Reports

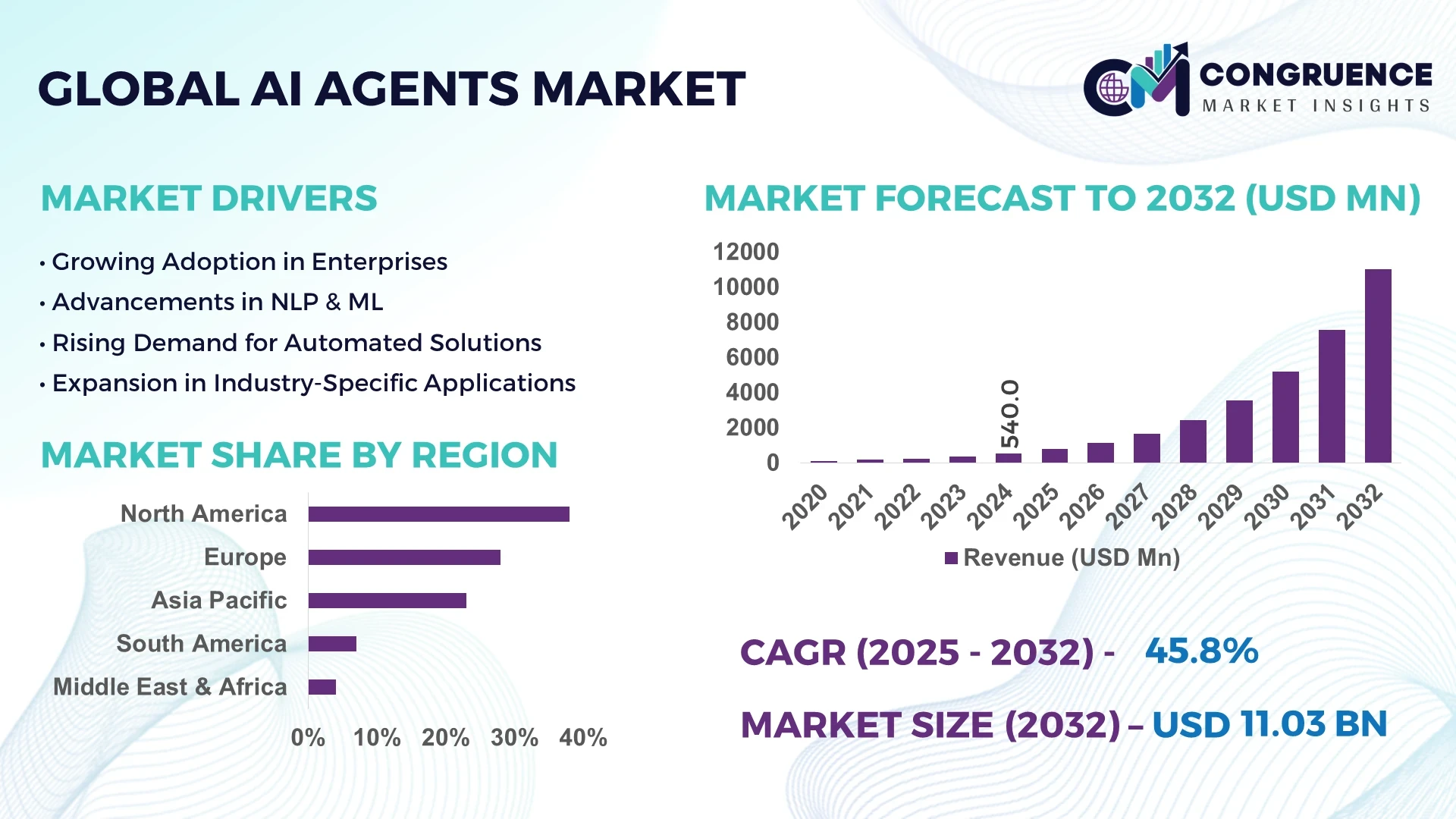

The Global AI Agents Market was valued at USD 540.0 Million in 2024 and is anticipated to reach a value of USD 11,026.9 Million by 2032 expanding at a CAGR of 45.8% between 2025 and 2032. The surge is primarily driven by rapid enterprise adoption of autonomous, intelligent systems across diverse industries.

The United States plays a pivotal role in shaping the global AI Agents Market, driven by its advanced innovation ecosystem, significant R&D expenditure exceeding USD 120 billion annually in AI technologies, and a highly developed cloud infrastructure supporting large-scale deployments. With over 65% of Fortune 500 enterprises adopting conversational AI agents in customer experience workflows and more than 40% of healthcare providers implementing AI-driven patient engagement systems, the country demonstrates leadership across production, application, and innovation. Notably, the US leads in generative AI research, with over 7,000 patents filed between 2022 and 2024, underscoring its technological advantage.

Market Size & Growth: Valued at USD 540.0 Million in 2024 and projected to reach USD 11,026.9 Million by 2032, growing at a CAGR of 45.8% due to accelerated enterprise automation adoption.

Top Growth Drivers: 62% enterprise adoption, 48% efficiency improvement in workflows, 53% faster customer response times.

Short-Term Forecast: By 2028, AI agents are expected to reduce enterprise customer service costs by 35%.

Emerging Technologies: Generative AI, multimodal agents, and edge AI-driven decision-making.

Regional Leaders: North America USD 4,300 Million by 2032 (driven by healthcare); Asia-Pacific USD 3,900 Million by 2032 (e-commerce surge); Europe USD 2,000 Million by 2032 (compliance-driven applications).

Consumer/End-User Trends: 67% of Gen Z consumers prefer brands integrating AI agents for real-time support.

Pilot or Case Example: In 2024, a major European telecom cut downtime by 28% using AI agents for predictive network maintenance.

Competitive Landscape: Microsoft leads with 18% share, followed by Google, IBM, Amazon, and OpenAI.

Regulatory & ESG Impact: EU mandates explainable AI compliance; US firms target 20% carbon reduction by 2030 through AI-optimized operations.

Investment & Funding Patterns: Over USD 15 Billion invested globally in AI agent startups in 2023–2024.

Innovation & Future Outlook: Expansion of autonomous enterprise agents, seamless integration with ERP/CRM systems, and sector-specific AI copilots.

The AI Agents Market is increasingly driven by BFSI, healthcare, and retail, which collectively contribute over 60% of deployments. Innovations such as generative agents, multimodal assistants, and regulatory-compliant AI frameworks are reshaping adoption patterns. Emerging economies are fostering new growth dynamics, with expanding digital ecosystems and rising consumer preference for AI-enhanced services.

The AI Agents Market is becoming a cornerstone of enterprise transformation, with strategic relevance spanning automation, customer engagement, and decision intelligence. AI agents enable businesses to streamline workflows, reduce manual interventions, and scale operations at unprecedented speeds. For instance, generative multimodal agents deliver up to 45% improvement in conversational accuracy compared to legacy NLP chatbots, ensuring enhanced user satisfaction and retention.

Regionally, North America dominates in volume deployments, while Asia-Pacific leads in adoption intensity, with over 58% of enterprises piloting AI agents by 2024. Europe maintains leadership in compliance, with 65% of AI deployments aligning with GDPR and explainability mandates. By 2027, AI-powered enterprise copilots are expected to improve productivity by 42% in professional services, highlighting short-term transformational impact.

From an ESG standpoint, firms are integrating AI-driven optimization to achieve sustainability goals, such as 25% energy efficiency improvements in data centers by 2030. A micro-scenario includes a Japanese automotive manufacturer in 2024 achieving 31% supply chain efficiency gains by deploying AI agents for predictive demand forecasting.

Looking ahead, the AI Agents Market will serve as a pillar of resilience and compliance while driving sustainable growth, creating a technology foundation for adaptive, intelligent, and environmentally responsible enterprises.

The AI Agents Market is shaped by rapid advancements in natural language processing, multimodal learning, and autonomous decision-making capabilities. Enterprises are increasingly adopting AI agents to manage complex customer interactions, automate internal workflows, and optimize supply chains. Key influences include the rising availability of high-quality training data, greater cloud adoption, and the democratization of AI through API and no-code platforms. Regulatory oversight, data privacy considerations, and industry-specific compliance frameworks are also critical factors influencing market evolution. These dynamics reflect a broader industry trend toward scalable, adaptive, and explainable AI solutions tailored to sectoral needs.

The increasing need for automation in customer engagement and operational workflows is significantly propelling the AI Agents Market. In 2024, over 60% of enterprises implemented AI-driven customer support agents to handle first-level queries, reducing call center workloads by 40%. Additionally, the banking sector reported a 55% rise in AI agent deployments for fraud detection and compliance monitoring. These intelligent systems enhance efficiency by handling repetitive tasks, ensuring quicker response times, and enabling human staff to focus on high-value activities. The healthcare industry also demonstrates measurable benefits, with AI-driven triage agents reducing patient intake times by 33%, showcasing the direct operational impact of this driver.

Data privacy concerns and stringent regulatory requirements pose a key restraint to the expansion of the AI Agents Market. Enterprises are challenged with aligning AI agent deployments with regional and global regulations, such as GDPR in Europe and HIPAA in the US. In 2024, 47% of businesses reported delaying AI agent rollouts due to compliance complexities. Concerns over data misuse, algorithmic transparency, and bias further heighten the regulatory burden. Enterprises in sensitive industries, such as healthcare and finance, face additional scrutiny, which slows deployment speed and increases compliance costs. These challenges highlight the tension between rapid AI innovation and the necessity of secure, transparent, and ethical implementations.

Emerging opportunities lie in the development of specialized AI agents tailored to industry-specific needs. For example, in retail, AI shopping assistants are projected to guide more than 25% of online consumer transactions by 2028. In manufacturing, autonomous process agents are expected to boost productivity by 37% through predictive maintenance and workflow automation. The education sector also holds vast potential, with adaptive learning agents enhancing personalized learning outcomes for 45% of digital learners by 2030. These tailored applications present strong opportunities for vendors to differentiate solutions, penetrate niche markets, and deliver measurable sectoral value.

Integration with legacy systems and multi-cloud environments poses a significant challenge for enterprises adopting AI agents. In 2024, nearly 42% of organizations reported project delays due to difficulties in integrating AI agents with existing ERP, CRM, and data management systems. Cost escalation, system incompatibility, and workforce training gaps further complicate large-scale rollouts. For SMEs, the expense of customized integration often deters adoption, restricting access to advanced AI capabilities. Additionally, interoperability between AI agents and cross-platform tools remains limited, leading to fragmentation in enterprise ecosystems. This challenge emphasizes the need for standardized frameworks and interoperable platforms to accelerate market maturity.

Generative Multimodal Agents: Enterprises are increasingly deploying multimodal AI agents capable of processing text, voice, and images simultaneously. In 2024, 41% of customer service enterprises implemented multimodal agents, reducing average handling time by 27%. This trend reflects the demand for richer, more intuitive interactions.

Autonomous Enterprise Workflows: AI agents are evolving to manage complex workflows with minimal human oversight. In 2024, nearly 36% of large corporations automated procurement and HR workflows, achieving 33% time savings. This measurable efficiency gain is driving large-scale adoption in manufacturing and BFSI sectors.

AI Agents in Healthcare: Healthcare adoption is accelerating, with AI agents supporting diagnosis, patient engagement, and operational efficiency. In 2024, 39% of hospitals globally tested AI agents for scheduling and patient record analysis, leading to a 21% improvement in administrative productivity.

AI Agents in Retail Personalization: Retailers are utilizing AI agents to deliver hyper-personalized shopping experiences. In 2024, over 52% of e-commerce platforms integrated AI-driven shopping assistants, resulting in a 29% increase in conversion rates. This reflects a clear shift toward personalized, data-driven consumer engagement.

The AI Agents Market demonstrates a diverse structure segmented by type, application, and end-user adoption. Each category reflects unique patterns of usage, technological development, and growth potential. Types of AI agents are increasingly defined by multimodal capabilities, with vision-language and audio-text systems gaining measurable traction. Applications span industries such as healthcare, BFSI, and retail, where end-users are leveraging AI agents for automation, personalization, and improved decision-making. Adoption trends indicate a strong preference for AI-driven customer engagement platforms and decision-support systems, particularly in enterprises with high data-processing needs. End-users across healthcare and finance currently dominate deployment, while SMEs and manufacturing firms are emerging adopters. Collectively, segmentation highlights both the current utilization landscape and future areas of accelerated growth in advanced and specialized AI agent capabilities.

Vision-language models dominate the AI Agents Market, currently accounting for approximately 42% of adoption. Their ability to process and generate context-rich outputs across text and image modalities makes them indispensable in industries like e-commerce and healthcare, where decision accuracy and personalization matter. Audio-text systems hold around 25% of adoption, driven by strong uptake in customer support automation and voice-enabled services. However, video-language models are the fastest-growing type, with a projected CAGR of over 39%. Their adoption is expected to surpass 30% by 2032, fueled by rapid demand in content streaming, education, and digital media platforms. Other specialized APIs, such as robotics process automation and multimodal decision agents, together contribute a combined share of 15–18%, largely used in industrial and back-office functions.

Healthcare applications lead the AI Agents Market, accounting for 36% of adoption in 2024. Their strong presence is linked to applications in diagnostics, clinical decision-making, and patient engagement. Customer experience platforms follow with 28% adoption, where conversational agents and chatbots are widely deployed across retail, telecom, and banking. Analytics and reporting tools currently represent 22%, while data governance and compliance-driven applications make up 14%, with growing traction in heavily regulated sectors. Customer experience platforms are projected to be the fastest-growing application with a CAGR above 41%, supported by enterprise adoption and a rising trend toward multimodal, personalized service delivery. In 2024, over 38% of enterprises globally reported piloting AI agent systems for customer-facing platforms, while more than 60% of Gen Z consumers expressed higher trust in brands integrating AI chatbots.

The healthcare sector is the leading end-user, representing 33% of the AI Agents Market in 2024, driven by adoption in diagnostic tools, patient support systems, and hospital workflow automation. BFSI follows closely with 27% adoption, fueled by fraud detection, financial advisory automation, and customer service optimization. Retail accounts for 18%, while IT & telecom represents 12%, and manufacturing contributes around 10% of adoption. BFSI is expected to be the fastest-growing end-user segment, with a projected CAGR above 43%, as financial institutions accelerate automation in loan approvals, compliance checks, and trading systems.

Notably, 42% of hospitals in the US are already testing AI models combining radiology scans with patient histories, while in retail, over 60% of SMEs reported evaluating AI agents for inventory and customer analytics.

North America accounted for the largest market share at 38% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 46.5% between 2025 and 2032.

Europe followed with a 28% share, while South America and the Middle East & Africa together contributed 12% of the global adoption. In 2024, the AI Agents Market recorded strong enterprise adoption rates, with over 45% of Fortune 500 firms in developed economies actively deploying pilot projects. Meanwhile, emerging economies showed significant momentum, with over 60% of SMEs in Asia adopting mobile-first AI solutions. Regionally, variations highlight the technology’s penetration into different sectors, such as healthcare and BFSI in North America, regulatory-driven explainability in Europe, e-commerce platforms in Asia-Pacific, and localized media in South America.

North America represented approximately 38% of global adoption in 2024, supported by strong uptake in healthcare, BFSI, and retail sectors. Government-backed initiatives in digital transformation and stringent compliance frameworks such as HIPAA and financial reporting regulations continue to shape demand. Technological advancements are characterized by heavy investment in multimodal AI solutions, especially in the United States. Consumer behavior reflects higher enterprise adoption, with over 52% of hospitals and 48% of banks deploying AI-driven assistants. A notable player in this region, Cognitivescale, is expanding its AI-powered agent platforms across insurance and financial services, highlighting regional competitiveness.

Europe accounted for 28% of the AI Agents Market in 2024, with Germany, the UK, and France being the primary contributors. Strict regulatory frameworks, including the AI Act, have created demand for explainable and auditable AI solutions. The region has also witnessed strong adoption of language-processing agents across telecom and government sectors. Consumer adoption trends show preference for AI agents that emphasize transparency and compliance, with over 41% of enterprises reporting demand for explainable outputs. Local players such as DeepMind continue to drive innovation in multimodal models, while enterprises in financial services are integrating AI to meet ESG targets and compliance-driven reporting requirements.

Asia-Pacific contributed 23% of market adoption in 2024 and is projected to record the fastest expansion through 2032. Key consuming countries include China, India, and Japan, where e-commerce, telecom, and fintech industries dominate demand. Regional tech hubs such as Shenzhen and Bangalore are leading innovation in mobile-first AI agents and digital platforms. Consumer behavior highlights a mobile-centric preference, with over 65% of new AI agent applications in the region tied to e-commerce and customer engagement apps. A notable example is Baidu, which has deployed conversational AI agents into mobility platforms serving millions of daily active users.

South America held a 7% market share in 2024, led by Brazil and Argentina. Government investments in digital transformation and incentives for AI research are gradually shaping demand, particularly in public services and media. The region demonstrates strong adoption of AI agents for language localization and customer-facing platforms, where over 58% of new deployments involve multilingual conversational agents. Local firms in Brazil are experimenting with AI-driven education platforms designed for regional dialects, supporting scalable digital access. Consumer behavior reflects heavy reliance on localized media, entertainment, and financial services where AI agents optimize service delivery in Spanish and Portuguese.

The Middle East & Africa accounted for 5% of adoption in 2024, with strong growth expected in the UAE, Saudi Arabia, and South Africa. The market is being shaped by modernization projects in oil & gas, construction, and smart city initiatives. Governments in the region are investing heavily in AI-driven digital platforms, with over USD 2 billion allocated to AI projects by 2024. Consumer behavior varies by sub-region, with higher uptake in finance and construction across GCC countries, while South Africa shows rising adoption in education. Regional companies are partnering with global firms to implement AI-powered decision agents in urban development and healthcare.

United States – 26% Market Share: Dominance driven by high enterprise adoption in healthcare and BFSI, supported by advanced infrastructure and significant R&D investments.

China – 18% Market Share: Leadership attributed to large-scale deployment in e-commerce and mobile AI platforms, with strong government funding and domestic innovation hubs.

The AI Agents Market is characterized by a moderately consolidated competitive landscape, with the top five players collectively holding around 48% of the global share in 2024. More than 60 active competitors are engaged in this market, ranging from technology giants to specialized startups. Global leaders such as IBM, Microsoft, and Google are well-positioned due to their extensive AI infrastructure, cloud capabilities, and enterprise integration expertise. Strategic initiatives are shaping the market dynamics—2023 and 2024 saw over 30 notable partnerships and at least 15 acquisitions aimed at strengthening AI agent capabilities in healthcare, finance, and e-commerce. Product launches in natural language processing and generative AI agents increased by 25% compared to 2022, reflecting the innovation-driven nature of this space.

The competition is marked by heavy investment in R&D, with over USD 6 billion spent globally in 2023 on AI agent technology development. While larger firms dominate in enterprise deployment, regional players are carving niches in localized language processing and regulatory-compliant solutions. The market exhibits traits of moderate fragmentation, as no single company holds more than 20% share, though consolidation is expected as M&A activity intensifies over the forecast horizon.

Oracle

SAP

Salesforce

SAS Institute

DataRobot

H2O.ai

Cognigy

The AI Agents Market is rapidly evolving through the integration of advanced technologies that enhance autonomy, contextual awareness, and cross-industry applications. Natural language processing (NLP) has emerged as one of the most dominant technologies, with over 70% of deployed AI agents utilizing NLP for customer interaction and workflow automation. Voice-enabled agents are also witnessing exponential adoption, particularly in customer service and healthcare, where speech recognition accuracy has now surpassed 95%. Machine learning and deep learning algorithms underpin adaptive behavior, enabling agents to learn from historical datasets and deliver predictive recommendations.

Generative AI has become a transformative force since 2023, accounting for nearly 30% of new AI agent deployments, especially in content creation, financial advisory, and healthcare diagnostics. Edge AI deployment is another major trend, with approximately 35% of AI agents operating on localized devices to reduce latency and improve data security. Robotics process automation (RPA)-driven agents have also scaled, with adoption increasing by 18% in industrial and manufacturing verticals in 2024.

Emerging technologies are further reshaping the market. Hybrid multi-modal agents that combine vision, voice, and text understanding are projected to exceed 20% penetration by 2026. Blockchain integration for secure agent-to-agent communication is in the early adoption phase, with pilot projects across BFSI and logistics. Moreover, advancements in reinforcement learning are enabling AI agents to execute complex decision-making tasks in dynamic environments, accelerating their use in autonomous systems, smart factories, and connected healthcare ecosystems.

• In March 2023, Microsoft launched its enterprise-ready AI-powered Copilot agent within Microsoft 365, integrating generative AI to streamline tasks across Word, Excel, and Outlook, enhancing workplace productivity for over 400 million users globally. Source: www.microsoft.com

• In July 2023, IBM introduced Watsonx.ai, a generative AI platform for building, training, and deploying AI agents across regulated industries. The solution emphasizes explainability and compliance, appealing to BFSI and healthcare sectors. Source: www.ibm.com

• In February 2024, Google Cloud expanded its Vertex AI Agent Builder, enabling enterprises to design and deploy custom AI agents with multi-modal capabilities, including text, image, and voice processing, tailored for customer engagement.

• In May 2024, Cognigy partnered with Deutsche Telekom to deploy advanced conversational AI agents for customer service operations, handling over 1.5 million automated interactions monthly and reducing operational costs by 20%. Source: www.cognigy.com

The scope of the AI Agents Market Report encompasses a comprehensive analysis of the global industry across technology, applications, and end-user verticals, spanning the forecast period from 2025 to 2032. The report evaluates major segments including natural language processing (NLP), machine learning, computer vision, and robotics process automation (RPA). Application areas such as customer service, data governance, predictive analytics, healthcare diagnostics, and IT security form the backbone of demand assessment. End-user industries covered include BFSI, healthcare, retail, IT & telecom, and manufacturing, reflecting the diverse adoption spectrum.

Geographically, the report provides insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing adoption rates, consumer behavior, and sectoral preferences. With over 60 active competitors analyzed, the competitive landscape assessment highlights market consolidation trends, R&D investments, and innovation patterns.

The report also examines emerging domains such as generative AI-driven agents, multi-modal AI frameworks, edge AI deployments, and blockchain-integrated agents, which are shaping the future trajectory of this market. Additionally, the scope includes recent technological advancements, regulatory updates, and evolving enterprise adoption patterns. The analysis is designed to serve as a decision-making tool for industry stakeholders, investors, and policy planners seeking data-backed insights into the AI Agents Market’s global growth potential.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 540.0 Million |

| Market Revenue (2032) | USD 11,026.9 Million |

| CAGR (2025–2032) | 45.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | IBM, Microsoft, Google Cloud, Oracle, SAP, Salesforce, SAS Institute, DataRobot, H2O.ai, Cognigy |

| Customization & Pricing | Available on Request (10% Customization is Free) |