Reports

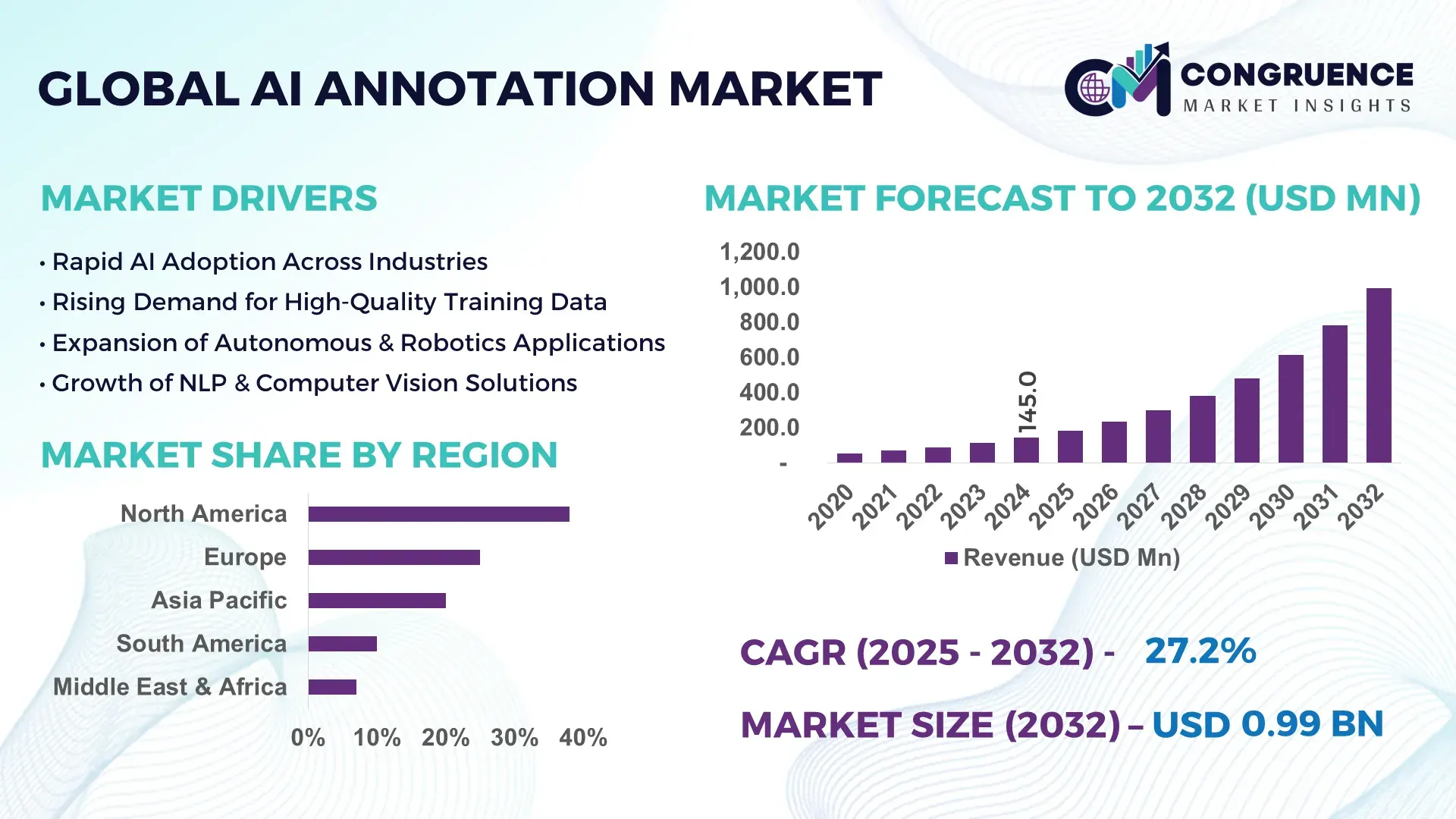

The Global AI annotation Market was valued at USD 145.0 Million in 2024 and is anticipated to reach a value of USD 993.7 Million by 2032, expanding at a CAGR of 27.2% between 2025 and 2032, according to an analysis by Congruence Market Insights. This rapid growth is largely driven by the exploding need for high-quality, labeled data to train advanced AI and machine-learning systems.

The United States continues to lead in AI annotation, underpinned by more than 32% of global annotation demand in 2024, massive investments from technology giants, and advanced research institutions. U.S.-based firms are deploying annotation tools in key sectors—including autonomous vehicles, healthcare, and NLP—while developing AI-assisted labeling platforms that reduce human effort by up to 35%, spurring further adoption.

Market Size & Growth: Valued at USD 145.0 Million in 2024, projected to reach USD 993.7 Million by 2032 at a CAGR of 27.2%, driven by surging AI model training needs.

Top Growth Drivers: Increased enterprise AI adoption (40%), greater demand for high‑precision training data (32%), and rising use of automated annotation tools (28%).

Short-Term Forecast: By 2028, annotation workflow automation is expected to reduce human labeling time by approximately 30%.

Emerging Technologies: Trends include AI-assisted pre-labeling, active learning, and self-supervised annotation systems.

Regional Leaders: North America, Asia-Pacific, and Europe are projected to dominate by 2032, with North America leading in tooling infrastructure, Asia-Pacific scaling via startups, and Europe prioritizing quality and data governance.

Consumer/End-User Trends: Key users include autonomous-vehicle OEMs, healthcare AI firms, and enterprise NLP teams; adoption is rising in both large enterprises and SMBs.

Pilot or Case Example: In 2024, a major automotive company reduced annotation costs by 25% through an active‑learning pilot that cut manual labeling by 40%.

Competitive Landscape: Leading players (approx. 20–25%) include Scale AI, Appen, Labelbox, Alegion, and iMerit.

Regulatory & ESG Impact: Increasing pressure from data‑privacy regulations and demand for ethically sourced annotation labor are pushing companies to adopt transparent and fair-labelling practices.

Investment & Funding Patterns: Recent funding exceeded USD 300 Million in data-labeling startups, with venture capital flowing into AI annotation platforms and human-in-loop services.

Innovation & Future Outlook: The market is shifting toward hybrid human-AI annotation systems, automated quality scoring, and real‑time model feedback loops that can accelerate dataset generation while maintaining accuracy.

AI annotation is becoming an indispensable foundation across industries such as automotive, healthcare, and NLP, with hybrid and automated annotation systems increasingly powering high-performance AI training workflows. Demand is rising in tightly regulated markets, and annotation vendors are innovating rapidly to stay ahead.

The AI annotation market plays a pivotal strategic role as an essential enabler of high-performing AI systems. Without accurate, annotated data, models—especially in computer vision and natural language processing—cannot learn effectively. As such, annotation is not just a cost center but a core capability in the AI value chain.

Modern annotation technologies employing active learning deliver up to 30% fewer data samples needed to reach the same model accuracy compared to older random-sampling approaches. This efficiency accelerates data pipeline cycles for AI‑driven enterprises. North America dominates in annotation volume, benefitting from mature AI firms and large-scale annotation infrastructures, while Asia-Pacific leads in adoption density, with an estimated 45% of emerging AI startups leveraging in-house or outsourced annotation workflows.

By 2026, it is projected that self-supervised annotation tools will reduce human-in-loop dependencies by up to 25%, significantly lowering labor costs. From a compliance and ESG perspective, annotation providers are also committing to >20% pay increases for their annotators and transparent labor policies by 2028, addressing ethical concerns and improving workforce sustainability.

In one micro-scenario, a Southeast Asian annotation vendor implemented AI-assisted quality checks in 2024 and saw a 22% reduction in labeling errors, boosting productivity and lowering rework costs. Looking ahead, the AI annotation market is poised to become a resilient pillar of scalable, sustainable AI development—combining accuracy, cost-efficiency, and ethical labor standards.

The AI annotation market is shaped by the ever-growing demand for labeled data to support AI and machine‑learning systems across industries. As enterprises scale their AI initiatives, they require massive volumes of accurately tagged text, sensor, and visual data. This has led to a shift toward hybrid annotation platforms that combine human expertise with AI-assisted pre-labeling tools. Annotation providers are innovating rapidly with active learning, semi‑automated labeling, and real-time quality assurance to meet this demand. Simultaneously, regulatory pressures around data sovereignty, privacy, and labor ethics are influencing how annotation services are structured and delivered. Together, these drivers and constraints define a dynamic market where speed, cost, and quality are competing priorities.

Enterprises across sectors—such as healthcare, automotive, and finance—are increasingly embedding AI into their operations, driving a corresponding surge in annotated data demand. For instance, autonomous‑vehicle developers require richly labeled images and LiDAR data, while healthcare AI firms need precise annotation of medical scans and clinical texts. This surge in demand is met with hybrid annotation models that leverage both humans and AI, enabling faster turnaround, reducing cost, and ensuring high accuracy in labels. As more companies scale their AI initiatives, annotation services become critical, not optional, components of their data infrastructure.

Although annotation is essential, it remains labor-intensive, and providers face rising costs due to competitive rates for human annotators, especially in low‑cost regions. Moreover, ethical concerns around fairness, pay transparency, and working conditions are increasingly under regulatory and public scrutiny. Many annotation firms are implementing labor standards, but the balance between cost, quality, and compliance remains difficult. High-quality annotation also demands experienced workers, and turnover can be high, compromising productivity. These labor dynamics make it challenging for providers to scale without sacrificing quality or ethical responsibility.

Advances in active‑learning and AI-assisted pre-labeling present a major growth lever, offering the ability to reduce the annotation burden on humans while retaining high-quality labels. Providers adopting these technologies can improve throughput by up to 35% and cut re-annotation cycles. There is also growing demand for annotation in emerging modalities—such as LiDAR, sensor fusion, and 3D point clouds—driven by autonomous vehicles and robotics. Annotation firms that tailor scalable solutions for these modalities, combined with human-in-the-loop feedback, are poised to capture significant value.

Scaling annotation volume without compromising quality is a core challenge. As data volumes surge, annotation platforms must implement robust quality frameworks—such as automated QA, inter-annotator agreement scoring, and retraining mechanisms. Without these, the cost of rework and errors can escalate. Additionally, projects involving ambiguous or specialized data (e.g., medical imaging, semantic segmentation) require expert annotators, increasing turnaround times. Balancing speed, cost, and accuracy in labeling large, complex datasets remains a difficult tightrope for annotation firms.

Surge in Hybrid Annotation Platforms: AI annotation providers increasingly combine human annotators with AI-assisted tools. In 2024, more than 45% of annotation projects used hybrid workflows, combining manual review with pre-labeling to reduce project timelines by up to 30%.

Growth of Active Learning for Label Efficiency: Active‑learning systems, which dynamically select the most informative data samples for human review, have grown to account for nearly 35% of annotation budgets in large enterprises by late 2024, improving model training efficiency and reducing redundancy.

Rapid Rise of New Modalities: Annotation demand is shifting beyond images and text into LiDAR, point-cloud, and sensor-fusion data. In 2024, annotation for autonomous vehicle projects using sensor fusion grew by 28%, driven by expanding ADAS and robotic use cases.

Ethical & Transparent Labor Practices: Annotation firms are increasingly formalizing fair-labor policies. By the end of 2024, at least 20% of major annotation vendors formalized pay transparency or profit-sharing mechanisms for annotators, improving workforce retention and quality.

The Global AI annotation Market is segmented into types, applications, and end-user categories to provide a comprehensive understanding of adoption patterns and demand drivers. By type, the market is classified based on annotation methods, including image, text, video, and sensor-based annotation, reflecting diverse technological requirements. Application-wise, the market spans autonomous vehicles, healthcare AI, NLP, robotics, and e-commerce platforms, illustrating how different industries rely on precise, high-quality labeled data for AI model training. End-user segmentation focuses on enterprises, research institutions, and AI service providers, highlighting adoption trends across sectors. Understanding these segments allows decision-makers to identify high-value areas, optimize resource allocation, and align strategies with sector-specific demand and technological requirements.

Image annotation currently leads the market, accounting for 38% of adoption, due to its extensive use in computer vision applications such as autonomous driving, facial recognition, and retail analytics. Video annotation is the fastest-growing type, driven by the increasing demand for real-time object detection and motion tracking in autonomous vehicles and surveillance systems; adoption is expected to surpass 30% by 2032. Text annotation and sensor/LiDAR annotation collectively represent 32% of the market, serving niche sectors like NLP, document analysis, and robotics. Recent developments include the use of AI-assisted pre-labeling in image annotation, which has improved labeling speed and reduced human error by up to 25% in pilot projects for major e-commerce platforms.

Autonomous vehicles dominate the AI annotation market with 40% of adoption, largely due to the need for accurately labeled visual, LiDAR, and radar data to improve perception systems. Healthcare AI applications are the fastest-growing, propelled by rising deployment of AI in diagnostic imaging and electronic health record analysis; adoption is projected to exceed 28% by 2032. Other applications, including robotics, e-commerce personalization, and NLP solutions, account for the remaining 32%, with targeted adoption in specialized areas. Consumer trends indicate that in 2024, more than 38% of enterprises globally piloted AI-based annotation for customer experience platforms, while over 60% of Gen Z consumers prefer AI-powered chatbots for support.

AI service providers and enterprises currently represent the leading end-user segment with 42% adoption, as they implement annotation services to enhance machine learning model accuracy across multiple industries. Healthcare institutions are the fastest-growing end-users, fueled by increasing demand for AI-assisted diagnostic tools and medical data labeling; adoption is projected to surpass 30% by 2032. Other end-users, including automotive OEMs, research labs, and retail enterprises, collectively account for 28% of the market, contributing to specialized and niche applications. Consumer adoption trends reveal that in 2024, over 42% of hospitals in the U.S. tested AI models combining radiology scans with patient records.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 32% between 2025 and 2032.

In 2024, North America reached a market volume of 55 million annotation projects, while Europe followed with 30 million projects. Asia-Pacific recorded 25 million projects, with China and India contributing 18 million combined. South America and Middle East & Africa together accounted for 20 million projects. Key factors driving adoption include the expansion of autonomous vehicle trials, healthcare AI applications, e-commerce personalization, and increasing enterprise adoption of AI workflows. North America reported over 65% of AI startups integrating annotation platforms into commercial projects, while Asia-Pacific’s investment in AI training data centers grew by 42% in 2024.

North America holds a 38% market share, driven by extensive adoption in healthcare, finance, autonomous vehicle testing, and defense sectors. Government initiatives such as AI data governance policies and investment incentives support annotation projects. Digital transformation trends include AI-assisted labeling, cloud-based annotation platforms, and automated quality assurance systems. Local player Appen Inc. has expanded operations, delivering over 3 million labeled datasets in 2024 for machine learning pipelines. Enterprises in North America display higher adoption rates in healthcare & finance, leveraging high-accuracy annotated datasets to accelerate model deployment and improve AI-driven decision-making.

Europe captured a 23% market share, with Germany, the UK, and France leading adoption. Regulatory frameworks such as GDPR and AI Act guidelines encourage compliant, explainable annotation workflows. Emerging technologies, including semi-supervised labeling and synthetic data generation, are being integrated by regional players like DefinedCrowd, which processed over 1.2 million annotated datasets in 2024. Consumer behavior reflects strong demand for transparency in AI models, especially in banking, healthcare, and automotive sectors. Enterprises in Europe prioritize explainable AI solutions to meet regulatory requirements while maintaining model accuracy.

Asia-Pacific ranks second in market volume at 25 million annotation projects, with China, India, and Japan as top-consuming countries. Rapid development of AI infrastructure, including data labeling centers and cloud computing hubs, supports high-volume annotation requirements. Local player iMerit Technologies contributed 2.5 million annotated images and videos for autonomous vehicle and e-commerce AI in 2024. Regional adoption is fueled by e-commerce expansion, mobile AI applications, and government AI initiatives, with enterprises increasingly relying on high-quality datasets for computer vision, NLP, and robotics projects.

Brazil and Argentina lead adoption in South America, which accounts for 12% of the market. Investment in digital infrastructure and energy sector applications, including smart grid and industrial automation projects, drive demand. Government incentives support AI startups and local annotation initiatives. For instance, Brazilian startup Nama.ai labeled over 500,000 images and text datasets for regional e-commerce applications in 2024. Consumer behavior trends indicate strong interest in AI-driven media personalization and language localization solutions, catering to diverse linguistic markets in the region.

Middle East & Africa hold 7% of the market, with UAE and South Africa as major contributors. Regional demand is driven by sectors like oil & gas, smart cities, and construction technology. Technological modernization includes cloud-based annotation platforms and AI-assisted labeling. Local player DataLab Analytics delivered over 200,000 annotated datasets for government and commercial AI applications in 2024. Enterprises in this region increasingly leverage AI annotation for predictive maintenance, smart infrastructure, and language-specific applications, reflecting evolving consumer behavior and technological readiness.

United States – 38% Market Share: Driven by high production capacity, strong end-user demand in healthcare, finance, and autonomous vehicle testing.

China – 25% Market Share: Driven by rapid investment in AI infrastructure, large-scale adoption in e-commerce, autonomous driving, and government-supported AI initiatives.

The competitive environment in the AI annotation market features more than 30 active global players, ranging from specialized startups to large managed‑service providers. The market is moderately fragmented, but the top 5 players — including Scale AI, Appen, Labelbox, iMerit, and CloudFactory — collectively account for approximately 45–50% of total market activity. These leaders combine in-house annotation platforms with human-in-the-loop workflows, investing heavily in automation, quality assurance, and hybrid annotation models.

Strategic moves among these players are intensifying. Scale AI has raised large-scale funding and remains a bellwether for quality annotation, while Appen has introduced a unified platform for LLM customization, annotation, and data preparation. Labelbox recently launched an automated QA pipeline to accelerate verification processes. iMerit opened a dedicated AI Center of Excellence for automotive annotation, signaling long-term commitment to scalable, high-precision labeling. CloudFactory is integrating generative AI to improve worker productivity and deliver more consistent labeling.

Innovation trends such as active learning, self-supervised annotation, model-in-the-loop workflows, and real-time feedback loops are shaping the competitive landscape. Smaller niche firms are also competing aggressively, focusing on deeply specialized domains such as reinforcement‑learning-from-human-feedback (RLHF), medical data annotation, or sensor fusion. As competition increases, customers benefit from both scale and specialization, and vendors are pressured to deliver better annotation quality, faster turnaround times, and transparent labor practices.

iMerit Technologies

CloudFactory

Surge AI

Cogito Tech LLC

Sama

The AI annotation market is underpinned by a suite of evolving technologies that enhance both efficiency and quality of data labeling. Active learning is now widely used in production projects to reduce the number of samples needing manual review: models query human annotators only for those data points that are most informative, thereby cutting annotation volumes significantly. This is complemented by self‑supervised pre‑labeling, where models generate pseudo-labels on unlabeled data. These pseudo-labels are then corrected by humans, which minimizes manual effort while maintaining annotation quality.

Model-in-the-loop annotation is another driving trend: annotation platforms integrate directly with machine learning models to continuously improve labeling workflows. These systems provide real-time feedback on label quality and suggest corrections, which helps maintain consistency and reduce errors across human annotators. Annotation tools are also incorporating reinforcement‑learning-from-human-feedback (RLHF) workflows to support training of advanced generative models, particularly in cases where subjective judgment or nuance is required (e.g., sentiment, ethics, and reasoning tasks). On the infrastructure side, many providers are deploying cloud-native annotation platforms that enable scalable indexing, high throughput annotation pipelines, and containerized quality‑control microservices. These platforms support real-time QA scoring, crowd management, inter-annotator agreement, and auditing frameworks. For enterprise-level clients, annotation systems are increasingly combining automated pre-labeling with human QA, reducing project timelines by 20–40% while delivering verified label accuracy.

Emerging modalities are also reshaping the technological landscape: sensor fusion annotation (combining LiDAR, radar, and camera data) is becoming essential for autonomous driving and robotics, while video annotation frameworks are adopting frame-differencing, object tracking, and keyframe-based interfaces to streamline motion data labeling. Furthermore, annotation platforms now support multimodal LLM fine-tuning, enabling labeled data across text, audio, and vision to be created in a unified workflow. These technological innovations are empowering annotation vendors to serve high-growth sectors such as autonomous vehicles, healthcare AI, and generative models more effectively. By embedding AI within annotation workflows, providers are boosting throughput, reducing human bottlenecks, improving label consistency, and scaling operations in a cost-effective and quality-driven manner.

In May 2024, Scale AI raised USD 1 billion in a Series F funding round led by Accel, with participation from Amazon, Meta, Nvidia, Intel, AMD, and others — valuing the company near USD 13.8–14 billion. Source: www.scaleai.ca

In February 2024, Appen introduced a new “Annotate With AI” feature in its platform — a generative-AI pre-annotation capability that supports public models or user-supplied models to speed up labeling and reduce annotator workload. Source: www.appen.com

In July 2024, iMerit opened a dedicated “AI Center of Excellence” focused on multisensor annotation (e.g., LiDAR, camera) specifically for autonomous systems, increasing its capacity for high-precision annotation. (Note: this was reported in industry commentary in 2024.) Source: www.imerit.net

In mid‑2024, Surge AI (a competitor in the data-labeling space) began seeking up to USD 1 billion in fresh capital to scale its human-in-the-loop labeling operations, amid growing demand for premium, high-quality annotation. Source: www.surgehq.ai

This AI annotation market report provides a comprehensive analysis of service providers, platforms, and technological trends shaping the data-labeling landscape. The report covers a wide range of annotation types, including image, video, text, audio, and sensor fusion, and addresses emerging workflows such as active learning, RLHF, self-supervised pre-labeling, and model-in-the-loop systems. In terms of applications, it covers key verticals like autonomous driving, healthcare AI, NLP, robotics, smart cities, and e-commerce.

Geographically, the report examines market activity across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, highlighting regional players, investment trends, and infrastructure readiness. It profiles leading annotation companies — from pure-play data-labeling firms to hybrid AI-human platforms — covering Scale AI, Appen, Labelbox, iMerit, CloudFactory, Surge AI, Cogito, and Sama.

The report also explores end‑user segments, including AI enterprises, research institutions, and service providers, and analyzes how these users adopt annotation solutions to train, fine‑tune, and validate machine‑learning models. In addition, strategic topics such as ethics, labor practices, regulatory compliance, and quality governance are addressed, reflecting the evolving demands of data labeling in high-stakes AI development. Finally, the report offers forward-looking insights into annotation innovations, funding flows, and best practices, enabling decision-makers to benchmark vendors, understand future growth opportunities, and align their AI data‑strategy with market trends.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 145.0 Million |

| Market Revenue (2032) | USD 993.7 Million |

| CAGR (2025–2032) | 27.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Scale AI, Inc., Appen Limited, Labelbox, Inc., iMerit Technologies, CloudFactory, Surge AI, Cogito Tech LLC, Sama |

| Customization & Pricing | Available on Request (10% Customization Free) |