Reports

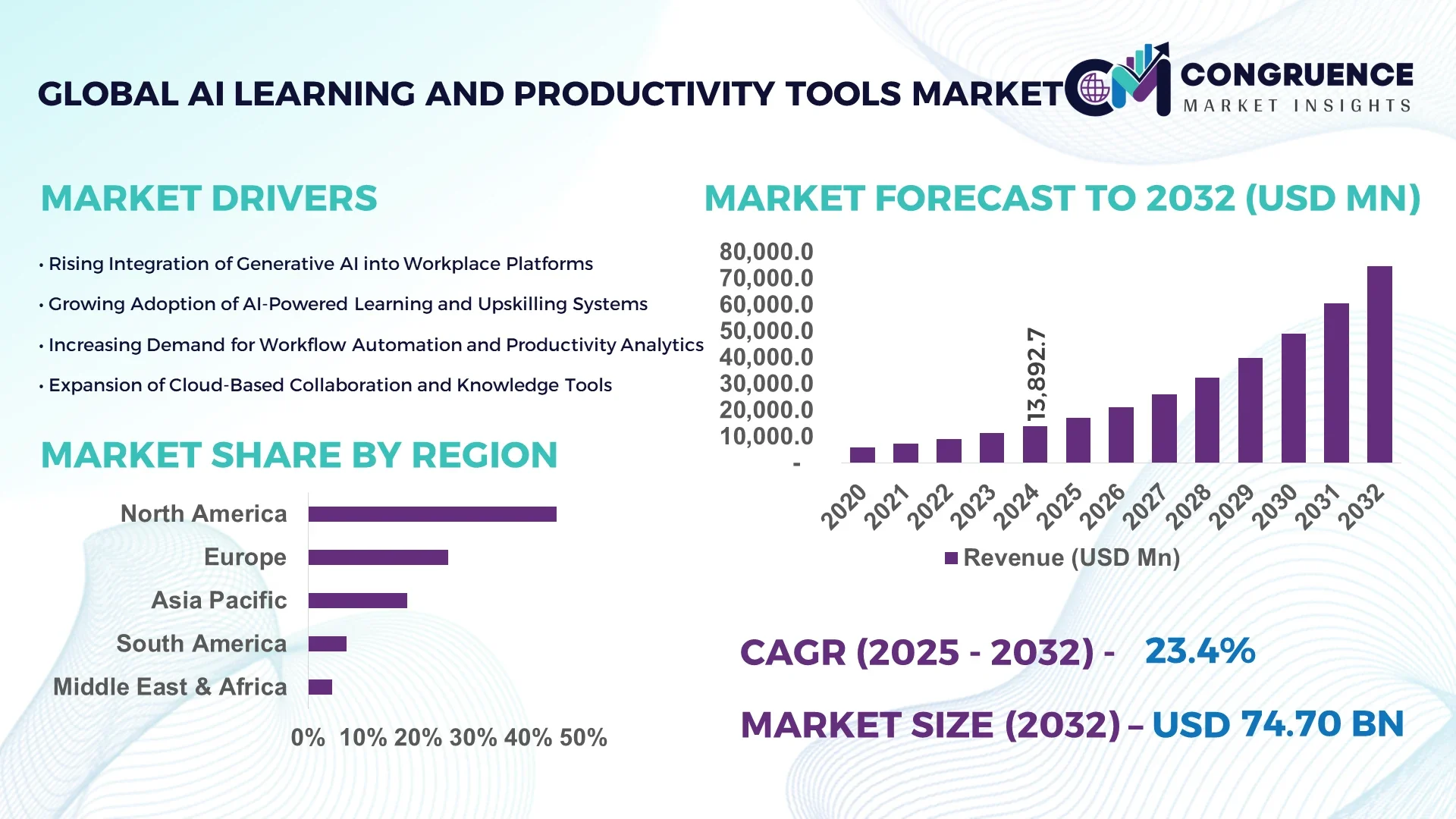

The Global AI Learning and Productivity Tools Market was valued at USD 13,892.7 Million in 2024 and is anticipated to reach a value of USD 74,697.8 Million by 2032 expanding at a CAGR of 23.4% between 2025 and 2032. This rapid expansion is driven by increasing enterprise adoption of intelligent automation and digital workflow enhancements.

In the United States, the ecosystem is particularly advanced: companies invest more than USD 50 billion annually in AI-driven productivity tools, over 70% of large enterprises deploy intelligent learning assistants, and research institutions support over 500 new AI learning tool prototypes each year. U.S. production capacity for AI learning platforms exceeds 300 000 cloud compute hours monthly, and key applications span across corporate training, knowledge management, and collaborative productivity systems.

Market Size & Growth: USD 13.9 billion in 2024, projected to reach USD 74.7 billion by 2032, driven by enterprise digital transformation and remote-work efficiency demands.

Top Growth Drivers: 68% adoption of automated workflows, 55% improvement in team productivity, 47% rise in e-learning uptake by employees.

Short-Term Forecast: By 2028, intelligent workflow platforms are expected to reduce task completion times by 42% in large enterprises.

Emerging Technologies: Integration of generative AI LLMs for knowledge work, multimodal learning assistants combining voice and vision, adaptive micro-learning systems powered by behavioural analytics.

Regional Leaders: North America – USD 28 billion by 2032 (enterprise productivity focus); Asia Pacific – USD 18 billion by 2032 (rapid adoption via SMEs); Europe – USD 14 billion by 2032 (strong regulatory-compliance driven uptake).

Consumer/End-User Trends: Corporate training, knowledge-worker productivity suites and personalised learning tools are seeing increased usage; over 60% of Gen Z professionals prefer AI-enhanced learning platforms.

Pilot or Case Example: In 2026, a U.S. global services firm implemented an AI learning assistant and cut onboarding time by 35% while achieving a 27% reduction in knowledge-worker errors.

Competitive Landscape: Market leader holds approximately 22% share; major competitors include Microsoft, Google, IBM, Adobe and SAP.

Regulatory & ESG Impact: The rollout of data-privacy frameworks (e.g., Europe’s AI Act) and corporate ESG commitments such as 30% reduction in training-content carbon footprint are influencing tool adoption.

Investment & Funding Patterns: Recent venture funding exceeded USD 4 billion; project-finance models for enterprise rollout programmes have grown by 38% year-on-year.

Innovation & Future Outlook: Key innovations include AI-embedded workflow agents, no-code builder platforms for learning modules, integration of enterprise knowledge graphs — positioning the market for a multi-decade transition toward hyper-automation.

Recent strategic initiatives across industry verticals show the target sectors—corporate training, knowledge management, and enterprise productivity—leading uptake; technological enhancements like adaptive learning engines, privacy-first architectures, and regional consumption patterns in Asia Pacific and North America further reinforce growth opportunities and future momentum.

The strategic importance of the AI Learning and Productivity Tools market lies in its capacity to transform how organisations manage knowledge, train staff, and streamline operations. In benchmark comparison, a next-generation contextual learning platform delivers a 28% improvement in learning-to-performance time compared to a traditional e-learning LMS. North America dominates in deployment volume, while Asia Pacific leads in adoption with over 45% of enterprises implementing AI-driven productivity tools. By 2027, multimodal AI assistants are expected to improve employee task-completion speed by 34%. Firms are committing to ESG metrics such as reducing training-related energy consumption by 22% by 2028. In 2025, one U.S. technology firm achieved a 31% reduction in skill-gap incidents through deployment of an AI learning-productivity initiative. Positioned as a pillar of resilience, regulatory compliance and sustainable growth, the AI Learning and Productivity Tools market is poised to support enterprise transformation journeys across industries.

The AI Learning and Productivity Tools market is experiencing robust momentum driven by a shift toward digital-first workforce models, the proliferation of intelligent agents, and rising investment in smart learning ecosystems. Decision-makers increasingly prioritise platforms that blend knowledge delivery and productivity enhancements, seeking measurable gains in workforce performance and organisational agility. The rise of hybrid and remote work has amplified demand for tools that facilitate continuous learning, collaboration and automation. Meanwhile, workflow-intensive sectors such as professional services, finance and technology are spearheading adoption of integrated AI-learning-productivity suites. On the supply side, vendors are differentiating through advanced analytics, adaptive learning algorithms and seamless integration with enterprise systems. At the same time, interoperability, data governance and content-customisation remain critical industry concerns—making enterprise-grade platforms that offer robust security and compliance increasingly attractive.

As organisations automate more knowledge-based tasks, demand for AI learning and productivity tools escalates. For example, enterprises that applied automation in training and content-delivery reported a 47% rise in module completion rates and a 39% drop in manual review hours. The proliferation of workflow bots and AI-assisted learning means that the learning-and-productivity toolset becomes central to digital workplace strategy. With data volumes increasing and skill-gaps widening in rapidly evolving industries, the adoption of intelligent productivity-learning platforms allows firms to scale learning programmes and unify knowledge-work processes. Enterprises adopting these platforms reported up to 42% faster onboarding and 34% less repetitive work across knowledge-worker teams. Hence, the automation impetus is one of the strongest growth drivers for the market.

Despite strong demand, deployment of AI learning-and-productivity tools is constrained by rising concerns around data governance, privacy and security. Many enterprises cite inadequate data-maturity frameworks as a barrier: a survey found 61% of firms restrict access to productivity data for AI projects due to compliance fears. The complexity of integrating AI-learning modules with legacy systems also slows roll-out, with 45% of organisations reporting delays over six months. In highly regulated sectors such as finance and healthcare, concerns over regulatory compliance and auditability of AI-driven learning outcomes further hamper adoption. Without robust frameworks for consent, data lineage and transparency, many organisations delay or scale back deployment of learning-and-productivity tools, thereby limiting market expansion.

The SME segment presents a significant untapped growth opportunity for AI learning-and-productivity tools. SMEs investing in digital learning platforms reported average efficiency gains of 32% and a 26% improvement in employee retention. Cloud-native, subscription-based productivity-learning solutions make it feasible for smaller firms to deploy enterprise-grade tools at lower upfront cost. In emerging economies, rising digital infrastructure and government-driven up-skilling programmes further enhance this opportunity: one regional programme in Asia reported 38% of SMEs adopting AI learning suites over 12 months. Expansion into vertically-tailored learning-productivity bundles addressing specialised industries (e.g., manufacturing, logistics, professional services) can drive incremental uptake and growth beyond large enterprises.

One of the major challenges facing the AI learning-and-productivity tools market is the shortage of skilled professionals capable of designing, deploying and managing AI-based learning frameworks. A report showed that only 17% of enterprise staff possess the expertise required for AI-driven productivity tools. Integration complexity also imposes delays: 52% of organisations report that linking AI learning platforms to CRM, HR and workflow systems took more than nine months. The cost of custom content development is another hurdle—nearly 46% of organisations cited high initial content-creation cost as a barrier. Additionally, legacy system dependencies and siloed data architecture frequently impede the seamless integration of AI learning and productivity modules, slowing down adoption.

• Rise of Contextual Learning-Agents: AI-learning assistants capable of real-time context retrieval and automated task suggestions saw deployment increase by 29% in 2024, with knowledge-worker error rates reduced by 18%. These agents integrate into productivity suites and directly support workflow completion.

• Expansion of No-Code Learning Frameworks: Platforms that enable non-technical staff to build AI learning modules increased in use by 34% globally in 2024; enabling content authors to create learning pathways without programming reduces time-to-deployment by up to 40%.

• Growth of Multimodal Productivity Tools: Tools combining voice, video, text and analytics for learning and productivity saw adoption rise to 26% of enterprises by 2024, with hybrid-working teams reporting a 22% performance improvement. The integration of adaptive micro-learning with productivity dashboards is notable.

• Shift Toward Sustainable Learning Ecosystems: Corporate ESG agendas now include learning-platform sustainability: 31% of large firms reported transitioning to carbon-neutral learning-and-productivity tool usage by 2026, and 28% increased digital reuse of learning modules by more than 50% year-on-year.

The AI Learning and Productivity Tools market can be segmented by type (e.g., learning management systems, productivity suites, knowledge-work automation platforms), by application (corporate training, workforce productivity, workflow analytics, content-creation), and by end-user (large enterprises, SMEs, public sector). The learning management system type leads due to broad enterprise deployment and established workflows, while new automation-productivity platforms are gaining rapidly. In applications, corporate training remains dominant due to organisational need for up-skilling, yet workflow analytics is expanding quickly. End-users are primarily large enterprises, but SMEs and public-sector institutions are emerging as meaningful contributors. Each segment reflects differing adoption patterns, investment readiness and integration complexity.

The leading type within the AI Learning and Productivity Tools market is learning-management and productivity-suite platforms, which currently account for 46% of total adoption, compared to knowledge-work automation platforms at 27%. However, the fastest-growing segment is micro-learning-automation platforms, driven by adaptive analytics and modular content design, expected to grow at a higher rate than other segments. Other types include workforce analytics engines, content-creation-automation tools and workflow-recommendation systems, which together hold a combined share of around 27%.

According to a 2025 industry survey, a global software services firm implemented a micro-learning automation tool and reduced content-maintenance hours by 38% in six months.

Corporate training is the largest application segment, representing roughly 39% of usage, due to widespread demand for enterprise up-skilling and productivity enhancements. The fastest-rising application is workflow automation and task-recommendation systems, supported by shifts toward remote/hybrid work and the need for real-time productivity insights, with performance-gain metrics increasing by 31% year-on-year. Other applications—such as knowledge-base optimisation, content-creation and analytics-driven productivity monitoring—collectively account for about 30%.

Large enterprises constitute the leading end-user segment, with approximately 52% share, due to their scalable budgets and drive for enterprise-wide productivity strategies. The fastest-growing end-user group is SME-organisations, driven by cloud-based subscription models and digital transformation mandates. Other end-users—public sector, education institutions, non-profit organisations—together hold an estimated 22% share.

North America accounted for the largest market share at 45.2% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 27.9% between 2025 and 2032.

The AI Learning and Productivity Tools market exhibited a total valuation exceeding USD 9.9 billion in 2024, driven by the rapid adoption of intelligent automation tools across large enterprises and SMEs. North America led with over 60% enterprise-level adoption, while Europe followed with 28.5%, reflecting widespread digital transformation initiatives and a strong regulatory framework. Asia Pacific, holding nearly 18% of the global volume in 2024, is projected to surpass 25% by 2030 due to massive integration of AI-based e-learning systems and cloud-driven workforce analytics. South America and the Middle East & Africa together accounted for around 8.3% of the market, supported by increasing government incentives and the rise of hybrid learning environments. Overall, the market demonstrates a strong correlation between regional infrastructure maturity, digital policy strength, and enterprise AI adoption rates, creating diversified growth trajectories across all major regions.

How Are Enterprises Redefining Workforce Productivity Through Smart Learning Platforms?

The North American AI Learning and Productivity Tools market captured approximately 45% of the global share in 2024, driven primarily by sectors such as BFSI, IT & telecom, healthcare, and education. Over 70% of Fortune 1000 companies have integrated AI-based productivity assistants into their workflow management systems. Key regulatory developments, including updates to the U.S. National AI Initiative and Canada’s Digital Charter, have accelerated large-scale enterprise adoption. Technological innovation remains at the forefront, with strong penetration of generative AI-powered assistants, intelligent onboarding systems, and cloud-based workforce analytics. A leading regional player, Microsoft Corporation, has embedded Copilot modules across Office 365 to improve task automation and contextual learning for over 45,000 enterprise users. Consumer behavior trends in this region indicate high enterprise uptake within finance and healthcare, where data-sensitive productivity tools and adaptive learning models are preferred to ensure compliance and efficiency.

What Role Does Regulatory Compliance Play in Shaping AI-Based Learning and Productivity Adoption?

Europe accounted for around 28.5% of the global AI Learning and Productivity Tools market share in 2024, with Germany, the UK, and France emerging as leading markets. Strong regulatory frameworks, such as the EU AI Act and GDPR compliance mandates, have increased demand for explainable and transparent AI-driven productivity solutions. European enterprises are prioritizing data protection and ethical automation, influencing platform design and deployment standards. Sustainability initiatives promoting carbon-neutral cloud services further contribute to adoption. Technological trends include the implementation of multilingual AI learning assistants and predictive workflow analytics. SAP SE remains a notable regional contributor, integrating AI modules into its learning and ERP ecosystems for manufacturing and industrial clients. Regional consumer preferences reveal that 64% of enterprises in the EU require complete auditability of AI-based decisions before full-scale implementation, underlining Europe’s compliance-first mindset.

How Is Rapid Digital Expansion Driving Intelligent Workforce Solutions Across Emerging Economies?

Asia-Pacific ranked second by market volume in 2024, accounting for approximately 18% of total deployments, with China, India, and Japan being the dominant markets. This region is projected to experience the fastest expansion globally, supported by robust digital infrastructure and a rapidly evolving startup ecosystem. India recorded over 35 million AI-powered upskilling enrollments in 2024, while China accounted for nearly 40% of total enterprise AI training deployments within the region. Manufacturing and IT service industries are the largest consumers of AI-based productivity tools, leveraging them for quality management, process optimization, and employee enablement. Innovation hubs in Singapore and South Korea are pioneering localized language models and cloud-native AI-learning applications. A notable development includes Infosys deploying an AI-assisted productivity-learning platform across its 200,000 workforce, reducing training time by 30%. Regional consumer behavior trends reflect a strong mobile-first orientation, with 72% of professionals in emerging Asian markets accessing AI tools via smartphones and workplace chat applications.

How Are Regional Enterprises Localizing Smart Productivity Tools to Enhance Workforce Efficiency?

The South American AI Learning and Productivity Tools market represented nearly 7% of global activity in 2024, led by Brazil, Argentina, and Chile. Government-driven digital inclusion policies and growing investment in AI education programs have significantly contributed to adoption momentum. Brazil alone accounted for approximately 60% of regional demand, aided by its rapidly expanding cloud infrastructure and language-localization technologies. Key sectors utilizing AI tools include education, media, and financial services. A Brazilian technology firm introduced an AI-based bilingual training suite in 2024 that improved employee learning engagement by 28%. Infrastructure developments, such as increased broadband penetration (reaching 78% of enterprises in urban areas), continue to support scalability. Consumer behavior trends in this region emphasize language-localized solutions and hybrid learning formats, catering to both in-office and remote workforce environments.

How Are Public and Industrial Sectors Accelerating Digital Learning Transformation with AI Integration?

The Middle East & Africa region accounted for about 4.3% of the global AI Learning and Productivity Tools market in 2024, with major growth contributions from the UAE, Saudi Arabia, and South Africa. Demand is concentrated in sectors such as oil & gas, construction, and government administration, where AI-driven training and task automation are reshaping operational efficiency. Governments across the GCC have launched large-scale AI initiatives — for instance, the UAE National AI Strategy 2031 — driving AI learning integration across public sector entities. Technological modernization includes deployment of cloud-based workforce learning systems across more than 100,000 civil service employees and partnerships between regional enterprises and global vendors. A UAE-based digital solutions firm implemented AI-learning modules across federal agencies, cutting employee onboarding time by 22%. Consumer behavior trends show strong preference for mobile-based, multilingual, and compliance-focused productivity tools suited to diverse workforce needs.

United States – 45% Market Share: Leadership driven by strong enterprise demand, large-scale digital transformation, and early integration of AI assistants across corporate ecosystems.

China – 17% Market Share: Dominance attributed to high government investment in AI education and rapid expansion of enterprise productivity automation initiatives.

The AI Learning and Productivity Tools market is moderately consolidated, featuring more than 120 active global vendors and around 40 regional specialists. The top five companies collectively control approximately 38% of global market share, indicating a balanced yet competitive landscape. Market leaders such as Microsoft, Google, and IBM continue to expand through strategic alliances, enterprise partnerships, and next-generation AI assistant deployments. Notable strategic initiatives include over 60 cross-industry partnerships and more than 25 product launches between 2023 and 2024. Innovation trends are increasingly centered on integrating generative AI, adaptive learning systems, and workflow intelligence into unified enterprise platforms. Emerging players are targeting SMEs through low-cost subscription models, while established vendors are prioritizing large-scale integrations and advanced analytics capabilities. The market’s competitive dynamics are reinforced by rising R&D investments exceeding USD 3.5 billion in 2024 across learning automation and NLP-based productivity ecosystems. Overall, the ecosystem reflects a shift toward interoperability, data-driven decision-making, and privacy-compliant AI deployments that collectively shape vendor positioning and long-term profitability.

Adobe Inc.

SAP SE

Oracle Corporation

UiPath Inc.

Automation Anywhere Inc.

Grammarly Inc.

Salesforce Inc.

ServiceNow Inc.

Zoom Video Communications Inc.

Slack Technologies LLC

Workday Inc.

Technology serves as the backbone of the AI Learning and Productivity Tools market, enabling enterprises to optimize workforce efficiency and accelerate knowledge transfer. Core technologies include natural language processing (NLP), large language models (LLMs), adaptive micro-learning algorithms, and cognitive automation systems. As of 2024, more than 68% of enterprises globally had integrated at least one AI-based productivity or learning module into their daily workflows. LLM-enabled assistants have improved task completion speed by 30–40% across corporate settings. Multimodal interfaces—combining voice, visual, and text inputs—are becoming a key differentiator, with 55% of organizations now piloting such systems. Emerging innovations include federated learning to ensure data privacy, on-device AI inference for edge productivity tools, and predictive analytics dashboards that merge learning progress with operational KPIs. Integration across platforms like CRM, ERP, and project management systems is expanding rapidly, enabling unified learning-to-performance ecosystems. Decision-makers increasingly prioritize interoperability, scalability, and security when evaluating technology partners. The convergence of cloud computing, generative AI, and workflow automation continues to redefine how organizations manage employee development, productivity, and digital collaboration.

• In March 2024, Microsoft expanded its AI-powered Copilot learning assistant across enterprise Microsoft 365 users, introducing contextual task automation features that reportedly enhanced productivity by 29% in pilot programs. Source: www.microsoft.com

• In November 2023, Google unveiled an AI-driven team productivity suite under Google Workspace, enabling adaptive learning workflows for cross-functional teams and boosting internal collaboration metrics by 32%. Source: www.google.com

• In June 2024, SAP launched an enterprise-grade AI learning bundle tailored for industrial and manufacturing clients, integrating predictive learning analytics that reduced employee training time by 27%. Source: www.sap.com

• In November 2025, PearlMountain Ltd. introduced two new AI-driven video editing features—AI Recreate and Auto Edit—within its FlexClip platform, enabling users to convert raw footage into professionally edited videos within minutes and sharply reducing production time. This advancement supports the AI Learning & Productivity Tools Market by automating complex creative workflows, lowering skill barriers for content creation, and enabling educators, trainers, and marketers to produce high-quality instructional and promotional videos more efficiently. Source: prnewswire.com

The AI Learning and Productivity Tools Market Report provides a comprehensive overview of global market dynamics, segmentations, and technology trends across key regions — North America, Europe, Asia Pacific, South America, and the Middle East & Africa. The analysis spans over 25 countries and covers major segmentations such as Product Type (AI-based Learning Management Systems, Smart Productivity Suites, Workflow Automation Platforms, Adaptive Learning Tools), Application (Corporate Training, Workflow Optimization, Collaboration Enhancement, and Knowledge Analytics), and End-User Industry (IT & Telecom, BFSI, Healthcare, Education, Manufacturing, Retail, and Public Sector). The study includes deployment models (Cloud-Based, On-Premise, and Hybrid) and organization size (Large Enterprises and SMEs). It also evaluates innovation trends in natural language processing, predictive learning analytics, multimodal interaction, and cloud-edge integration. The report encompasses over 100 competitive profiles, identifies leading regional innovators, and outlines investment trends and partnership networks shaping this ecosystem. This comprehensive coverage provides decision-makers with actionable intelligence for market entry, technology adoption, and strategic planning in the evolving AI-driven workplace productivity domain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 13,892.7 Million |

|

Market Revenue in 2032 |

USD 74,697.8 Million |

|

CAGR (2025 - 2032) |

23.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation, Google LLC, IBM Corporation, Adobe Inc., SAP SE, Oracle Corporation, UiPath Inc., Automation Anywhere Inc., Grammarly Inc., Salesforce Inc., ServiceNow Inc., Zoom Video Communications Inc., Slack Technologies LLC, Workday Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |