Reports

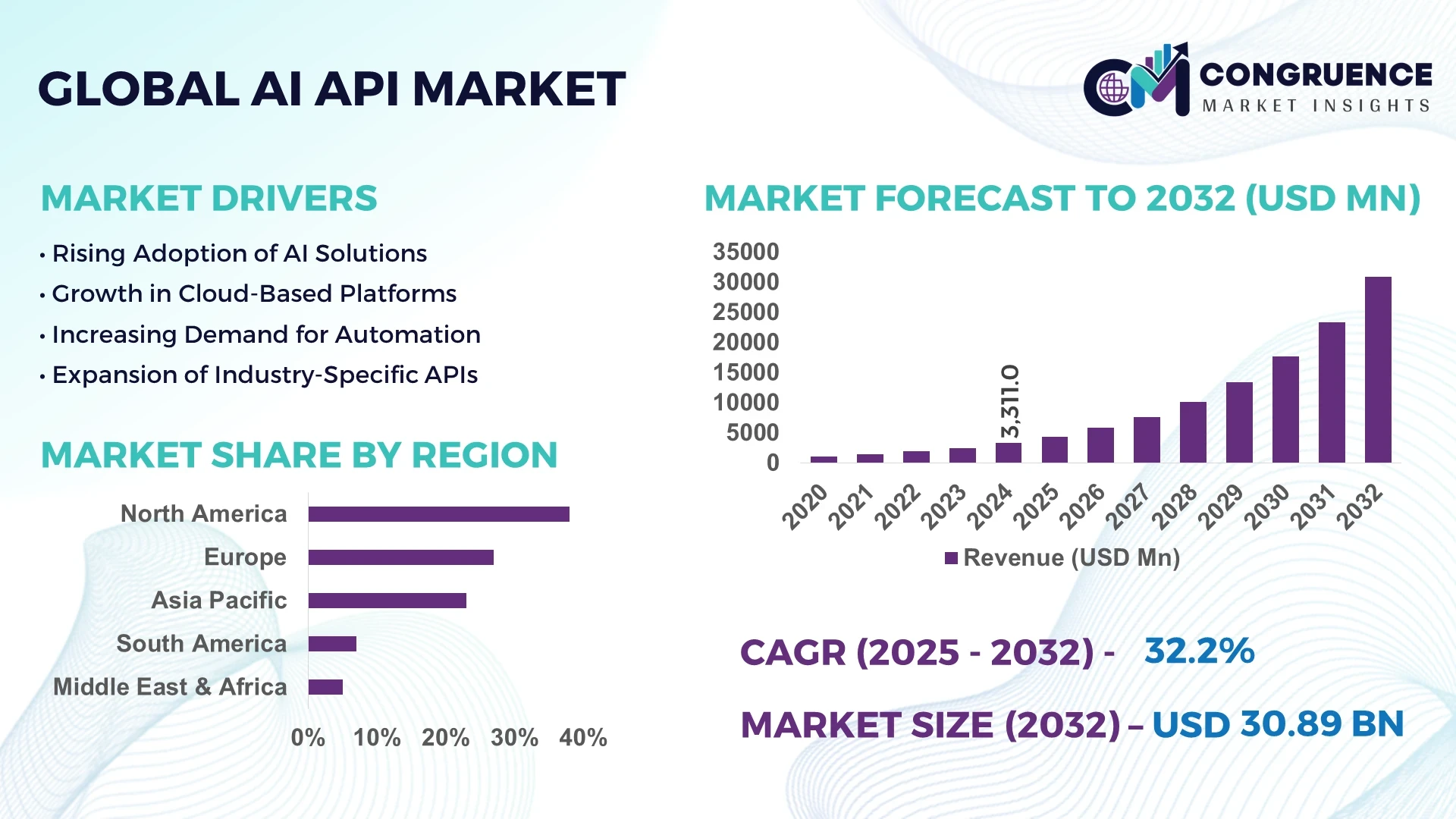

The Global AI API Market was valued at USD 3,311.0 Million in 2024 and is anticipated to reach a value of USD 30,889.5 Million by 2032 expanding at a CAGR of 32.2% between 2025 and 2032. This growth is driven by the rising integration of AI capabilities across diverse enterprise applications.

The United States plays a pivotal role in shaping the global AI API Market, underpinned by large-scale investments from both private and public entities. In 2024, U.S. AI-related R&D investment exceeded USD 32.0 billion, with over 58% of enterprises actively deploying AI APIs in cloud-based platforms. The country leads in developing generative AI, natural language processing, and computer vision APIs, which are widely integrated into sectors such as healthcare diagnostics, fintech risk assessment, and autonomous mobility solutions. With over 1,200 AI-focused startups and more than 70% of Fortune 500 companies embedding AI APIs into their digital ecosystems, the U.S. stands out as a technological powerhouse advancing innovation at scale.

Market Size & Growth: Valued at USD 3,311.0 Million in 2024, projected to reach USD 30,889.5 Million by 2032, expanding at a CAGR of 32.2%. Growth is fueled by accelerated enterprise adoption of AI-driven applications.

Top Growth Drivers: 65% adoption in cloud platforms, 48% operational efficiency improvement, and 52% demand surge in customer experience applications.

Short-Term Forecast: By 2028, AI API integration is expected to reduce enterprise IT costs by 37% while enhancing data processing speeds by 42%.

Emerging Technologies: Rapid adoption of generative AI APIs and edge AI integration, coupled with automated MLOps toolkits.

Regional Leaders: North America projected to reach USD 13.2 Billion by 2032, Europe to USD 8.4 Billion with strong adoption in finance, Asia-Pacific to USD 7.9 Billion driven by cloud-native startups.

Consumer/End-User Trends: Enterprises in healthcare, retail, and finance are witnessing adoption rates above 50%, with growing deployment in real-time analytics and customer engagement.

Pilot or Case Example: In 2024, a U.S. healthcare pilot reduced diagnostic error rates by 29% using AI API integration in imaging workflows.

Competitive Landscape: Microsoft holds an estimated 22% share, followed by Amazon Web Services, Google Cloud, IBM, and OpenAI.

Regulatory & ESG Impact: The EU’s AI Act mandates compliance with ethical AI guidelines, while 40% of firms are targeting explainable AI integration by 2027.

Investment & Funding Patterns: Recent AI API-related funding exceeded USD 15.5 Billion globally, with venture capital accounting for over 60% of flows.

Innovation & Future Outlook: AI APIs are moving toward industry-specific customization, seamless integration with IoT devices, and regulatory-compliant deployment models.

AI APIs are reshaping critical industry verticals, including healthcare (32% adoption), financial services (27%), and retail (21%), with innovations such as multimodal AI APIs, regulatory-compliant automation frameworks, and ESG-driven deployment practices positioning the market for sustainable, long-term growth across global regions.

The strategic relevance of the AI API Market lies in its ability to unlock scalable intelligence across industries by offering modular, cost-efficient, and high-performance solutions. Organizations are leveraging APIs as the core enablers of digital transformation, supported by measurable gains in efficiency and compliance. For instance, generative AI APIs deliver a 41% improvement in real-time data processing compared to legacy machine learning frameworks.

Regional dynamics further highlight these pathways. North America dominates in volume, driven by enterprise-scale deployments, while Europe leads in adoption with over 62% of enterprises actively integrating AI APIs into regulatory-compliant use cases. By 2027, edge AI APIs are expected to reduce latency in manufacturing automation by 36%, improving throughput across connected devices and industrial robotics.

Sustainability is also emerging as a core driver. Firms are committing to ESG targets, such as achieving a 25% reduction in computational carbon footprints by 2030 through optimized AI API architectures. In 2023, Japan’s healthcare sector achieved a 31% improvement in patient throughput by deploying AI diagnostic APIs, demonstrating tangible benefits of API-driven healthcare innovation.

Looking ahead, the AI API Market is set to be a cornerstone of global resilience, ensuring enterprises remain agile, compliant, and competitive while aligning with sustainability imperatives. This convergence of innovation, ESG accountability, and scalability positions AI APIs as a central pathway toward future-proof digital ecosystems.

The AI API Market is evolving rapidly as enterprises shift toward embedded intelligence across operational and customer-facing systems. Advances in natural language processing, computer vision, and predictive analytics are influencing adoption patterns, particularly in industries where automation, compliance, and real-time decision-making are critical. A surge in cross-industry collaboration is fueling innovation, with API ecosystems increasingly supporting interoperability between cloud, edge, and on-premises platforms. Simultaneously, regulatory frameworks are steering vendors toward ethical AI integration, while consumer demand for personalized, secure, and transparent AI-driven services accelerates market maturity.

The integration of AI APIs into cloud-native environments is significantly boosting enterprise agility and scalability. Over 65% of global enterprises now deploy AI APIs through cloud platforms to achieve seamless integration with existing IT infrastructures. This adoption trend reduces deployment timelines by 45% and enhances data management efficiency by 38%. AI APIs are also enabling enterprises to scale applications across geographies with reduced infrastructure costs, thus catalyzing digital transformation initiatives.

Data privacy remains a critical restraint as AI APIs process sensitive information across industries such as healthcare, finance, and retail. In 2024, nearly 43% of enterprises cited regulatory compliance and cybersecurity vulnerabilities as major barriers to full-scale adoption. Complexities around GDPR and cross-border data transfer add further challenges, as enterprises face the need for encryption, anonymization, and strict governance, slowing adoption momentum despite technological readiness.

The growing demand for industry-tailored APIs presents significant opportunities for market expansion. Customized AI APIs for healthcare diagnostics, fintech fraud detection, and smart retail analytics are enabling enterprises to unlock domain-specific efficiency. For example, healthcare AI APIs enhance diagnostic accuracy by 28%, while retail APIs improve customer engagement conversion rates by 35%. This trend underscores the potential of vertical-specific innovation to fuel next-phase growth in the AI API ecosystem.

Despite rapid advancements, the high infrastructure cost of integrating and maintaining AI APIs poses a challenge for enterprises, especially SMEs. Establishing scalable cloud, edge, and hybrid ecosystems requires significant capital, with infrastructure expenses consuming up to 18% of IT budgets in some industries. Additionally, training and workforce upskilling costs further limit adoption, creating barriers for widespread deployment across emerging economies.

Surge in Generative AI API Integration: In 2024, over 47% of enterprises adopted generative AI APIs for natural language, content creation, and design automation. Adoption has resulted in 34% efficiency gains in customer interaction workflows and 29% reduction in manual knowledge management processes.

Expansion of Edge AI API Deployments: Edge computing APIs witnessed 42% growth in deployment, enabling faster decision-making with 37% latency reduction in IoT-driven applications. Manufacturing plants adopting edge APIs achieved a 31% productivity gain in connected device operations by the end of 2024.

Rising Demand for Multimodal AI APIs: More than 38% of enterprises adopted multimodal APIs integrating text, image, and speech recognition. These deployments enhanced cross-channel analytics accuracy by 41% and improved customer service resolution time by 27%, particularly in retail and telecommunications.

Increasing Focus on Ethical and Explainable AI APIs: In 2024, 44% of firms integrated explainability features into APIs, ensuring compliance with transparency regulations. Explainable APIs improved model auditing speed by 33% and enhanced regulatory reporting accuracy by 25%, aligning with ESG-driven enterprise governance requirements.

The AI API Market is segmented across types, applications, and end-user groups, each contributing distinct value to the evolving landscape. By type, innovation is shaping categories such as vision-language, audio-text, and video-language APIs, enabling enterprises to unlock multimodal intelligence. Applications span customer engagement, healthcare, financial services, and enterprise automation, each leveraging AI-driven capabilities for enhanced accuracy and operational efficiency. End-user insights reveal strong adoption among technology-driven sectors such as healthcare, BFSI, and retail, with SMEs increasingly investing in AI-enabled APIs for scalable growth. The segmentation reflects a balanced interplay between established adopters and emerging demand clusters, showcasing a clear pathway for accelerated, sector-specific innovation.

Vision-language models currently account for 42% of adoption due to their widespread utility in search, recommendation engines, and document intelligence platforms. Their dominance is driven by enterprises embedding these models to enhance accuracy in image-to-text and cross-modal analytics. Audio-text systems follow with 25% of adoption, particularly useful in call centers and voice assistants, where speech recognition accuracy exceeds 90% in enterprise-grade deployments. Video-language models are witnessing the fastest growth, expected to surpass 30% adoption by 2032, fueled by rising demand in e-learning, media, and surveillance analytics. These models are increasingly used to automate captioning, summarize long-format video, and enhance accessibility features. Remaining types, including specialized APIs for robotics, biomedical imaging, and multimodal translation, together hold approximately 33% combined share, serving niche but critical use cases.

Customer experience platforms dominate the AI API application landscape, accounting for 39% adoption, as businesses increasingly deploy chatbots, virtual assistants, and recommendation engines to enhance real-time engagement. Healthcare applications follow closely with 28%, supported by strong integration of diagnostic imaging APIs and patient data management solutions. However, financial services applications represent the fastest-growing segment, projected to expand at a CAGR exceeding 34%, as AI APIs enable fraud detection, credit risk modeling, and algorithmic trading enhancements. Other applications, including logistics, manufacturing, and education, together account for around 33% of market adoption, largely driven by automation and data intelligence requirements. In 2024, more than 38% of enterprises globally reported piloting AI API-enabled platforms for customer experience enhancement. Additionally, 42% of hospitals in the U.S. are testing multimodal APIs that integrate radiology scans with patient records for improved diagnosis.

The healthcare sector leads the AI API Market with 35% adoption, leveraging APIs for advanced diagnostics, predictive patient analytics, and medical imaging solutions. BFSI follows at 29%, adopting APIs for secure transaction monitoring, risk modeling, and customer personalization. Retail is the fastest-growing end-user segment, projected to expand at a CAGR exceeding 36%, driven by e-commerce platforms integrating AI APIs for inventory management, personalized shopping experiences, and real-time customer support. Other key end-users such as education, logistics, and manufacturing contribute a combined 36% share, demonstrating a diverse adoption landscape across industries. In 2024, more than 41% of global retailers piloted multimodal AI chatbots for enhanced customer service, while 60% of Gen Z consumers reported greater trust in brands that utilized AI-driven conversational platforms.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 34.1% between 2025 and 2032.

Europe followed with a 27% share, supported by strong regulatory frameworks and adoption in finance and healthcare. South America captured 7% of the global landscape, with Brazil leading deployments across fintech and retail. Meanwhile, the Middle East & Africa represented 5% of total demand, with the UAE and South Africa at the forefront of regional adoption. By 2032, North America is projected to exceed USD 13.2 billion, Europe USD 8.4 billion, and Asia-Pacific USD 7.9 billion, underscoring diverse regional adoption trajectories and investment priorities.

North America commanded 38% of the market share in 2024, driven by advanced deployment across healthcare, BFSI, and retail sectors. The region benefits from supportive regulatory frameworks, including AI governance guidelines emphasizing responsible innovation. Rapid digital transformation initiatives have enabled more than 65% of large enterprises to integrate AI APIs into cloud platforms, with healthcare leading through diagnostic imaging APIs and financial services leveraging risk management APIs. Microsoft and Amazon Web Services are active local players, continuously expanding AI API portfolios for enterprises. Consumer behavior highlights higher adoption in healthcare and finance, with over 58% of enterprises in these sectors deploying API-driven automation to optimize outcomes.

Europe held 27% of the global market share in 2024, with Germany, the UK, and France driving the majority of adoption. Regulatory pressure from the EU’s AI Act has accelerated demand for explainable AI APIs, particularly in financial compliance and government services. Sustainability initiatives and data localization requirements further strengthen adoption. Enterprises are actively deploying APIs for fraud detection, supply chain visibility, and consumer engagement. SAP has introduced AI API integrations focused on enterprise resource planning, boosting efficiency for manufacturing clients. Consumer adoption patterns reveal heightened preference for transparent, explainable AI services, with more than 55% of European businesses prioritizing compliance-focused API integration in 2024.

Asia-Pacific represented 23% of the market volume in 2024, ranking as the fastest-growing region. China, India, and Japan are the top consuming countries, driven by strong e-commerce ecosystems, manufacturing automation, and rapid adoption of mobile AI applications. Major innovation hubs such as Shenzhen, Bengaluru, and Tokyo are spearheading the development of AI-powered APIs across education, retail, and fintech. Baidu and Infosys have launched region-specific AI APIs for language processing and customer experience platforms. Regional consumer behavior reflects high adoption of mobile-first AI applications, with over 62% of digital consumers in China using AI-powered services in e-commerce and fintech daily.

South America accounted for 7% of the market share in 2024, with Brazil and Argentina as primary growth drivers. The demand is largely influenced by fintech innovation, media localization, and e-commerce integration. Governments are incentivizing digital transformation projects, with Brazil allocating dedicated funding for AI integration across public services. Local players, such as TOTVS in Brazil, are developing AI APIs for business automation and ERP systems. Consumer behavior highlights rising demand for language localization APIs, with over 45% of media platforms deploying AI-powered captioning and translation tools to better serve diverse populations.

The Middle East & Africa captured 5% of the global market in 2024, with the UAE, Saudi Arabia, and South Africa driving expansion. Regional demand is strongly tied to digital transformation in oil & gas, construction, and smart city initiatives. Governments are investing heavily, with the UAE’s AI strategy focusing on API-enabled platforms for urban planning and mobility. Local companies are deploying APIs for Arabic language processing, expanding regional adoption in education and customer service. Consumer behavior indicates high interest in fintech APIs, with over 40% of enterprises in the region integrating AI APIs to enhance digital payment systems and fraud prevention.

United States – 28% Market Share: Strong dominance due to high enterprise adoption across healthcare, finance, and retail, supported by robust R&D investment and advanced cloud infrastructure.

China – 21% Market Share: Leadership driven by large-scale deployment in e-commerce, manufacturing, and mobile AI applications, backed by significant government and private sector investment.

The AI API Market exhibits a moderately consolidated structure with over 120 active global competitors, encompassing technology giants, specialized AI startups, and enterprise-focused API solution providers. The top five companies—Microsoft, Amazon Web Services, Google Cloud, IBM, and OpenAI—collectively hold approximately 62% of the market, reflecting both dominance and competitive fragmentation in specialized niches. Strategic initiatives are shaping the competitive landscape, including cross-industry partnerships, product launches, and acquisitions targeting AI integration in cloud platforms, financial analytics, healthcare, and retail automation. For instance, Microsoft recently expanded its Azure AI API offerings with enhanced natural language processing and computer vision tools, while Google Cloud introduced multimodal AI APIs enabling cross-channel customer engagement. Innovation trends influencing competition include generative AI APIs, edge AI deployment, explainable AI, and multimodal integration. Additionally, more than 58% of medium and large enterprises globally are actively piloting AI APIs, increasing pressure on companies to innovate rapidly. Strategic mergers and licensing collaborations further strengthen competitive positioning, as vendors seek to enhance scalability, security, and domain-specific customization across diverse industry applications.

IBM

OpenAI

SAP

Oracle

Salesforce

Baidu

Infosys

Technological innovation is central to the AI API Market, with rapid developments in natural language processing, computer vision, multimodal AI, and generative AI shaping enterprise adoption. Vision-language APIs now account for over 42% of type-based deployments, while audio-text and video-language APIs collectively represent 55%, enabling real-time analytics and automated content generation. Edge AI integration is emerging strongly, with more than 40% of enterprises leveraging local processing to reduce latency and improve data security. Explainable AI APIs are gaining traction, with 44% of businesses implementing transparent models to meet regulatory compliance and enhance trust. Advances in MLOps platforms are streamlining the deployment, monitoring, and management of AI APIs across cloud, hybrid, and on-premises environments. Specialized industry APIs in healthcare, fintech, and retail are driving domain-specific automation, such as predictive diagnostics, fraud detection, and personalized customer engagement. Recent innovations also include API orchestration platforms enabling seamless cross-functional integration and improved workflow efficiency, with measurable reductions in manual processing time by up to 35%. These technologies collectively reinforce the AI API Market as a critical enabler of scalable, secure, and innovative enterprise intelligence.

In March 2023, Google Cloud launched Vertex AI multimodal APIs, integrating image, text, and speech recognition, enabling enterprises to process over 5 million queries per day across customer support platforms. Source: www.cloud.google.com

In August 2023, Microsoft introduced Azure OpenAI Service expansions, providing GPT-based API capabilities to more than 1,200 enterprise clients for natural language processing and automated documentation. Source: www.microsoft.com

In February 2024, AWS unveiled Amazon Bedrock API services, allowing businesses to deploy foundation models without managing infrastructure, supporting over 500 enterprise AI workflows globally. Source: www.aws.amazon.com

In November 2024, OpenAI released GPT-4 Turbo APIs for real-time translation and semantic search, enabling multinational organizations to handle over 200 million multilingual interactions monthly. Source: www.openai.com

The scope of the AI API Market Report encompasses an in-depth evaluation of product types, applications, end-users, and regional dynamics to provide a comprehensive understanding of market evolution. It examines the deployment of vision-language, audio-text, video-language, and other specialized AI APIs across industries such as healthcare, financial services, retail, education, manufacturing, and logistics. The report evaluates adoption patterns in North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting technological innovation, regulatory compliance, and infrastructure readiness. It further covers emerging technologies including edge AI, multimodal APIs, generative AI, and explainable AI, illustrating their impact on operational efficiency, data security, and user engagement. Investment patterns, funding trends, and strategic initiatives such as mergers, product launches, and partnerships are also within scope.

Additionally, the report provides insights on consumer adoption behavior, industry-specific use cases, and innovation trajectories, alongside emerging niche segments like AI-driven ERP APIs, telemedicine platforms, and e-commerce personalization. By integrating technology, application, and regional perspectives, the report offers actionable intelligence for decision-makers seeking to navigate growth opportunities, optimize deployments, and anticipate future market trends in the AI API ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,311.0 Million |

| Market Revenue (2032) | USD 30,889.5 Million |

| CAGR (2025–2032) | 32.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Microsoft, Amazon Web Services, Google Cloud, IBM, OpenAI, SAP, Oracle, Salesforce, Baidu, Infosys |

| Customization & Pricing | Available on Request (10% Customization is Free) |