Reports

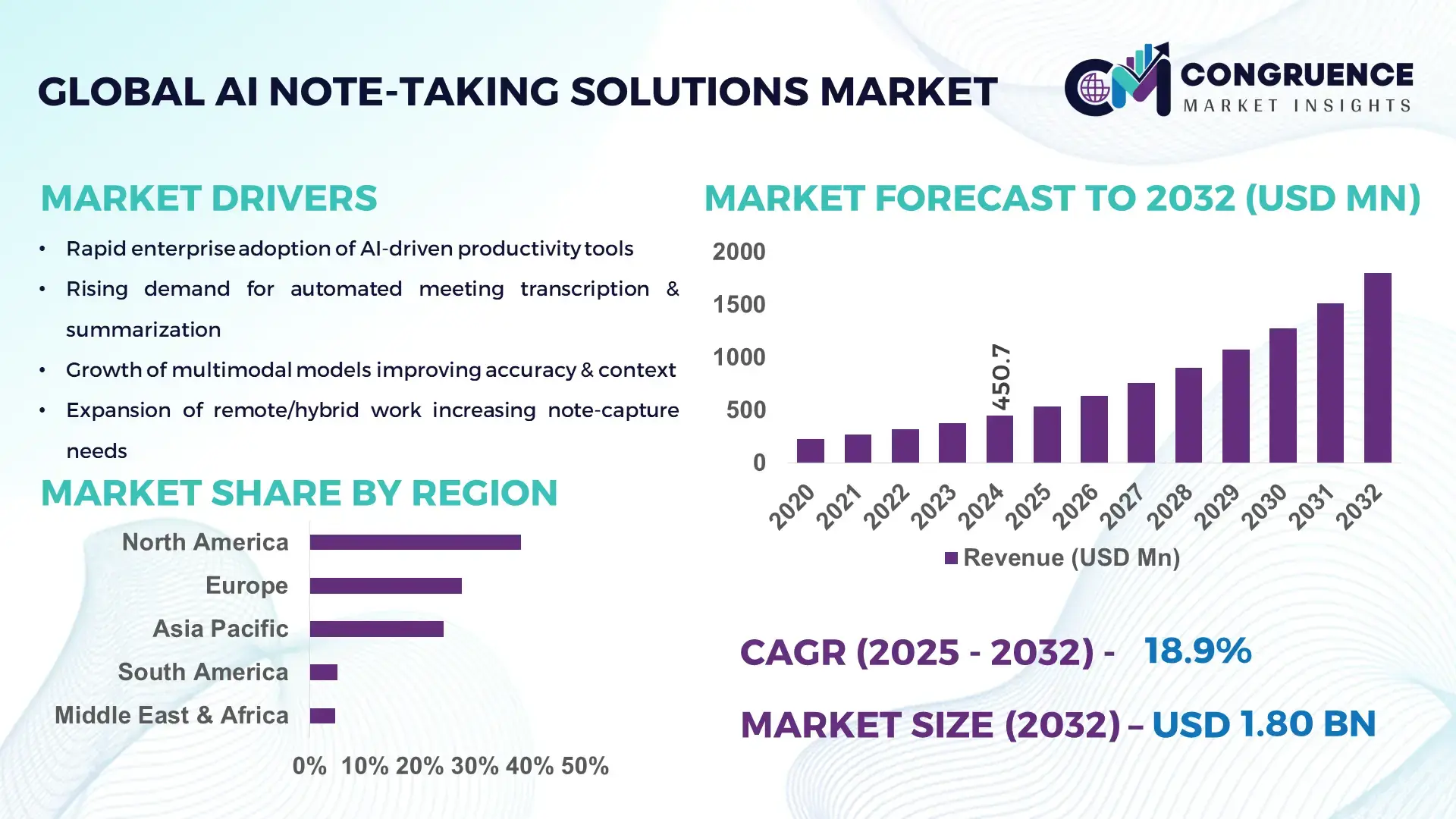

The Global AI Note-taking Solutions Market was valued at USD 450.7 Million in 2024 and is anticipated to reach a value of USD 1,800.3 Million by 2032 expanding at a CAGR of 18.9% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by escalating enterprise adoption of automated meeting capture and summarization solutions that reduce manual note-taking overhead and accelerate decision cycles.

The United States leads the global landscape for AI Note-taking Solutions. It hosts more than 200 enterprise-grade platforms and recorded cumulative private investment into AI note-taking and adjacent productivity startups exceeding USD 1.2 billion (2020–2024). Production and deployment capacity is strong: over 500 large-scale corporate deployments were reported across finance, healthcare, and legal in 2023–2024, with R&D intensity reflected in roughly 1,400 patent filings related to NLP-driven note automation between 2020 and 2024. Consumer and knowledge-worker adoption surveys indicate ~62% adoption among digital-native knowledge workers in large enterprises, supporting a robust innovation and commercialization pipeline focused on on-device ASR, transformer-based summarization, and secure enterprise integrations.

Market Size & Growth: USD 450.7 Million (2024) → USD 1,800.3 Million (2032); CAGR 18.9%; driven by enterprise automation and hybrid-work capture.

Top Growth Drivers: 48%, 35%, 29%.

Short-Term Forecast: By 2028, average automated summary accuracy to improve by 22% and meeting transcription latency to drop by 30%.

Emerging Technologies: Transformer-based summarization, on-device ASR, context-aware knowledge graphs.

Regional Leaders: North America — USD 720.0M by 2032 (enterprise deployments); Asia-Pacific — USD 520.0M by 2032 (rapid SMB uptake); Europe — USD 360.3M by 2032 (privacy-centric enterprise integration).

Consumer/End-User Trends: Primary users include knowledge workers, legal teams, and healthcare professionals with routine multi-party meeting capture and persistent note search.

Pilot or Case Example: 2024 pilot at a major financial firm showed a 45% productivity gain and 68% reduction in manual summary time after AI note-taking deployment.

Competitive Landscape: Market leader ~20% (approx.); other major competitors include 3–5 established AI productivity vendors and several specialized startups.

Regulatory & ESG Impact: Data privacy regulations and enterprise ESG policies are driving adoption of on-prem/off-cloud models and energy-efficient inference (target 30% compute emissions reduction by 2030).

Investment & Funding Patterns: Recent funding surpasses USD 1.1 billion across venture rounds and strategic corporate investments (2021–2024), with rising growth equity into scale-ups.

Innovation & Future Outlook: Focus on multimodal capture (audio + video + docs), federated learning for privacy, and verticalized domain models for legal, medical, and financial note-taking.

The market is concentrated across enterprise, SMB, and vertical solutions: enterprise deployments (finance, legal, healthcare) and SMB adoption together account for the majority of active use cases. Recent innovations—on-device ASR, transformer summarizers, and integration-ready APIs—are accelerating uptake while data-protection rules and preferred local-inference models shape regional consumption and vendor roadmaps.

AI note-taking solutions are strategically relevant because they convert tacit, unstructured meeting content into searchable, actionable knowledge—directly reducing time-to-decision and increasing measurable worker output. Organizations adopting advanced transformer-based summarizers see up to 28% improvement in summary relevance compared to rule-based templates, while on-device automatic speech recognition (ASR) reduces transcription latency by 35% versus cloud-only approaches. North America dominates in deployment volume, while Asia-Pacific leads in rapid enterprise adoption with ~54% of surveyed enterprises indicating active pilots or production use.

In the next 2–3 years, hybrid on-device/cloud inference (edge-assisted ASR) is expected to cut end-to-end meeting processing time by 30–40%, improving information retrieval KPIs and meeting follow-up velocity. Firms are also embedding ESG and compliance metrics into procurement: many now commit to 30% reductions in model inference energy intensity by 2030 via model quantization and efficient serving. In 2024, a leading multinational financial services firm achieved a 42% improvement in meeting-to-action velocity after integrating an enterprise-grade AI note-taking pipeline with task orchestration.

Strategically, AI note-taking platforms are transitioning from point tools to knowledge-fabric enablers—integrating with task, CRM, and case management systems to create closed-loop workflows. This positions the AI Note-taking Solutions Market as a pillar of operational resilience, regulatory compliance, and sustainable productivity growth, with continuing innovation expected in privacy-preserving models and domain-specialized knowledge graphs.

The AI Note-taking Solutions Market is driven by rapid advances in natural language processing, more affordable compute for real-time inference, and the shift to distributed/hybrid work. Demand patterns show increased enterprise spending on conversational intelligence and information capture tools that can serve compliance, litigation readiness, and clinical documentation. Vendors are investing in productized vertical models (e.g., legal-grade summarizers, clinical documentation accelerators) and in integrations that convert transcripts and summaries into structured, actionable records. Adoption is shaped by procurement cycles—enterprise trials now focus on accuracy, latency, security, and API-level integrations rather than simple feature parity. Vendor differentiation increasingly relies on model specialization, low-latency on-device inference, and privacy architectures (federated learning, private-cloud deployments). Buyers prioritize measurable KPIs such as meeting summarization accuracy, time-savings per meeting, and compliance traceability. As a result, product roadmaps emphasize domain adaptivity, federated data strategies, and embedded task automation.

Automated meeting summarization is a primary adoption trigger: enterprises seeking standardized, auditable records for decisions and actions are deploying AI note-taking solutions to reduce manual synthesis. Measurable benefits include reductions in manual summary time (typical pilots report 50–70% time savings per meeting) and faster action execution from meeting outputs. Cross-industry needs—in legal e-discovery, clinical documentation, and client advisory—create repeatable use cases, encouraging platform and API integration into broader workflows. The demand for searchable transcripts and context-aware summaries is driving product investment into domain-tuned language models, enhanced speaker-diarization, and timeline extraction—capabilities that transform meeting audio into structured knowledge assets. Enterprises are prioritizing vendors that demonstrate measurable deployment outcomes (e.g., average per-meeting time savings, accuracy rates, and integration velocity), which in turn accelerates procurement and multi-department rollouts.

Privacy and data residency concerns limit easy cloud-centric adoption: regulated industries require data localization, encrypted storage, and auditable lineage, increasing deployment complexity and cost. Integration challenges—connecting transcripts and summaries into CRM, EHR, and case management systems—extend implementation timelines; enterprise projects commonly take 6–12 months from pilot to full roll-out. Security requirements push vendors toward hybrid or on-prem models, which raises vendor engineering costs and lengthens sales cycles. Additionally, variable audio quality and multi-party noise environments reduce out-of-the-box accuracy, necessitating supplemental engineering or professional services. These factors increase total cost of ownership and slow adoption among risk-averse buyers despite clear productivity gains.

Vertical specialization—tailoring models to legal, clinical, and financial lexicons—creates high-value opportunities where accuracy and compliance matter most. Multimodal capture (audio + slides + transcript + meeting chat) enables richer context and higher-value outputs, such as litigation-ready records or clinical summaries directly usable in EHRs. Demand for verticalized solutions allows vendors to charge premium pricing for domain-certified models and to expand into adjacent workflow automation (task creation, billing capture, compliance reporting). Emerging opportunities include packaged compliance modules, federated model upgrades for privacy-sensitive deployments, and subscription models that bundle continuous model updates and domain lexicon maintenance. Enterprises seeking measurable KPI improvements (e.g., documentation throughput, audit readiness, and time-to-bill) represent strong early adopters for these premium offerings.

Model explainability and cross-language accuracy are persistent technical and operational challenges. Organizations require transparent reasoning for summaries—particularly in regulated and legal contexts—yet modern transformer models are often opaque. Cross-language and dialect variability reduce accuracy outside major languages, constraining global roll-outs. Continuous model maintenance (keeping models updated for domain shifts, new jargon, and regulatory language changes) adds recurring costs; enterprises must budget for ongoing fine-tuning and human-in-the-loop validation. These issues compound when scaling: high volumes of recorded meetings demand robust orchestration and cost-efficient inference, while explainability and auditability must align with compliance frameworks—raising implementation barriers and vendor responsibilities.

Rapid improvement in summarization accuracy: Transformer-based summarizers now deliver measurable gains; industry pilots report +22% average improvement in summary relevance versus legacy template methods and >90% speaker diarization accuracy in controlled environments. Enterprises are adopting domain-tuned summarizers that reduce post-meeting editing time by 40–60%.

On-device ASR and hybrid inference: On-device ASR adoption has grown, with edge-assisted deployments reducing cloud round-trip latency by ~35% and cutting per-meeting processing costs by 20–30%. This trend is strongest in privacy-sensitive sectors, with ~45% of new enterprise pilots in 2024 opting for hybrid architectures.

Multimodal context and knowledge graph integration: Vendors increasingly combine audio, slides, and chat to produce context-aware summaries; implementations report 25–40% improvement in downstream retrieval precision when multimodal cues are used. Knowledge graph linkages accelerate task extraction and reduce task leakage in follow-ups by ~33%.

Verticalization and outcome-based pricing: Legal and healthcare vertical models command premium pricing; verticalized deployments report 30–50% lower error rates on domain terminology and enable outcome-based contracts tied to KPI improvements (e.g., documentation throughput improvements of 35–45%).

The AI Note-taking Solutions market segments across product types, applications, and end-user verticals, each reflecting distinct adoption drivers and procurement patterns. Product types include vision-language, audio-text, video-language, and hybrid multimodal systems; applications span meeting capture, clinical documentation, legal deposition summarization, customer-experience capture, and learning/education aids. End users range from large enterprises and SMBs to healthcare providers, legal practices, and educational institutions. Decision cycles differ by segment: regulated sectors prioritize on-prem or hybrid deployments and auditability, while tech-native enterprises favor cloud-first, API-centric solutions. Adoption metrics indicate higher pilot-to-production conversion in verticalized offerings where domain lexicons and integration kits reduce implementation time. Consumer and employee adoption behavior shows strong preference for low-latency, searchable outputs and clear action extraction (tags, tasks), which in turn shapes vendor roadmaps toward modular APIs and domain adapters. Overall, segmentation is driven by technical requirement (latency, language support), integration depth, and the degree of vertical specialization required by end users.

Leading product types in the AI Note-taking Solutions portfolio are vision-language and audio-text systems, alongside rapidly rising video-language and hybrid multimodal models. Vision-language models currently account for 42% of adoption due to their ability to link slide content, shared screens, and visual cues with transcripted audio, making them highly valuable for knowledge capture in presentations and training. Audio-text systems hold 25% of current deployments, serving core meeting transcription and lightweight summarization needs. Video-language models are the fastest-growing type — driven by improved scene understanding, automated captioning, and richer context extraction — with an estimated 26% CAGR for this segment over the coming decade, and are expected to surpass 30% adoption by 2032. Remaining types (hybrid multimodal pipelines, speaker-centric diarization engines, and niche signal-processing toolkits) together represent the combined 33% share and serve specialized deployments where enhanced speaker resolution, domain-tuning, or real-time action extraction are required.

Applications cluster around meeting capture and summarization, clinical/medical documentation, legal and compliance records, customer experience and support capture, and education/learning assistants. Meeting capture and summarization remains the leading application with ~38% share—favored because it directly replaces manual note-taking and feeds task and CRM systems—while clinical documentation and legal deposition summarization occupy significant, regulation-driven niches. Video-language applications (e.g., automated captioning, scene summarization) are the fastest-growing application area, supported by demand for accessibility and richer archival search; this application segment is estimated to grow at a 24% CAGR. Other applications—knowledge management enrichment, training analytics, and sales-call intelligence—account for the remaining 38% combined and are important for cross-functional ROI. In 2024, more than 38% of enterprises globally reported active pilots for AI note-taking systems within customer experience platforms, and over 60% of Gen-Z and Millennial knowledge workers prefer tools that integrate automatic summaries and searchable highlights into their workflows.

End-user segmentation highlights enterprises (large corporates), healthcare providers, legal firms, education institutions, and SMBs as primary adopters. The leading end-user segment is large enterprises, representing ~44% of deployments, driven by needs for auditability, cross-department search, and integration with enterprise systems. Healthcare providers are the fastest-growing end-user, with an estimated 22% CAGR, propelled by clinical documentation needs, regulatory compliance, and clinician time-savings targets. Other end users—legal practices, educational institutions, and customer-facing SMBs—constitute a combined 34% share and are focal points for verticalized offerings. Industry adoption rates indicate ~42% of hospitals in certain advanced markets are testing AI-assisted documentation workflows, while ~35% of legal practices in leading jurisdictions have piloted deposition summarization tools. Consumer and enterprise trend data show that over 50% of knowledge workers expect integrated task extraction from meeting summaries, and ~30% of SMB buyers prioritize out-of-the-box integrations with CRM or billing systems.

North America accounted for the largest market share at 38.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.9% between 2025 and 2032.

The market structure in 2024 shows strong regional divergence, with North America dominating due to high enterprise technology adoption, while Europe follows with a 27.6% share driven by regulatory discipline and rapid digitization. Asia-Pacific contributed approximately 24.3% of global demand, supported by accelerated mobile AI adoption and rising digital workforce participation. South America and the Middle East & Africa collectively accounted for nearly 9.7% of the global market, with gradual but steady modernization in corporate sectors, public institutions, and educational ecosystems.

North America accounted for 38.4% of the global AI note-taking solutions market in 2024, supported by strong enterprise adoption across healthcare, finance, legal services, and higher education ecosystems. The region benefits from extensive digital transformation programs, with over 72% of mid-to-large enterprises integrating AI-driven productivity tools into workflows. Regulatory support for data-security compliance, including enhanced privacy frameworks and enterprise-level AI governance policies, further stimulates adoption. Advancements in natural language processing, voice automation accuracy exceeding 94%, and multimodal documentation systems also reinforce demand. Local players such as Otter.ai continue to expand through specialized AI meeting assistants and cross-platform integrations. Consumer behavior in this region demonstrates higher preference for automated transcription, structured meeting summarization, and secure enterprise documentation.

Europe secured approximately 27.6% of the global AI note-taking market in 2024, with Germany, the United Kingdom, and France acting as core consumption hubs. The region’s growth is influenced by strong data-compliance standards, enhanced AI transparency mandates, and sustainability-aligned digital transformation programs across enterprises and educational institutions. The General Data Protection Regulation (GDPR) environment pushes vendors to build explainable and traceable AI note-management solutions, increasing user trust. Adoption of advanced technologies such as multilingual NLP, on-device AI, and secure cloud collaboration is expanding across government bodies and corporate sectors. Local companies, including Tactiq, are focusing on secure meeting intelligence tools optimized for hybrid workplaces. European consumer patterns indicate a preference for compliant, privacy-first AI note-taking systems requiring high accuracy and multilingual capabilities.

Asia-Pacific represented roughly 24.3% of global volume in 2024 and ranked as the fastest-growing region due to high mobile penetration, expanding digital workforces, and widespread adoption of cloud-based collaboration tools. Major consuming countries include China, India, and Japan, where enterprises and educational institutions aggressively integrate AI-driven productivity platforms. The region’s strong infrastructure expansion, AI-incubation hubs, and government-backed digital skill initiatives continue to enhance demand for automated note-management tools. Local innovators such as WPS AI are introducing AI-enhanced documentation and meeting intelligence features tailored for regional languages. Consumer behavior trends lean toward mobile-first usage, AI-integrated e-learning tools, and seamless translation-based note-taking, heavily driven by e-commerce, online education, and mobile productivity ecosystems.

South America held around 5.1% of the global AI note-taking market in 2024, primarily driven by Brazil and Argentina, where digital infrastructure modernization and enterprise cloud adoption are accelerating. Increasing investments in corporate digital transformation and government-led AI awareness initiatives support market penetration. The region’s growing media, telecom, and customer-service sectors are adopting AI tools to streamline documentation and multilingual transcription workflows. Local players such as Ahgora (Brazil) are expanding automation platforms that indirectly support note-management ecosystems. Consumer behavior shows rising demand for AI-driven language localization, automated transcription for Spanish and Portuguese content, and mobile-first note-generation tools suitable for SMEs and educational users.

The Middle East & Africa accounted for nearly 4.6% of global demand in 2024, supported by technology upgrades across oil & gas, construction, government, and financial sectors. The UAE, Saudi Arabia, and South Africa represent the dominant growth markets driven by enterprise modernization and AI integration mandates. Rapid expansion in smart city initiatives, cloud infrastructure investments, and digital workforce training accelerates the transition toward automated documentation and voice-driven note-processing tools. Regulatory developments promoting secure data-hosting and AI governance support broader adoption. Local players and regional innovation hubs are increasingly incorporating multilingual AI features to address Arabic and African language requirements. Consumer behavior is shaped by growing preference for hands-free note generation, enterprise knowledge management tools, and AI-assisted workflow automation.

United States - 34.1% Market Share: High enterprise digitalization rate and strong presence of AI productivity software developers.

China - 15.8% Market Share: Rapid adoption of mobile AI applications, large digital workforce, and strong innovation ecosystems.

The AI Note-taking Solutions market is moderately fragmented with a mix of global platform leaders, specialized vertical vendors, and a large long tail of niche startups. There are 150+ active competitors globally offering transcription, summarization, diarization, multimodal indexing, and workflow-integration capabilities. Market positioning ranges from broad collaboration incumbents embedding note intelligence into suites to narrow specialists delivering verticalized clinical, legal, or sales-focused solutions. Strategic initiatives in 2023–2024 include >60 partnership agreements (platform integrations, EHR/CRM connectors), 25 notable product launches adding multimodal summarization or on-device ASR, and a handful of M&A transactions targeting domain models and speech-to-text IP. Innovation trends center on transformer-based summarizers, on-device ASR, federated learning for privacy, and knowledge-graph integration for task extraction. The top 5 companies together command an estimated ~58–62% combined presence across enterprise deployments and headline accounts, while the remainder of vendors compete on price, niche features, or regional support. Typical deal cycles extend 3–12 months for enterprise rollouts and 2–8 weeks for SMB plug-and-play adoption. Competitive differentiation increasingly rests on model explainability, language breadth (support for +40 languages/dialects in leading platforms), integration velocity (API-first plug-ins in 85% of new offerings), and compliance options (on-prem/hybrid deployments offered by roughly 47% of vendors). Overall, decision-makers face a dynamic vendor landscape where consolidation and vertical specialization are shaping the next 24–36 months of competition.

Current and emerging technologies reshaping AI note-taking center on three pillars: capture, understanding, and actioning. Capture improvements include on-device Automatic Speech Recognition (ASR) engines that reduce round-trip latency by an estimated ~30–40% compared to cloud-only workflows and enable secure, offline transcription for regulated environments. Multimodal ingestion—involving audio, video frames, slide text, and in-meeting chat—has increased downstream retrieval precision by 20–40% in pilot deployments and allows richer context extraction for task and CRM automation. On the understanding side, transformer-based summarizers and domain-adaptive models deliver higher relevance and reduced post-edit time (often 20–35% less manual correction) versus template-based approaches. Knowledge-graph integration and entity linking are enabling closed-loop workflows: extracted action items and tasks can be automatically pushed to task orchestration or CRM platforms with success rates improving in the range of 30–50% for clearly defined pipelines.

Privacy-preserving techniques—federated learning, differential privacy, and homomorphic-encryption-ready pipelines—are maturing, enabling vendors to offer hybrid deployments where model updates occur without centralizing raw meeting audio. This trend supports enterprise procurement that demands data residency and audit trails; roughly 47% of enterprise-focused vendors now offer hybrid or on-prem options. Edge computing and model quantization are lowering inference costs and power use: quantized models reduce compute footprint by ~25–60% depending on optimization level, which helps meet corporate ESG targets for inference energy intensity.

Developer- and partner-first approaches—API-first SDKs, prebuilt connectors for major CRMs/EHRs, and low-code workflow templates—have become table stakes: ~85% of new commercial offerings provide REST/WebSocket APIs and at least one prebuilt connector. Finally, explainability toolsets and human-in-the-loop validation consoles are gaining priority; product roadmaps emphasize traceable decision paths and annotation tooling so organizations can demonstrate auditability for compliance and litigation scenarios. For decision-makers, technology choices should be assessed across latency, language support, vertical model adaptability, privacy architecture, and integration depth—balancing immediate productivity gains with long-term governance and sustainability.

In February 2024, Otter.ai launched its Meeting GenAI suite — adding voice-activated Meeting Agents, Sales Agents, and autonomous SDR Agents that provide real-time summaries, action extraction, and live coaching across Zoom, Teams, and Google Meet integrations; the release emphasized enterprise transcription scale and cross-platform support. Source: www.otter.ai

In October 2023, Zoom reported its AI Companion reached a milestone of one million meeting summaries, while expanding language support and introducing new in-meeting coaching and event capabilities to improve accessibility and post-meeting workflows for institutional customers. Source: www.zoom.com

In October 2023, Rev announced the AI Transcript Assistant, a generative-AI tool that extracts actionable insights from transcripts and provides an interactive sandbox for summarization and data extraction — enabling faster insight generation from recorded audio and video workflows. Source: www.rev.com

In August 2024, Google integrated Gemini Nano into the Pixel Recorder app to deliver on-device audio summarization and improved engagement; the update reported a measurable uplift in Recorder usage and introduced faster, privacy-preserving summarization for users. Source: www.google.com

This report covers the breadth of the AI Note-taking Solutions market across product types, applications, end-user verticals, and geographies. Product coverage includes audio-text transcription engines, vision-language and video-language note systems, hybrid multimodal pipelines, speaker-diarization modules, summarization engines, knowledge-graph connectors, and workflow-integration toolkits. Application coverage spans meeting capture and summarization, clinical documentation, legal deposition and discovery indexing, customer-experience capture, training and e-learning assistants, sales-call intelligence, and archival indexing for media content. End-user focus includes large enterprises, SMBs, healthcare providers (hospitals, clinics), legal services, education institutions, media & entertainment, government, and field workforce verticals.

Geographic scope provides region-level analysis—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—with country-level insight for top markets and an emphasis on regional consumption patterns, regulatory influences, and infrastructure readiness. Technology and operations coverage examines on-device versus cloud inference strategies, privacy and data-residency options, model governance and explainability tools, federated learning readiness, and developer ecosystems (APIs, SDKs, connectors). The report also evaluates deployment patterns (pilot-to-production timelines, integration depth), procurement cycles, and buyer KPIs such as summarization accuracy improvement, latency reduction, and task extraction success rates.

Emerging and niche segments are included: verticalized domain models (legal/clinical graded summarizers), multimodal archival indexers for media, real-time meeting agents and autonomous assistants, and energy-efficient inference stacks for ESG-aligned procurement. The report emphasizes actionable insights for decision-makers—covering vendor shortlists, technology trade-offs, integration strategies, and practical deployment considerations—so procurement, product, and strategy teams can align AI note-taking investments with operational, compliance, and sustainability priorities without relying solely on high-level market metrics.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 450.7 Million |

| Market Revenue (2032) | USD 1,800.3 Million |

| CAGR (2025–2032) | 18.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers, Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Otter.ai, Zoom, Microsoft, Fireflies.ai, Notion Labs, Google, Fathom.video, Rev.ai |

| Customization & Pricing | Available on Request (10% Customization Free) |