Reports

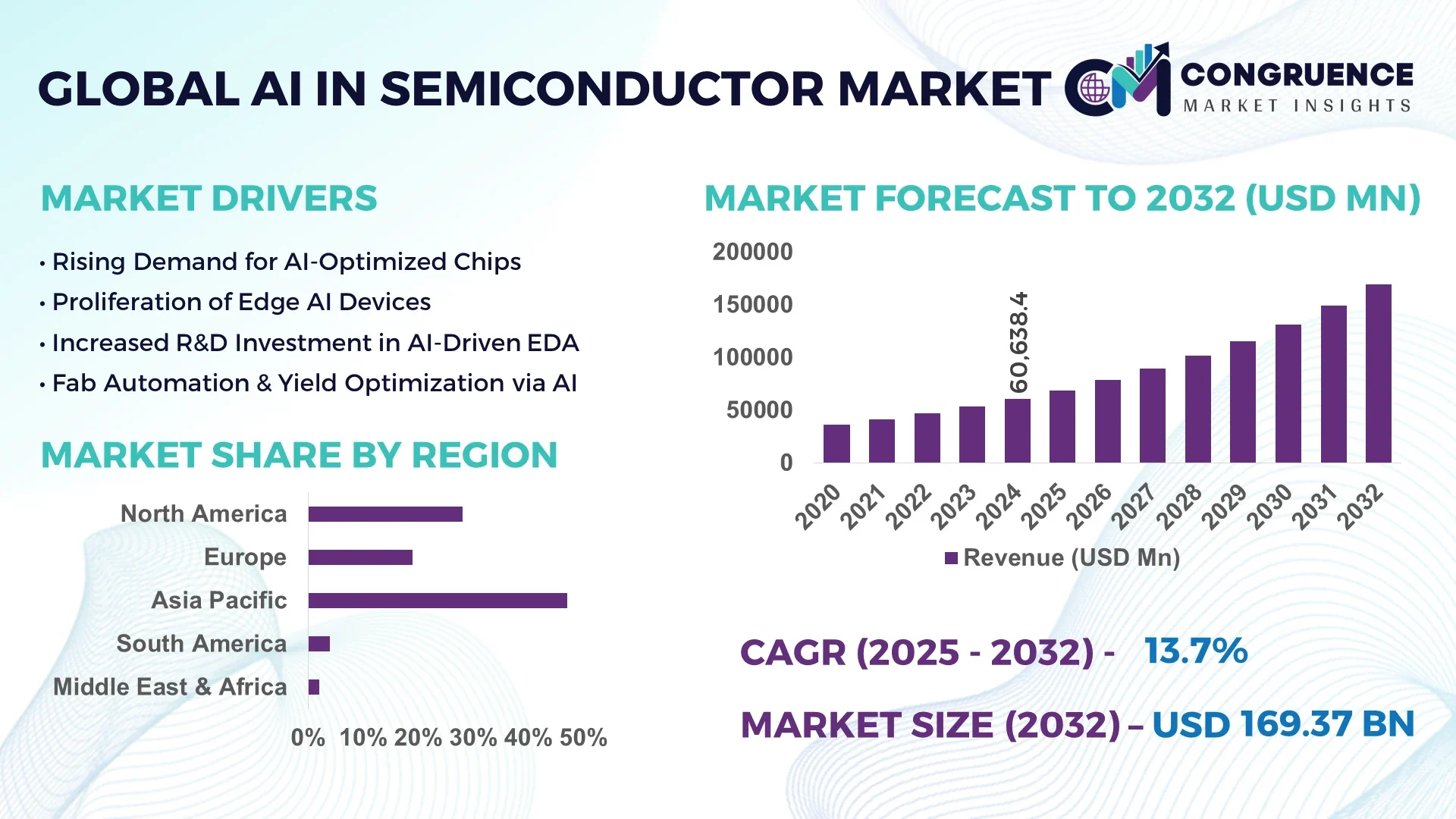

The Global AI in Semiconductor Market was valued at USD 60,638.4 Million in 2024 and is anticipated to reach a value of USD 169,368.0 Million by 2032 expanding at a CAGR of 13.7% between 2025 and 2032.

In China, an unrivaled production powerhouse, domestic firms are investing heavily in AI chip manufacturing infrastructure, with new fabs capable of advanced node production and multi-million-unit output annually. China also leads in state-backed AI chip R&D, with continuous breakthroughs in neural network accelerators and high-volume wafer capacities.

Key industry sectors—such as data centers, automotive AI platforms, consumer electronics, and edge computing—are driving rapid deployment of accelerators, smart SoCs, and neuromorphic processors. Innovations include AI-optimized EDA tools that automate layout and verification, generative design workflows, and energy-efficient architectures that reduce power draw per inference. Regulatory frameworks now mandate carbon reporting in chip fabs, prompting adoption of AI-driven thermal control and precision cooling systems. Regionally, North America excels in high-performance compute demand, while Asia Pacific shows robust growth in AI-enabled mobile and IoT semiconductors. Emerging trends include chiplet architectures with AI-based interconnect optimization, AI-powered yield prediction in manufacturing, and co-development models between OEMs and AI platform providers—all suggesting a future where intelligent semiconductor design and production are deeply integrated.

AI in Semiconductor Market transformation is accelerating with AI-driven tools reshaping design, verification, and manufacturing pipelines. Decision-makers are witnessing tangible benefits: automated layout optimization reduces design iterations by up to 30%, while AI-enhanced predictive maintenance systems in fabrication plants can detect equipment anomalies up to 48 hours in advance, yielding higher throughput. AI in Semiconductor Market has seen adoption of AI-co-pilots—like Synopsys.ai’s DSO.ai suite—which enabled commercial tape-outs with notable returns in productivity and a marked drop in power consumption. Verification tasks have streamlined; clients report up to 10x faster coverage closure and a 30% uplift in verification throughput using AI-powered reinforcement learning tools. AI in Semiconductor Market is also seeing deployment of closed-loop production systems, where real-time process data triggers adjustments in etch and doping controls, ultimately improving wafer yield and uniformity. In high-volume manufacturing, AI in Semiconductor Market applications now include adaptive control systems that adjust lithography alignment for each wafer, reducing defect density significantly. From enablers in design to operational optimization, AI in Semiconductor Market is proving itself as a transformation catalyst across the chip lifecycle.

“In 2024, Synopsys’s AI-powered VSO.ai tool reduced functional coverage gaps by up to 10× and improved IP verification productivity by around 30 percent in a major chip development case.”

AI in Semiconductor Market dynamics center on converging pressures from hyperscale compute demand, talent shortages, and geopolitical supply chain shifts. Design complexity at advanced nodes is skyrocketing, leading firms to incorporate AI-based automation across design verification, yield prediction, and fab control. Geopolitical tensions drive localization of AI semiconductor supply chains, particularly in Asia. At the same time, fabrication fabs are embedding AI analytics to manage energy usage, thermal control, and equipment uptime. The industry’s return profile is increasingly bifurcated—only top innovators reap economic value—so adopting AI in Semiconductor Market is becoming a necessity to maintain competitiveness. Structural shifts such as modular chiplet adoption, AI-centric packaging, and embedded AI microcontrollers in edge devices are reshaping development pipelines. For decision-makers, AI in Semiconductor Market underscores the need to align data strategy, IP workflows, and workforce capabilities to remain agile amid rapid technological change.

Efficient design automation through AI is driving major shifts in the AI in Semiconductor Market. Companies deploying AI-powered EDA suites are observing reduction in design cycle times, with layout and verification phases shortened by up to 30%. This efficiency allows semiconductor firms to compress time-to-market for complex SoCs and advanced node architectures. AI-enabled test generation tools also reduce manual efforts by automatically generating and validating test cases, significantly improving throughput. As design complexity grows, AI’s contribution to optimization, power-performance trade-offs, and verification speed is becoming a decisive competitive edge in the AI in Semiconductor Market.

Despite promising gains, the AI in Semiconductor Market faces constraints in adoption due to infrastructure and tooling cost barriers. Integrating AI-driven design tools often requires upgrading compute clusters with high-performance GPUs or TPUs, incurring substantial capital expense. Legacyfabs may also lack the data infrastructure to feed AI models with real-time sensor data, limiting implementation of AI-based process control. Moreover, proprietary AI tools often come with significant licensing fees, which can deter smaller OEMs or regional players. These cost-related challenges slow the broader diffusion of AI in Semiconductor Market innovations, keeping benefits concentrated among well-funded players.

AI in Semiconductor Market holds untapped opportunity in achieving yield improvements and energy savings. Advanced fabs are beginning to deploy AI models that analyze multi-sensor data to preemptively adjust process parameters, improving wafer yield by percentages that translate into millions in cost savings. Similarly, AI-driven thermal control systems dynamically manage cleanroom environments and tool operation, reducing energy consumption by several percent. These efficiencies are especially valuable in high-volume manufacturing contexts, offering operational cost reductions and sustainable ‘green’ manufacturing credentials—areas where AI in Semiconductor Market can make a meaningful difference.

Widespread adoption of AI in Semiconductor Market is constrained by a critical shortage of hybrid talent—professionals skilled in both chip design and AI/ML. This skills gap hinders the ability to integrate AI tools effectively into existing design workflows. Even when tools like AI-driven layout optimizers exist, firms struggle to train design teams rapidly enough to leverage their full potential. Educational programs and workforce development initiatives are trying to bridge this gap, but the pace of demand far outstrips supply. Without resolving this, adoption of AI in Semiconductor Market remains uneven and impeded.

• AI-Copilots Accelerating Design Workflows: AI-powered copilots embedded in design environments are enabling engineers to complete RTL authoring and verification tasks in seconds instead of hours. This surge in automation is particularly evident in complex system-on-chip development and is reshaping productivity expectations in the AI in Semiconductor Market.

• Generative AI Streamlining ASIC Design: Generative frameworks are now translating natural language specifications directly into HDL code, rapidly prototyping functional modules with validated performance. This shift is enabling teams in AI in Semiconductor Market to slash manual coding effort and accelerate early-stage design iterations.

• AI-Enabled Yield Prediction in Fabs: Predictive models trained on process and sensor data are now identifying patterns leading to yield loss. Fabs implementing these models have seen defect densities drop, with early adopters reporting fewer retests and improved first-pass yield—enhancing cost efficiency across high-volume production.

• AI-Optimized Power & Thermal Control: Integrated AI systems in cleanrooms and test lines dynamically adjust cooling output, humidity, and tool cycle thresholds in real-time. This approach improves energy utilization and tightens environmental controls, supporting both green manufacturing and high throughput—all visible across AI in Semiconductor Market leadership fabs globally.

Market segmentation in the AI in Semiconductor Market enables tailored strategic decisions by product type, application, and end-user profile. By type, the most advanced design automation platforms and AI optimizing closed-loop manufacturing systems lead due to broad applicability across complex chip processes. On the application front, high-performance compute accelerators for data centers represent a dominant use case, while emerging domains like automotive AI SoCs and energy-efficient edge devices are gaining traction. Regarding end users, hyperscale cloud/AI service providers lead deployment, followed closely by semiconductor OEMs investing in next-gen design tools. Industrial chipmakers and foundry operators are fast-adopting AI solutions in their internal ecosystems. Overall, segmentation reveals that tools and platforms focused on design acceleration, yield improvement, and fab automation are the most critical levers in the AI in Semiconductor Market today.

Leading the type segment are AI-augmented EDA platforms—tools offering design layout, RTL synthesis, and verification optimization—due to their widespread use in reducing development cycles and improving power-performance trade-offs. The fastest-growing type is generative AI workflows that translate specifications into HDL code, driven by accelerated SoC prototyping and workforce efficiency needs. Hybrid systems combining AI software with fab automation (e.g., real-time thermal control) are also emerging, providing niche value in advanced fabs. Other types, such as third-party AI yield analytics or model libraries, contribute in more specialized or supplementary roles.

Among applications, high-performance AI accelerator design for data centers remains the leading segment, as hyperscale providers demand tailored silicon with optimized compute density. The fastest-growing application is automotive and edge AI semiconductor design, fueled by rising EV deployments and smart mobility initiatives. Other areas—like IoT sensor SoCs and smart home device chips—serve as growing but smaller applications, often adopting AI in pilot stages or lab environments.

Hyperscale cloud and AI data center operators constitute the leading end-user segment—they both consume and drive innovation in AI-in-Semiconductor tools. The fastest-growing segment is semiconductor OEMs designing custom AI SoCs for differentiated products, spurred by differentiation needs and internal compute optimization. Other end-users—including industrial IoT device makers, automotive Tier 1s, and fab operators—are increasingly integrating AI into their workflows, either through design tool use or process automation, gradually expanding AI in Semiconductor Market's reach.

Asia-Pacific accounted for the largest market share at 47% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 15.1% between 2025 and 2032.

Asia-Pacific’s strong position is underpinned by large-scale investments in semiconductor fabs, rising demand from consumer electronics, and the rapid growth of AI-powered applications in China, Japan, and South Korea. Meanwhile, North America’s accelerated adoption is driven by technological leadership, increasing demand for advanced AI processors, and strong regulatory support for semiconductor R&D. This dual dynamic highlights both the scale of consumption and the innovation-driven expansion that defines the global AI in Semiconductor Market landscape.

Advancing AI-Optimized Chip Ecosystem for Next-Gen Applications

North America represented nearly 28% of the AI in Semiconductor Market in 2024, reflecting the region’s dominance in high-performance compute and advanced AI processors. Demand is strongly influenced by industries such as autonomous vehicles, defense, aerospace, and cloud data centers, which rely heavily on AI-optimized chips. Government initiatives, including semiconductor funding programs and export control regulations, are shaping investment patterns while incentivizing domestic chip production. Technological progress includes AI-assisted EDA workflows, AI-accelerated HPC systems, and significant advances in neuromorphic chip research. With rising adoption of AI across industrial automation and healthcare, the region continues to lead innovation in AI in Semiconductor Market development.

Driving Sustainable AI-Powered Semiconductor Innovations

Europe held around 19% of the AI in Semiconductor Market in 2024, with Germany, France, and the UK serving as leading markets. European regulatory agencies are pushing sustainability initiatives, encouraging low-power semiconductor architectures and environmentally responsible manufacturing processes. Strong adoption is seen in the automotive sector, particularly with electric vehicles and advanced driver-assistance systems integrating AI processors. France and Germany are also advancing AI in industrial IoT and robotics, while the UK focuses on AI-driven semiconductor research hubs. With a balanced emphasis on green technology and digital innovation, Europe is becoming a key hub for sustainable AI in Semiconductor Market expansion.

Expanding AI Semiconductor Manufacturing and Innovation Hubs

Asia-Pacific dominated the AI in Semiconductor Market with approximately 47% share in 2024, making it the largest global consumer and producer. China, Japan, South Korea, and India are the top contributors, with large-scale fabrication hubs and rapid investment in AI-optimized chips. Manufacturing capacity is expanding with advanced fabs capable of 5nm and below, while local demand is driven by consumer electronics, smart devices, and AI-powered mobility solutions. Regional hubs like Shenzhen, Tokyo, and Seoul are leading AI semiconductor research, with a focus on chiplet architectures, advanced memory integration, and AI-driven IoT processors. This strong ecosystem ensures continued market strength in Asia-Pacific.

Rising Adoption of AI-Powered Semiconductors Across Industries

South America contributed around 4% of the AI in Semiconductor Market in 2024, with Brazil and Argentina leading demand. The market is shaped by the growing energy and mining sectors adopting AI-driven semiconductor solutions for predictive maintenance and efficiency improvements. Infrastructure upgrades and smart city projects are also creating opportunities for AI-powered chip applications. Government policies are increasingly promoting digital transformation, while trade agreements facilitate import of semiconductor equipment and design tools. With growing demand for localized AI chip solutions in agriculture and industrial automation, South America is gradually strengthening its presence in the global AI in Semiconductor Market.

Accelerating AI-Driven Transformation in Industrial and Energy Sectors

Middle East & Africa accounted for about 2% of the AI in Semiconductor Market in 2024, with the UAE, Saudi Arabia, and South Africa emerging as key markets. Demand is driven by oil & gas modernization, construction technology, and renewable energy integration, all of which increasingly rely on AI-powered chips. Governments are investing in smart infrastructure, AI hubs, and regional technology parks to support local semiconductor innovation. Countries like the UAE are prioritizing AI in data centers and cloud computing, while South Africa focuses on industrial automation. Regulatory frameworks and trade partnerships are further encouraging AI semiconductor adoption in the region.

China – 29% market share

Strong semiconductor manufacturing infrastructure and heavy investment in AI-optimized fabs support China’s leadership.

United States – 24% market share

Advanced chip design expertise and high demand from hyperscale data centers drive dominance in AI in Semiconductor Market.

The AI in Semiconductor Market is characterized by high competition, with over 50 active global competitors spanning design automation, manufacturing, and specialized AI processor development. Leading firms are strategically positioning themselves through partnerships, mergers, and joint ventures to secure supply chains and enhance technological capabilities. Innovation is at the forefront, with top companies launching AI-powered EDA tools, neuromorphic processors, and AI-driven chiplets. Regional players are focusing on customized AI chips for niche applications such as automotive and industrial IoT, while global leaders concentrate on high-performance compute. Competitive intensity is further shaped by government-backed funding programs, cross-border restrictions on technology transfer, and accelerating investments in AI chip design hubs. Companies that succeed in balancing cost efficiency, speed-to-market, and AI-driven design integration are emerging as front-runners in this evolving market.

Nvidia Corporation

Intel Corporation

Advanced Micro Devices, Inc. (AMD)

Qualcomm Incorporated

Samsung Electronics Co., Ltd.

Taiwan Semiconductor Manufacturing Company Limited (TSMC)

Synopsys, Inc.

Cadence Design Systems, Inc.

Broadcom Inc.

Huawei Technologies Co., Ltd.

Technological innovations are reshaping the AI in Semiconductor Market by integrating AI throughout the design, manufacturing, and deployment lifecycle. AI-driven EDA platforms now automate circuit layout, verification, and testing, reducing time-to-market by as much as 30%. Neuromorphic processors, designed to mimic brain-like efficiency, are gaining traction in energy-constrained edge computing, with research prototypes demonstrating significant reductions in power consumption per inference. AI-enhanced manufacturing solutions leverage predictive analytics for wafer yield improvement, cutting defect rates and optimizing throughput in advanced fabs. Chiplet-based architectures combined with AI-optimized interconnects allow modular scaling, which reduces costs and improves flexibility for system integration.

Emerging technologies such as AI-driven generative design enable automatic creation of optimized HDL code from high-level functional descriptions, significantly lowering manual engineering effort. In parallel, AI-powered digital twins of fabs are helping operators simulate production environments, fine-tune equipment calibration, and enhance uptime. Edge AI chips, particularly in automotive and IoT, are advancing with integrated AI accelerators that deliver real-time analytics on-device, minimizing reliance on cloud compute. Collectively, these advancements ensure the AI in Semiconductor Market remains at the forefront of innovation, where efficiency, scalability, and intelligence converge to drive the industry forward.

In February 2024, Nvidia unveiled its latest AI semiconductor platform designed for data centers, featuring enhanced GPU accelerators capable of processing trillions of parameters for generative AI workloads. This platform boosts training efficiency while lowering energy consumption.

In May 2024, Samsung Electronics began mass production of its 3nm AI-focused semiconductors, integrating gate-all-around (GAA) transistor technology to enhance efficiency and reduce power draw, strengthening its edge in AI computing solutions.

In September 2023, Intel launched AI-optimized Meteor Lake processors using chiplet architecture, enabling improved performance in PC-based AI applications and offering modular integration for diverse computing requirements.

In December 2023, TSMC introduced AI-powered yield optimization tools across its 5nm fabs, reducing defect density rates and improving wafer production efficiency, enabling clients to accelerate tape-outs for AI-driven chips.

The scope of the AI in Semiconductor Market Report encompasses a detailed analysis of market segments, technologies, applications, and geographic regions, providing actionable insights for decision-makers. Segmentation covers type-based categories such as AI-powered EDA tools, neuromorphic processors, and AI-driven fab automation systems, offering clarity on both established and emerging product lines. Application-focused insights highlight critical areas like data centers, automotive AI platforms, IoT devices, and edge computing, where demand for AI-enabled semiconductors continues to expand rapidly.

Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, identifying both leading and emerging regions while providing data on market share distribution. The report also examines industry verticals including consumer electronics, automotive, healthcare, industrial automation, and defense, reflecting diverse adoption across sectors. Emerging technologies such as generative AI for chip design, AI-enhanced chiplets, and advanced power-efficient architectures are emphasized as transformative drivers. The scope further incorporates competitive dynamics, highlighting key players, innovation strategies, and market positioning. With a focus on both macro trends and niche growth segments, this report delivers comprehensive intelligence tailored to business leaders, investors, and analysts navigating the AI in Semiconductor Market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 60638.4 Million |

|

Market Revenue in 2032 |

USD 169368.0 Million |

|

CAGR (2025 - 2032) |

13.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User Industry

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nvidia Corporation, Intel Corporation, Advanced Micro Devices, Inc. (AMD), Qualcomm Incorporated, Samsung Electronics Co., Ltd., Taiwan Semiconductor Manufacturing Company Limited (TSMC), Synopsys, Inc., Cadence Design Systems, Inc., Broadcom Inc., Huawei Technologies Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |