Reports

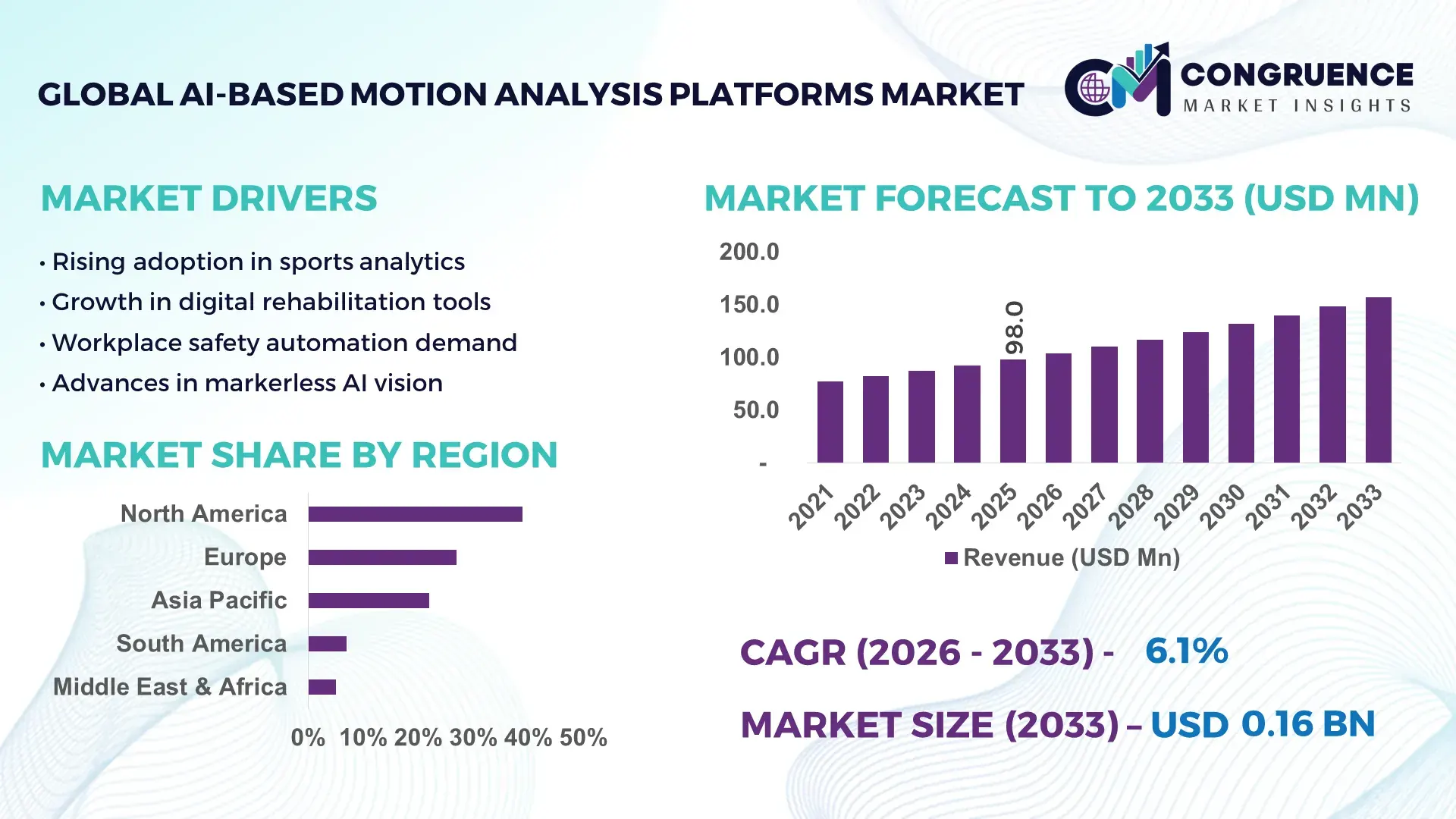

The Global AI-Based Motion Analysis Platforms Market was valued at USD 98 Million in 2025 and is anticipated to reach a value of USD 157.4 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is supported by rising adoption of AI-driven biomechanics, computer vision, and real-time analytics across healthcare, sports performance, industrial ergonomics, and defense training applications.

The United States dominates the AI-Based Motion Analysis Platforms Market, driven by strong production capacity, high enterprise adoption, and sustained investment in AI and computer vision technologies. In 2024, the U.S. accounted for over 38% of global AI software spending, with motion analytics platforms seeing accelerated uptake in sports science, rehabilitation, and occupational safety. More than 65% of Tier-1 sports franchises and Olympic training centers in the U.S. deploy AI-based motion analysis for performance optimization and injury prevention. The healthcare sector represents over 40% of domestic platform deployments, supported by more than USD 12 billion in annual digital health and AI investments. Additionally, U.S.-based firms lead advancements in markerless motion capture, edge-based inference, and FDA-cleared clinical motion analysis solutions, strengthening nationwide technological leadership.

Market Size & Growth: Valued at USD 98 Million in 2025, projected to reach USD 157.4 Million by 2033 at a CAGR of 6.1%, driven by expanding AI adoption in healthcare diagnostics and sports performance analytics.

Top Growth Drivers: Healthcare adoption (42%), sports and fitness analytics penetration (31%), industrial ergonomics and safety optimization (27%).

Short-Term Forecast: By 2028, AI-based motion platforms are expected to improve biomechanical assessment accuracy by 35% while reducing manual analysis time by 40%.

Emerging Technologies: Markerless motion capture, deep learning–based pose estimation, edge AI for real-time kinematic analysis.

Regional Leaders: North America (USD 62 Million by 2033) driven by clinical adoption; Europe (USD 44 Million) led by sports science integration; Asia-Pacific (USD 36 Million) supported by digital fitness and smart manufacturing use cases.

Consumer/End-User Trends: Rehabilitation centers, elite sports teams, and manufacturing firms increasingly adopt subscription-based AI motion platforms for continuous monitoring.

Pilot or Case Example: In 2024, a U.S. sports medicine network reduced athlete injury recurrence rates by 28% using AI-driven gait and motion analysis.

Competitive Landscape: Vicon (~18% share) leads the market, followed by Qualisys, Xsens, OptiTrack, and Noraxon.

Regulatory & ESG Impact: Growing compliance with clinical validation standards and ergonomic safety regulations is accelerating adoption.

Investment & Funding Patterns: Over USD 420 Million invested globally since 2022, with strong venture funding in digital health and sports AI platforms.

Innovation & Future Outlook: Integration with digital twins, wearable sensors, and cloud-based analytics is shaping next-generation motion intelligence platforms.

AI-Based Motion Analysis Platforms are increasingly deployed across healthcare (45%), sports and fitness (30%), and industrial ergonomics (15%), with defense and animation applications contributing the remainder. Recent innovations include real-time markerless tracking, AI-driven injury risk prediction, and integration with wearable IMUs. Regulatory support for digital health, rising workplace safety mandates, and strong North American and European consumption patterns continue to shape future growth, alongside expanding adoption in Asia-Pacific.

The AI-Based Motion Analysis Platforms Market holds strong strategic relevance as organizations prioritize data-driven decision-making in human performance, safety, and clinical outcomes. These platforms enable precise biomechanical insights that support cost optimization, productivity gains, and improved health outcomes across multiple industries. Deep learning–based markerless motion analysis delivers approximately 30% higher accuracy compared to traditional marker-based systems, reducing setup complexity and operational downtime.

Regionally, North America dominates in deployment volume, while Europe leads in structured adoption, with nearly 52% of professional sports and rehabilitation centers integrating AI motion analytics into standard workflows. By 2028, real-time edge AI processing is expected to reduce motion analysis latency by 45%, enabling instant feedback in surgical training, rehabilitation, and industrial safety environments.

From an ESG perspective, firms are committing to ergonomic risk reduction targets, including a 25% decrease in workplace musculoskeletal injuries by 2030 through AI-driven motion monitoring. In 2024, a U.S.-based manufacturing group achieved a 32% reduction in lost-time injuries by deploying AI motion analysis to redesign high-risk workflows.

Looking ahead, the AI-Based Motion Analysis Platforms Market is positioned as a critical pillar supporting operational resilience, regulatory compliance, and sustainable workforce and healthcare outcomes, reinforcing its role in long-term digital transformation strategies.

The AI-Based Motion Analysis Platforms Market is shaped by rapid advancements in computer vision, machine learning, and sensor fusion technologies. Increasing demand for objective, data-driven assessment of human movement is influencing adoption across healthcare, sports, manufacturing, and defense sectors. Integration with cloud platforms and wearable devices is improving scalability and accessibility, while enterprise demand for real-time analytics is driving innovation in edge computing. Regulatory recognition of digital diagnostics and ergonomic monitoring further supports market momentum, although data privacy and system interoperability remain influential factors.

Organizations increasingly rely on AI-based motion analysis to replace subjective visual assessments with quantifiable metrics. In healthcare, over 60% of rehabilitation clinics adopting AI motion platforms report improved treatment personalization and faster patient recovery timelines. Sports organizations use motion analytics to enhance performance efficiency by up to 25%, while industrial users apply these systems to reduce repetitive strain injuries. The demand for standardized, repeatable motion insights continues to accelerate platform deployment across professional environments.

Despite technological progress, implementation complexity remains a challenge. Integration with legacy IT systems, calibration requirements, and the need for skilled operators limit adoption, particularly among small and mid-sized organizations. Approximately 35% of potential users cite upfront system configuration and training requirements as barriers. Data privacy concerns, especially in healthcare and workplace monitoring, further slow decision-making, requiring robust compliance frameworks and secure data architectures.

The growth of tele-rehabilitation and remote patient monitoring creates substantial opportunities for AI-based motion platforms. Home-based motion tracking solutions enable continuous assessment, reducing in-clinic visits by up to 40%. Aging populations and chronic musculoskeletal conditions are expanding demand for scalable, AI-driven rehabilitation tools. Integration with consumer wearables and mobile applications further broadens addressable use cases across preventive care and wellness programs.

The lack of standardized motion data formats and interoperability between platforms complicates large-scale deployment. Enterprises operating across regions face difficulties integrating motion analytics with electronic health records, training systems, or industrial IoT platforms. Over 30% of enterprise users report challenges in cross-platform data comparison, increasing customization costs and deployment timelines, and highlighting the need for industry-wide data standards.

Accelerated Adoption of Markerless Motion Capture: Markerless AI systems now account for over 48% of new deployments, reducing setup time by 50% and improving user comfort. Healthcare and sports users report up to 20% higher session throughput due to simplified capture processes.

Integration with Wearables and IoT Sensors: More than 60% of new platforms integrate wearable IMUs and smart sensors, enabling hybrid motion datasets. This integration improves movement classification accuracy by approximately 28% and supports continuous monitoring use cases.

Expansion into Workplace Ergonomics and Safety: Industrial adoption increased by 34% between 2022 and 2024, with enterprises using AI motion analysis to cut ergonomic injury rates by up to 30% and improve compliance with safety standards.

Growth of Cloud-Based Analytics and Digital Twins: Cloud-enabled motion platforms support multi-site deployments, with 45% of enterprises leveraging digital twins to simulate human movement scenarios, improving training efficiency by 22% and reducing operational risk.

The AI-Based Motion Analysis Platforms Market is structured around three primary dimensions—type, application, and end-user—reflecting how motion intelligence is created, deployed, and consumed across industries. On the supply side, segmentation by type differentiates systems based on sensing modality, AI architecture, and data fusion approach, ranging from vision-only platforms to hybrid wearable–camera solutions. By application, the market spans clinical biomechanics, sports performance, workplace ergonomics, animation and media, and defense training, each requiring distinct accuracy levels, real-time processing needs, and regulatory compliance. End-user segmentation highlights how hospitals, elite sports organizations, manufacturing firms, research institutions, and fitness enterprises adopt these platforms at varying intensities based on workflow maturity and digital readiness. Adoption patterns are increasingly shaped by integration capability with wearables, electronic records, and industrial IoT systems, as well as by data governance requirements that differ across regions and sectors.

Vision-based (markerless) motion models currently represent the leading product type, accounting for roughly 42% of total platform adoption because they eliminate physical markers, reduce setup time by nearly half, and enable scalable deployment in clinics, factories, and sports facilities. Their dominance is reinforced by advances in real-time pose estimation and edge inference, which allow high-precision capture using standard RGB or depth cameras rather than specialized labs. The fastest-growing type is video-based temporal motion analytics, expanding at approximately 14% annually, driven by demand for continuous movement tracking, longitudinal injury monitoring, and automated video review in professional sports and rehabilitation. Multi-frame learning architectures are improving motion prediction accuracy and reducing false positives in complex environments such as crowded factory floors or outdoor training fields. Sensor-fusion systems (IMU wearables combined with cameras) hold about 25% adoption, favored in industrial safety and remote rehabilitation where line-of-sight capture is unreliable. Depth-camera platforms serve niche but critical roles in gait labs and robotics training, while optical marker-based legacy systems remain relevant in high-precision biomechanics research. Together, these remaining categories contribute roughly 33% of the market, primarily in specialized laboratories and regulated clinical settings.

Clinical biomechanics is the leading application area at about 40% share, as hospitals and rehabilitation centers rely on AI motion platforms to standardize gait assessment, post-surgical recovery tracking, and neurological movement analysis. The segment benefits from rising demand for objective, repeatable metrics and tighter clinical documentation standards. The fastest-rising application is workplace ergonomics and safety, growing around 13% annually, propelled by stricter occupational safety mandates, rising compensation costs for musculoskeletal injuries, and the integration of motion analytics with factory digital twins. Large manufacturers increasingly use AI systems to redesign workflows and predict high-risk movements before injuries occur. Sports performance and coaching account for roughly 22%, driven by adoption among professional leagues, academies, and national training centers. Media and animation represent about 8%, while defense and tactical training contribute approximately 10%, with the remaining 20% spread across education, robotics, and smart fitness. Consumer and enterprise adoption trends are accelerating: in 2025, over 36% of global enterprises reported piloting AI motion systems for worker safety or training, and 58% of Gen Z fitness users indicated greater trust in gyms using AI-powered movement feedback. Additionally, 41% of U.S. hospitals were testing AI platforms that combine gait video with patient records for remote rehabilitation.

Hospitals and rehabilitation networks are the leading end-user segment with about 38% share, reflecting their need for standardized, data-driven movement assessment and growing reimbursement support for digital therapeutics. Integration with electronic health records and tele-rehab platforms has made motion analytics a core clinical workflow rather than an experimental tool. The fastest-growing end-user group is industrial manufacturers, expanding at roughly 15% annually as firms adopt AI motion monitoring to cut injury rates, meet compliance requirements, and optimize assembly-line ergonomics. Smart factories increasingly pair motion analytics with digital twins and robotics, amplifying efficiency gains. Elite sports organizations and academies represent around 24%, while universities and research labs contribute 12%, primarily for biomechanics and human–robot interaction studies. Fitness and wellness providers account for 10%, and defense or public-sector training bodies make up the remaining 16%. Adoption rates are highest in manufacturing (about 46% of large firms), followed by hospitals (42%) and professional sports organizations (67% among top-tier teams). In 2025, more than 37% of enterprises globally reported piloting AI motion platforms for safety and productivity use cases, and 60% of Gen Z consumers expressed stronger brand trust toward gyms and clinics using transparent AI movement coaching tools.

North America accounted for the largest market share at 39% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.8% between 2026 and 2033.

North America’s leadership is anchored in deep clinical digitization, high R&D intensity, and widespread deployment of AI-driven biomechanics across hospitals, sports institutes, and smart factories. Europe followed with approximately 27% share in 2025, supported by stringent workplace safety rules, explainable-AI requirements, and strong adoption in Germany, the UK, and France. Asia-Pacific held around 22% share, driven by rapid manufacturing automation, booming digital fitness platforms, and government-backed AI initiatives in China, Japan, South Korea, and India. South America contributed roughly 7%, with demand concentrated in Brazil and Argentina around media, sports analytics, and industrial ergonomics. The Middle East & Africa represented about 5%, gaining traction through smart-city projects, construction safety programs, and oil-and-gas workforce optimization. Across all regions, rising integration with wearables, digital twins, and cloud analytics is reshaping deployment patterns and investment priorities.

North America commands roughly 39% of global market volume, reflecting high enterprise maturity, strong venture funding, and dense clinical infrastructure. Hospitals and rehabilitation networks are the primary demand drivers, with large systems integrating AI motion analytics into tele-rehab, post-surgical monitoring, and neurological gait assessment. Professional sports leagues and collegiate athletics programs represent another major pillar, using real-time biomechanical analytics to reduce injury recurrence and optimize performance. Regulatory tailwinds—such as expanded reimbursement pathways for digital therapeutics and workplace safety mandates from federal agencies—have accelerated deployment in both healthcare and manufacturing. Technologically, the region leads in markerless capture, edge AI inference, and cloud-based motion platforms that integrate with electronic health records and industrial IoT dashboards. A notable local player, Vicon, is expanding hybrid camera–wearable systems for hospitals and elite sports centers, while several U.S. startups are commercializing AI gait assessment approved for clinical workflows. From a consumer behavior standpoint, North American users show higher enterprise adoption in healthcare and finance-related occupational ergonomics, prioritizing accuracy, compliance, and data interoperability over cost.

Europe accounts for approximately 27% of market volume, with Germany, the UK, and France forming the core demand centers. Automotive, advanced manufacturing, and public healthcare systems are the dominant adopters, using AI motion analytics to reduce workplace injuries, improve rehabilitation outcomes, and support human–robot collaboration. The European Union’s AI Act framework and strict data-protection rules (GDPR) are pushing vendors toward explainable, auditable motion models with transparent decision logic. Sustainability initiatives under the Green Deal are also encouraging firms to deploy AI ergonomics tools that lower workplace injury rates and cut compensation costs. Adoption of emerging technologies is strong in Germany’s Industry 4.0 ecosystem, where digital twins are paired with motion analytics for assembly-line optimization. In the UK, NHS pilots are integrating AI gait analysis into community rehabilitation programs. French biomechanics firms are advancing high-precision depth-sensing platforms for clinical and sports use. A leading regional player, Qualisys (Nordics), is expanding cloud-enabled motion labs for hospitals and universities. Consumer behavior shows that European buyers prioritize explainable, compliant, and privacy-first AI motion systems, even if deployment timelines are longer.

Asia-Pacific is the second-largest and fastest-expanding region by volume, driven by massive manufacturing bases in China, Japan, and South Korea and a rapidly digitizing healthcare sector in India. China leads adoption in smart factories and robotics training, integrating AI motion analytics with industrial vision systems and digital twins. Japan emphasizes eldercare rehabilitation and workplace safety in automotive and electronics plants. India is emerging as a hub for AI-based tele-rehabilitation and sports analytics startups. Infrastructure investments in 5G, cloud computing, and smart-city projects are enabling real-time motion analytics across logistics, construction, and public safety. Innovation clusters in Shenzhen, Tokyo, Seoul, and Bengaluru are accelerating development of markerless capture and low-cost wearable–camera hybrids. Local players such as Hikvision and SenseTime spin-offs are embedding pose estimation into industrial monitoring platforms, while Japanese med-tech firms are commercializing AI gait analysis for aging populations. Regionally, consumer adoption is propelled by mobile AI fitness apps, e-commerce logistics automation, and video-based coaching tools, creating broad-based market pull.

South America represents about 7% of global market volume, led by Brazil and Argentina. Demand is concentrated in media production, sports analytics, and industrial ergonomics, with growing use in soccer performance analysis and workplace safety monitoring in manufacturing and mining. Brazil’s expanding smart-manufacturing initiatives and renewable-energy projects are creating new use cases for AI motion analytics in wind and solar maintenance workflows. Argentina is seeing increased adoption in animation studios, broadcasting, and rehabilitation clinics in major urban centers. Government incentives for digital transformation and industrial modernization are gradually improving infrastructure, while trade partnerships with North American and European technology providers are accelerating access to advanced platforms. Cloud connectivity in metropolitan areas is enabling remote motion assessment for rural healthcare. A notable local trend is Brazilian startups integrating motion analytics into sports academies and physical therapy chains. Consumer behavior shows that South American demand is closely tied to media production, language localization, and video-based sports analytics, rather than purely clinical use.

The Middle East & Africa region holds roughly 5% of global market volume, with demand centered on construction safety, oil-and-gas workforce monitoring, and smart-city initiatives in the UAE, Saudi Arabia, and South Africa. Large infrastructure projects are increasingly using AI motion analytics to reduce accidents, monitor worker fatigue, and improve site productivity. Technological modernization is advancing through 5G rollouts, cloud adoption, and digital twins in urban planning. National AI strategies in the UAE and Saudi Arabia are encouraging pilot projects in healthcare rehabilitation and sports science. South Africa is seeing growing use in mining safety and industrial ergonomics. Local regulations on workplace safety and international trade partnerships are facilitating technology transfer from North American and European vendors. Government-backed innovation hubs in Dubai and Riyadh are testing AI motion systems for smart transportation and public safety. A regional example includes UAE construction firms piloting AI motion monitoring on mega-projects to cut onsite injuries and rework costs. Consumer behavior varies, but enterprise buyers prioritize risk reduction, compliance, and productivity gains, while fitness adoption remains emerging.

United States – 34% Market Share: Strong clinical digitization, elite sports adoption, and deep AI R&D ecosystem.

China – 18% Market Share: Large-scale smart manufacturing, robotics integration, and government-backed AI industrialization.

The AI-Based Motion Analysis Platforms Market features a moderately consolidated competitive environment with a blend of long-established motion capture legacy providers and emerging AI-centric innovators. Across the landscape, there are 20+ active competitors offering varied solutions—from high-precision optical systems to smartphone-based and cloud-native platforms—targeting healthcare, sports science, entertainment, industrial ergonomics, and research. Leading incumbents such as Vicon Motion Systems Ltd., OptiTrack, Xsens Technologies B.V., Motion Analysis Corporation, and Qualisys AB collectively hold an estimated ~42–48% combined share of the core market, reflecting concentration among top performers.

These market leaders engage in strategic initiatives, including technology partnerships, platform enhancements, modular AI integrations, cloud analytics rollouts, and expanded global distribution agreements, to expand capabilities and address cross-industry demands. For example, partnerships targeting real-time data pipelines in animation and performance capture are gaining traction, and several vendors are integrating AI-driven markerless motion analysis into their core offerings to reduce dependency on traditional hardware rigs.

Innovation trends influencing competition include markerless and hybrid capture solutions with deep learning pose estimation, cross-platform cloud analytics, edge AI processing for real-time feedback, and mobile sensor convergence. Emerging players and startups are carving niche positions with lightweight SDKs and cloud-centric services that emphasize usability and rapid integration. The competitive landscape thus blends heritage hardware prowess with software-first AI motion intelligence, offering decision-makers a broad spectrum of choices aligned with performance, scalability, and deployment preferences.

Qualisys AB

Motion Analysis Corporation

Perception Neuron (Noitom Ltd.)

DeepMotion

Move.ai

iPi Soft LLC

Simi Reality Motion Systems GmbH

Noraxon USA Inc.

PhaseSpace Inc.

Kinovea

Phaser Motion Capture

Cubemos GmbH

Rokoko Electronics ApS

Within the AI-Based Motion Analysis Platforms Market, current and emerging technologies are redefining how motion data is captured, processed, and applied across industries. AI-enhanced markerless motion capture is a dominant trend, using deep neural networks to infer skeletal poses directly from video streams without the need for traditional markers, reducing setup complexity and increasing scalability. These systems support real-time analysis and are increasingly embedded within cloud-native frameworks, enabling distributed access and collaborative analytics.

Sensor fusion—blending data from RGB/depth cameras, wearable IMUs, and other sensors—is boosting robustness in environments where single-source capture is challenged. Such hybrid approaches yield richer motion datasets for clinical gait analysis, sports performance monitoring, and workplace ergonomic assessment. Edge computing hardware is also gaining adoption, allowing high-fidelity inference near the point of capture with minimal latency—a critical capability for real-time feedback loops in industrial and healthcare settings.

Cloud platforms and digital twin technologies are further enhancing decision-support capabilities by synchronizing motion data streams with virtual replicas of physical entities, allowing stakeholders to simulate, visualize, and optimize human movement pathways. Integration with mobile devices and smartphone-based solutions is lowering the barrier to entry, enabling clinicians and end-users to perform gait and mobility analysis without specialized hardware.

Advanced algorithms, including deep learning pose estimators and AI-driven anomaly detection, are improving the reliability of motion insights, detecting subtle biomechanical deviations and enabling predictive analytics for injury prevention. These technology streams are complemented by open-source frameworks such as Google’s MediaPipe, which provide extensible architectures for pose estimation and real-time computer vision processing that accelerate innovation across vendors.

Collectively, these technologies not only increase the precision and versatility of motion analysis platforms but also expand their applicability across sectors—from clinical diagnostics and rehabilitation to sports science, human-machine interaction, and digital content creation.

• In March 2025, Vicon Motion Systems Ltd. launched markerless motion capture solutions at the Game Developers Conference (GDC), bringing advanced real-time 3D tracking capabilities to developers and creators, enhancing workflows for virtual production and interactive experiences. Source: www.vicon.com

• In May 2025, Vicon introduced “Active Crown” hardware, designed to deliver faster, high-quality and precise camera tracking for virtual production professionals, improving spatial accuracy in complex studio environments. Source: www.vicon.com

• In December 2024, Vicon announced deployment of its motion capture technology by Boys Town National Research Hospital to support advanced studies on childhood speech and motor development, expanding clinical research applications. Source: www.vicon.com

• In March 2024, DeepMotion launched SayMotion™ open beta, a new AI-powered platform that enables creators to generate detailed 3D animations via text prompts, broadening access to motion capture capabilities across creative industries. Source: www.deepmotion.com

The AI-Based Motion Analysis Platforms Market Report provides a comprehensive perspective on how platforms that interpret human motion with AI are structured, adopted, and evolving across industries. It covers core technology types such as markerless computer vision systems, sensor-fusion solutions combining IMUs and cameras, and smartphone-based AI motion analytics enabling clinical or consumer deployment without specialized hardware. The report analyzes use cases spanning healthcare (gait analysis, rehabilitation monitoring), sports performance and biomechanics, workplace ergonomics, gaming and entertainment motion capture, and industrial human-robot collaboration.

Geographically, the report evaluates regional dynamics in North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting variation in adoption intensity, regulatory influences, and infrastructure readiness that shape investment and deployment strategies. Application segmentation goes deeper into how institutions and enterprises leverage motion analysis—from clinical decision support to media content creation and safety compliance. End-user insights detail how providers in hospitals, sports teams, manufacturing firms, research labs, and digital fitness sectors configure and integrate these technologies into workflows.

Emerging and niche areas—such as AI-enabled digital twin integration, cloud-native analytics suites, mobile motion intelligence platforms, and open-source AI frameworks—are examined for their potential to unlock new market segments and drive future innovation. The report systematically juxtaposes technological enablers with industry requirements, offering decision-makers a granular understanding of what capabilities and trends are influencing investments, competitive positioning, and strategic planning in the global AI-based motion analysis ecosystem. It is tailored to executives, product strategists, and technology leaders seeking actionable insights and market intelligence for informed decision-making.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 98.0 Million |

| Market Revenue (2033) | USD 157.4 Million |

| CAGR (2026–2033) | 6.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Vicon Motion Systems Ltd.; Xsens Technologies B.V.; OptiTrack (NaturalPoint, Inc.); Qualisys AB; Motion Analysis Corporation; Perception Neuron (Noitom Ltd.); DeepMotion; Move.ai; iPi Soft LLC; Simi Reality Motion Systems GmbH; Noraxon USA Inc.;PhaseSpace Inc.; Kinovea; Phaser Motion Capture; Cubemos GmbH; Rokoko Electronics ApS |

| Customization & Pricing | Available on Request (10% Customization Free) |