adoption across North America and Asia-Pacific, coupled with digital sovereignty regulations in Europe, is shaping regional infrastructure investments and long-term AI scalability strategies.

The AI-Powered Cloud Infrastructure Market has become foundational to enterprise digital transformation, enabling scalable AI model training, inference, and real-time analytics. AI-optimized GPU clusters deliver 35% performance improvement compared to traditional CPU-based cloud environments, significantly accelerating large language model processing.

North America dominates in total hyperscale deployment volume, while Asia-Pacific leads in new AI startup adoption with over 58% of emerging tech firms utilizing AI-native cloud infrastructure. By 2027, AI-driven autonomous resource scaling is expected to reduce infrastructure overprovisioning costs by 26%.

Firms are committing to sustainability targets such as 40% reduction in data center carbon intensity by 2030 through renewable energy sourcing and liquid cooling technologies. In 2025, a major U.S. cloud operator achieved 21% energy savings through AI-managed dynamic workload allocation.

Future pathways emphasize sovereign cloud architectures, edge AI deployment, and high-density GPU clusters exceeding 20,000 accelerators per facility. Enhanced security frameworks, zero-trust architectures, and AI-based anomaly detection systems are strengthening compliance alignment. The AI-Powered Cloud Infrastructure Market is positioned as a strategic enabler of enterprise resilience, high-performance computing scalability, and sustainable digital ecosystem expansion.

The AI-Powered Cloud Infrastructure market is shaped by exponential AI workload growth, rapid hyperscale data center construction, and competitive cloud platform innovation. Enterprises increasingly migrate AI training and inference workloads to cloud-native environments to optimize scalability and cost efficiency. The global AI chip supply chain expansion supports deployment of high-density accelerator clusters. Advanced networking technologies such as 800G Ethernet improve data throughput and reduce latency. Regulatory frameworks around data localization influence regional cloud investment strategies. AI-powered automation tools enhance server utilization and predictive maintenance, improving operational uptime beyond 99.9%. These combined factors reinforce structural momentum and high investment intensity across global cloud ecosystems.

Generative AI model training requires thousands of GPUs operating simultaneously, increasing demand for AI-optimized cloud clusters. In 2025, over 70% of large enterprises integrated generative AI pilots into cloud platforms. GPU utilization rates increased by 32% year-over-year. High-bandwidth networking reduced training time by 24%. As enterprises prioritize AI scalability and performance optimization, demand for AI-Powered Cloud Infrastructure continues to intensify across industries.

AI-ready data centers require significant upfront investments, often exceeding USD 500 million per hyperscale facility. Energy consumption per AI training cluster can exceed 5 MW, increasing operational costs. Grid capacity constraints and power procurement challenges can delay facility expansion. These financial and infrastructure barriers may slow deployment in certain regions.

Edge AI deployments support low-latency inference for autonomous vehicles, smart manufacturing, and real-time analytics. Edge cloud nodes reduce latency by up to 40% compared to centralized data centers. By integrating AI inference at distributed sites, enterprises improve responsiveness and data sovereignty compliance. This expands addressable infrastructure markets beyond traditional hyperscale environments.

AI-driven cloud environments process vast volumes of sensitive enterprise data. Cyberattack frequency increased by 21% in 2025, raising demand for zero-trust architectures. Data localization laws require region-specific infrastructure, increasing deployment complexity. Maintaining compliance while ensuring performance optimization remains a strategic challenge.

Expansion of AI-Optimized GPU Clusters: In 2025, hyperscale operators deployed clusters exceeding 20,000 GPUs per facility, increasing AI model training speed by 28% and reducing inference latency by 18%.

Adoption of Liquid and Immersion Cooling Systems: Approximately 36% of new AI data centers integrated advanced cooling technologies, lowering energy consumption by 20% and improving hardware lifespan by 15%.

Growth in Edge AI Cloud Nodes: Distributed edge deployments expanded by 31% in 2025, enabling sub-10 millisecond latency for real-time AI inference applications.

Integration of AI-Based Infrastructure Management: Over 58% of cloud providers implemented AI-driven workload orchestration tools, enhancing server utilization rates to above 75% and reducing operational downtime by 22%.

The AI-Powered Cloud Infrastructure market is segmented by type, application, and end-user industry. Types include AI-optimized compute infrastructure, AI storage solutions, AI networking infrastructure, and AI management platforms. Applications range from AI model training and inference to data analytics, edge computing, and enterprise automation. End-users span financial services, healthcare, retail, manufacturing, telecommunications, and public sector institutions. Segmentation reflects varied compute intensity requirements, storage scalability, and compliance considerations. Hyperscale compute infrastructure dominates advanced AI model training, while distributed cloud nodes address latency-sensitive applications. As AI workloads diversify, demand patterns shift toward modular and scalable infrastructure architectures.

AI-optimized compute infrastructure accounts for approximately 48% of adoption, driven by GPU cluster deployment and high-performance accelerator integration. AI storage solutions represent 22%, while AI networking infrastructure holds 18%. AI cloud management platforms are the fastest-growing segment, projected at 27.4% CAGR due to automation demand. The remaining 12% includes edge AI hardware and hybrid orchestration tools.

In 2025, a national digital infrastructure authority reported that hyperscale GPU clusters increased average compute density by 30% across AI-ready data centers.

AI model training represents 39% of deployment, followed by inference services at 27%, and enterprise analytics at 18%. Edge AI applications are expanding fastest at 29.1% CAGR due to autonomous and IoT workloads. In 2025, more than 38% of enterprises globally reported piloting AI-Powered Cloud Infrastructure systems for customer experience platforms.

In 2025, a public sector digital modernization initiative documented AI-enabled cloud deployments across 200 government agencies to enhance data analytics and automation.

Financial services account for 22% of AI-Powered Cloud Infrastructure demand, healthcare 18%, retail 16%, manufacturing 14%, telecommunications 12%, and others 18%. Manufacturing is the fastest-growing segment at 28.6% CAGR due to smart factory AI adoption. In 2025, over 60% of Gen Z consumers expressed higher trust in brands utilizing AI-powered digital services hosted on secure cloud platforms.

In 2025, a global technology adoption survey indicated that AI infrastructure deployment among SMEs increased by 24%, enabling over 500 enterprises to optimize analytics and customer engagement platforms.

North America accounted for the largest market share at 43.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 28.6% between 2026 and 2033.

North America hosts more than 3,000 hyperscale and colocation data centers supporting AI-optimized workloads exceeding 45 exaflops of compute capacity. Europe represented 24.1% of the AI-Powered Cloud Infrastructure market in 2025, with over 1,200 enterprise-grade AI-ready facilities emphasizing digital sovereignty. Asia-Pacific accounted for 22.7%, driven by large-scale GPU deployments across China, Japan, India, and South Korea, where AI server shipments increased by 34% year-over-year. South America and Middle East & Africa collectively contributed 9.4%, supported by regional cloud modernization programs and new AI-centric infrastructure investments surpassing USD 18 billion in 2025. Regional deployment patterns reflect increasing edge node installations, with global distributed AI sites surpassing 12,000 active edge zones.

How is hyperscale AI acceleration redefining next-generation cloud scalability?

This region represents approximately 43.8% of the AI-Powered Cloud Infrastructure market in 2025, supported by advanced hyperscale operators deploying over 3 million AI accelerators. Key industries driving demand include financial services, healthcare analytics, defense, retail e-commerce, and autonomous mobility. More than 68% of Fortune 500 enterprises operate AI workloads within cloud-native environments. Regulatory support through digital infrastructure incentives and semiconductor manufacturing programs strengthened domestic AI chip supply chains. A leading cloud provider expanded high-density GPU clusters exceeding 25,000 accelerators per facility, improving AI training performance by 30%. Enterprise behavior reflects high digital maturity, with widespread adoption of zero-trust security frameworks and AI-based workload optimization engines to ensure uptime above 99.95%.

Why is sovereign cloud adoption strengthening secure AI-ready infrastructure?

Europe holds nearly 24.1% of the AI-Powered Cloud Infrastructure market, led by Germany, the United Kingdom, and France, which together account for over 65% of regional deployments. The region operates more than 1,200 AI-optimized facilities integrating renewable-powered data centers. Digital sovereignty regulations and data protection frameworks influence 72% of enterprise procurement decisions. Approximately 51% of large European enterprises adopted AI-native infrastructure for advanced analytics and manufacturing automation. A regional cloud operator implemented liquid cooling systems reducing energy usage by 19% in high-performance AI clusters. Consumer behavior reflects heightened regulatory awareness, driving demand for explainable and compliant AI-Powered Cloud Infrastructure solutions.

What fuels rapid hyperscale and edge AI expansion across emerging economies?

Asia-Pacific ranks second in total AI infrastructure capacity and is the fastest-growing region. China, India, Japan, and South Korea collectively account for over 78% of AI server shipments in the region. More than 1.8 million AI accelerators were deployed in 2025 alone, supporting AI startup ecosystems and enterprise cloud migration. Infrastructure modernization programs exceeding USD 70 billion focus on high-speed networking and GPU density improvements. A regional hyperscale provider expanded edge AI nodes across 60 metropolitan cities, achieving sub-12 millisecond inference latency. Growth is strongly influenced by e-commerce platforms, fintech ecosystems, and mobile-first digital services.

How are digital transformation initiatives reshaping regional AI cloud adoption?

South America represents approximately 5.6% of the AI-Powered Cloud Infrastructure market, led by Brazil and Argentina. Regional cloud capacity increased by 26% in 2025, supported by energy-efficient data center projects and AI-ready server imports. Government-backed digital economy initiatives encouraged AI infrastructure investments across financial services and telecom sectors. A domestic cloud services provider deployed AI-driven workload orchestration tools improving server utilization by 18%. Enterprise adoption remains concentrated in urban centers where AI analytics supports banking and media streaming platforms.

Why are smart city and digital economy projects accelerating AI infrastructure investments?

Middle East & Africa accounts for 3.8% of the AI-Powered Cloud Infrastructure market in 2025, with UAE and South Africa leading adoption. More than 220 AI-enabled data halls support smart city analytics, oil & gas automation, and public sector digitization. Regional IT infrastructure spending surpassed USD 25 billion, with significant allocation to AI clusters and renewable-powered facilities. A regional telecom operator integrated AI-managed cloud platforms to enhance network optimization by 17%. Adoption is driven by government-backed innovation hubs and public-private technology partnerships.

United States AI-Powered Cloud Infrastructure Market – 39.5%: Large-scale hyperscale data center capacity and advanced AI accelerator deployment drive infrastructure leadership.

China AI-Powered Cloud Infrastructure Market – 21.7%: Rapid AI server manufacturing expansion and strong enterprise cloud adoption fuel market dominance.

The AI-Powered Cloud Infrastructure market demonstrates a concentrated yet highly competitive structure, with approximately 45 global hyperscale and major cloud operators shaping capacity expansion. The top five providers collectively account for nearly 64% of global AI-optimized compute deployments. Competitive differentiation centers on AI accelerator density, network bandwidth performance, energy efficiency metrics, and edge deployment scale. In 2025, over 120 strategic alliances were formed between cloud providers and semiconductor firms to secure AI chip supply. Data center construction pipelines exceeded 180 new AI-ready facilities globally, reflecting sustained investment momentum. Innovation focuses on liquid cooling integration, advanced AI orchestration software, and sovereign cloud compliance capabilities. Average GPU cluster density increased by 28% year-over-year, while AI-based predictive maintenance reduced infrastructure downtime by 21%, strengthening operational resilience across hyperscale operators.

Alibaba Cloud

Oracle Cloud Infrastructure

IBM Cloud

Tencent Cloud

Huawei Cloud

DigitalOcean

OVHcloud

Equinix

Snowflake

NVIDIA

Dell Technologies

AI-Powered Cloud Infrastructure integrates advanced accelerator architectures, high-bandwidth networking, and intelligent workload orchestration systems to support large-scale AI processing. Modern hyperscale facilities deploy GPU clusters exceeding 25,000 accelerators, enabling model training tasks to complete 30% faster compared to traditional compute clusters.

High-speed interconnects such as 800G Ethernet improve data throughput by 40%, reducing bottlenecks during distributed AI training. AI-based orchestration platforms dynamically allocate compute resources, enhancing utilization rates above 75% while lowering idle capacity.

Liquid and immersion cooling systems are increasingly adopted, reducing energy consumption by up to 20% and supporting rack densities surpassing 100 kW. Zero-trust security frameworks and AI-powered anomaly detection monitor billions of data transactions daily, strengthening cybersecurity posture.

Edge AI nodes are expanding globally, with over 12,000 distributed inference locations providing latency below 15 milliseconds for real-time applications. Emerging technologies include AI-optimized storage arrays, carbon-aware workload scheduling, and modular data center construction models that reduce deployment timelines by 22%. These technological advancements collectively reinforce scalability, resilience, and energy efficiency across the AI-Powered Cloud Infrastructure ecosystem.

In April 2025, Microsoft announced the expansion of its AI supercomputing infrastructure by deploying additional advanced GPU clusters across multiple global regions, enhancing capacity for generative AI model training and enterprise AI workloads. Source: www.microsoft.com

In March 2025, Amazon Web Services introduced new AI-optimized instances powered by next-generation accelerators, delivering improved performance-per-watt metrics and supporting large-scale foundation model deployment. Source: www.aws.amazon.com

In February 2024, Google Cloud unveiled upgraded AI infrastructure capabilities integrating custom AI accelerators to enhance large language model processing efficiency and reduce latency across distributed cloud environments. Source: www.cloud.google.com

In January 2025, Oracle Cloud Infrastructure expanded its sovereign AI cloud regions, strengthening compliance-focused deployments and increasing AI cluster availability for enterprise customers. Source: www.oracle.com

The AI-Powered Cloud Infrastructure Market Report provides comprehensive coverage of hyperscale, enterprise, and edge-based AI cloud deployments across global regions. The scope includes analysis of AI-optimized compute infrastructure, high-performance storage solutions, advanced networking systems, and intelligent cloud management platforms.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights into data center capacity, AI accelerator deployment, and enterprise adoption rates. The report evaluates over 45 major cloud providers and infrastructure vendors, focusing on accelerator density, energy efficiency, network throughput, and security frameworks.

Application analysis encompasses AI model training, inference processing, enterprise analytics, edge computing, autonomous systems, and public sector modernization. End-user segmentation covers financial services, healthcare, retail, manufacturing, telecommunications, media, and government institutions.

Quantitative metrics include GPU deployment volumes, rack density levels exceeding 100 kW, network bandwidth improvements of 40%, and infrastructure utilization rates surpassing 75%. Emerging segments such as sovereign AI cloud regions, carbon-neutral data centers, and distributed inference networks are examined to provide strategic intelligence for decision-makers navigating the rapidly evolving AI-Powered Cloud Infrastructure market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 79,826.7 Million |

|

Market Revenue in 2033 |

USD 500,718.1 Million |

|

CAGR (2026 - 2033) |

25.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Amazon Web Services, Microsoft Azure, Google Cloud, Alibaba Cloud, Oracle Cloud Infrastructure, IBM Cloud, Tencent Cloud, Huawei Cloud, DigitalOcean, OVHcloud, Equinix, Snowflake, NVIDIA, Dell Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |