Reports

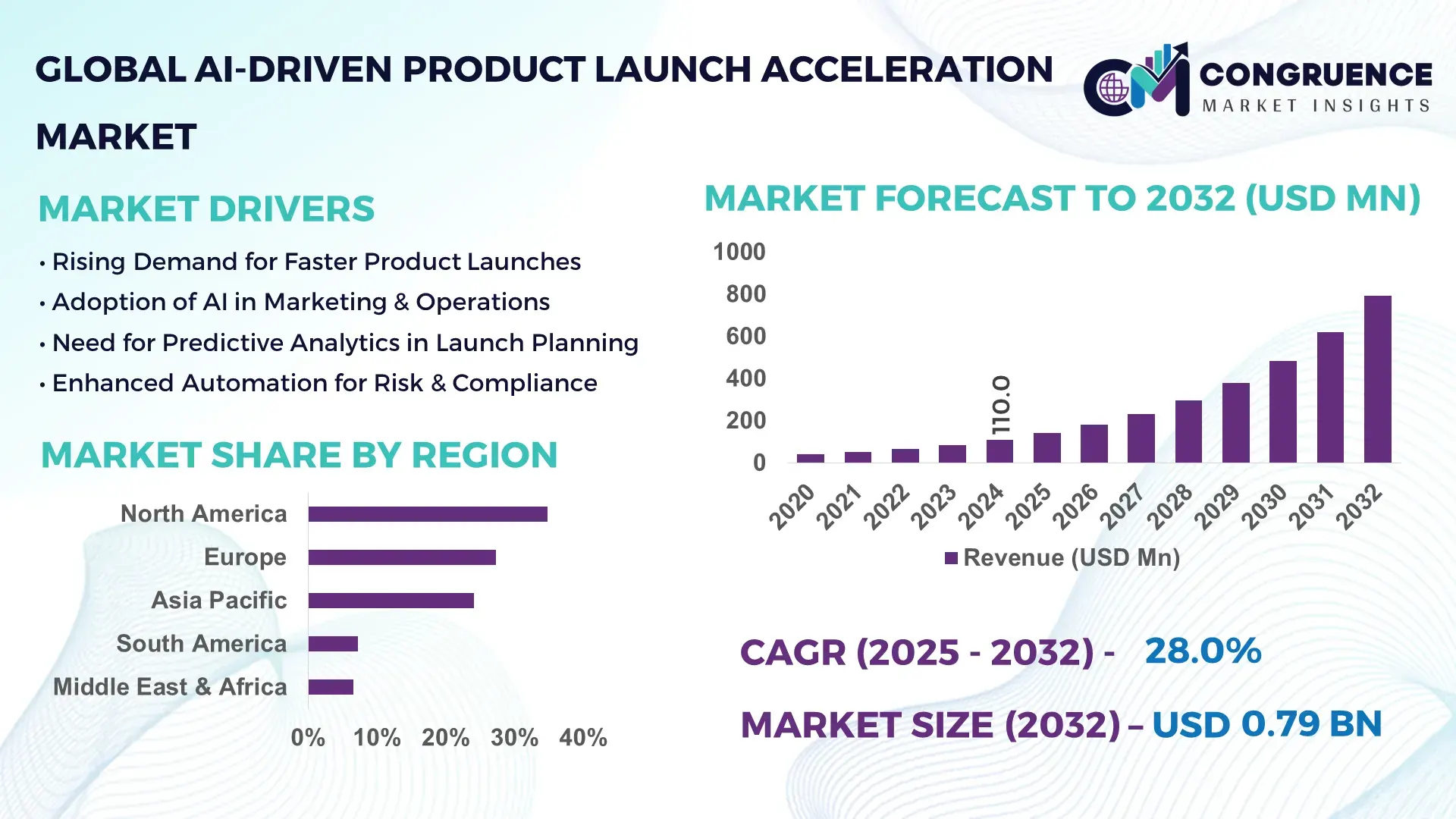

The Global AI-Driven Product Launch Acceleration Market was valued at USD 110.0 Million in 2024 and is anticipated to reach a value of USD 792.6 Million by 2032 expanding at a CAGR of 28% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rapid enterprise adoption of AI-enabled automation across product development, GTM execution, and cross-functional launch workflows.

The United States leads global development of AI-driven product launch acceleration technologies, supported by the world’s largest concentration of enterprise AI deployments, with over 6,500 AI-focused firms and more than USD 67 Billion invested in AI-integrated SaaS capabilities between 2020 and 2024. The country’s strong innovation ecosystem enables large-scale production of orchestration engines, predictive launch analytics, and automated testing frameworks. US enterprises report above 45% adoption of AI-based GTM optimization tools, particularly in technology, retail, and digital consumer sectors, reflecting strong integration into operational launch systems.

Market Size & Growth: Valued at USD 110.0 Million in 2024, projected to reach USD 792.6 Million by 2032, expanding at a 28% CAGR driven by rising enterprise automation of launch workflows.

Top Growth Drivers: 42% rise in AI-led workflow automation; 38% improvement in predictive launch accuracy; 33% increase in cross-functional coordination efficiency.

Short-Term Forecast: By 2028, AI-assisted launch platforms expected to improve project cycle efficiency by 27% through automated planning and reduced manual operations.

Emerging Technologies: Rapid adoption of generative AI for content automation; multi-agent orchestration for real-time launch decisions; digital twins for pre-launch simulation.

Regional Leaders: North America expected to reach USD 342 Million by 2032 with strong enterprise AI uptake; Europe projected at USD 188 Million with advanced regulatory alignment; Asia Pacific to reach USD 164 Million driven by high digital adoption.

Consumer/End-User Trends: High usage among technology, retail, and consumer electronics firms where over 40% rely on AI for testing, messaging, and performance benchmarking.

Pilot or Case Example: In 2024, a US-based SaaS vendor ran an AI-driven launch sequencing pilot achieving 31% reduction in campaign downtime.

Competitive Landscape: Leading player holds ~19% market share, followed by four major competitors offering AI-enabled orchestration, analytics, and collaboration modules.

Regulatory & ESG Impact: Global digital governance policies are promoting compliant AI adoption with firms targeting 20% improvement in auditability and traceability.

Investment & Funding Patterns: More than USD 4.8 Billion invested in AI-enabled enterprise productivity platforms between 2022–2024, with increasing funding for workflow automation.

Innovation & Future Outlook: Advancements in real-time AI decision engines, autonomous campaign optimization, and cross-platform integration are shaping next-generation launch environments.

Unique industry advances within the AI-Driven Product Launch Acceleration Market include rising adoption of AI-enabled orchestration tools in technology, consumer goods, and digital commerce sectors, supported by emerging predictive testing models, simulation platforms, and compliance-driven automation. Strong deployment flows in North America and East Asia, combined with rapid regulatory modernization and enterprise digitalization, are accelerating adoption across both mature and emerging business environments.

The AI-Driven Product Launch Acceleration Market has emerged as a mission-critical pillar of enterprise digital transformation, enabling organizations to streamline launch cycles, strengthen forecasting accuracy, and improve cross-functional coordination. As enterprises face shorter innovation cycles and heightened competitive intensity, AI-powered launch systems offer measurable efficiency gains by automating planning, sequencing, simulation, and performance monitoring. Modern orchestration engines now integrate demand sensing, NLP-based content automation, and multi-agent reasoning, resulting in up to 35% faster end-to-end launch execution compared to traditional manual frameworks. In addition, next-generation platforms provide deeper visibility into risk management, compliance validation, and multi-market alignment, supporting global expansion strategies.

A comparative benchmark demonstrates this transition: Intelligent Workflow Automation delivers 42% operational improvement compared to legacy project management standards. Regional variations further influence strategic planning—North America dominates in volume, while Asia Pacific leads in adoption with 46% of enterprises deploying at least one AI-enabled launch system. By 2027, autonomous AI-driven sequencing is expected to reduce planning time by 29%, transforming how firms prepare, validate, and execute complex launches.

ESG alignment is strengthening strategic relevance. Firms are committing to structured operational transparency, targeting 25% improvements in digital audit readiness by 2028. In 2024, a European consumer-tech company achieved a 34% cycle-time reduction through an AI-driven initiative designed to optimize regulatory pre-validation and adaptive market testing. As AI capabilities mature, integration with predictive analytics, real-time decision engines, and simulation-based launch modeling will shape the future ecosystem. The AI-Driven Product Launch Acceleration Market will increasingly serve as a foundation for enterprise resilience, regulatory compliance, and sustainable, future-oriented growth.

The AI-Driven Product Launch Acceleration Market is expanding as enterprises prioritize automation, predictive modeling, and advanced digital infrastructure to shorten launch cycles and improve execution accuracy. The market is influenced by strong adoption of generative AI tools, workflow automation platforms, and data-driven GTM optimization systems. Accelerated digital transformation across technology, retail, healthcare, and consumer goods sectors is boosting demand for intelligent orchestration platforms and multi-layered AI analytics. Rising investments in enterprise AI governance, model monitoring, and compliance automation are further shaping the competitive landscape. Shifts toward cloud-native architectures, microservices-led deployment, and integrated collaboration ecosystems continue to support scalable adoption across both developed and emerging regions.

Automation is playing a significant role in transforming the AI-Driven Product Launch Acceleration Market by reducing manual processes, enhancing precision, and allowing enterprises to handle more complex multi-market launches. Automated planning engines now support detailed sequencing, dependency tracking, and scenario modeling, enabling up to 40% improvement in operational efficiency. Predictive launch simulators use large datasets to anticipate performance deviations and optimize timing decisions. Industries such as technology and retail increasingly adopt these tools to manage fast-changing consumer expectations, relying on automated content generation, risk scoring, and testing workflows. Automated versioning and collaborative AI tools further streamline cross-functional alignment, helping teams shorten approval cycles and improve execution. As automation becomes more advanced, platform integration with CRM, PLM, and analytics software provides unified insights, strengthening decision-making and reducing error margins across launch phases.

The scarcity of skilled AI professionals is a significant restraint affecting the AI-Driven Product Launch Acceleration Market, particularly in regions where enterprise digital transformation is still emerging. Organizations face challenges in deploying advanced orchestration engines due to limited expertise in model training, workflow optimization, and AI governance. This shortage increases implementation timelines and elevates operating costs by up to 25% due to reliance on external consultants. Many enterprises also struggle to maintain quality data pipelines, which are essential for predictive analytics and automated decision-making. Insufficient AI literacy across marketing, product, and operations teams slows integration of new tools and inhibits full utilization of platform capabilities. Additionally, enterprises in developing regions report gaps in data infrastructure, limiting their ability to implement high-accuracy simulation models and automated content generation systems. This talent and infrastructure deficit slows overall market scalability.

Enterprise-wide digital acceleration presents strong opportunities for growth in the AI-Driven Product Launch Acceleration Market, especially as organizations increase investments in workflow automation, cloud-native deployments, and real-time analytics. More than 60% of enterprises undergoing major digital modernization are prioritizing launch automation capabilities to enhance cross-functional collaboration and decision accuracy. Integration of AI-assisted content engines, adaptive simulation environments, and multi-agent orchestration models is opening new avenues for precision-based launch optimization. Expanding use of digital twins for pre-launch testing offers opportunities to minimize risks and reduce cycle times. Furthermore, sectors such as consumer electronics, e-commerce, and healthcare are adopting advanced analytics tools to align launch timing with demand signals, creating additional demand for predictive operational systems. As global enterprises expand into multi-market environments, demand for scalable, compliance-ready AI launch platforms will continue to rise.

Integration complexities pose a substantial challenge for the AI-Driven Product Launch Acceleration Market as enterprises grapple with connecting orchestration systems to CRM, ERP, PLM, analytics platforms, and marketing automation suites. Many organizations operate fragmented digital ecosystems with incompatible data architectures, which can increase deployment timelines by 30% or more. Data normalization issues complicate predictive modeling and hinder simulation accuracy. Legacy systems often lack APIs or require extensive customization to support AI-driven workflows. Cross-departmental alignment challenges also arise as teams adapt to AI-powered execution models and new collaboration tools. Security, compliance, and data governance requirements further complicate integration, delaying enterprise rollout. These combined issues heighten operational costs, reduce system adoption speed, and limit the full strategic impact of AI-driven launch acceleration technologies.

Acceleration of AI-Powered Multimodal Launch Systems: Enterprises are integrating multimodal AI engines that combine text, image, and behavioral analytics to enhance pre-launch testing efficiency. These systems have enabled up to 37% faster insight generation and 28% reduction in corrective iterations during early launch cycles, significantly optimizing workflows in technology and consumer electronics sectors.

Growth in Predictive Demand-Sensing Engines: Predictive engines using over 200+ data variables are reshaping demand forecasting accuracy, helping companies improve launch timing accuracy by 32%. Adoption is particularly strong in North America and Asia Pacific, where over 45% of digitally mature enterprises are implementing real-time predictive launch models.

Expansion of AI-Enabled Cross-Functional Collaboration Platforms: Collaborative AI systems have recorded 41% improvement in communication efficiency and 30% reduction in approval delays across product, marketing, and supply-chain teams. These platforms support automated version control, task allocation, and risk tracking, enabling global enterprises to streamline multi-region launches.

Rise of Simulation-Based “Digital Launch Twins”: Simulation platforms replicating launch environments allow firms to test messaging, sequencing, and risk factors with 48% higher accuracy before deployment. Adoption has increased across complex sectors such as automotive and consumer goods, where over 35% of companies now run digital launch tests before full execution.

The AI-Driven Product Launch Acceleration Market is segmented by type, application, and end-user, reflecting a broadening ecosystem of intelligent tools supporting faster and more accurate product launches. Market segmentation shows strong traction in advanced AI orchestration engines, predictive analytics systems, and autonomous workflow automation tools, each contributing to differentiated adoption patterns. On the application side, organizations primarily leverage these platforms for launch planning, campaign sequencing, testing automation, and cross-functional execution management, driven by rising operational complexity and shorter innovation cycles. End-user analysis highlights robust demand from technology, consumer goods, retail, and healthcare enterprises, supported by expanding digital maturity and increasing reliance on real-time decision intelligence. Collectively, these segments demonstrate accelerating adoption across diverse industry settings, with new integrations into CRM, PLM, and digital commerce platforms strengthening long-term growth potential.

The AI-Driven Product Launch Acceleration Market comprises several key types, including AI orchestration platforms, predictive launch analytics engines, autonomous content generation systems, and simulation-based launch modeling tools. Among these, AI orchestration platforms currently lead the market with approximately 41% of total adoption, supported by their ability to coordinate multi-stage launch workflows, monitor dependencies, and ensure real-time operational alignment across diverse business functions. Predictive launch analytics follows with around 28%, offering data-driven insights that enhance timing accuracy and reduce performance variability across product categories. The fastest-growing type is simulation-based “digital launch twin” technology, expanding at an estimated 18% CAGR, driven by rising enterprise demand for risk-free testing environments and precision-based launch optimization. These systems enable firms to evaluate message positioning, operational timing, and cross-market performance before deployment. Autonomous content generation systems, which combine generative AI with domain-specific models to automate product messaging and testing scripts, contribute to roughly 19% combined share when grouped with niche workflow intelligence tools.

Applications within the AI-Driven Product Launch Acceleration Market span launch planning, campaign sequencing, automated testing, risk modeling, compliance validation, and post-launch performance optimization. Launch planning is the leading application, accounting for 39% of total adoption, driven by increasing demand for structured cycle management and automated forecasting capabilities that reduce operational uncertainty. Campaign sequencing follows with approximately 27%, supported by growing reliance on AI agents that coordinate multichannel execution and monitor real-time deviations in campaign performance. The fastest-growing application is automated testing and validation, expanding at an estimated 17% CAGR, fueled by rising deployment of generative AI testing suites capable of evaluating content accuracy, message consistency, compliance alignment, and user-journey integrity. Other applications—including cross-functional collaboration automation and real-time risk modeling—collectively represent 34% of remaining adoption, delivering value across complex enterprise environments. In 2024, more than 38% of enterprises globally reported piloting AI-led launch automation for customer experience platforms, reflecting broader digital transformation pressures. Over 60% of Gen Z consumers report higher trust in brands with AI-supported digital engagement workflows, increasing the relevance of real-time adaptation.

End-users in the AI-Driven Product Launch Acceleration Market include technology firms, consumer goods manufacturers, retail companies, healthcare organizations, and industrial enterprises. Technology companies constitute the leading segment with 44% of total adoption, driven by faster product cycles, large digital infrastructures, and higher AI maturity across operational units. Consumer goods and retail collectively account for 31%, supported by rising product variation, omnichannel execution requirements, and real-time demand sensing adoption. Healthcare and life sciences represent the fastest-growing end-user group, expanding at an estimated 19% CAGR, as organizations adopt AI-enabled platforms for clinical product launches, regulatory documentation automation, and predictive risk modeling. Remaining industries—including automotive, industrial equipment, and enterprise SaaS providers—collectively make up 25% of adoption, reflecting steady integration into product development and operational workflows. In 2024, more than 38% of global enterprises piloted AI-driven launch orchestration for customer-facing platforms, reinforcing the rising importance of intelligent automation. In the U.S., 42% of hospitals experimented with AI systems combining clinical data and operational workflows to accelerate product introduction and regulatory alignment.

North America accounted for the largest market share at 34.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.6% between 2025 and 2032.

North America’s dominance stems from the early deployment of AI orchestration engines across over 1,200 large enterprises and the presence of more than 450 AI-focused SaaS vendors contributing to product launch automation. Europe followed with a 27.3% share, supported by stringent digital compliance frameworks and rising demand for explainable AI across Germany, France, and the UK. Asia-Pacific reached 24.1% in 2024, driven by China’s rapidly scaling digital commerce ecosystem and India’s rising enterprise software adoption. South America held 7.2%, and the Middle East & Africa captured 6.6%, collectively strengthening through government-funded digital transformation programs, industry automation initiatives, and localized AI solutions addressing regional product rollout complexities.

North America captured a significant 34.8% market share in 2024, supported by high enterprise readiness and widespread integration of AI-led launch orchestration tools. Demand is driven strongly by healthcare, finance, and consumer technology sectors, each relying on real-time predictive analytics and automated campaign sequencing to manage frequent product rollouts. The region has experienced notable regulatory momentum, with updated U.S. AI governance guidelines and Canada’s Algorithmic Impact Assessment encouraging responsible automation. North American companies exhibit accelerated digital transformation, with more than 62% of enterprises deploying generative AI for content validation and scenario testing. Local players such as HubSpot expanded their AI automation suites in 2024 to support multi-stage product launch workflows, enabling mid-sized firms to shorten launch cycles by up to 22%. Consumer behavior in the region favors automated personalization, with enterprises in healthcare and finance showing the highest adoption intensity.

Europe accounted for approximately 27.3% of the global market share in 2024, driven by strong adoption across Germany, the UK, France, and the Nordics. Regional growth is shaped heavily by the EU AI Act, GDPR-driven compliance frameworks, and sustainability initiatives that encourage the use of transparent, explainable AI in product development and go-to-market planning. European enterprises are increasingly adopting digital launch twins, automated risk modeling, and AI-based compliance validation to support complex cross-border product strategies. Countries like Germany lead in industrial AI deployment, while the UK shows higher adoption of AI-driven marketing automation. Local innovators such as Finland-based Aiven expanded cloud-based AI launch orchestration capabilities in 2024, enabling scalable integration between product data streams and campaign workflows. Consumer behavior in Europe favors transparency and regulatory compliance, driving strong demand for explainable AI systems embedded in product launch tools.

Asia-Pacific represented 24.1% of global market volume in 2024 and ranked as the fastest-growing region in overall adoption. China, India, Japan, and South Korea collectively contribute over 78% of regional demand, driven by rapidly expanding e-commerce ecosystems, high mobile penetration, and strong investments into AI-based industrial digitalization. Manufacturing and consumer electronics companies in China and Japan widely deploy AI simulation engines and automated launch testing tools to accelerate product cycles. India’s SaaS expansion and cloud infrastructure growth have significantly boosted enterprise adoption of AI-driven launch workflows. Innovation hubs such as Shenzhen, Bengaluru, and Tokyo are driving advancements in real-time analytics, generative content engines, and workflow intelligence. A notable example includes India’s Zoho strengthening its AI orchestration capabilities in 2024 to support automated multi-market product releases. Regional consumer behavior trends show strong preference for mobile-first engagement, rapid product iteration, and AI-enabled personalization.

South America accounted for roughly 7.2% of global market share in 2024, with Brazil and Argentina representing more than 61% of regional demand. Growth is supported by increasing digital adoption in financial services, retail, and media—industries that rely heavily on multilingual content generation and AI-assisted campaign sequencing. Infrastructure development in cloud computing and regional data centers has accelerated enterprise readiness for AI-driven product launch solutions. Governments in Brazil and Chile have introduced digital transformation incentives and AI-focused innovation programs to increase competitiveness across consumer markets. Local companies such as Brazil’s Take Blip expanded AI-driven customer experience automation in 2024, indirectly supporting demand for launch acceleration technologies. Consumer behavior in this region is characterized by strong emphasis on localized content, cultural adaptation, and language-specific optimization across marketing channels.

The Middle East & Africa region held a 6.6% market share in 2024, with strong demand originating from technology adoption initiatives in the UAE, Saudi Arabia, and South Africa. Growth is driven by rapid digital modernization across sectors such as oil & gas, construction, financial services, and telecommunications, where AI-based orchestration and automated validation tools are increasingly applied for product rollout efficiency. Regional governments have invested heavily in AI strategies, including the UAE’s National AI Program and Saudi Vision 2030, promoting enterprise adoption of intelligent automation. Local players like Bayanat AI expanded predictive analytics capabilities in 2024 to support complex operational planning and product introduction workflows. Consumer behavior in the region favors streamlined digital services, with heightened interest in automation for service-driven industries.

United States – 29.4% Market Share: Dominance enabled by strong enterprise AI adoption, advanced cloud infrastructure, and high product launch frequency across technology and healthcare sectors.

China – 18.1% Market Share: Leadership supported by large-scale digital commerce activity, rapid innovation cycles, and extensive integration of AI-driven automation across manufacturing and consumer electronics.

The AI-Driven Product Launch Acceleration Market is moderately fragmented, featuring over 30 active global competitors ranging from enterprise software giants to niche AI orchestration startups. The combined share of the top 5 players is estimated at approximately 38–45%, indicating substantial room for innovation and specialization. Key companies are heavily investing in agentic AI, workflow orchestration, and multi-agent platforms, with several strategic initiatives underway: partnerships (e.g., alliances between orchestration vendors and cloud providers), new product launches (such as AI agents dedicated to sequencing and launch decisioning), and even acquisitions of smaller AI startups to bolster automation capabilities.

Competitive positioning varies: legacy enterprise software firms emphasize governance, auditability, and integration with PLM/CRM systems; pure-play AI companies stress agility, real-time orchestration, and predictive analytics; and niche players focus on very specific verticals such as life sciences or consumer goods. Innovation trends that influence this landscape include the rise of multi-agent orchestration frameworks, digital twin modeling for launch simulation, and generative AI for automatic campaign content and testing.

Several firms are formalizing agent governance frameworks and embedding explainability into their orchestration stacks. The drive to reduce manual launch coordination, especially in large enterprises with cross-functional go-to-market operations, is fueling competitive intensity. Many players are also forming partnerships with consulting firms and domain experts to offer managed “AI launch acceleration as a service,” further amplifying competition and market reach.

Omneky

Microsoft

IBM

The AI-Driven Product Launch Acceleration Market is underpinned by a suite of technologies that enable smarter, faster, and more coordinated product introductions. Central among these is multi-agent orchestration, where autonomous AI agents coordinate across launch workflows—handling tasks like sequencing campaigns, validating compliance, and integrating cross-functional dependencies. This agentic architecture is rapidly maturing to support persistent context, memory, and long-term goal alignment, making it possible to run complex launch operations with minimal human intervention.

Generative AI is another critical enabler; it automates the creation of launch content (marketing copy, test cases, campaign messages), enabling teams to iterate quickly. Simulation-based “digital launch twins” are emerging as powerful tools, where firms mirror product launch environments in a virtual space to test hypotheses, optimize sequence, and mitigate risk before live deployment. These models can replicate launch scenarios under different market conditions, helping teams validate strategy without operational exposure.

Predictive analytics and demand sensing technologies also play a vital role, using large datasets from market research, CRM, and external signals (e.g., social trends) to forecast adoption trajectories, identify risk, and optimize timing. In addition, integration technologies—including APIs, iPaaS (integration-platform-as-a-service), and low-code/no-code orchestration layers—are enabling faster embedding of AI-driven launch platforms into existing enterprise architecture (CRM, ERP, PLM, data lakes).

Finally, explainable and governance-focused AI tools are gaining traction. As enterprises scale their AI-driven launch frameworks, they demand traceability, audit logs, policy enforcement, and compliance mechanisms. These features are being baked into orchestration products, allowing model actions to be reviewed, constrained, and governed. This technological convergence ensures that AI-driven launch acceleration is not only powerful but also compliant and transparent for large enterprises.

In September 2023 Microsoft announced Microsoft 365 Copilot for enterprises, with general availability set for November 1, 2023. The release bundles AI assistants into workflow apps, enabling automated content generation, task summarization, and contextual workplace insights that accelerate product collateral and launch coordination. Source: www.microsoft.com

In May 2024 IBM unveiled the next chapter of watsonx, releasing open-source Granite models and expanding watsonx capabilities for enterprise AI lifecycle, model alignment, and domain tuning — measures that enable firms to operationalize generative AI for launch analytics, simulation, and governance at scale. Source: www.ibm.com

On January 8, 2024 Omneky announced it achieved SOC 2 Type II compliance, validating enterprise-grade security controls across its generative advertising platform. The certification strengthened Omneky’s position to support large-scale, automated campaign generation and secure AI-driven launch orchestration for enterprise customers. Source: www.omneky.com

In May 2024 Google expanded generative-AI experiences across Search (AI Overviews rollout) and other products, bringing AI-driven summarization and planning capabilities to hundreds of millions of users; these capabilities support faster discovery, market research, and content ideation for launch teams. Source: www.blog.google

This report covers global market dynamics of AI-Driven Product Launch Acceleration, addressing all major geographic regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It analyzes product types, including orchestration platforms, predictive analytics engines, content generation systems, and simulation-based modeling tools, detailing how each type supports different parts of the launch lifecycle.

On the application side, the scope extends to launch planning, campaign sequencing, automated testing, compliance validation, risk modeling, and post-launch performance optimization. The report also dives into end-user segments, from technology and consumer goods firms to healthcare, retail, and industrial enterprises, examining adoption rates, use-case maturity, and digital transformation strategies.

Technology insights include agentic AI, generative models, multi-agent orchestration, digital twin modeling, and integration layers such as iPaaS. The report highlights innovation trends such as explainability, agent governance, persistent memory, and real-time simulation.

Emerging and niche areas are also addressed—such as AI acceleration in pharmaceutical launches, SaaS product rollouts, and emerging market deployments. The analysis integrates regulatory and governance factors, including AI safety, auditability, and enterprise compliance, and reviews funding and partnership activity shaping the competitive landscape.

Designed for business decision-makers, this report provides strategic intelligence on market participants, technology roadmaps, investment priorities, and future growth pathways to guide enterprise investments, partner selection, and roadmap planning in the AI-driven product launch domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 110.0 Million |

| Market Revenue (2032) | USD 792.6 Million |

| CAGR (2025–2032) | 28.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Adobe, UiPath, Axtria, Google, Omneky, Microsoft, IBM |

| Customization & Pricing | Available on Request (10% Customization Free) |