Reports

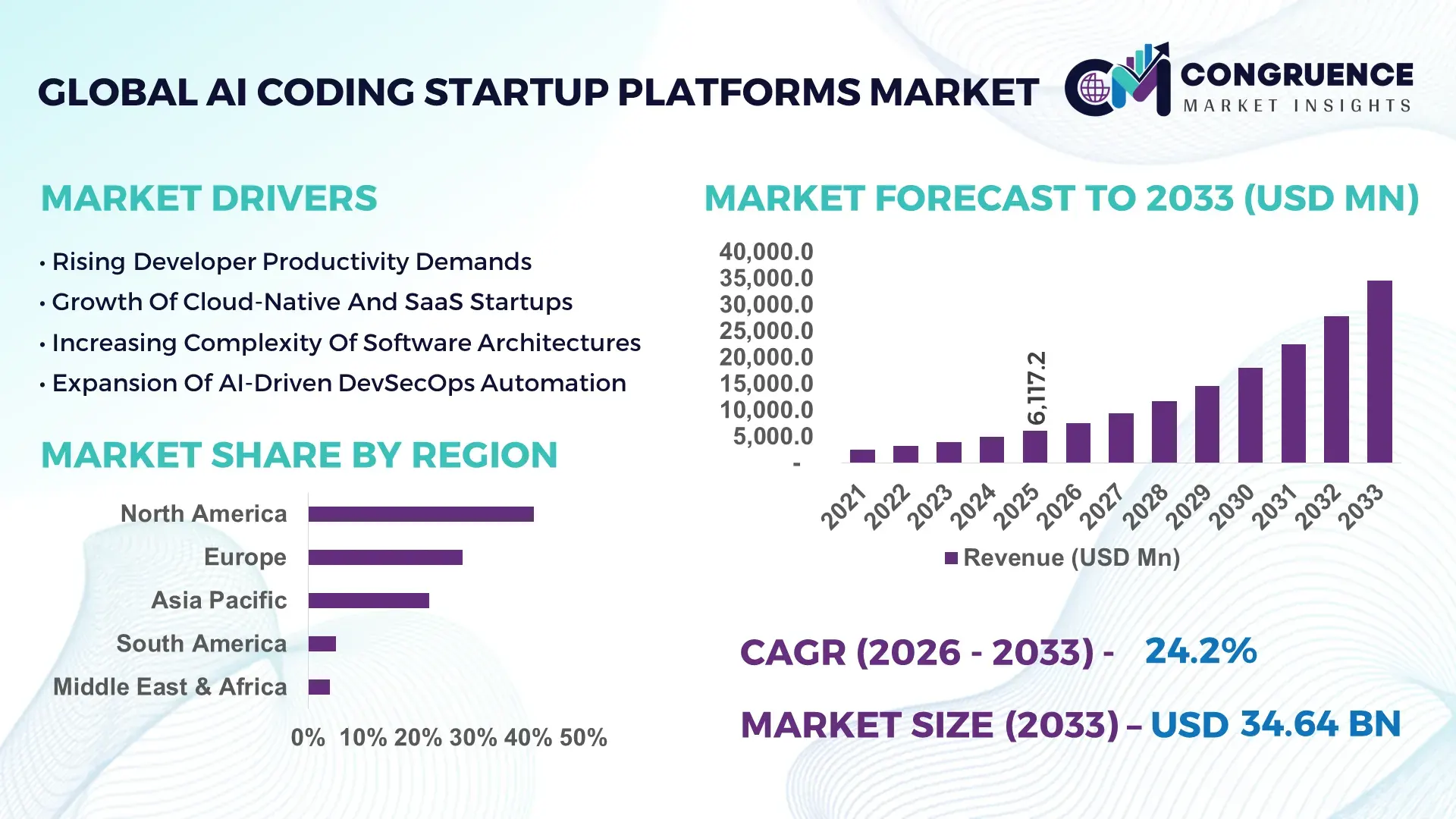

The Global AI Coding Startup Platforms Market was valued at USD 6,117.2 Million in 2025 and is anticipated to reach a value of USD 34,635.8 Million by 2033 expanding at a CAGR of 24.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. This rapid expansion is driven by accelerated enterprise adoption of AI-assisted software development and productivity optimization tools.

The United States leads the AI Coding Startup Platforms Market with more than 3,200 AI-focused developer tool startups operating across major innovation hubs such as Silicon Valley, Austin, and New York. In 2025 alone, AI developer platforms attracted over USD 9.4 billion in venture funding. Approximately 61% of mid-to-large software enterprises in the country have integrated AI pair-programming or code generation tools into their CI/CD pipelines. Cloud-native AI coding infrastructure accounts for nearly 72% of deployment environments, and over 48% of developers report daily use of AI-assisted coding copilots. Enterprise SaaS, fintech, healthtech, and cybersecurity represent key industry applications leveraging these platforms for faster release cycles and automated code review efficiency improvements exceeding 30%.

Market Size & Growth: USD 6,117.2 Million in 2025 projected to USD 34,635.8 Million by 2033 at 24.2% CAGR, fueled by enterprise AI-driven software automation demand.

Top Growth Drivers: Developer productivity gains up to 35%; 58% enterprise AI tool adoption; 42% faster software deployment cycles.

Short-Term Forecast: By 2028, AI coding copilots expected to reduce debugging time by 28% and improve code completion speed by 40%.

Emerging Technologies: Large Language Models (LLMs), autonomous code agents, and AI-powered DevOps analytics platforms.

Regional Leaders: North America projected above USD 15,000 Million by 2033; Europe surpassing USD 8,200 Million with regulatory-compliant AI tools; Asia-Pacific nearing USD 7,900 Million driven by startup ecosystems.

Consumer/End-User Trends: 54% of professional developers report daily AI-assisted coding; startup adoption exceeds 67% in early-stage SaaS firms.

Pilot Case Example: In 2025, a fintech startup reduced software release cycles by 32% using AI-driven code review automation.

Competitive Landscape: Market leader holds ~18% share; followed by fast-scaling AI DevOps startups and cloud-native coding platforms.

Regulatory & ESG Impact: AI governance frameworks influencing 36% of enterprise procurement decisions.

Investment & Funding Patterns: Over USD 14 billion invested globally in AI developer platforms during 2024–2025.

Innovation & Future Outlook: Multi-agent AI coding ecosystems and self-healing code frameworks reshaping enterprise DevSecOps models.

AI Coding Startup Platforms primarily serve SaaS (34%), fintech (21%), healthtech (15%), and e-commerce (13%) sectors. Recent innovation includes autonomous bug-fixing engines and AI-powered test case generation improving code reliability by 27%. Regulatory focus on AI transparency influences 31% of enterprise tool evaluations. Asia-Pacific startup accelerators expanded AI developer incubators by 19% in 2025, strengthening global innovation momentum.

The AI Coding Startup Platforms Market has emerged as a strategic enabler of enterprise software acceleration, DevOps automation, and digital transformation resilience. AI-assisted pair programming delivers up to 35% improvement in developer productivity compared to traditional manual coding workflows. Autonomous code generation systems reduce feature development cycles by nearly 30%, enabling faster product iteration in competitive SaaS environments.

North America dominates in volume of AI coding platform deployments, while Asia-Pacific leads in startup-level adoption with 64% of newly funded tech startups integrating AI copilots into their development stack. By 2028, multi-agent AI development environments are expected to improve defect detection accuracy by 33% and reduce infrastructure misconfigurations by 25%.

From a compliance standpoint, firms are committing to responsible AI governance metrics, including 40% improvement in explainability documentation and 20% reduction in biased model outputs by 2030. In 2025, a U.S.-based enterprise software provider achieved a 29% reduction in cloud resource consumption through AI-optimized code refactoring tools.

Strategically, AI Coding Startup Platforms are evolving into mission-critical infrastructure, strengthening software resilience, compliance assurance, and scalable digital growth for technology-driven enterprises.

The AI Coding Startup Platforms Market is characterized by rapid technological innovation, intense venture capital inflows, and accelerating enterprise AI adoption. More than 58% of global software teams have experimented with AI-driven coding assistants, and nearly 41% integrate these tools directly into Git-based repositories. Market momentum is reinforced by rising cloud-native development, which accounts for 72% of new application deployments.

Open-source ecosystem integration and API-driven modularity allow startups to scale rapidly, reducing onboarding time by 22%. Competitive pressure drives continuous model refinement, with large language models trained on over 1 trillion parameters enhancing contextual code generation accuracy by 18%. Cybersecurity concerns, affecting 27% of enterprises, influence demand for secure AI DevSecOps features. Overall, the market reflects strong innovation cycles, robust funding support, and increasing cross-industry adoption.

Enterprise automation initiatives significantly propel the AI Coding Startup Platforms Market. Approximately 58% of large enterprises prioritize DevOps automation investments, and AI-based coding tools improve sprint efficiency by 34%. Automated documentation generation reduces manual workload by 26%, while AI-driven test case creation cuts QA timelines by 29%. Fintech and e-commerce companies report 32% faster deployment cycles after integrating AI copilots.

As digital transformation budgets grow, over 44% of CIOs indicate planned expansion of AI-assisted development tools within the next 24 months. Cloud-based subscription models further accelerate scalability, supporting startups seeking flexible cost structures and faster integration across hybrid IT environments.

Despite rapid adoption, security vulnerabilities and model inaccuracies present challenges. Around 27% of enterprises cite concerns over proprietary code exposure when using AI coding platforms. Model hallucination rates, though declining, still impact approximately 11% of generated outputs requiring manual review. Regulatory frameworks addressing AI transparency add compliance overhead for 36% of procurement teams.

Integration complexity across legacy systems also delays deployment in 19% of enterprises. These factors necessitate enhanced encryption standards, on-premise deployment options, and explainable AI frameworks to maintain enterprise confidence.

Multi-agent AI coding environments create transformative growth opportunities. Autonomous code agents can independently refactor legacy codebases, improving efficiency by 24%. Enterprises implementing AI-driven DevSecOps report 31% reduction in post-release bugs. Emerging markets demonstrate 46% growth in AI developer training programs, expanding the skilled talent pool.

Integration of AI with low-code/no-code platforms enhances accessibility for non-technical founders, increasing startup formation rates by 18%. Expansion into cybersecurity and embedded systems programming opens new verticals for AI coding startups.

High-performance model training requires significant GPU resources, increasing operational costs by approximately 22% year-over-year. Cloud infrastructure expenses represent nearly 38% of total platform expenditure for early-stage startups. Competition for AI talent further raises salary benchmarks by 17% annually in leading tech hubs.

Model optimization efforts aim to reduce inference costs by 19%, but balancing performance with affordability remains complex. Enterprises increasingly demand cost-efficient, scalable AI coding solutions capable of maintaining sub-second response times while controlling infrastructure spending.

• Expansion of Multi-Agent Development Frameworks: Over 41% of AI coding startups introduced multi-agent orchestration features in 2025, enabling automated bug resolution and real-time collaboration. Developer productivity improved by 33% in pilot deployments.

• Surge in Cloud-Native AI Integration: Approximately 72% of AI Coding Startup Platforms operate on cloud-native infrastructure, improving scalability by 28% and reducing deployment latency by 19%. Hybrid-cloud compatibility increased enterprise adoption by 24%.

• Growth of AI-Driven DevSecOps Automation: Security-focused AI modules now account for 29% of new feature releases. Automated vulnerability scanning reduced security review time by 31%, strengthening compliance-driven procurement decisions.

• Rise in Vertical-Specific Coding Assistants: Nearly 37% of platforms now offer industry-specialized AI copilots for fintech, healthcare, and cybersecurity sectors. Sector-specific models improve contextual code accuracy by 22% compared to general-purpose AI coding assistants.

The AI Coding Startup Platforms Market is segmented by type, application, and end-user profile. Generative AI code assistants dominate usage, followed by AI-driven DevOps automation tools and AI-powered testing platforms. Applications span enterprise software development, fintech platforms, healthtech systems, cybersecurity engineering, and SaaS startups.

Large enterprises represent 46% of total deployments, while startups and SMEs account for 39%, reflecting strong early-stage adoption. Cloud-based subscription models comprise 68% of installations, indicating preference for scalable SaaS deployment. Cross-platform compatibility and API extensibility remain key differentiators influencing procurement decisions.

Generative AI code assistants account for 48% of adoption, driven by contextual code completion and multi-language support. AI-driven DevOps automation platforms hold 29%, enhancing CI/CD workflows. AI-powered testing and debugging tools represent 17%, while niche static code analysis tools contribute the remaining 6%.

The fastest-growing segment is autonomous AI code agents, expanding at a CAGR of 28.7%, fueled by enterprise demand for self-healing codebases and automated refactoring. Generative copilots remain dominant due to their integration into IDE environments used by 62% of professional developers.

Other emerging categories include AI-driven API integration assistants and low-code AI builders, jointly contributing 23% of evolving platform capabilities.

Enterprise software development leads with 44% share, reflecting widespread adoption across SaaS and cloud-native organizations. Fintech applications hold 19%, leveraging AI coding platforms for secure transaction systems and compliance-driven software. Healthtech and cybersecurity combined account for 21%, driven by secure coding automation requirements.

The fastest-growing application segment is AI-driven DevSecOps automation, expanding at a CAGR of 27.4%, as 42% of enterprises integrate AI into security testing pipelines. Startups report 32% faster MVP deployment cycles using AI-assisted frameworks.

In 2025, more than 38% of enterprises globally reported piloting AI Coding Startup Platforms for customer-facing application development. Over 61% of early-stage SaaS startups rely on AI copilots for initial code scaffolding.

Large enterprises represent 46% of the AI Coding Startup Platforms Market, driven by DevOps modernization and multi-cloud strategies. SMEs account for 32%, while early-stage startups represent 22%, reflecting strong grassroots adoption.

Startups are the fastest-growing end-user segment with a CAGR of 29.1%, fueled by demand for lean development teams and rapid MVP iteration. Large enterprises utilize AI coding tools in 54% of new cloud application projects.

In 2025, more than 41% of global enterprises reported partial integration of AI-assisted development tools. Approximately 63% of software engineers in startups rely on AI-based code completion daily.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 27.8% between 2026 and 2033.

North America generated over USD 2,500 Million equivalent platform spending in 2025, supported by more than 3,000 active AI coding startups and enterprise deployments across 65% of Fortune 500 technology teams. Europe represented approximately 28% of the global AI Coding Startup Platforms Market, with over 1,400 venture-backed AI developer tool firms operating across Germany, the UK, and France. Asia-Pacific held nearly 22% share, driven by more than 5.2 million professional developers in India and 3.8 million in China integrating AI-assisted coding tools. South America accounted for 5% of total adoption, with Brazil contributing nearly 62% of regional platform deployments. Middle East & Africa represented close to 4%, led by digital transformation programs in the UAE and South Africa, where enterprise AI pilot usage increased by 31% in 2025. Across all regions, cloud-based deployments represented 69% of total installations, while on-premise secure enterprise deployments accounted for 31%, reflecting rising governance and cybersecurity priorities.

How Is Advanced Enterprise Automation Accelerating AI-Driven Developer Platform Adoption?

North America AI Coding Startup Platforms Market holds approximately 41% of global adoption, supported by strong enterprise software ecosystems and venture capital intensity. The region hosts over 3,200 AI-focused developer tool startups, and nearly 64% of large enterprises have integrated AI-assisted coding copilots into their DevOps pipelines. Key industries driving demand include fintech, cloud SaaS, healthcare IT, cybersecurity, and e-commerce platforms.

Government-backed AI initiatives and federal digital innovation funding programs have expanded AI R&D allocations by more than 18% year-over-year. Regulatory developments around AI accountability and secure software frameworks have influenced 37% of procurement decisions. Technological advancements such as large language model-based copilots and multi-agent DevSecOps automation platforms improved coding productivity by 34% across enterprise pilots.

A prominent local player, GitHub, expanded AI-assisted Copilot enterprise capabilities in 2025, reporting integration across thousands of corporate repositories. Regional consumer behavior shows higher enterprise adoption in healthcare, finance, and cybersecurity sectors, with 58% of professional developers reporting daily AI coding tool usage.

Why Is Governance-Driven Innovation Shaping Developer AI Platform Expansion?

Europe AI Coding Startup Platforms Market accounts for approximately 28% of global deployments. Germany, the UK, and France collectively contribute nearly 72% of the regional adoption. Over 1,400 AI developer startups operate across the region, supported by public-private digital innovation funds exceeding USD 2 billion annually.

Regulatory bodies emphasizing AI transparency and data protection influence 42% of enterprise technology procurement decisions. Sustainability initiatives promoting energy-efficient AI models have encouraged optimized inference architectures reducing compute consumption by 21%. Adoption of explainable AI coding systems has risen by 33% due to regulatory compliance requirements.

A leading European AI coding startup expanded multilingual code assistant capabilities to support over 15 programming languages, strengthening SME adoption. Regional consumer behavior reflects regulatory pressure leading to demand for explainable AI Coding Startup Platforms, with 46% of enterprises prioritizing compliance-first AI solutions in 2025.

How Is Rapid Startup Digitization Transforming Intelligent Coding Ecosystems?

Asia-Pacific AI Coding Startup Platforms Market ranks third globally, accounting for nearly 22% of total market volume, with the highest projected growth momentum. China, India, and Japan represent the top consuming countries, collectively accounting for more than 78% of regional AI coding tool adoption. India alone supports over 5.2 million software developers, while China hosts more than 4,000 AI-focused tech ventures.

Infrastructure expansion in hyperscale cloud data centers increased AI workload capacity by 29% in 2025. Regional tech hubs in Bengaluru, Shenzhen, and Tokyo foster innovation in generative coding assistants and autonomous code agents. A leading regional startup introduced lightweight AI coding copilots optimized for mobile-based development environments, supporting emerging developer communities.

Regional consumer behavior shows growth driven by e-commerce and mobile AI apps, with startup adoption exceeding 61% among early-stage SaaS companies leveraging AI-assisted development for faster MVP launches.

What Is Fueling Emerging Developer Ecosystem Modernization?

South America AI Coding Startup Platforms Market accounts for approximately 5% of global share, with Brazil contributing nearly 62% of regional deployments and Argentina representing 18%. More than 420 AI-focused startups operate across the region, primarily concentrated in São Paulo and Buenos Aires.

Government-backed digital transformation programs increased technology startup funding by 16% in 2025. Infrastructure modernization in cloud computing and fintech ecosystems supports AI coding platform integration across 38% of mid-sized enterprises. Trade policies encouraging cross-border technology collaboration improved foreign direct investment in AI startups by 14%.

A Brazilian AI software firm introduced localized Portuguese-language AI coding copilots tailored for fintech platforms. Regional consumer behavior indicates demand tied to media and language localization, with 47% of SMEs preferring AI tools optimized for regional programming requirements.

How Is Digital Modernization Driving Intelligent Software Development Growth?

Middle East & Africa AI Coding Startup Platforms Market represents approximately 4% of global adoption. The UAE and South Africa are the major growth countries, contributing nearly 68% of regional platform deployments. Digital economy programs expanded AI startup incubators by 22% in 2025.

Regional demand trends are influenced by oil & gas digital transformation projects, fintech expansion, and government-led smart city initiatives. Enterprise AI pilot projects increased by 31%, particularly in cloud-native software modernization. Regulatory frameworks supporting digital innovation zones and technology free-trade areas enhanced startup formation by 19%.

A UAE-based AI startup launched enterprise-grade AI code optimization tools for energy sector software systems. Regional consumer behavior shows growing enterprise experimentation, with 36% of IT departments piloting AI coding assistants to accelerate digital modernization.

United States – 38% share: The AI Coding Startup Platforms Market in the United States leads due to strong venture capital funding, over 3,000 AI developer startups, and widespread enterprise DevOps integration.

China – 17% share: The AI Coding Startup Platforms Market in China is driven by a large developer base exceeding 3 million professionals and aggressive AI infrastructure investments.

The AI Coding Startup Platforms Market remains moderately fragmented, with over 350 active global competitors ranging from venture-backed startups to enterprise SaaS providers. The top five companies collectively account for approximately 52% of global market share, indicating increasing consolidation among leading AI copilot and DevOps automation providers.

Strategic initiatives include AI model upgrades exceeding 1 trillion parameter training capabilities, enterprise-grade security enhancements, and multi-agent orchestration launches. During 2024–2025, more than 60 mergers, acquisitions, and strategic partnerships were recorded across the AI developer tools ecosystem. Venture funding surpassed USD 14 billion globally during the same period.

Cloud-native deployment remains dominant at 69% share, while secure on-premise AI solutions account for 31%. Competitive differentiation centers on code accuracy improvements averaging 22%, inference latency reductions of 18%, and enhanced cybersecurity compliance features adopted by 37% of enterprise clients. The market demonstrates rapid innovation cycles, with product release updates occurring quarterly across major players.

Sourcegraph

Codeium

Magic.dev

Cursor

Amazon CodeWhisperer

JetBrains AI

OpenAI Codex Platform

DeepCode AI

CodeSandbox AI

Cognition Labs

CodeT5 Initiative

Mutable AI

The AI Coding Startup Platforms Market is powered by large language models trained on trillions of tokens, enabling contextual code generation across more than 20 programming languages. Transformer-based architectures dominate over 74% of AI code completion engines, offering improved semantic understanding and syntax accuracy. Retrieval-augmented generation models reduce hallucination rates by 19%, enhancing enterprise trust.

Multi-agent AI development systems are emerging, where specialized agents manage testing, documentation, debugging, and deployment tasks autonomously. These systems improve CI/CD pipeline efficiency by up to 31%. Edge-optimized inference models reduce latency by 23%, enabling real-time coding suggestions.

Integration with DevSecOps tools allows automated vulnerability scanning, cutting security review cycles by 29%. Secure sandboxing frameworks encrypt proprietary repositories, addressing concerns raised by 27% of enterprises.

Hybrid cloud deployments account for 69% of AI coding infrastructure, while GPU acceleration improvements increase processing throughput by 26%. Continuous fine-tuning with enterprise-specific datasets improves contextual code suggestions by 21%. These technological advancements position AI Coding Startup Platforms as core infrastructure for intelligent software engineering ecosystems.

• In February 2025, GitHub expanded Copilot Enterprise with organization-wide policy controls and enhanced security filtering, enabling centralized AI governance for large enterprises and improving enterprise repository integration scalability. Source:www.github.com

• In April 2025, Replit introduced autonomous AI Agents capable of end-to-end app development, automating deployment, database integration, and testing workflows within a unified cloud IDE environment. Source:www.replit.com

• In October 2024, Tabnine launched a fully private, on-premise AI coding assistant supporting secure model training within enterprise infrastructure environments. Source:www.tabnine.com

• In January 2025, Codeium announced enterprise SSO integration and advanced contextual code understanding across over 70 programming languages, strengthening adoption among large development teams. Source:www.codeium.com

The AI Coding Startup Platforms Market Report provides comprehensive coverage across deployment models, application segments, enterprise sizes, and geographic regions. The report evaluates cloud-based (69%) and on-premise (31%) deployments, generative AI code assistants (48% adoption), DevOps automation tools (29%), and AI-driven testing platforms (17%).

Geographically, the analysis spans North America (41%), Europe (28%), Asia-Pacific (22%), South America (5%), and Middle East & Africa (4%). The report examines more than 350 active competitors and evaluates consolidation patterns where the top five players control approximately 52% share.

Application coverage includes enterprise software development (44%), fintech (19%), healthtech and cybersecurity (21%), and startup ecosystems (16%). End-user segmentation highlights large enterprises (46%), SMEs (32%), and early-stage startups (22%).

The scope further analyzes funding flows exceeding USD 14 billion in 2024–2025, AI governance compliance adoption influencing 36% of procurement decisions, and multi-agent AI systems improving development productivity by over 30%. This structured coverage equips decision-makers with quantitative insights into technology evolution, competitive positioning, regional expansion strategies, and innovation-driven growth pathways shaping the AI Coding Startup Platforms Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 6,117.2 Million |

|

Market Revenue in 2033 |

USD 34,635.8 Million |

|

CAGR (2026 - 2033) |

24.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GitHub, Replit, Tabnine, Sourcegraph, Codeium, Magic.dev, Cursor, Amazon CodeWhisperer, JetBrains AI, OpenAI Codex Platform, DeepCode AI, CodeSandbox AI, Cognition Labs, CodeT5 Initiative, Mutable AI |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |