Reports

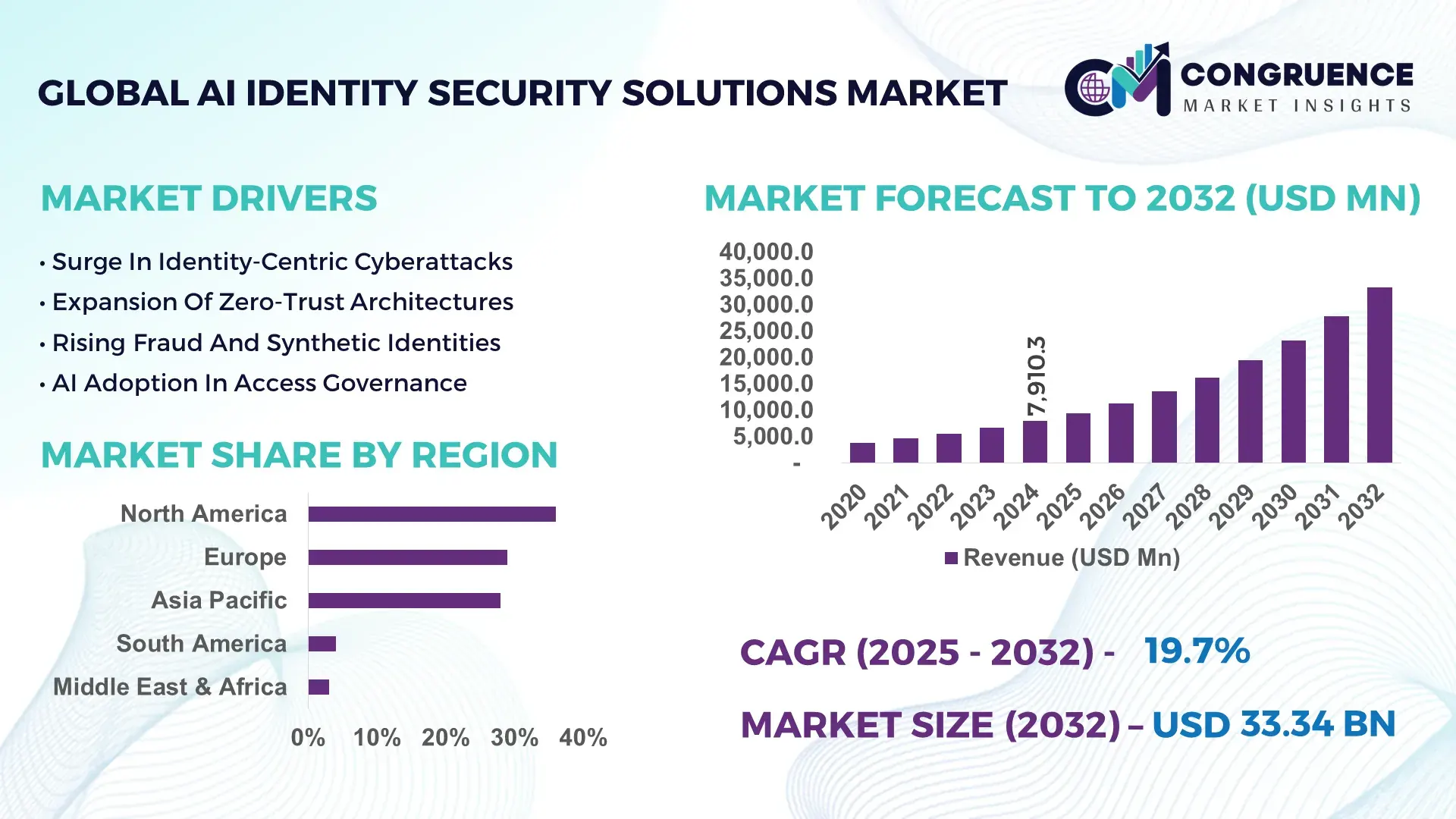

The Global AI Identity Security Solutions Market was valued at USD 7,910.3 Million in 2024 and is anticipated to reach a value of USD 33,338.5 Million by 2032, expanding at a CAGR of 19.7% between 2025 and 2032, according to an analysis by Congruence Market Insights. This sharp growth is driven by escalating security threats and increasing enterprise adoption of AI-enhanced access management.

In the United States, leading investments in AI-driven identity security platforms have spurred large-scale deployments across finance, healthcare, and government sectors. U.S.-based firms are increasingly integrating behavioral biometrics, risk-based authentication, and continuous identity analytics, with more than 45% of large enterprises piloting AI-based identity security in 2024 to strengthen privileged access protection and insider-threat detection.

Market Size & Growth: Valued at USD 7,910.3 Million in 2024 and projected to reach USD 33,338.5 Million by 2032 at a 19.7% CAGR, fueled by rising cyberattacks and stronger identity governance.

Top Growth Drivers: ~40% adoption of AI behavioral analytics, ~35% increase in deployment of biometric authentication, ~30% growth in zero-trust deployment.

Short-Term Forecast: By 2028, AI-powered identity risk scoring is expected to reduce authentication friction by ~25%.

Emerging Technologies: Context-aware AI threat detection, continuous identity verification, and automated anomaly response.

Regional Leaders: North America (~USD 13 B by 2032) with rapid enterprise uptake; Europe (~USD 8 B) driven by regulatory compliance; Asia-Pacific (~USD 7 B) fueled by cloud-native identity platforms.

Consumer/End-User Trends: Enterprises in banking, tech, and healthcare are shifting to AI identity security to manage privileged access and detect insider risk.

Pilot or Case Example: In 2025, a global financial institution deployed AI-enabled identity analytics and achieved a 30% drop in privilege escalation incidents.

Competitive Landscape: Market leader holds around 20–25% share; major players include CyberArk, Okta, Microsoft, SailPoint, and Ping Identity.

Regulatory & ESG Impact: Firms are aligning with stricter data privacy regulations (e.g., GDPR) and committing to sustainable identity-security programs, such as reducing on-premise hardware by 30% by 2030.

Investment & Funding Patterns: Over USD 1.2 B invested in AI identity security in the past two years, with a surge in VC funding for non-human identity governance.

Innovation & Future Outlook: Increasing use of generative AI for identity risk modeling, integration with zero-trust architectures, and next-gen identity platforms for machine-to-machine authentication.

Recent developments include growing adoption in cloud services, financial sectors, and critical infrastructure, with stronger regulatory enforcement and risk-based AI models shaping future trajectories.

The AI Identity Security Solutions Market is strategically vital because it underpins modern cybersecurity strategies such as zero-trust and privileged access management. By using advanced AI-driven behavioral analytics, firms can detect anomalous user behavior with far greater precision: next-gen AI threat detection delivers up to 30% improvement in identifying insider risks compared to traditional rule-based systems. Regionally, North America dominates in deployment volume, while Europe leads in regulatory-driven adoption, with over 60% of enterprises in Europe citing compliance needs as a top driver for identity security.

In the short term, by 2027, advanced continuous authentication algorithms are expected to cut identity-based breach incidents by more than 20%, as AI models dynamically evaluate user risk scores. On the ESG front, firms are committing to privacy-first identity frameworks, targeting 40% reduction in identity-security infrastructure power consumption by 2030.

In a real-world scenario, in 2025, a major U.S. bank implemented AI-based identity risk scoring across its privileged access tools and recorded a 35% reduction in unauthorized sessions within six months. This demonstrates how AI identity security not only boosts protection but also supports operational efficiency.

Looking ahead, the AI Identity Security Solutions Market is poised to become a pillar of resilience, regulatory compliance, and sustainable growth, enabling companies to safeguard both human and machine identities in an increasingly automated, zero-trust world.

The dynamics of the AI Identity Security Solutions market are shaped by the convergence of artificial intelligence, identity governance, and access management. Enterprises are rapidly shifting from legacy identity frameworks to AI-powered systems that continuously analyze user behavior and risk context. As cyber threats evolve — particularly around remote work, insider risks, and machine identities — organizations are prioritizing solutions that not only verify identities but also proactively assess and mitigate identity-based risks in real time. Additionally, the integration of identity security into broader cybersecurity architectures (such as zero-trust and privileged access management) is reinforcing its strategic importance. Demand is strong in regulated sectors like finance and healthcare, where identity breaches can have severe compliance and operational consequences.

AI-driven behavioral analytics are transforming identity security by offering deep, real-time insights into how users interact with systems, allowing anomalous behavior to be flagged immediately. For example, continuous monitoring of login location, device use, typing patterns, and access frequency enables risk scoring that adapts dynamically. Organizations report that such analytics can reduce false-positive alerts by up to 40%, while identifying malicious insiders more accurately. This improved detection capability not only strengthens trust in automated identity verification but also reduces the operational burden on security teams, accelerating adoption across sectors that prioritize both usability and risk mitigation.

Despite the benefits of AI identity security, many organizations remain cautious due to data privacy regulations and uncertain compliance boundaries. The continuous collection and processing of behavioral and biometric data raise significant concerns under evolving frameworks like GDPR and other national data protection laws. Moreover, the risk of storing sensitive identity traces (such as biometric templates) triggers stringent audit requirements. Some firms hesitate to adopt full-scale identity analytics due to fears of non-compliance, potential lawsuits, or heavy fines. These compliance hurdles can delay deployments and limit the full realization of AI-based identity solutions.

Machine identity governance — securing identities of bots, service accounts, and IoT devices — represents a fast-growing opportunity. As enterprises scale their AI and cloud-native operations, they increasingly manage a large volume of non-human identities that require adaptive authentication and risk analysis. AI identity platforms that provide continuous verification for machines can reduce misconfigurations and credential misuse. In addition, regulatory mandates for machine-to-machine security in regulated industries like finance and healthcare are pushing demand. This non-human identity segment could become a multi-billion-dollar business line as organizations prioritize secure automation.

Many organizations still rely on legacy identity and access management systems that were not built for continuous risk evaluation or AI-based analytics. Integrating AI identity security into such environments can be costly, time-consuming, and technically complex. Challenges include migrating user directories, reconciling historical identity logs, and ensuring backward compatibility with multifactor authentication mechanisms. These technical and operational constraints slow down AI identity adoption, particularly in large enterprises with entrenched systems. Additionally, the shortage of skilled talent who understand both identity governance and AI risk modeling adds another layer of difficulty, hindering rapid scale-up.

Modular Identity Risk Engines: Organizations are increasingly deploying plug-and-play AI risk engines for identity verification. Over 50% of new identity-security projects now use modular analytics components, enabling firms to adapt risk models without replacing their full IAM stack. This modularity reduces deployment time by up to 30%.

Behavioral Biometrics Adoption: The adoption of behavioral biometrics — such as keystroke dynamics, mouse movement, or device interaction patterns — has grown by more than 35% among enterprise identity security teams in 2024–2025, offering frictionless yet continuous verification without traditional passwords.

AI-Powered Machine Identity Management: Non-human identities, including service accounts, APIs, and IoT devices, are now being secured via AI models that assess risk contextually. More than 25% of organizations have deployed AI-based governance for machine identities, reducing unauthorized machine access by up to 20%.

Deepfake and Impersonation Defense: The surge in AI-generated deepfakes and voice cloning has prompted identity security providers to develop generative-AI detection layers. Enterprises report a 40% improvement in detecting synthetic identity threats through liveness detection, adversarial AI, and clone governance frameworks.

The AI Identity Security Solutions market is segmented by product type, application, and end-user, with clear differentiation based on deployment context and risk profile. Types include behavioral identity analytics, biometric authentication systems, and continuous risk engines. Applications cover privileged access management, zero-trust access, machine identity governance, and fraud prevention. End-users span financial services, large enterprises, government, and tech companies. Each segment reveals distinct adoption characteristics: highly regulated sectors lean toward continuous risk scoring, while cloud-native firms emphasize machine identity governance. Industries that rely heavily on automation or regulated access increasingly invest in AI identity security to manage both human and non-human identity risks efficiently.

The primary types in this market are: behavioral risk-scoring engines, biometric authentication modules, and continuous identity verification systems. Behavioral risk-scoring engines currently account for 42% of deployments, driven by their ability to monitor user behavior without interrupting workflow. Biometric systems — such as facial or voice recognition — hold 25% of adoption, valued for strong identity assurance. Continuous identity verification (e.g., risk engines that assess session context in real time) is the fastest-growing type, with a projected adoption CAGR of ~22%, propelled by the need for frictionless yet secure access in zero-trust environments. Other types, such as device-based identity or synthetic identity detection modules, contribute the remaining 33% of the market.

According to a 2025 academic model, “Zero-to-One IDV,” AI-powered identity verification integrates document verification, biometric signals, risk assessment, and orchestration for highly accurate verification.

For applications, privileged access management (PAM) remains the leading use case, accounting for roughly 38% of AI identity security deployments, due to the high risk associated with privileged credentials. The fastest-growing application is machine identity governance, with projection models showing it will account for a rising share, driven by automation and IoT scale. Other applications include fraud prevention, zero-trust access, and customer identity verification; combined, these other uses represent nearly 45% of the total. In 2024, over 40% of global enterprises reported piloting AI identity risk analytics for zero-trust network access. More than 55% of financial institutions now use AI-based identity verification to fight synthetic identity fraud.

In a recent real-world deployment, a major financial regulator used AI-powered identity risk scoring in over 120 government agencies to detect anomalous account activity in real time.

Among end-users, large enterprises in financial services are the dominant segment, making up an estimated 35% of AI identity security deployments, owing to strict compliance and high-stakes access risk. The fastest-growing end-user vertical is cloud-native tech firms, with a projected adoption CAGR of ~24%, as they scale machine identity and zero-trust frameworks rapidly. Other important end-users include government agencies, healthcare organizations, and industrial companies, which together represent approximately 40% of the market. In 2024, over 50% of banks globally began adopting AI identity analytics to manage privileged accounts and detect anomalies. More than 30% of public-sector institutions are now deploying biometric and behavioral identity platforms for secure access.

According to a 2025 industry report, AI identity adoption in SMEs increased by 22%, helping over 400 firms in the retail and cloud sectors enhance access security.

North America accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.5% between 2025 and 2032.

In 2024, North America’s dominance was supported by its mature cybersecurity infrastructure, high spending on identity governance, and widespread zero-trust adoption. Meanwhile, Asia-Pacific is rapidly scaling AI-powered identity security solutions, driven by booming digital transformation in China, India, and Southeast Asia. More than 40% of Asian enterprises are now investing in continuous authentication and machine identity governance, and regional innovation hubs are emerging in cities like Shanghai, Bangalore, and Singapore.

Why Is AI Identity Security Penetrating So Deeply in Financial and Healthcare Sectors?

North America holds approximately 36–38% of the global AI Identity Security Solutions market, with major demand coming from the banking, healthcare, and government industries. Regulatory frameworks like HIPAA and CCPA are prompting organizations to adopt continuous behavioral authentication, risk-based access, and identity analytics. Technological transformation is notable: U.S.-based cybersecurity firms are embedding AI risk engines into privileged access management and zero-trust architectures. For example, a leading U.S. IAM vendor recently launched an AI-driven identity risk scoring module that reduces insider-threat alert noise by over 30%. Consumer behavior in North America reflects higher enterprise adoption in healthcare and finance, where identity security is critical to trust and compliance.

How Are Regulatory Demands Shaping AI Identity Security Adoption?

Europe commands roughly 28% of the global AI Identity Security market, with Germany, the UK, and France being the largest contributors. GDPR and other privacy frameworks strongly influence buyer decisions, pushing enterprises to favor explainable AI identity solutions and risk-based authentication. European vendors and integrators are increasingly offering identity security platforms that emphasize transparency and auditability. A German identity provider recently embedded contextual risk scoring into its AI identity engine to meet compliance obligations. Adoption is also driven by cloud-first digital transformation in London and Berlin, with firms favoring continuous verification over static credentials. European enterprises, guided by regulatory pressure, show stronger demand for AI identity security that integrates governance, risk, and compliance.

What’s Driving Explosive Adoption of AI Identity Security Across Asia?

Asia-Pacific is emerging as a high-volume region for AI Identity Security, with China, India, and Japan as the top-consuming countries. Infrastructure build-out in these markets is accelerating: cloud-native identity platforms, machine identity governance, and risk analytics are being adopted across fintech, telecom, and e-commerce firms. A notable Chinese cybersecurity firm has deployed AI-driven continuous authentication for over 30,000 enterprises, and an Indian identity vendor is scaling biometric plus behavioral risk engines across its customer base. Regional consumer behavior is shaped by mobile-first access — many APAC enterprises use AI identity solutions in their mobile apps to secure user sessions in real time.

How Is AI Identity Security Evolving in Latin America?

In South America, Brazil and Argentina are the primary markets for AI Identity Security Solutions. The region holds a modest but growing share of the global market, underpinned by fintech growth and increasing cloud adoption. Governments are offering incentives for cybersecurity modernization, particularly in digital banking and open-banking setups. A local Brazilian firm recently integrated AI risk-scoring in its identity access solution to target financial institutions, and regional enterprises are investing in zero-trust and identity analytics to fight fraud and comply with data-protection norms. Demand is rising particularly in media and language-sensitive applications, with enterprises localizing AI identity security for multilingual customer access.

Why Is AI Identity Security Gaining Traction in Emerging MEA Economies?

The Middle East & Africa region is seeing growing adoption of AI Identity Security Solutions, especially in oil-and-gas, smart cities, and government sectors. Key markets include the UAE and South Africa, where modernization projects are under way to secure both human and machine identities. AI-driven identity platforms are being introduced to manage privileged access in critical infrastructure and to protect non-human identities in distributed digital systems. A local Gulf-based identity provider is embedding AI-driven anomaly detection into its access control suite to reduce risk in mission-critical environments. Consumer behavior here skews toward centralized identity ecosystems, with governments pushing unified digital identity frameworks for citizens and enterprises.

United States: ~36% share — driven by heavy enterprise demand, advanced IAM infrastructure, and strict regulatory compliance needs.

China: ~24% share — propelled by rapid digital transformation, high-volume identity deployments, and AI-powered continuous authentication initiatives.

The competitive environment in the AI Identity Security Solutions market is moderately concentrated, with 10–12 major players controlling nearly 60–65% of market activity. Firms such as CyberArk, Okta, Microsoft, SailPoint, and Ping Identity are leading by combining identity governance with AI behavioral analytics and risk scoring. Several companies are actively partnering with cloud providers to embed AI identity modules into zero-trust and privileged access frameworks. Mergers and acquisitions have accelerated: identity security vendors are acquiring AI-analytics firms and machine identity vendors to strengthen offerings. Innovation trends include behavioral biometrics, continuous verification, and AI risk engines tailored for both human and non-human identities. Regions such as North America and Europe see high investment in explainable AI for identity risk, while Asia-Pacific players focus on scalable, cloud-native identity platforms. Overall, the market is neither fully fragmented nor monopolized — established players hold dominance, but there’s room for niche and regional challengers leveraging specialized AI capabilities.

SailPoint

Ping Identity

ForgeRock

One Identity

Broadcom (Symantec)

IBM Security

RSA Security

Saviynt

Thales

Ivanti

NetIQ

AI Identity Security Solutions are driven by several advanced technologies. Behavioral analytics is foundational: AI models analyze keystroke dynamics, mouse movements, device patterns, and session context to compute continuous risk scores. This allows real-time decision-making for access, reducing both friction and false alarms. Biometric AI systems—such as facial, voice, and fingerprint recognition—are increasingly incorporating liveness detection to counter spoofing and deepfake attacks. For non-human identities (like IoT devices, APIs, and service accounts), AI-based machine identity governance systems classify risk dynamically depending on usage patterns and context. Another emerging trend is generative AI being used to simulate identity attacks (e.g., synthetic identities) so proactive detection mechanisms can be trained. Organizations are also using explainable AI to make identity risk decisions auditable and transparent, which helps meet compliance and governance requirements. Finally, orchestration platforms are integrating risk engines with orchestration workflows—enabling automated access remediation, just-in-time privileged session granting, or anomaly-triggered MFA—all powered by AI.

• In March 2024, CyberArk launched a new AI-powered Identity Threat Detection and Response (ITDR) module that uses machine-learning to analyze privileged account behavior and detect anomalous sessions in real time. Source: www.cyberark.com

• In August 2023, Okta introduced continuous risk-based authentication using AI that adapts login requirements based on device behavior and user patterns, reducing verification friction by over 20%. Source: www.okta.com

• In May 2024, Microsoft announced an update to its Azure Active Directory Identity Protection offering, embedding AI risk scoring to better flag compromised sign-ins and risky identities. Source: www.microsoft.com

• In November 2023, SailPoint unveiled its identity security platform integration with generative AI, allowing identity access policies to be dynamically generated based on threat intelligence. Source: www.sailpoint.com

This market report covers a comprehensive analysis of the AI Identity Security Solutions industry globally, focusing on technology, deployment types, use cases, and key geographies. The report segments the market by identity-security technology (behavioral analytics, biometric authentication, continuous verification), by application (privileged access management, zero-trust, machine identity governance, fraud prevention), and by end-user (financial services, healthcare, large enterprises, governments, cloud-native firms). Geographically, it examines regional dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regulatory drivers, investment trends, and deployment maturity. On the technology front, the report delves into AI architectures such as risk-scoring engines, generative-AI for identity modeling, explainable AI, and orchestration platforms. It also explores emerging challenges and opportunities: compliance frameworks, privacy-driven identity governance, machine-to-machine identity risk, and identity for non-human actors. Strategic focus areas include innovation through M&A, partnerships between identity vendors and cloud/zero-trust firms, and regional differentiation in product adoption.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 7,910.3 Million |

|

Market Revenue in 2032 |

USD 33,338.5 Million |

|

CAGR (2025 - 2032) |

19.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

CyberArk, Okta, Microsoft, SailPoint, Ping Identity, ForgeRock, One Identity, Broadcom (Symantec), IBM Security, RSA Security, Saviynt, Thales, Ivanti, NetIQ |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |