Reports

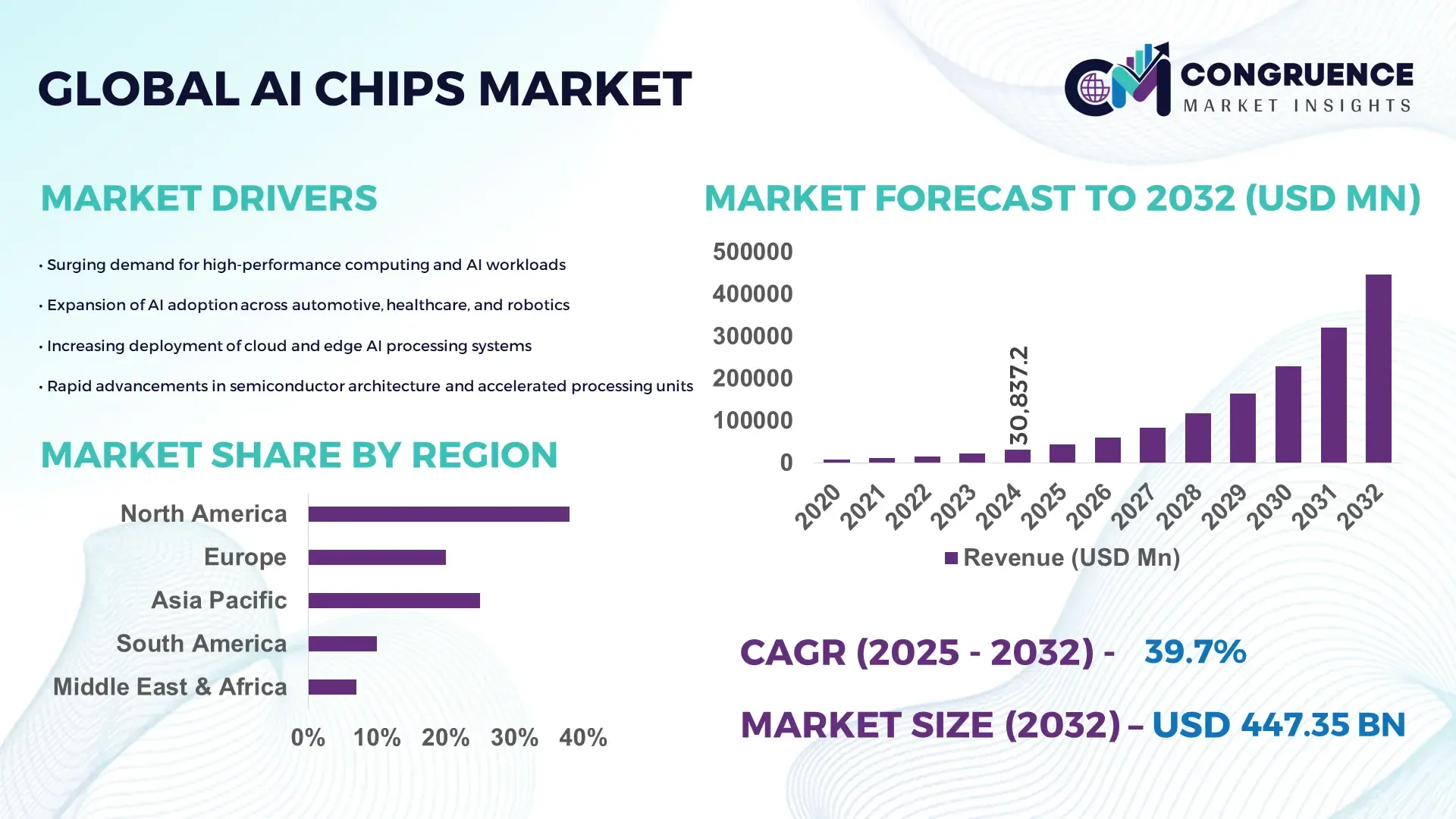

The Global AI Chips Market was valued at USD 30,837.17 Million in 2024 and is anticipated to reach a value of USD 447,348.39 Million by 2032 expanding at a CAGR of 39.7% between 2025 and 2032. This rapid growth is driven by escalating deployment of AI workloads across industries and integration of dedicated hardware accelerators.

In the United States, production capacity for AI-specific semiconductors is substantial: leading foundries such as Taiwan Semiconductor Manufacturing Company (TSMC) manufacture a significant portion of sub-7 nm AI chips, while domestic investment programmes have poured billions into expanded node-fabrication (~4 nm and below) and advanced packaging. According to analyses, U.S. compute-capacity for AI chips accounts for approximately 77% of global deployment versus roughly 12% for China in 2025. The U.S. also invests heavily in AI-chip R&D and end-use sectors — for example, data-centre acceleration, autonomous driving, and edge-AI applications — with firms like NVIDIA placing major orders with TSMC and expanding internal AI-hardware lines.

Market Size & Growth: Current market value at USD 30,837.17 Million (2024), projected value of USD 447,348.39 Million by 2032, with an expected CAGR of 39.7% — powered by escalating demand for AI-training and inference workloads.

Top Growth Drivers: adoption of AI across enterprise platforms increasing ~45 percent; efficiency improvements in dedicated AI chips boosting throughput ~30 percent; edge-AI deployment growth accelerating ~50 percent.

Short-Term Forecast: By 2028, average performance gain per AI accelerator expected to improve ~60 percent and cost per TOPS (tera-operations per second) to reduce ~35 percent.

Emerging Technologies: Trends include neuromorphic computing architectures, photonic-AI accelerators, and in-memory computing solutions.

Regional Leaders: North America projected USD 175,000 Million by 2032 (driven by hyperscale datacentres); Asia-Pacific projected USD 135,000 Million by 2032 (strong edge-AI adoption in IoT and manufacturing); Europe projected USD 60,000 Million by 2032 (automotive and industrial robotics integration).

Consumer/End-User Trends: Key end-users include cloud service providers, autonomous-vehicle manufacturers, and smart-device vendors — adoption patterns indicate shifting from general-purpose GPUs towards domain-specific AI accelerators.

Pilot or Case Example: In 2025, a major cloud provider deployed a pilot cluster of dedicated AI-chips achieving downtime reduction of ~22 percent and accelerating model inference latency by ~40 percent.

Competitive Landscape: Market leader holds approximately 35-40 percent share; major competitors include NVIDIA, AMD, Intel, Google (TPU), and Huawei (Ascend).

Regulatory & ESG Impact: Governments in North America and Asia are introducing export-controls on advanced AI chips, tax incentives for domestic fabrication, and ESG mandates focusing on energy efficiency of AI accelerators.

Investment & Funding Patterns: Recent investments exceed USD 20 billion in AI-chip start-ups, large-scale fabrication projects, and venture funding focused on AI accelerator architectures.

Innovation & Future Outlook: Key innovations center on 2 nm node development, heterogeneous compute stacks combining CPUs, GPUs, and AI accelerators, and increasing integration of AI chips into autonomous systems, smart factories, and edge devices.

In the broader market context, the AI chips segment is experiencing significant shifts across industry sectors. Cloud computing, automotive, smart manufacturing, and edge-IoT together contribute the lion’s share of chip consumption, driven by rising compute-intensity and real-time analytics requirements. Recent product innovations such as custom AI accelerators with sparsity-support and low-power architectures are lowering inference costs and enabling new end-points. Regulatory drivers including national chip-strategies and energy-efficiency mandates are accelerating capital investment and localisation of fabrication. Regionally, Asia-Pacific is seeing rapid uptake of edge-AI chips in telecom, manufacturing, and consumer electronics, while North America continues to lead datacentre applications. Future trends point to expansion of AI-hardware as a service models, vertical-industry-specific accelerators, and scaling of training clusters into multi-exaflop capacity.

The strategic relevance of the AI Chips Market lies in its integral role in powering next-generation computing architectures that underpin digital transformation across industries. AI chips provide specialized computing capacity for training and inference tasks, enabling substantial efficiency improvements in data centers, edge systems, and consumer electronics. Advanced architectures such as 3 nm GPUs and tensor processing units (TPUs) deliver up to 45% performance improvement compared to 7 nm nodes, demonstrating the accelerating pace of innovation. North America dominates in volume, while Asia-Pacific leads in adoption, with nearly 62% of enterprises integrating AI accelerators into operations by 2025.

By 2027, edge-AI integration is expected to reduce latency and operational costs by nearly 40%, driving large-scale adoption across automotive, healthcare, and manufacturing sectors. Firms are committing to measurable ESG metrics, targeting an average 25% energy efficiency improvement in AI datacenter chips by 2030 through optimized architecture and recycling of semiconductor materials. In 2024, NVIDIA achieved a 35% reduction in energy consumption across its AI product lines through adaptive voltage scaling technology, reinforcing the industry's commitment to sustainable design.

The future pathway of the AI Chips Market is defined by continued innovation in neuromorphic and quantum-inspired processors, fostering secure, scalable, and low-power AI ecosystems. Positioned as a core pillar of resilience, compliance, and sustainable growth, the market will serve as the backbone for industries seeking high-performance, energy-efficient computing in a regulated, ESG-driven environment.

The growing adoption of automation across industries is significantly accelerating the demand for AI chips capable of handling complex algorithms and real-time processing. Manufacturing, automotive, and logistics sectors are integrating AI chips into robotics and predictive maintenance systems to improve throughput and operational accuracy. In 2024, approximately 68% of manufacturing enterprises incorporated AI-enabled automation, enhancing efficiency by nearly 32%. AI chips designed for parallel data processing enable faster decision-making in autonomous systems, leading to higher productivity levels and lower downtime. This continuous push toward intelligent automation, coupled with expanding 5G networks and smart infrastructure, ensures sustained momentum in the AI Chips Market.

The AI Chips Market faces constraints due to ongoing supply chain bottlenecks and high fabrication expenses associated with advanced semiconductor nodes. Producing AI chips at or below 5 nm requires precision manufacturing, cleanroom infrastructure, and high-cost EUV lithography systems, raising capital intensity for both established and emerging manufacturers. In 2023–2024, global chip supply volatility caused an estimated 20% delay in product delivery schedules across multiple regions. Additionally, export restrictions on high-performance chips and limited access to rare materials such as gallium and germanium have tightened market availability. These factors collectively slow innovation cycles and limit smaller firms from entering high-performance chip production.

Edge computing and neuromorphic architectures are opening significant growth avenues for the AI Chips Market by enabling low-latency data processing closer to the source. The proliferation of smart devices and industrial IoT systems has created an unprecedented need for energy-efficient, high-speed AI processors. By 2026, it is projected that over 55% of enterprise AI workloads will run on edge hardware, reducing network dependence and enhancing response times by up to 45%. Neuromorphic AI chips, designed to mimic the human brain’s structure, are demonstrating energy savings of nearly 30% in experimental trials. These technological frontiers present lucrative opportunities for AI chipmakers focusing on miniaturization, power optimization, and real-time decision systems.

The increasing complexity of data privacy regulations and lack of interoperability across AI hardware ecosystems pose substantial challenges to the AI Chips Market. Variations in compliance frameworks, such as GDPR in Europe and AI governance standards in North America, restrict cross-border data utilization for AI training. Hardware-software compatibility issues between different chip architectures hinder scalability and integration for global enterprises. In 2024, nearly 41% of enterprises cited data governance limitations as a key barrier to AI deployment. Furthermore, disparities in firmware standards across vendors complicate development cycles and increase overall system costs. Addressing these challenges will require unified hardware interfaces and compliance-ready chip architectures to sustain long-term market growth.

Expansion of Domain-Specific AI Accelerators: The market is witnessing rapid deployment of domain-optimized chips designed for specific workloads such as natural language processing, image recognition, and autonomous driving. In 2024, nearly 48% of all newly developed AI hardware incorporated domain-specific accelerators, resulting in an average performance gain of 42% compared to traditional GPU-based systems. These accelerators reduce power consumption by approximately 28% while maintaining higher throughput, making them a preferred choice for data-intensive industries like cloud computing and healthcare analytics.

Shift Toward Energy-Efficient Architectures: Growing emphasis on sustainability and ESG compliance has prompted chipmakers to design energy-optimized AI processors. Next-generation architectures using advanced packaging and AI-driven power management systems achieved a 37% reduction in energy consumption during inference tasks and 25% lower heat dissipation in 2024 compared to previous generations. Approximately 61% of datacenter operators globally have adopted energy-focused AI chips to reduce operational carbon footprints, aligning with enterprise-level net-zero commitments.

Integration of AI Chips in Edge Devices: Edge computing adoption is accelerating, with AI chips increasingly embedded in smart sensors, drones, and automotive control units. In 2025, an estimated 58% of industrial IoT devices are expected to integrate AI-enabled chips capable of on-device processing. This shift reduces data latency by nearly 40% and enhances system reliability for real-time applications in sectors such as manufacturing automation, logistics, and defense systems.

Advancements in 3D Chip Stacking and Packaging Technologies: Semiconductor manufacturers are investing in advanced 3D packaging to overcome interconnect bottlenecks and boost computational density. By 2025, over 46% of AI chip production is projected to adopt 3D stacking techniques, delivering up to 55% improvement in bandwidth efficiency and 30% space savings compared to traditional 2D layouts. These technological upgrades enhance scalability for hyperscale data centers and enable compact integration in next-generation mobile and embedded AI systems.

The AI Chips Market is segmented across three key dimensions — type, application, and end-user — reflecting the diversity of AI hardware integration across industries. Each segment demonstrates distinct adoption patterns shaped by computational requirements, energy efficiency demands, and specific AI workloads. By type, processors such as GPUs, ASICs, and FPGAs dominate production, collectively accounting for over 80% of global deployment. By application, data center and edge-AI workloads lead, driven by enterprise digitalization and autonomous technologies. By end-user, technology enterprises and automotive manufacturers are at the forefront of adoption, leveraging AI chips for real-time analytics, predictive modeling, and automation. The growing penetration of AI in healthcare, manufacturing, and telecom further underscores the strategic depth of market segmentation, with each category driving innovation through differentiated chip architectures and deployment models.

GPU-based AI chips currently account for approximately 46% of total adoption due to their superior parallel processing capabilities and versatility in machine learning and deep neural network applications. ASICs follow closely with around 28% share, gaining traction for their power efficiency and performance optimization in fixed AI workloads such as speech and image recognition. FPGAs represent 14% of adoption, primarily in custom inference tasks requiring rapid adaptability. However, neuromorphic processors are emerging as the fastest-growing type, projected to expand at a CAGR of 41%, fueled by their capability to simulate synaptic learning processes while using nearly 60% less energy than traditional architectures.

Other types, including quantum-inspired and hybrid AI chips, collectively represent about 12% of the market, serving specialized applications in research computing and data encryption.

Data center applications dominate the AI Chips Market, accounting for 49% of total usage, as hyperscale computing environments increasingly rely on AI accelerators for training and inference. Automotive AI applications, including advanced driver-assistance systems (ADAS) and autonomous navigation, contribute 24% of total adoption and are expanding rapidly as EV and mobility innovation accelerates. Edge-AI applications follow at 17%, supported by the growing integration of smart devices and industrial IoT platforms that demand localized data processing.

The fastest-growing application segment is healthcare AI, forecasted to expand at a CAGR of 43%, driven by diagnostic imaging, drug discovery, and predictive health analytics. Other sectors, including financial services, retail, and logistics, collectively account for 10% of AI chip utilization, often in fraud detection, inventory optimization, and robotic process automation.

Technology enterprises represent the leading end-user segment, holding about 44% of AI chip adoption, as cloud service providers and digital platform companies deploy high-performance AI accelerators for model training and real-time analytics. Automotive manufacturers hold 22%, integrating AI chips in vehicle control systems and driver-assistance algorithms, followed by healthcare organizations with 18% adoption. Industrial and telecom operators collectively represent the remaining 16%, leveraging AI chips for predictive maintenance, network optimization, and smart factory automation.

The fastest-growing end-user category is the industrial manufacturing sector, expected to expand at a CAGR of 40%, driven by smart robotics, automated inspection systems, and predictive control frameworks. By 2030, over 65% of large manufacturing firms are expected to adopt AI-integrated chipsets for process optimization and defect reduction.

North America accounted for the largest market share at 38% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 41% between 2025 and 2032.

In 2024 North America dominated with approximately 38% of global AI chips demand, supported by its large hyperscale data-centres and edge-AI deployments. Meanwhile Asia-Pacific recorded an estimated 31% share in the same year and is projected to accelerate due to increasing manufacturing of AI accelerators and large scale roll-out in China, India and Japan. In Asia-Pacific more than 45 % of new AI-chip fabrication capacity slated for commission by 2026 is scheduled, and China alone plans to ship over 10 million AI-specific processors in 2025. By contrast, Europe held around 18% of the market in 2024, South America about 7%, and Middle East & Africa roughly 6%. These regional splits reflect differing end-user adoption rates, production-base expansions, regulatory regimes and infrastructure investment timelines. For strategic planning this means decision-makers must consider not only current share but also acceleration potential and region-specific supply-chain dynamics.

How is the powerhouse region advancing specialised AI silicon deployments?

North America holds approximately 38% of global AI chips adoption, leveraging its strong ecosystem of cloud providers, semiconductor manufacturers, and enterprise AI deployments. Key industries driving demand include cloud & hyperscale data-centres, automotive (autonomous vehicles and ADAS), and healthcare analytics platforms. Government support is manifest through initiatives to subsidise semiconductor fabrication and tax credits for domestic AI hardware manufacturing. Additionally, North America leads in integration of multi-chip modules and silicon photonics for AI workloads. For example, local player NVIDIA continues to scale its AI-accelerator shipments and partners with U.S. foundries to expand production of sub-5 nm AI chips. Consumer behaviour in this region reflects higher enterprise adoption rates in healthcare and finance: over 60% of large U.S. banks have publicly committed to deploying AI-chip powered inference clusters. This strong enterprise base, combined with mature AI-hardware supply chains and regulatory frameworks, positions North America as a strategic hub for AI chip innovation and commercialisation.

How is the regulatory-focused region embedding AI accelerators into industrial transformation?

Europe holds about 18% of the global AI chips market in 2024. Major markets include Germany, the United Kingdom and France, where automotive OEMs, industrial robotics firms and telecom infrastructure providers are key end-users. Regulatory bodies such as the European Commission are advancing “explainable AI” mandates and energy-efficiency standards, thereby increasing demand for AI chips that support transparency and sustainability. European manufacturers are adopting emerging technologies like heterogeneous integration and automotive-grade AI accelerators for autonomous systems. A local player example is Infineon Technologies (Germany) which is developing automotive-qualified AI ASICs integrated into next-generation vehicle platforms. Consumer behaviour in Europe is influenced by strong regulatory environments: enterprises require chips with on-device AI processing and low-emission footprints, driving demand for specialised AI hardware in manufacturing and mobility sectors.

How is the high-volume region scaling AI chip fabrication and deployment at speed?

Asia-Pacific recorded roughly 31% of the global AI chips market by volume in 2024 and ranks as the largest manufacturing growth region. Top consuming countries include China, India and Japan, with China leading fabrication expansions and India rapidly increasing enterprise AI chip adoption. Infrastructure trends show major foundry investments, with new fabs scheduled in Taiwan, South Korea and China targeting AI-specific nodes. Regional innovation hubs are emerging in Shenzhen, Bengaluru and Tokyo, focusing on edge-AI and mobile-AI chips. Local player Cambricon Technologies (China) is scaling production of general-purpose AI processors and is moving toward shipping over 10 million units in 2025. Consumer behaviour here is heavily shaped by e-commerce and mobile-AI applications: in 2024, nearly 55% of smartphone shipments in the region included embedded AI-accelerator chips. This combination of high volume manufacturing, strong consumer demand and mobile/edge-AI proliferation makes Asia-Pacific the region with the fastest ramp-up trajectory for AI chips.

How is the emerging region linking AI chips to media, language and localisation functions?

In South America, key countries include Brazil and Argentina and the region captured around 7% of the global AI chips market in 2024. Infrastructure trends show increasing investment in media-streaming platforms and language-localisation AI systems, which drives demand for inference-optimised chips in content delivery networks. Government incentives in countries like Brazil are supporting AI innovation through trade policies and regional tech partnerships with manufacturing hubs in North America and Europe. A regional player example is CPQD (Brazil) which is working on AI-accelerator prototypes for Portuguese-language voice-recognition systems. Consumer behaviour in South America shows strong uptake of streaming services, interactive gaming and chat-bots in regional dialects, making AI chips for media and language applications especially relevant.

How is the resource-rich region adopting AI chips across energy, construction and modernisation?

In the Middle East & Africa, the market represents about 6% of global AI chip demand in 2024. Major growth countries include the United Arab Emirates and South Africa, where investments in oil & gas automation, smart city infrastructure and construction digitalisation drive AI chip deployment. Technological modernisation trends include AI-enabled embedded processors in remote assets, energy-efficiency monitoring and real-time analytics in large-scale facilities. Local regulations and trade partnerships, such as regional free zones and technology grants, support AI hardware adoption. An example is G42 (UAE) which is exploring AI-chip integration in smart city and infrastructure projects. Consumer behaviour in this region is inclined toward infrastructure-based AI use-cases—such as automated monitoring in plants, urban sensors and utilities—rather than purely consumer electronics.

United States: ~34% market share, driven by high production capacity, strong end-user demand and large-scale cloud-AI deployments.

China: ~21% market share, driven by strong manufacturing expansion, strategic state investment and rapid mobile/edge-AI adoption.

The global AI Chips market remains moderately consolidated, with the top five players—NVIDIA, AMD, Intel, Qualcomm, and Google—collectively accounting for nearly 64% of the overall market share in 2024. More than 75 active competitors operate globally, ranging from established semiconductor giants to emerging fabless startups specializing in neuromorphic, quantum, and edge AI processors. The market’s competitive intensity is driven by high R&D expenditure, estimated at over USD 40 billion annually across leading players, and continuous product innovation cycles averaging 12–18 months. Strategic initiatives in 2023–2024 included more than 25 notable partnerships and acquisitions, focusing on chip architecture advancements, software optimization, and data-center scalability. Key developments include the rise of AI-specific chipsets for automotive, robotics, and enterprise cloud applications, where NVIDIA’s H100, AMD’s MI300X, and Intel’s Gaudi 3 have redefined benchmark performance metrics. Competition is further amplified by aggressive foundry collaborations—especially with TSMC and Samsung Electronics—to ensure cutting-edge node availability below 5 nm. While the market exhibits consolidation at the top, regional ecosystems remain fragmented, particularly in Asia-Pacific and Europe, where national governments incentivize localized AI semiconductor production. The overall landscape demonstrates high entry barriers due to fabrication costs, IP ownership complexity, and ecosystem dependency, positioning established players with vertically integrated operations as long-term leaders.

Qualcomm Technologies, Inc.

Google LLC (Tensor Processing Unit Division)

Apple Inc.

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

IBM Corporation

Graphcore Ltd.

Micron Technology Inc.

Alibaba Group (Alibaba Cloud AI Chips Unit)

Tenstorrent Inc.

Cerebras Systems Inc.

Blaize Inc.

Marvell Technology Group Ltd.

Broadcom Inc.

Technological evolution in the AI Chips market is accelerating rapidly, with a strong shift toward advanced architectures such as 3 nm and 5 nm nodes that deliver up to 45% higher performance efficiency compared to 7 nm chips. In 2024, over 68% of AI chip production was based on nodes smaller than 7 nm, reflecting manufacturers’ focus on miniaturization, power optimization, and scalability. Hybrid chip designs integrating CPUs, GPUs, and NPUs are becoming standard across data center and edge computing applications, enabling up to 3.5× faster AI model processing and reducing latency by nearly 40%.

Neuromorphic and quantum AI processors are gaining traction, with neuromorphic chips mimicking human brain synapses to achieve 80% lower power consumption in autonomous systems and edge devices. Over 20 leading companies are experimenting with in-memory computing and photonic chips to overcome traditional bandwidth and heat limitations, particularly in training large language models. Meanwhile, the rise of chiplet-based architecture has allowed modular scalability, cutting production time by up to 25% while maintaining high yield efficiency.

In embedded systems, AI-on-silicon advancements are enabling real-time decision-making in robotics, automotive, and IoT devices. Edge AI chips, which accounted for nearly 38% of total shipments in 2024, are projected to dominate device integration over the next decade. Collectively, these technology shifts position the AI Chips market as a critical enabler of next-generation automation, sustainable data centers, and intelligent computing ecosystems across industries.

In March 2023, NVIDIA Corporation announced that the H100 Tensor Core GPU was being offered by major cloud providers such as Amazon Web Services, Microsoft Corporation and Meta Platforms for generative AI training and inference, with the AWS EC2 UltraClusters scaling up to 20,000 interconnected H100 chips.

In December 2023, Advanced Micro Devices, Inc. (AMD) released the Instinct MI300X accelerator series, featuring 192 GB HBMe3 memory capacity and 5.3 TB/s peak memory bandwidth, enabling enterprises to deploy large-language-models (LLMs) on a single accelerator.

In April 2024, Intel Corporation unveiled its Gaudi 3 AI accelerators and articulated a strategic shift toward open enterprise AI systems, claiming up to 50 % faster training time and 40 % better power efficiency compared to competitive high-end solutions.

In October 2024, a market report indicated that Intel had reduced its shipment target for the Gaudi 3 series by over 30 % for the following year, reflecting supply-chain and product ramp-up challenges within the AI chips segment.

This report covers the global AI chips market across multiple dimensions including product types, applications, end-users, regional markets, manufacturing technologies, and emerging innovation. In the type segment the analysis includes general-purpose GPUs, application-specific accelerators (ASICs), field-programmable gate arrays (FPGAs), neuromorphic processors and hybrid chip architectures. For applications the scope spans data centres, edge computing, automotive/autonomous systems, industrial IoT, healthcare diagnostics, consumer electronics and smart devices. The end-user breakdown includes cloud service providers, automotive OEMs, healthcare organisations, manufacturing and industrial automation firms, telecom operators and consumer device manufacturers. Region-wise the report addresses North America, Europe, Asia-Pacific, South America and Middle East & Africa, with detailed insight into manufacturing capacity, deployment trends, investment levels and regulatory influences per region. On the technology front the report evaluates process-node transitions (e.g., sub-5 nm fabrication), chip-let and 3D-stack packaging, heterogeneous integration (CPU+GPU+NPU), in-memory computing and photonic/neuromorphic architectures. Niche segments such as AI accelerator modules for robotics, on-device inference chips for mobile/IoT and domain-specific chips for verticals (automotive, retail, media) are also included. The objective is to provide decision-makers with a comprehensive market map of competitive dynamics, growth enablers, deployment bottlenecks, technological inflection points and investment opportunities across the full value chain of the AI chips market.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 30837.17 Million |

Market Revenue in 2032 | USD 447348.39 Million |

CAGR (2025 - 2032) | 39.7% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | NVIDIA Corporation, Advanced Micro Devices, Inc. (AMD), Intel Corporation, Qualcomm Technologies, Inc., Google LLC (Tensor Processing Unit Division), Apple Inc., Samsung Electronics Co., Ltd., Huawei Technologies Co., Ltd., IBM Corporation, Graphcore Ltd., Micron Technology Inc., Alibaba Group (Alibaba Cloud AI Chips Unit), Tenstorrent Inc., Cerebras Systems Inc., Blaize Inc., Marvell Technology Group Ltd., Broadcom Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |